In this briefing:

- MYOB (MYO AU): Shareholders Are Caught Between a Rock and a Hard Place

- New Pride Rights Offer: Tempting but Tricky

- LG Chem Share Class: Another Pref to Watch as Div Yield Gap at 4Y High

- Daelim Industrial Share Class: One of Prefs to Arb Trade on Div Payout Record Date

- MYOB Caves And Agrees To KKR’s Reduced Offer

1. MYOB (MYO AU): Shareholders Are Caught Between a Rock and a Hard Place

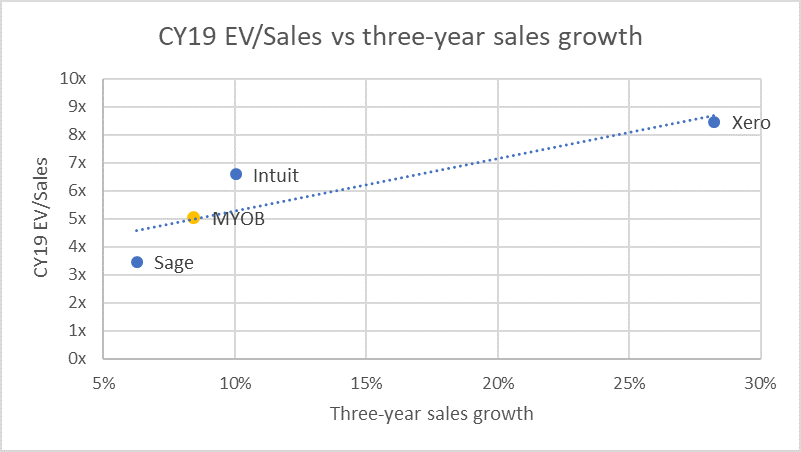

On 24 December, MYOB Group Ltd (MYO AU) announced that it entered into a scheme implementation agreement under which KKR will acquire MYOB at $3.40 per share, which is 10% lower than 2 November offer price of A$3.77. MYOB claims its decision to recommend KKR’s lower offer was based on current market uncertainty, long-term nature of its strategic growth plans and the go-shop provisions of the deal.

We believe that KKR’s revised offer is opportunistic, but MYOB’s shareholders are caught between a rock and a hard place. Shareholders can take a short-term view and grudgingly accept the revised offer. Alternatively, shareholders can take a long-term view by rejecting the offer and hope MYOB’s strategic growth plans and a market recovery can reverse the inevitable share price collapse.

2. New Pride Rights Offer: Tempting but Tricky

- New Pride Corp (900100 KS) announced a ₩36.2bil rights offer. This is a public offering, so there won’t be subscription rights to trade. Pricing will be done as 3-day VWAP on Jan 9~11 at a 30% discount.

- Supposedly, we can have ample opportunity to arb trade. This may be what the company is hoping. Simply, we wait until Jan 16~17 (subscription period) and see the spread. At this much discount, there must be a huge spread opening.

- Proration risk can be much more annoying than a usual stockholder offering. In the previous public offering event by New Pride, subscription rate went as high as 370 to 1. It should be way much lower this time. But still this is risky enough.

3. LG Chem Share Class: Another Pref to Watch as Div Yield Gap at 4Y High

- LG Chem Ltd (051910 KS) 1P is now at a 44.20% discount to Common. Div would be the same as last year of ₩6,000 despite lower earnings. Payout would be 28%. Div yield for Common will be 1.68%, and 3.03% for 1P. Div yield difference stands at 1.35%p. This is a record high at least since 2014.

- 1P’s discount to Common is hovering at the highest level in 2 years. On a 20D MA, it is close to +1 σ. It may not be tempting enough for those seeking high yields. Otherwise, this’d be worth giving it a shot. Liquidity shouldn’t be an issue. Short recovering risk on Common also appears to be limited.

4. Daelim Industrial Share Class: One of Prefs to Arb Trade on Div Payout Record Date

- Daelim Industrial (000210 KS) is one of the main targets of local activist movement. This makes a setting for higher dividends. Common div yield to 1.58% and Pref to 4.18%. Difference is 2.59%p. This is the widest gap in many years.

- Pref is currently at a 60.89% discount to Common. Among those > ₩100bil MC prefs, it is the second highest discounted pref, only behind CJ Cheiljedang 1P (097955 KS). Local street expects at least ₩1,600 div per share. This should be a conservative estimate. On a 20D MA, Pref is above +1 σ.

- Dec 26 is record date of dividend payout. I expect a price catchup movement tomorrow in favor of Pref. I’d go long Pref and short Common as early in the morning as possible.

5. MYOB Caves And Agrees To KKR’s Reduced Offer

It could have gone either way.

After securing a 19.9% stake from Bain in early October and initially pitching A$3.70/share, in a textbook bear hug, KKR (marginally) bumped its indicative offer to A$3.77/share to a get a look under the hood, then following seven weeks of due diligence, backtracked with a lower price of A$3.40/share, citing adverse market conditions.

MYOB Board’s response last week to the reduced offer was to inform KKR that it is not in a position to recommend the revised proposal, however, “it remains in discussions with KKR regarding its proposal”, leaving the door open for ongoing negotiations. KKR for its part, said there were no landmines following the DD process. The price action last Friday suggested the outcome was a coin toss.

Today, KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal and subject to an independent expert concluding the Offer is in the best interest of shareholders. The Offer price assumes no full-year dividend is paid.

The agreement provides a “go shop” provision until the 22 February 2019 – when MYOB is expected to release its FY18 results – to solicit competing proposals.

The Offer appears reasonable when compared to peers and with regards to the 14% decline in the ASX technology index; but conversely, could be construed as being opportunistic.

A Scheme Booklet is expected to be dispatched mid-March with an estimated implementation date of 3 May. Currently trading at a 3.8%/11% gross/annualised spread. 1 January makes a new year and there will be investors who would want to take an agreed deal at 11%.