This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

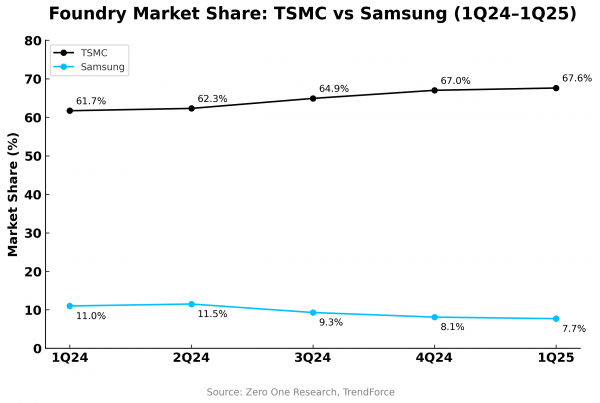

1. What TSMC’s 1Q25 Results Reveal About the Future of Chipmaking in the U.S. (Structural Long)

- TSMC’s Arizona Yield Success Silences Doubts: Management confirmed first U.S. fab has achieved yields comparable to Taiwan, validating global replication model and reinforcing alignment with U.S. clients like Apple, Nvidia.

- U.S. Buildout Anchoring TSMC’s Long-Term Dominance: With 30% of N2 and beyond capacity to be in USA, TSMC building footprint across fabs, packaging, and R&D competitors will struggle to match.

- Margins Resilient, AI Demand Accelerating: 1Q25 beat on AI strength despite smartphone softness and earthquake disruption. 2Q25E revenue guidance of +13% QoQ reflects continued momentum in advanced nodes and HPC.

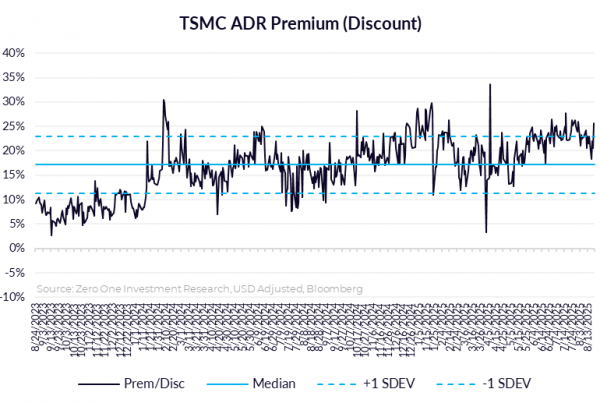

2. Taiwan Dual-Listings Monitor: TSMC Premium at Mid-Range; Short Interest Highs for ASE & IMOS

- TSMC: 16.5% Premium; Short Interest Remains Near Historical Highs for ADR and Local

- ASE: +2.2% Premium; Wait for Closer to Par Before Going Long; Short Interest in Local Shares at Highs

- ChipMOS: +1.1% Premium; Short Interest in Local Shares Hits New Highs

3. Faraday Technology’s Breakout: AI Packaging Demand Defying the Global Semiconductor Slowdown

- Faraday Top-Line Soars on CoWoS Chip Packaging Services Support Ramp — 78% of MP Revenue Came from AI/HPC Applications

- TSMC-Aligned Execution Enables Asset-Light Business Scaling for Faraday — New Fabless OSAT Service is Highly Differentiated; Competitive Advantage

- Outlook: Continued Very Strong Momentum into 2Q25 — 1H25 Revenue Will Be Higher Than All of 2024

4. SK Hynix Earnings Highlights Strong AI Dependence and Tariff Concerns

- SK hynix announced their second-highest revenue and operating profit for the first quarter of 2025

- Much of the company’s performance is the result of its first-mover advantage and excellent execution in the HBM market

- Two issues threaten the company: AI growth may stall, and tariff changes could interfere with the company’s global supply chain

5. Taiwan Tech Weekly: TSMC U.S. Bet Pays Off; UMC & Faraday Step Up Next; Latest Mobile Shipments Data

- TSMC’s Arizona fab hits Taiwan-level yields, easing replication concerns and reinforcing its global leadership across N2 and advanced packaging.

- AI demand offsets smartphone softness in 1Q25; TSMC guides +13% QoQ revenue for 2Q25 as margins hold firm despite tariff and earthquake headwinds.

- Faraday and UMC results ahead this week — Key readouts on Taiwan’s ASIC, mature node, and design service momentum amid U.S.-China tech decoupling.

6. Intel (INTC.US): Exploring a Tough Journey. (IV)

- After the new CEO, Mr. Lip-Pu Tan, took office at the chip giant Intel Corp (INTC US), he initiated a large-scale restructuring of the executive team and organization.

- Intel Corp (INTC US) to sell 51% share of Altera to Silver Lake, a global leader in technology investing. This deal is further to deal with non-performing assets.

- Now, the critical question is, who are the clients of Intel Corp (INTC US) IFS (Intel Foundry Service)?

7. UMC (2303.TT; UMC.US): 2Q25 Guidance Beat; Tariff Affection Unknown; No GF Merger Plan Right Now.

- 2Q25 guidance: Wafer shipments: increase 5~7%, ASP in USD: flat, GM: About 30%.

- The US tariffs affect customer outcome visibility in 2Q25 and 2H25 is limited.

- UMC is seeking a strategic plan to enhance shareholder value, and there is no ongoing merger plan at the moment, which implies no merger plan with GF.

8. UMC Sees Broad Rebound in Demand Ahead But Is Demand Being Pulled Forward by Tariffs?

- UMC guides for 2Q25 rebound, expecting 5–7% QoQ wafer shipment growth and margin recovery to ~30%, though 2H25 visibility remains low due to tariff and inventory uncertainty.

- Intel Corp (INTC US) 12nm project progressing; Initial client orders planned for 2026E, with management leaving the door open to future partnerships—including rumored GLOBALFOUNDRIES (GFS US) collaboration—amid strategic diversification efforts.

- Tariff-Driven pull-forward of orders IS happening but impact reportedly limited so far, with UMC noting mixed customer behavior; near-term demand strength appears broad-based. We have a Neutral rating for UMC.

9. Intel Q125 Earnings. Outlook Disappoints As LBT Shows Senior Executives The Door

- Intel reported Q125 revenues of $12.7 billion, down 0.4% YoY, down 11% QoQ but still $500 million above the guided midpoint, precisely the same beat as in the prior quarter.

- Looking ahead, Intel forecasted current quarter revenues of $11.8 billion at the midpoint, this time extending the range from $1 billion in the prior quarter to $1.2 billion

- LBT is in the process of undertaking sweeping changes to his ELT, flattening its structure, taking on multiple additional reports and showing many senior executives the door. That’s good.

10. Keyence (6861 JP): A Beneficiary of Rising Interest Rates

- Keyence stands to benefit from a rising return on its large holdings of cash and securities, which are also available for investment and higher dividends.

- The company’s engineering-service business model should keep gross and operating margins high while it continues to expand overseas.

- Projected valuations at the low end of their 5-year ranges. Recession and abrupt appreciation of the yen are the primary risks.