In this briefing:

- (Mostly Asia) M&A in 2018: What Was Hot, And What Was Not

- Healius (HLS AU): Bid Rejection Provides Option Value

- Amarin–2019’s Biggest Buyout Target for Big Pharma

- Healius And The (Likely) First Salvo

- EGM Diaries

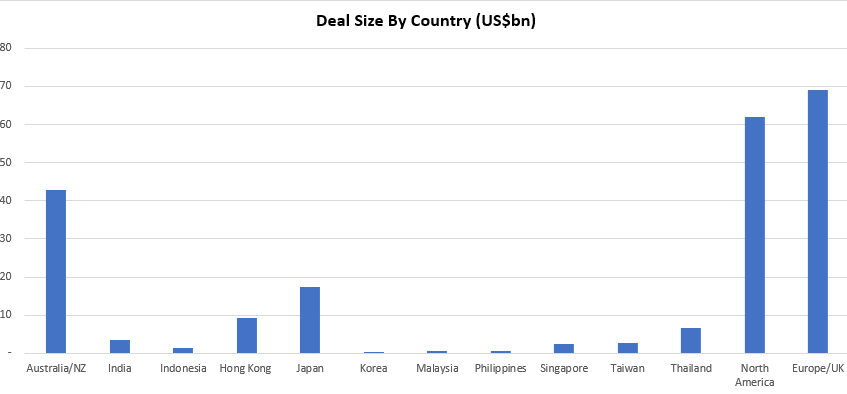

1. (Mostly Asia) M&A in 2018: What Was Hot, And What Was Not

This insight briefly summarises the 93 M&A transactions, with a collective deal size of ~US$215bn, published on Smartkarma in 2018.

Transactions discussed were typically Asia-Pacific-centric or concerned an outbound transaction initiated from an Asia-Pacific-listed company. The majority of these deals involved a market cap/deal size in excess of US$100mn.

The mega deals of Takeda Pharmaceutical (4502 JP)/Shire PLC (SHP LN), Sprint Corp (S US)/T Mobile Us Inc (TMUS US) and Intl Business Machines (IBM US)/Red Hat Inc (RHT US) were first discussed in May, June and November respectively.

- The most generous country? The average premium for Australian and Hong Kong deals was almost identical at 38%.

- The stingiest? Singapore with 16%.

- The graveyard award? 49 deals were completed with 35 ongoing. Australia had four deals (out of a total of 29, the most for any country) that were abandoned for various reasons – such as CKI getting dinged by FIRB in its tilt for APA Group (APA AU). But in terms of outright fails, Hong Kong takes home that award following the failures in Pou Sheng Intl Holdings (3813 HK), Guoco Group Ltd (53 HK) and Spring Real Estate Investment Trust (1426 HK).

During the year a number of large, high profile transactions were completed that were also extensively analysed and discussed on Smartkarma. However, if the initial discussions between the two parties (acquirer & target) took place pre-2018, they are not included in the charts above. A selection of these include (in no particular order):

Broadcom Corp Cl A (BRCM US)/Qualcomm Inc (QCOM US)

Alps Electric (6770 JP)/Alpine Electronics (6816 JP)

Westfield Corp (WFD AU)/Unibail-Rodamco SE (UL FP)

Idemitsu Kosan (5019 JP)/Showa Shell Sekiyu Kk (5002 JP)

Orient Overseas International (316 HK)

2. Healius (HLS AU): Bid Rejection Provides Option Value

Healius (HLS AU), formerly known as Primary Health Care (PRY AU), is a leading Australian owner of GP clinics and pathology centres. Healius just took four days to reject Jangho Group Co Ltd A (601886 CH)’s 3 January 2018 proposal of A$3.25 cash per share as it “is opportunistic and fundamentally undervalues Healius.”

We believe that rejection of Jangho’s proposal provides shareholders with option value. If Healius’ growth initiatives generate value, we believe that the shares will be worth more than Jangho’s proposal. If Healius’ growth initiatives stall and the shares slide, we believe that Jangho will once again table a proposal.

3. Amarin–2019’s Biggest Buyout Target for Big Pharma

Amarin (AMRN US), a US-listed biotech firm, presented the full results of its “Reduce-It” (RI) clinical trial at a conference for the American Heart Association (AHA) last November. The new data announced showed that, Vascepa–Amarin’s cardiovascular drug–when used with statins, reduces the risk of heart attacks by 31%, strokes by 28%, and cardiovascular death by 20%–all with minimal safety issues. The stock has plunged by -37% since the AHA event, largely due to concerns–which are misplaced in our view–regarding the placebo used in the RI trial.

We attended the AHA event and its ancillary meetings in Chicago and, in this Insight, detail the main points covered there, the powerful efficacy of Vascepa, the addressable market, the placebo issue, and why we think Amarin could be 2019’s biggest buyout candidate among Big Pharma. We also analyze Amarin’s 2018 preliminary results and 2019 guidance from last Friday in detail.

