In this briefing:

- Softbank: Reduced Yield Competitiveness, End of Passive Buying and Softbank Group’s Hunger for Cash

- Samsung Bear Targets Coming into Focus

- (Mostly Asia) M&A in 2018: What Was Hot, And What Was Not

- Futu Holdings IPO Preview: Running Out of Steam

- Weekly Oil Views: Crude Remains at the Mercy of Fickle Financial Markets

1. Softbank: Reduced Yield Competitiveness, End of Passive Buying and Softbank Group’s Hunger for Cash

We are once again turning negative on Softbank Corp (9434 JP) as the stock price is now 18% above the ¥1,200 level which we mentioned looked cheap, outperforming Topix by 20% and the Nikkei by 21%.

Softbank Corp: When Does It Become a Buy?

In our view this IPO was oversold and probably to numerous weak hands who may now be looking at the large price drops that Softbank Group has occasionally suffered. We would hazard a guess that many of the individuals looking to flip the shares may still not have sold, however, if the stock dips below ¥1,200 we believe risk-reward would tilt positive until the passive buying is complete. Our view on this large drop is mostly that Softbank over-reached in terms of the size of the sale and the valuation.

The business, while subject to various headwinds should still be highly cash generative and at the current price is on just under 13x EV/OP. That’s not particularly cheap but nor is it ridiculously expensive if you believe OP will not drop (we believe it will). With a bit more of a discount and once the initial selling pressure from flippers dies down we believe the yield and passive buying should help the stock find a temporary floor. We do not view this as an attractive long-term holding in any way shape or form, but as a short-term trade the potential to make a 5-10% return on the back of a bounce following panic selling by retail supported by the yield and passive buying seems reasonably good.

Prior to that, we had flagged that retail demand for the IPO could be fragile in Softbank IPO: Signs Point to Risk of Early IPO Price Break and while there was a stronger sell-off than we expected immediately post listing, we would hazard a guess that there could still be an overhang close to the IPO price as there could be significant latent sell volume from retailers hoping to break-even and if that opportunity opens up in a weak market we believe many could choose to sell despite the rebound.

We would point to the news today regarding Softbank Group lowering its planned investment in WeWork from $16bn to just $2bn due to investors in the Vision Fund balking. As perhaps the most aggressive tech investor of the last few years, Softbank stepping back is not a good sign overall and raises questions about the viability of the valuations that other companies in its investment portfolio, namely Uber, are targeting for their upcoming IPOs. With news sources suggesting that Softbank Group is also looking to offload its Nvidia Corp (NVDA US) stake, the tide appears to have truly turned for tech in general and the chronically unprofitable platform companies such as Uber and WeWork in particular.

This raises the governance risks we initially highlighted regarding the use of Softbank Corp for funding the overall Softbank Group. As such, despite a final round of passive buying for Topix buying at the end of the month, the stock price looks vulnerable here.

2. Samsung Bear Targets Coming into Focus

Samsung Electronics (005930 KS) bear call from 50k has rewarded with a series of short trades with the most recent short from 46k and has sliced through support at 39,500. Impulsive nature of the decline tell us a key low will take more time to take shape.

SEC is pressing on critical relative support versus the Kospi. A break would send ripples through the broader market in terms of the direction bias. Kospi has already spent far too much time below the macro pivot barrier at 272k for signs of any immediate recovery. Risk lies with a downside overshoot below 250 support for the Kospi.

SEC is completing a minute full wave count down that sets up a counter trend bounce which is tradable but the major low remains elusive. We outline probable downside targets in late Q1/Q2, upside cap into Q3 and the more strategic buy support.

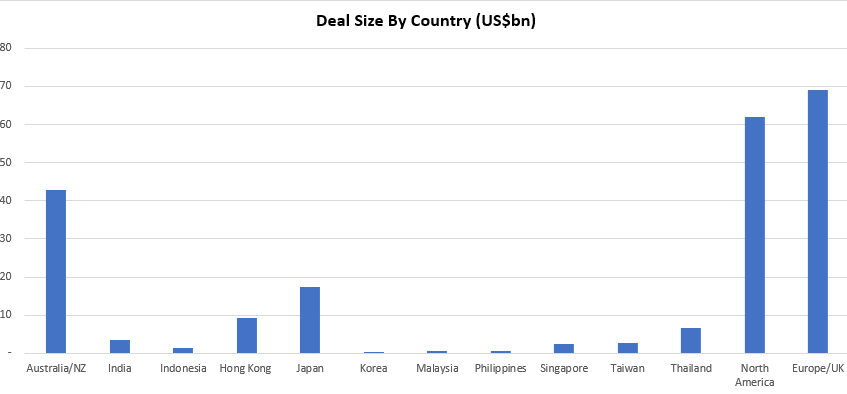

3. (Mostly Asia) M&A in 2018: What Was Hot, And What Was Not

This insight briefly summarises the 93 M&A transactions, with a collective deal size of ~US$215bn, published on Smartkarma in 2018.

