In this briefing:

- (Mostly Asia) M&A in 2018: What Was Hot, And What Was Not

- Futu Holdings IPO Preview: Running Out of Steam

- Weekly Oil Views: Crude Remains at the Mercy of Fickle Financial Markets

- Naver Bull Wedge to Trade Higher

- IPS Securex (IPSS SP): Micro-Cap Could Benefit from SG Gov’t HDB Upgrade Program

1. (Mostly Asia) M&A in 2018: What Was Hot, And What Was Not

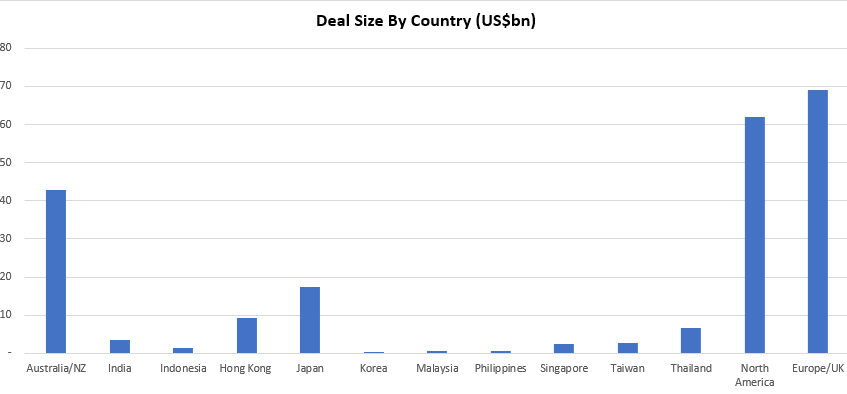

This insight briefly summarises the 93 M&A transactions, with a collective deal size of ~US$215bn, published on Smartkarma in 2018.

Transactions discussed were typically Asia-Pacific-centric or concerned an outbound transaction initiated from an Asia-Pacific-listed company. The majority of these deals involved a market cap/deal size in excess of US$100mn.

The mega deals of Takeda Pharmaceutical (4502 JP)/Shire PLC (SHP LN), Sprint Corp (S US)/T Mobile Us Inc (TMUS US) and Intl Business Machines (IBM US)/Red Hat Inc (RHT US) were first discussed in May, June and November respectively.

- The most generous country? The average premium for Australian and Hong Kong deals was almost identical at 38%.

- The stingiest? Singapore with 16%.

- The graveyard award? 49 deals were completed with 35 ongoing. Australia had four deals (out of a total of 29, the most for any country) that were abandoned for various reasons – such as CKI getting dinged by FIRB in its tilt for APA Group (APA AU). But in terms of outright fails, Hong Kong takes home that award following the failures in Pou Sheng Intl Holdings (3813 HK), Guoco Group Ltd (53 HK) and Spring Real Estate Investment Trust (1426 HK).

During the year a number of large, high profile transactions were completed that were also extensively analysed and discussed on Smartkarma. However, if the initial discussions between the two parties (acquirer & target) took place pre-2018, they are not included in the charts above. A selection of these include (in no particular order):

Broadcom Corp Cl A (BRCM US)/Qualcomm Inc (QCOM US)

Alps Electric (6770 JP)/Alpine Electronics (6816 JP)

Westfield Corp (WFD AU)/Unibail-Rodamco SE (UL FP)

Idemitsu Kosan (5019 JP)/Showa Shell Sekiyu Kk (5002 JP)

Orient Overseas International (316 HK)

2. Futu Holdings IPO Preview: Running Out of Steam

Futu Holdings Ltd (FHL US) is the fourth largest online broker in Hong Kong. Futu has filed for a Nasdaq IPO to raise $300 million, down from an earlier indication of a $500 million raise according to press reports. Futu is backed by Tencent Holdings (700 HK) (38.2% shareholder), Matrix Partners (6.1%) and Sequoia Capital (4.0%).

At first glance, Futu appears to be a winning new economy company as its rapid revenue growth has been accompanied by rising margins. However, on closer inspection, we believe that Futu’s fundamentals are at best mixed.

3. Weekly Oil Views: Crude Remains at the Mercy of Fickle Financial Markets

It has been anything but a happy start to 2019 for the stock markets, which remained under pressure as trading resumed in the new year. A clutch of weak manufacturing data for December – from China to the eurozone and the US – soured the mood for investors through last week.

That was followed by a rare revenue warning from Apple Inc (AAPL US) , citing slowing sales in China, which drew fresh attention to the vulnerability of American companies from the bitter trade war between the world’s two largest economies. The only assets that seemed to be in favour were the safe havens such as Gold (GOLD COMDTY) and the Japanese yen.

Beijing provided the first major lift to market sentiment on Friday, by lowering the reserve requirement ratio for Chinese banks, in a bid to inject more cash into the system. US Fed Chairman Jerome Powell signalling a “patient” approach to monetary policy in a panel discussion in Atlanta later in the day and a strong US jobs report for December completed the trinity of factors that closed the week with a rally in stock markets as well as crude.

Brent and WTI closed nearly 2% higher on the day, just above $57 and just under $48 respectively. Sentiment in the oil market was boosted by initial surveys showing a surprisingly large drop in OPEC production in December.

OPEC/non-OPEC cuts of 1.2 million b/d took effect on January 1 and should yield results in the coming weeks, but we expect crude to remain largely beholden to the twists and turns in the global economy. Just as in the broader financial markets, so in the oil markets, all eyes will now turn to the high-level trade negotiations between the US and China, due to be held in Beijing over January 7-8.

4. Naver Bull Wedge to Trade Higher

After an impulsive rise from the 110.5k dual bottom, Naver Corp (035420 KS) has formed a bull wedge that is expected to see a nice rally and perform over the Korean market.

RSI also shows a compelling set up for a rise.

Buy volumes are starting to improve and supportive.

Targets are 8% and 14% higher from current levels.

Macro pivot resistance will cap rally attermpts in Q1.

5. IPS Securex (IPSS SP): Micro-Cap Could Benefit from SG Gov’t HDB Upgrade Program

Since its founding in 1960 the Housing Development Board (HDB) has constructed over 1.1 million dwelling units across Singapore. Currently, over 80% of the Singapore population lives in HDB built housing. With the bulk of these buildings having been constructed between 1960-1988 many of them are up for extensive renewal and renovation works. Construction companies should benefit from this trend, as should the micro-cap Ips Securex Holdings (IPSS SP), a reseller of equipment that modifies HDBs with emergency monitoring systems for senior citizens.

Outgoing PM Lee Hsien Loong (LHL) was very outspoken about the need to upgrade HDBs and make them safer for many of SG’s “pioneers” and senior citizens during his speech at the 2018 National Day Parade (NDP). With a general election coming later this year (date TBC) investors in IPS can be hopeful that the company should be awarded some new contracts and finally end the three-year de-rating which has taken the stock from 0.32 SGD in December 2015 to 0.055 SGD recently.

IPS is cheap with a market cap of only 27M SGD (20M USD) but can only start to re-rate on new major contract announcements.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.