In this briefing:

- HDC Holdings Goes Activist on Samyang Foods

- Last Week in GER Research: API/Sigma, M1, Eclipx/Mcmillan and Hansoh IPO

- M1 Ltd (M1 SP): Axiata Throws in the Towel, Delisting Looms

- THK (6481 JP): New Orders Down by Two-Thirds in 4Q, Near the Bottom of the Cycle

- Horiba (6856 JP): Long-Term Buy on Pullbacks

1. HDC Holdings Goes Activist on Samyang Foods

- We have a really interesting and unusual situation in Korea right now with HDC Holdings (012630 KS) going activist on Samyang Foods (003230 KS). HDC Holdings is the second largest owner of Samyang Foods.

- HDC Holdings is recommending that the company should exclude executive directors that have been sentenced to imprisonment on cases such as embezzlement and extreme negligence resulting in significant losses for Samyang Foods. This is an agenda which will be discussed in the Samyang Foods’ AGM next month on March 22nd.

- HDC Holdings is taking a very unusual move right now in going against the traditional “save face” mentality in the Korea Inc. and trying to publicly urge Samyang Foods to make changes to its BOD.

2. Last Week in GER Research: API/Sigma, M1, Eclipx/Mcmillan and Hansoh IPO

In this version of the GER weekly research wrap, we assess the bump prospects in the Australian Pharma Industries (API AU) / Sigma Healthcare (SIG AU) potential merger. Arun updates on M1 Ltd (M1 SP) which could be delisted following an unconditional offer. In addition, we dig into the trading update for Eclipx (ECX AU) and assess the risks that Mcmillan Shakespeare (MMS AU) could walk away from the deal. Finally, we initiate on the IPO of Hansoh Pharmaceutical (HANSOH HK). A calendar of upcoming catalysts is also attached.

More details can be found below.

Best of luck for the new week – Rickin, Venkat and Arun

3. M1 Ltd (M1 SP): Axiata Throws in the Towel, Delisting Looms

After the market close last Friday, M1 Ltd (M1 SP) announced that the voluntary conditional offer (VGO) became unconditional as Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP) (KCL-SPH) has an interest in M1 of 76.4%. The offer became unconditional due to Axiata Group (AXIATA MK), the single largest shareholder with a 28.7% shareholding, accepting the offer.

KCL-SPH again extended the closing date of the offer from 18 February to 4 March 2019. M1’s shares are trading at S$2.04 per share, marginally below the VGO price of S$2.06 per share. We believe that the KCL-SPH should get the valid acceptances to complete the delisting and wholly own M1.

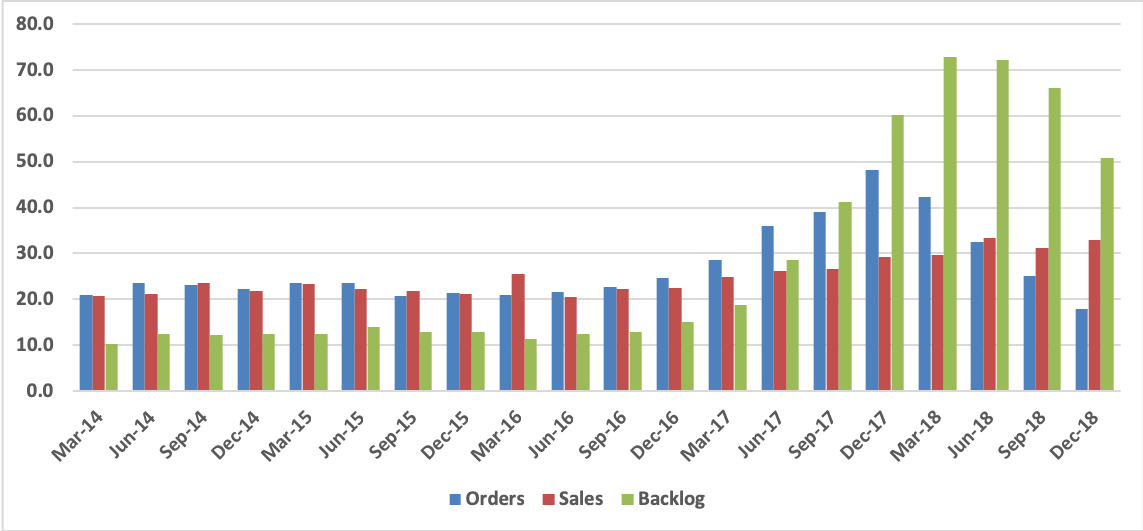

4. THK (6481 JP): New Orders Down by Two-Thirds in 4Q, Near the Bottom of the Cycle

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

5. Horiba (6856 JP): Long-Term Buy on Pullbacks

Horiba’s share price has rebounded on FY Dec-18 results that were above management’s most recent guidance and better than we had expected. Consolidated operating profit was up 7.5% on a 7.8% increase in sales, and net profit up 37.0% following extraordinary gains (vs. losses the previous year) and a lower effective tax rate.

4Q results were weak, primarily due to the downturn in semiconductor capital spending, but this was no surprise. Total consolidated operating profit was down 10.3% year-on-year on a 2.3% increase in sales in the three months to December, while operating profit on Semiconductor Instruments & Systems (primarily mass flow controllers) was down 32.8% on a 15.8% decrease in sales.

Looking ahead, management is guiding for year-on-year declines in both sales and profits in the six months to June, again due to weak demand for semiconductor equipment, followed by a sharp rebound in 2H and low single-digit growth FY Dec-19 as a whole. Judging from the semiconductor equipment order flow, it appears that a weak 1H will be hard to avoid, while there is as yet no sign pointing to recovery. Nevertheless, we have raised our own sales and profit estimates for this fiscal year and next based on the absolute levels of orders and sales.

Automotive Test Systems and the company’s other businesses should continue to grow, supported by the acquisition of FuelCon AG of Germany (an industry leader in battery and fuel cell validation) and Manta Instruments of the U.S. (which makes nanoparticle tracking analysis systems). The issue, then, is how soon and how rapidly semiconductor related investments will recover. We suspect later and more slowly than management hopes, but in any case the downturn appears to have been discounted.

At ¥5,980 (Friday, February 15, closing price), Horiba has rebounded by 44% from its January 4 low of ¥4,155, but is still 38% below its ¥9,590 all-time high reached last May. It is now selling at 13.6x our EPS estimate for this fiscal year and 12.3x our estimate for FY Dec-20. These and other projected valuations are on the low side of their 5-year historical ranges. Once the recent bounce has been consolidated, there should be another buying opportunity for longer term investors.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.