The Profits (And Perils) Of Independent Large Cap Research

The Profits (And Perils) Of Independent Large Cap Research

The Profits (And Perils) Of Independent Large Cap Research

The Profits (And Perils) Of Independent Large Cap ResearchIndependent insight published on Smartkarma 17th November 2017

Read more of Hemindra’s work by clicking here!

True, the field is crowded, and fresh insights are hard to come by. Still, contrary to Douglas Kim’s argument, it’s not mid-caps, but large-caps, that offer profitable subject matter for research. The advantage for the truly independent researcher is that, while the usual corporate doors are quickly shut, there are plenty of other doors no one thinks of opening.

For independent research to be recognized as a credible alternative to sell-side research, it has to play in the same field where the big girls and boys play, and in equities, it is large cap research. There is ample space for unusual perspectives and more importantly critical commentary for enterprising analysts to standout in the faceless herd and do the profession proud.

The proliferation of independent research analysts in the capital market as a result of cost pressures in the industry and introduction of Mifid II in Europe post January 1, 2018 has provided greater flexibility for analysts as well as more variety for institutional clients. As price discovery for independent research remains a work-in-progress, analysts are examining the most cost-effective, value-added service to provide to institutional clients.

In this respect, Douglas Kim has written an in-depth, insightful and well received article, ““Confessions of an Independent Analyst” on Smartkarma, documenting his experience as an independent research analyst and possible strategies analysts can adopt to prosper from 2018 onwards. One aspect of his comprehensive article is to suggest emphasizing mid and small size company research with a focus on generating “great investment ideas,” instead of venturing into the crowded large cap research, which is dominated by the bulge bracket firms. He does acknowledge the trade-off in research to write on “higher market cap stocks which may generate more interest vs. differentiated research in writing about “undiscovered” investment plays.”

Midcap research has a charm of its own. The competition amongst analysts is less, and the thrill of uncovering hidden gems is alluring. However, just as sectors have their day in the sun and can languish in the dark and go into hibernation, the volatility in midcaps can be far more severe and the winters long and hard. Typically, midcaps are a product of a bull market, rising rapidly with generous doses of liquidity. But come a bear phase, and liquidity in stocks dries up as institutional interest wanes.Exiting stocks may not be possible on account of high impact cost. In such a phase, dedicated midcap analysts are left high and dry, while large cap sector analysts can still survive on maintenance research.

Generating great investment ideas is the Holy Grail for analysts, but consistently recommending great investment ideas is extremely difficult for a single analyst, unless the market is bullish and all stocks are on fire. In the rare instance of an independent analyst consistently picking winners, he/she might well decide that, rather labouring and framing a logical argument to convince others, investing in those ideas makes better sense. Midcaps are also high risk, and their revenue can be volatile as they typically lack broad-based stability. Midcap analysts can earn a name recommending winners but lose credibility in any downturn.

No doubt, recommending winners is the ultimate objective for analysts. However, in the real world, to be recognized and appreciated as an analyst, it is more practical to consistently produce interesting, original insights on stocks, industries and the economy, defying the consensus when necessary. Framing a logical, well-researched angle is within the expertise of the analyst, but to achieve consistency in predicting winners and losers and the future direction of stock prices, which are influenced by a host of factors, is beyond the analyst’s control. Equity research analysts typically have their share of multi-baggers and stocks where their calls go horribly wrong, and that is par for the course. And while honest analysts make a genuine attempt to get their calls right, it is difficult to be consistent in getting calls right.

It is this writer’s contention that independent analysts, in recommending large cap stocks, should focus on providing unusual insights on the company, industry and the economy. Although large cap research is a highly competitive space, there is adequate room for providing critical research, an area which is largely and deliberately ignored by most analysts. Bloomberg’s Gadfly estimates that between “50 and 70% of a senior analyst’s time is spent on corporate access.” Unsurprisingly, then, not only does critical corporate analysis become a no-go area for most large cap analysts in bulge bracket firms, but also less time is devoted for thorough analysis. As a result, most large cap research has become an extension of corporate public relations in enhancing the image of the corporate. As Howard J Klein rightly points out in his erudite insight in the casino sector, sell-side analysts avoid asking about tough issues lest they injure ongoing relationships with corporate contacts they need to do their jobs. This is entirely understandable. But the downside is that the process tends to produce far too many softball questions in order to maintain a general air of civility and nurse relationships.

The business media are no better than most sell-side research. In India, the business media are focused on getting exclusive interviews with large cap Chief Executive Officers (CEOs) and Chief Financial Officers (CFOs). Anchors/editors hand over “Best CEO” and “Best Corporate” awards to large companies, and organise corporate round table conferences. And, of course, their business model is dependent on corporate advertising. As a result, in India, at least, investigative business reporting on large companies is virtually non-existent in the corporatized business media.

