In this briefing:

- THK (6481 JP): New Orders Down by Two-Thirds in 4Q, Near the Bottom of the Cycle

- Horiba (6856 JP): Long-Term Buy on Pullbacks

- Doosan Heavy & Doosan E&C Rights Offers: Situational Assessment & Offering Size Estimation

- Global Solar Energy Stocks Are Bottoming

- Minebea-Mitsumi Underpriced Tender for U SHIN (6985 JP) Launched

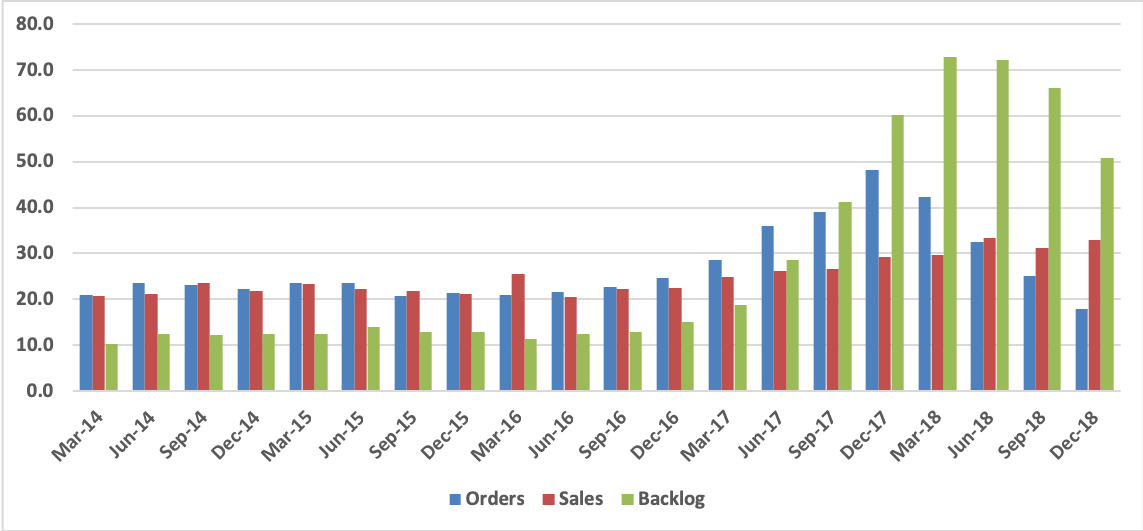

1. THK (6481 JP): New Orders Down by Two-Thirds in 4Q, Near the Bottom of the Cycle

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

2. Horiba (6856 JP): Long-Term Buy on Pullbacks

Horiba’s share price has rebounded on FY Dec-18 results that were above management’s most recent guidance and better than we had expected. Consolidated operating profit was up 7.5% on a 7.8% increase in sales, and net profit up 37.0% following extraordinary gains (vs. losses the previous year) and a lower effective tax rate.

4Q results were weak, primarily due to the downturn in semiconductor capital spending, but this was no surprise. Total consolidated operating profit was down 10.3% year-on-year on a 2.3% increase in sales in the three months to December, while operating profit on Semiconductor Instruments & Systems (primarily mass flow controllers) was down 32.8% on a 15.8% decrease in sales.

Looking ahead, management is guiding for year-on-year declines in both sales and profits in the six months to June, again due to weak demand for semiconductor equipment, followed by a sharp rebound in 2H and low single-digit growth FY Dec-19 as a whole. Judging from the semiconductor equipment order flow, it appears that a weak 1H will be hard to avoid, while there is as yet no sign pointing to recovery. Nevertheless, we have raised our own sales and profit estimates for this fiscal year and next based on the absolute levels of orders and sales.

Automotive Test Systems and the company’s other businesses should continue to grow, supported by the acquisition of FuelCon AG of Germany (an industry leader in battery and fuel cell validation) and Manta Instruments of the U.S. (which makes nanoparticle tracking analysis systems). The issue, then, is how soon and how rapidly semiconductor related investments will recover. We suspect later and more slowly than management hopes, but in any case the downturn appears to have been discounted.

