AsiaInfo Tech priced its IPO at HKD 10.50/share and will start trading today. Prior to the trading debut, in this short note, we summarize the latest information with updates on our valuation.

Tracking Traffic/Chinese Express & Logistics is the hub for our research on China’s express parcels and logistics sectors. Tracking Traffic/Chinese Express & Logistics features analysis of monthly Chinese express and logistics data, notes from our conversations with industry players, and links to company and thematic notes.

This month’s issue covers the following topics:

November express parcel pricing remained weak. Average pricing per express parcel fell by 7.8% Y/Y to just 11.06 RMB per piece. November’s average price represents a new all-time low for the industry, and November’s Y/Y decline was the steepest monthly decline in over two years (excluding Lunar New Year months, which tend to be distorted by the timing of the holiday).

Express parcel revenue growth dipped below 15% last month. Weak per-parcel pricing pulled express sector Y/Y revenue growth down to just 14.6% in November, the worst on record (again excluding distorted Lunar New Year comparisons). Chinese e-commerce demand has slowed and we suspect ‘O2O’ initiatives, under which online purchases are fulfilled via local stores, are also undermining express demand growth.

Intra-city pricing (ie, local delivery) remains firm relative to inter-city. Relative to weak inter-city express pricing (where ZTO Express (ZTO US) and the other listed express companies compete), pricing for local, intra-city express deliveries remained firm. In the first 11 months of 2018, express pricing rose 1.7% Y/Y versus a -2.9% decline in inter-city shipments (international pricing fell sharply, -14.5% Y/Y). Relatively firm pricing on local shipments may make it hard for local food delivery companies like Meituan Dianping (3690 HK) and Alibaba Group Holding (BABA US) ‘s ele.me to beat down unit operating costs.

Underlying domestic transport demand held up well again in November. Although demand for speedy, relatively expensive express service (and air freight) appears to be moderating, demand for rail and highway freight transport has held up well. The relative strength of rail and water transport (slow, cheap, industry-facing) versus express and air freight (fast, expensive, consumer-oriented) suggests a couple of things: a) upstream industrial activity is stronger than downstream retail activity and b) the people in charge of paying freight are shifting to cheaper modes of transport when possible.

We retain a negative view of China’s express industry’s fundamentals: demand growth is slowing and pricing appears to be falling faster than costs can be cut. Overall domestic transportation demand, however, remains solid and shows no signs of slowing.

Elastic NV (ESTC US) has been one of the best tech IPOs globally in 2018. Its current price is $62.53, up 74% from its IPO price of $36. Elastic’s share price has been holding up very nicely since its IPO on October 5th, 2018. Meanwhile, from October 5th to December 21st 2018, many tech stocks have experienced brutal declines. Elastic’s ability to outperform the top US tech stocks in a very difficult environment for the stock market sets the stage for a continued out-performance once the stock market starts to stabilize.

Since the IPO, the company reported better than expected second quarter results (quarter ending October 31, 2018) on December 4th. The company’s adjusted net loss in FY2Q19 was $0.38 per share, beating analysts’ consensus estimate by 9 cents. It generated revenue of $63.6 million, up 72% YoY. Calculated billings were also strong at $88.5 million, up 73% YoY.

The company’s guidance for FY3Q19 (quarter ending January 31, 2019) is to generate revenue in the range of $64 million to $66 million, representing a 56% YoY growth rate at the midpoint of the guidance. It expects to generate operating margin of negative 28% to negative 30% in FY3Q19.

A combination of major investors shifting their assets away from FAANG and semiconductor stocks has resulted in some improved performance of many software related stocks in recent months relative to other major tech stocks. In general, these stocks face less negative impact from a prolonged trade war between China and the US. Plus, theyare not as exposed to the higher cycle volatility as the semiconductor related stocks. In many respects, Elastic shares many business similarities with these software driven companies, and thus has been more immune from the decline in the stock prices since early October. We remain positive on Elastic NV (ESTC US).

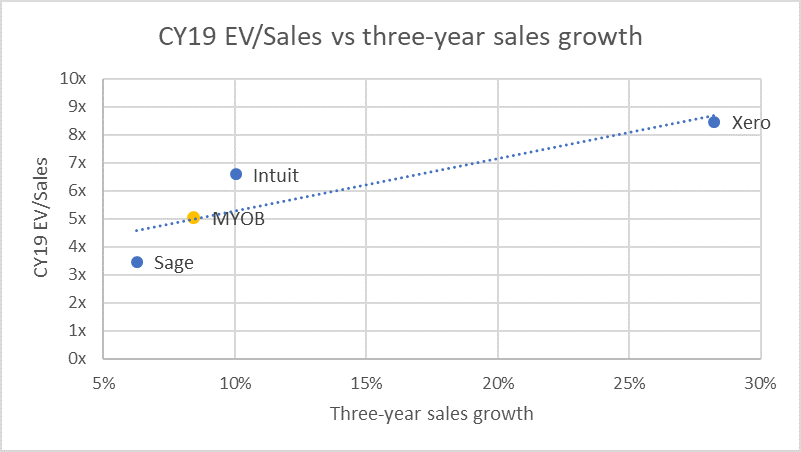

A last-minute lump of coal in the stocking from accounting software and services provider MYOB Group Ltd (MYO AU)?

