In this briefing:

- Harbin Electric: The Price Is Not Right

- MYOB (MYO AU): Shareholders Are Caught Between a Rock and a Hard Place

1. Harbin Electric: The Price Is Not Right

As speculated in Harbin Electric Expected To Be Privatised, Harbin Electric Co Ltd H (1133 HK) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption.

The Offer price of $4.56/share, an 82.4% premium to last close, has been declared final. The price corresponds to the subscription of 329mn domestic shares (~47.16% of the existing issued domestic shares and ~24.02% of the existing total issued shares) @$4.56/share by HEC in January this year.

Of greater significance, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors can justify recommending an Offer to shareholders at any price which gave cash less cavalier than cash.

Dissension rights are available, however, what constitutes a “fair price” under those rights, and the timing of the settlement under such rights, are not evident.

As all PRC approvals have been obtained, this transaction may complete earlier than prior mergers by absorption, which have taken 6-8 months from the initial announcement.

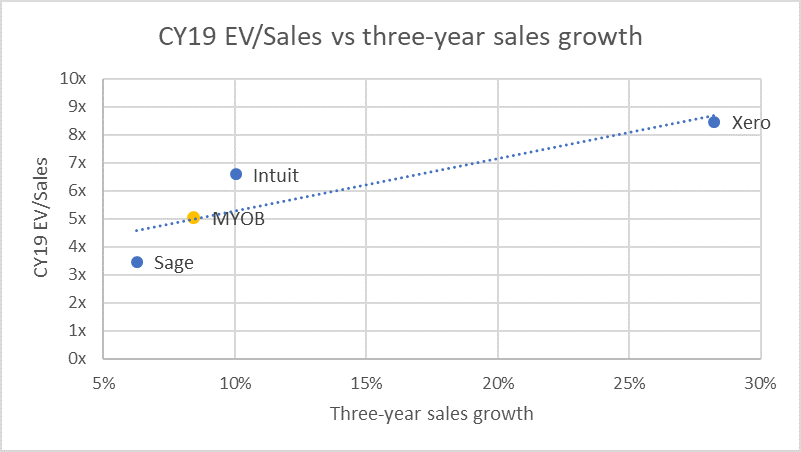

2. MYOB (MYO AU): Shareholders Are Caught Between a Rock and a Hard Place

On 24 December, MYOB Group Ltd (MYO AU) announced that it entered into a scheme implementation agreement under which KKR will acquire MYOB at $3.40 per share, which is 10% lower than 2 November offer price of A$3.77. MYOB claims its decision to recommend KKR’s lower offer was based on current market uncertainty, long-term nature of its strategic growth plans and the go-shop provisions of the deal.

We believe that KKR’s revised offer is opportunistic, but MYOB’s shareholders are caught between a rock and a hard place. Shareholders can take a short-term view and grudgingly accept the revised offer. Alternatively, shareholders can take a long-term view by rejecting the offer and hope MYOB’s strategic growth plans and a market recovery can reverse the inevitable share price collapse.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.