Transactions discussed were typically Asia-Pacific-centric or concerned an outbound transaction initiated from an Asia-Pacific-listed company. The majority of these deals involved a market cap/deal size in excess of US$100mn.

The mega deals of Takeda Pharmaceutical (4502 JP)/Shire PLC (SHP LN), Sprint Corp (S US)/T Mobile Us Inc (TMUS US) and Intl Business Machines (IBM US)/Red Hat Inc (RHT US) were first discussed in May, June and November respectively.

- The most generous country? The average premium for Australian and Hong Kong deals was almost identical at 38%.

- The stingiest? Singapore with 16%.

- The graveyard award? 49 deals were completed with 35 ongoing. Australia had four deals (out of a total of 29, the most for any country) that were abandoned for various reasons – such as CKI getting dinged by FIRB in its tilt for APA Group (APA AU). But in terms of outright fails, Hong Kong takes home that award following the failures in Pou Sheng Intl Holdings (3813 HK), Guoco Group Ltd (53 HK) and Spring Real Estate Investment Trust (1426 HK).

During the year a number of large, high profile transactions were completed that were also extensively analysed and discussed on Smartkarma. However, if the initial discussions between the two parties (acquirer & target) took place pre-2018, they are not included in the charts above. A selection of these include (in no particular order):

Broadcom Corp Cl A (BRCM US)/Qualcomm Inc (QCOM US)

Alps Electric (6770 JP)/Alpine Electronics (6816 JP)

Westfield Corp (WFD AU)/Unibail-Rodamco SE (UL FP)

Idemitsu Kosan (5019 JP)/Showa Shell Sekiyu Kk (5002 JP)

Orient Overseas International (316 HK)

4. Futu Holdings IPO Preview: Running Out of Steam

Futu Holdings Ltd (FHL US) is the fourth largest online broker in Hong Kong. Futu has filed for a Nasdaq IPO to raise $300 million, down from an earlier indication of a $500 million raise according to press reports. Futu is backed by Tencent Holdings (700 HK) (38.2% shareholder), Matrix Partners (6.1%) and Sequoia Capital (4.0%).

At first glance, Futu appears to be a winning new economy company as its rapid revenue growth has been accompanied by rising margins. However, on closer inspection, we believe that Futu’s fundamentals are at best mixed.

5. Weekly Oil Views: Crude Remains at the Mercy of Fickle Financial Markets

It has been anything but a happy start to 2019 for the stock markets, which remained under pressure as trading resumed in the new year. A clutch of weak manufacturing data for December – from China to the eurozone and the US – soured the mood for investors through last week.

That was followed by a rare revenue warning from Apple Inc (AAPL US) , citing slowing sales in China, which drew fresh attention to the vulnerability of American companies from the bitter trade war between the world’s two largest economies. The only assets that seemed to be in favour were the safe havens such as Gold (GOLD COMDTY) and the Japanese yen.

Beijing provided the first major lift to market sentiment on Friday, by lowering the reserve requirement ratio for Chinese banks, in a bid to inject more cash into the system. US Fed Chairman Jerome Powell signalling a “patient” approach to monetary policy in a panel discussion in Atlanta later in the day and a strong US jobs report for December completed the trinity of factors that closed the week with a rally in stock markets as well as crude.

Brent and WTI closed nearly 2% higher on the day, just above $57 and just under $48 respectively. Sentiment in the oil market was boosted by initial surveys showing a surprisingly large drop in OPEC production in December.

OPEC/non-OPEC cuts of 1.2 million b/d took effect on January 1 and should yield results in the coming weeks, but we expect crude to remain largely beholden to the twists and turns in the global economy. Just as in the broader financial markets, so in the oil markets, all eyes will now turn to the high-level trade negotiations between the US and China, due to be held in Beijing over January 7-8.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.