At ¥5,980 (Friday, February 15, closing price), Horiba has rebounded by 44% from its January 4 low of ¥4,155, but is still 38% below its ¥9,590 all-time high reached last May. It is now selling at 13.6x our EPS estimate for this fiscal year and 12.3x our estimate for FY Dec-20. These and other projected valuations are on the low side of their 5-year historical ranges. Once the recent bounce has been consolidated, there should be another buying opportunity for longer term investors.

3. Doosan Heavy & Doosan E&C Rights Offers: Situational Assessment & Offering Size Estimation

- Doosan Engineering & Construction (011160 KS) is considering a ₩400bil rights offer. At a usual 30% discount to the last closing price, this ₩400bil rights offer will issue a total 372M new shares. This is a 370% capital increase with a 79% share dilution. Per share allocation is 3.82.

- Doosan Heavy Industries (034020 KS) is left with no other option but to pursue its own rights offer as well. Considering Doosan Corp (000150 KS)‘s financial situation, Doosan Corp may be able to inject only about ₩100bil into Heavy.

- Factoring in this ₩100bil for a a 34.04% stake, we can estimate the size of Heavy’s rights offer at about ₩300bil. At a 30% discount to the last closing price, this ₩300bil rights offer will issue a total 45.5M new shares. This is a 35% capital increase with a 26% shareholding dilution. Per share allocation is 0.35.

4. Global Solar Energy Stocks Are Bottoming

In today’s report we highlight the following actionable solar energy names: First Solar (FSLR), SolarEdge Technologies (SEDG), GCL-Poly Energy (3800-HK), Meyer Burger Technology AG (MBTN-CH), Enphase Energy (ENPH), JinkoSolar Sponsored ADR (JKS), TerraForm Power (TERP), Beijing Enterprises Clean Energy Group (1250-HK), GCL New Energy (451-HK), and Viatron Technologies (141000-KR).

5. Minebea-Mitsumi Underpriced Tender for U SHIN (6985 JP) Launched

Three months ago, Minebea Mitsumi (6479 JP) announced that it would launch a Tender Offer for U Shin Ltd (6985 JP) and it would take just under three months until the approvals were received and it could officially start the Tender Offer process. It took a couple of weeks longer, as proposed by U Shin’s update on 30 January, which indicated anti-trust approvals had been received.

The background to the Tender Offer was discussed in Minebea Mitsumi Launches Offer for U-SHIN in early November.

My first conclusion in November was that this was the “riskiest” straight-out non-hostile TOB I had seen in a while.

This is a wide-open deal. The buyer owns 1 round lot. The largest holder is an activist. The deal is being proposed at not such a super-high multiple (8x forecast FY earnings for the year ending 31 December 2018) and 4.9x EV/EBITDA. It is 3.7-4.0x when taking into account the 67 different equity positions they held at the end of last year, some of which they have recently liquidated.

from (8 Nov 2018) Minebea Mitsumi Launches Offer for U-SHIN

In the interim, the activist dropped their position in half (necessitating a filing of a Large Shareholder Report for going below 5% – and they may have completely liquidated by now), and an investment bank has gone above 5% since then.

The financial advisory “valuations” at the time were more than questionable. A discussion of the valuation levels can be found in the previous insight (I don’t need to repeat them here, just go there).

Today, the company raised its OP and Ordinary Income forecasts for the year ended 31 December 2018, but lowered its Net Income forecast by 98.8% due to writeoffs at many overseas facilities. Then the promptly reported earnings (also only in Japanese) a few seconds later (only available in Japanese).

Op is now forecast to drop 2% in 2019 vs 2018, but the 2019 forecast is 11+% higher than the 2018 forecast was just yesterday. The forecast for Net Income is ¥99.35/share, putting the deal at <10x forecast PER. And even less if one considers that the cross-shareholdings could be reduced.

The New News

Today Minebea Mitsumi announced the launch of its Tender Offer, to commence tomorrow, at the same price as originally planned (¥985/share), and to run for 38 days.

This deal is still perplexing to me. It’s easy enough from an industrial standpoint. I mean, why not buy relatively cheap assets then see if you can cross-sell or assume some attrition. But for investors… I wonder why they put up with this.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.