This is fertile, virgin territory for independent researchers to showcase their expertise in providing critical analysis: on corporate strategy, exposing senior management incompetence, accounting transparency, and the likely chinks in the layered armour of large corporates. It is highly unlikely that institutional investors will approach independent analysts to fix meetings with large corporates, and hence the corporate contact loss to an independent analyst is far less. Large corporates may, in retaliation, boycott the critical independent analyst from their regular news flow; this is inconvenient, but an experienced analyst normally should have developed multiple sources in the companies and industry that he/she covers to compensate for the loss of official contact. Moreover, the mandatory disclosures and regular corporate analysts’ presentations provide adequate information on developments for independent analysts to be kept informed without having corporate access. ICICI Bank Ltd (ICICIBC IN), India’s second largest private sector bank by assets has refused to interact with this writer for nearly two decades post the publication of a critical research note in January 1999, and Axis Bank Ltd (AXSB IN), India’s third large private bank by assets in June 2017, declined to entertain any further queries from this writer. The management boycott has not prevented this writer from regularly publishing (here and here) critical, non-consensus research on both these banks which has been appreciated by not only institutional investors but also by insiders in these banks.

In large cap research, institutional investors are not only looking for investment ideas but are also looking for unusual insights contributing to earnings’ drivers. And since considerable sell-side coverage is flattery disguised as research, there is a huge, unsatiated appetite for well documented, critical research. Unfortunately, over time, sell-side research has got used to being spoon-fed (instead of the rigours of data analysis and reading the fine print) by investor relations (IR) executives and CFOs of the companies they cover, and loss of official corporate contact cuts off any flow of information, as analysts did not develop alternative sources of information within these companies or from the industry. In his over 20 years of experience, this writer, as a sector analyst and head of research had noticed a reluctance by analysts to develop contacts such as labour union leaders, corporate whistle-blowers, regulators and auditors – interacting with such individuals can provide an alternative to the image projected by industry chieftains. Such management-spoon-fed individuals have no future as independent analysts, as sell-side research will provide corporate access and regurgitate management commentary to institutional clients.

Financial Times All-World Index

Source: Financial Times

Equity analysts, in general, are more comfortable presenting bullish arguments and normally ‘Buy’ recommendations outnumber ‘Sell’ calls. Even during bearish phases, the analyst community remains optimistic and expects the phase to be short-lived – near term hiccups but long term growth story intact is the common message articulated. On account of global liquidity and some recent mild economic revival, global equity indices have been on an upswing since early 2016. It is, therefore, no surprise that even on Smartkarma, a platform dedicated for independent research analysts, bullish views are in the majority, while bearish views remain in the minority and critical commentary on large companies and their management is rare.

Bullish & Bearish Views on Smartkarma

Source: Smartkarma

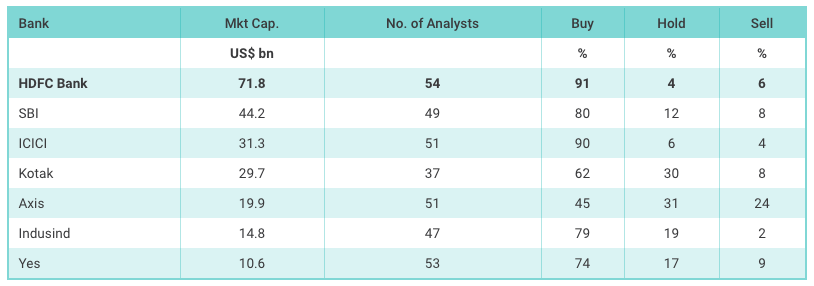

Analysts Coverage of Large Banks By Market Capitalisation in India

In India, large cap research is competitive and most of the global bulge bracket firms are present. As the financial sector has a high weightage in the market index, banks are extensively covered. HDFC Bank Limited (HDFCB IN) with a market capitalization of US$ 71.8 bn. is tracked by 54 analysts with 91% maintaining a ‘Buy’ recommendation and commentary is naturally positive. Yet Daniel Tabbush, an Insight provider at Smartkarma, is cautioning investors on HDFC Bank’s rising impairment costs. It is possible that HDFC Bank’s share price may continue to reward shareholders as it has done in the past, but Daniel Tabbush is taking on the consensus with a contrarian view supported by data. It is such outliers who get the attention of institutional investors and most importantly they will read and evaluate the merits of his argument.

Critical, independent, analytical research is not for the meek and there are pitfalls. There is no room for errors in critical research as the concerned corporate and investors will cross verify all the data points and analysts have to cross and double check the data prior to publishing. Corporates can boycott the critical analyst and deny her/him information and corporate access. Worse, vengeful companies can tie down analysts in lengthy, expensive law suits on charges of defamation and even use their extensive political contacts to make analysts experience the hospitality of the police – as happened in the case of fellow Smartkarma Insight provider, Nitin Mangal, for his critically acclaimed research on Indiabulls when he was with the independent research firm, Veritas.

For independent research to be recognized as a credible alternative to sell-side research, it has to play in the same field where the big girls and boys play, and in equities, it is large cap research. Midcap research is exotic, and can provide fabulous returns, but it is volatile and high-risk and in economic and market downturns, companies vaporise, as does the research. Independent research can and should do midcap research, but it should not be identified with midcap companies. Mifid II has provided a gateway for those brave, seasoned and enterprising analysts to forge a path of independence in a market heavily compromised by large corporate vested interests. It should use this opportunity to take the competition head-on, raise the bar on large corporate analysis, and in doing so, make proud the tribe of independent analysts.

The Profits (And Perils) Of Independent Large Cap Research

Independent insight published on Smartkarma 17th November 2017

Read more of Hemindra’s work by clicking here!