Kohlberg Kravis Roberts has reduced its indicative offer to $3.40 from $3.77 after sifting through MYOB’s books, with MYOB announcing:

Following completion of due diligence and finalisation of debt funding commitments, KKR has revised the offer price to $3.40 per share. … The board has informed KKR that it is not in a position to recommend the revised proposal, however it remains in discussions with KKR regarding its proposal. (my emphasis)

KKR’s revised non-binding proposal is scheduled to expire at 5pm Friday, providing a day and change for MYOB to sound out shareholders as to the next move. Either the lower tilt is grudgingly accepted, or MYOB rejects and KKR walks away (for now), or goes hostile.

Either way, with MYOB’s VWAP above the revised proposal on all but 6 days since the initial announcement on the 8 October and $3.47/share on average, there won’t be a lot of Ho Ho Ho’ing.

Shares are down 11% as I type, implying 13% upside and 11% downside (using the ASX performance-adjusted price) or ~18% downside when pegged to peers. That’s not an attractive risk/reward heading into year-end.

On December 18th, the Korean government announced numerous measures to reduce fine dust levels, including a significant increase in the number of hydrogen powered vehicles, including expandinghydrogen vehicles to 65,000 units by 2022 (cumulative).

The Korean government wants to encourage the growth of hydrogen powered economy and position the country as one of the global leaders in this segment. The Korean government plans to spend about 3.5 trillion won to support the Korean auto industry. The Korean government’s new plan is to expand the hydrogen vehicles to 65,000 units by 2022, which is a big increase from the previous plan of expanding the hydrogen vehicles to 15,000 units by 2022.

The Hyundai Motor Group also recently announced a grand plan to expand its fuel cell vehicles with the announcement of its ‘FCEV Vision 2030.’ The Hyundai Motor Group plans to increase its annual production capacity for fuel cell systems to 0.7 million units by 2030, with plans to invest about $7 billion in the next 10 years to develop hydrogen fuel cell systems.

There is an extensive history of writing on the NTT (Nippon Telegraph & Telephone) (9432 JP) family (and indeed Japan telecom sector) buybacks – their modalities and methods, impacts, legal and accounting requirements, competition, push-me-pull-you effect, etc.

One of the longstanding features of buybacks for NTT is that NTT is subject to the NTT Law which requires (for the moment) that the government hold at least one-third of the shares outstanding in NTT.

Today, the Nikkei carried an article noting that the Japanese government’sFY2019 budget currently being formed proposes a sale of JPY 160bn of shares to help fund any revenue impact from the upcoming consumption tax rate hike from 8% to 10% next October. The article helpfully notes that they plan on selling when NTT is buying back shares.

This news is not unexpected to Smartkarma readers of the ongoing series. And there are implications and read-throughs.

Over the weekend I published Softbank Corp, Takeda, and Newton’s Three Laws of Motion. Newton’s Three Laws helpfully guide one to understanding the nature of interaction of forces and bodies and the motion which results. Later, Euler’s laws of motion applied a framework for rigid and continuum bodies, and since then “action at a distance” has been replaced be Einstein’s Theory of General Relativity.

After I wrote the bit about one part of the index impact, FTSE unhelpfully changed their mind on timing based on an unhelpful change by the LSE. On Monday, the TSE exercised its discretion – clearly stated in the TOPIX Index Guidebook on p4 (2nd sentence of the opening paragraph) as something it may do – to go its own course in how it will adapt index changes to the first couple of increases in share count due to mergers with foreign corporations.

If an event not specified in this document occurs, or if TSE determines that it is difficult to use the methods described in this document, TSE may use an alternative method of index calculation as it deems appropriate.

So with the changes at FTSE and now TOPIX and JPX Nikkei 400, we no longer have quite the same clarity of forces on the bodies, and therefore less clarity on the resulting motion. The LSE’s announced market change appears to have led the MSCI to change its deletion date for Shire as well, now also (along with FTSE) deleting Shire at the close of the 21st (announcement early this AM Asia time).

Investors have prepared based on the idea that there was a reasonably tight relationship – helped because it was a lot of force applied in a short period (selling and buying all done in a short period in January) between the particles. Now that relationship is being stretched. A lot.

The problem resembles that which Einstein famously pooh-poohed as “Spooky Action At a Distance”. Schrödinger called this entanglement – and it turns out to be one of the weirder branches of quantum mechanics – a field broken wide open by Bell’s Theorem a decade after Einstein shuffled off this mortal coil* – and about which John Wheeler famously said, “If you are not completely confused by quantum mechanics, you do not understand it.”

I cheerfully say quantum mechanics completely baffles me.

I less cheerfully say this whole episode with Takeda and index providers has baffled me too.