Enthusiastic Response from Doctors over the “Reduce-It” Trial Data: The data released at the AHA event for Vascepa from its Reduce-It (RI) trial was so robust that it drew applause from the 2,500 doctors in attendance, 87% of whom were polled, responding that they would prescribe Vascepa. Given how safe the drug is and its high relative risk reduction (RRR) of cardiovascular events, Vascepa should be a blockbuster drug.

Q4 2018 Revenues & Prescriptions Surge Post Trial Results: Amarin just announced Q4 revenues and 2019 guidance last Friday. While its conservative 2019 guidance of $350m in revenues (+55% YoY) may disappoint, as it’s 16% below consensus estimates, the key focus should be on Q4 revenue growth of 38% YoY, with 35% growth in new prescriptions. This came on the back of the RI trial results and without any label expansion, which Amarin plans to file with the FDA during Q1. If label expansion is approved, Vascepa sales should soar further.

Peak Sales Could Easily Surpass $10bn if Vascepa is Approved in Europe & China: Counting only the patients with coronary heart disease and diabetes–the core target for Vascepa–there are 48m patients in North America, 98m in Europe and 230m in China. If only 30% of these patients use Vascepa by 2030–when its patent expires–peak sales could reach at least $12bn (see Table-3 below). The need for Vascepa is dire, as cardiovascular disease (CVD) is the leading cause of death worldwide (see chart-1). In the US, one in four adults have elevated triglycerides, yet only 4% have been treated. The upside for Vascepa is huge.

Stock Plunges Due to Concern Over Placebo Used in Reduce-It Trial: Just 16 minutes into the Reduce-It trial results being revealed at the AHA conference last November, Forbes published a “kill” story on the trial outcomes. The Forbes article (here) claimed that results were not trustworthy (quoting doctors in charge of clinical trials for a rival drug), as the mineral oil used in the placebo arm of the trial impacted statin absorption. This sent the stock plunging by -26% in the following two days after the conference. Below we discuss why these concerns are misplaced, especially since the FDA approved of mineral oil for use as a placebo.

Amarin is Now an Attractive Take-Over Candidate for Big Pharma: Based on our estimates, Amarin should reach $7.6bn in 2022 revenues and $8.40 in EPS (consensus is at $1.5bn and $2.23) on just 40% penetration of the CVD patients in the US and the Middle East (where Vascepa is already approved) and 30% penetration in Canada and Europe. On average, it takes drug makers at least $4bn over 10 years for new drug development and the success rate for FDA approval is only one in ten. In light of this, Amarin has become an attractive take-over candidate, with potential peak sales of $16bn (if China is successfully penetrated) and current market cap of only $4.2bn.

4. Healius And The (Likely) First Salvo

Healius (HLS AU) (until last month known as Primary Health Care Limited), a leading owner of general practice clinics and pathology centres in Australia, announced an unsolicited and conditional proposal (including DD) from Jangho Group Co Ltd A (601886 CH) at A$3.25/share (~10x FY19 EV/EBITDA) in a A$2.0bn deal. Jangho currently holds a 15.9% stake in Healius and has been on the shareholder register for two years.

The Offer price translates to a 33.2% premium to the undisturbed price but below the 12-month high of A$4.09 in March 2018. Optically and when referenced to closest peer Sonic Healthcare (SHL AU), the offer price appears light.

Reflecting the long laundry list of conditions attached to this indicative offer, such as securing debt financing and various regulatory approvals in China and Australia, notably data security, this indicative deal is trading wide at a gross/annualized spread of 25%/47%, assuming a deal completion date in early August.

This proposal does, however, indicate Healius was probably oversold.

This morning, Healius’ board rejected the proposal as it was considered opportunistic and fundamentally undervalued the company.

5. EGM Diaries

We recently attended the extraordinary general meeting (EGM) of Zydus Wellness (ZYWL IN). The primary agenda for the EGM was to approve the issue of fresh equity and raise debt to finance the acquisition of Kraft Heinz Co (KHC US) ‘s Indian subsidiary Heinz India Private Limited jointly with Cadila Healthcare (CDH IN). This will include the brands Complan (Health Food Drink), Glucon D (Glucose Powder), Nycil (Talcum Power) and Sampriti Ghee. We believe the deal is in sync with management’s vision of developing Pharma oriented consumer brands. However with recent acquisition of Glaxosmithkline Consumer Healthcare (SKB IN) by Hindustan Unilever (HUVR IN) the competition in the health food drink market may get intense. Having said that, the largest brand Glucon D will likely continue market leadership along with Everyuth and Nycil which will be a good addition to the Zydus Portfolio. Any attempt for market share gains with Complan and Sampriti ghee will be futile and may come at a cost of margins. Based on preliminary, we expect full effect of the deal to appear on FY 2020 financials. Our preliminary estimates indicate a FY 2021 EPS of 51.68, which with a average PE multiple of 34.56 leads to a price target of INR 1809 per share implying an upside of 35% from latest close price of INR 1342. We will revisit our estimates post Q4 FY19 numbers when a much clearer picture is likely to emerge.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.