But it is important to note that the timing and implications are vastly different than expected just two trading days ago. And the difference is worth thinking about. When the FTSE/MSCI net sell of risk was just 3 days apart, there was a clear connection across that three day distance. Now, the 6-10 week spread of time between the FTSE/MSCI events, the weird two weeks of SETSqx illiquid purgatory just as everyone is full up of risk, then the walk through the Valley of the Shadow of Flowback before we get the first really good net index inclusion to cover the Shire risk people have been dumping for months means that the certainty of understanding the movement of the particle on the other side is substantially lower.

If it all works out well, it might just be Spooky Action At a Distance.

*And there, of course, you have the third Hamlet reference this month… I haz all your Shakespeares!

Hitachi Ltd (6501 JP) announced the acquisition of an 80.1% stake in ABB Ltd (ABBN VX)’s power grids business for $6.4 billion. ABB will retain the remaining stake in the divested unit, which is valued at an EV of $11 billion. ABB’s power grids is a global #1 player and makes transformers, long distance electricity-transmission systems and energy storage units.

Setting aside the huge cultural and integration challenges, we believe that Hitachi’s acquisition of ABB’s power grids is a bold but a risky move.

Satellite companies attempting to convince the Federal Communications Commission to allow them to sell C-band spectrum they license from the U.S. have begun talks to secure customers, sources told CTFN.

Softbank Group (9984 JP) is set to raise JPY2.65 trillion ($23.5 billion) through the Softbank Corp (9434 JP) IPO, Japan’s biggest-ever IPO. However, SoftBank Corp’s IPO which is set for 19 December is oversubscribed by less than double, according to press reports. This level of oversubscription is well below blockbuster Japanese stock debuts such as Mercari Inc (4385 JP) and Recruit Holdings (6098 JP).

Based on client discussion on SoftBank Corp’s intrinsic value, we have put together a DCF-based valuation along with scenario analysis. Our conclusion remains the same that SoftBank Corp is overvalued at the proposed IPO price of JPY1,500 per share.

Although we were bearish on the IPO initially and turned increasingly so following the relatively poor reception among retailers that was discussed in Softbank IPO: Signs Point to Risk of Early IPO Price Break, we were still a touch surprised at the extent of the drop today, with the stock finishing down 14.53% to close at the lows with 271.5m shares changing hands. With a rising dividend yield and looming buying from passive funds on the on hand and a potentially large overhang from retailers who may have been looking to flip for a profit on the other, we discuss what would turn us more bullish below.

Softbank Group (9984 JP)’s market cap has consistently traded below its NAV. A popular expectation was that the Softbank Corp (9434 JP) IPO should be a catalyst to narrow the conglomerate discount (holdco discount). On its trading debut today, SoftBank Corp’s shares fell 14.5% from its IPO price of JPY1,500 to JPY1,282 per share – the worst first-day decline ever for a major IPO in Japan since the Japan Display (6740 JP) IPO in 2014.

In our previous research, we stated that the SoftBank Corp IPO is unlikely to meaningfully narrow SoftBank’s holdco discount. Our updated SoftBank SoTP analysis which reflects SoftBank Corp’s trading debut suggests that SoftBank’s holdco discount has not meaningfully narrowed.

We believe that TME is fairly valued based on peer companies’ price / sales ratios.

The Chinese internet peer companies as comparison bases in valuation have declined significantly more than indices, we believe it is not a concern that indices declined further.

We believe that the main business of music will grow strongly in 2019 and 2020 due to the rapid growth of both the paying user base and ARPU (Average Revenues per User per month).

AsiaInfo Tech priced its IPO at HKD 10.50/share and will start trading today. Prior to the trading debut, in this short note, we summarize the latest information with updates on our valuation.

Bloomberg reported Softbank Corp (9434 JP)‘s international bookbuild was 2 – 3x covered while retail offering was at almost 2x. There were other reports of bookrunners struggling to sell shares to retail investors.

In this insight, we will look at how peers and market have performed since bookbuild and provide a sensitivity table with implied valuations for different price points and thoughts on the price range for near-term trading.

We have already covered most aspects of Softbank Corp (9434 JP) ‘s IPO in our previous insights:

On 24 December, MYOB Group Ltd (MYO AU) announced that it entered into a scheme implementation agreement under which KKR will acquire MYOB at $3.40 per share, which is 10% lower than 2 November offer price of A$3.77. MYOB claims its decision to recommend KKR’s lower offer was based on current market uncertainty, long-term nature of its strategic growth plans and the go-shop provisions of the deal.

We believe that KKR’s revised offer is opportunistic, but MYOB’s shareholders are caught between a rock and a hard place. Shareholders can take a short-term view and grudgingly accept the revised offer. Alternatively, shareholders can take a long-term view by rejecting the offer and hope MYOB’s strategic growth plans and a market recovery can reverse the inevitable share price collapse.

As per reports, Infosys Ltd (INFO IN) may consider a proposal for a share buyback of $1.60 billion very soon. The buyback announcement is likely to be made on January 11 when the company board meets to consider the 3Q FY19 results. Before this, in November 2017, Infosys Ltd (INFO IN) had announced a buyback and spent Rs130 bn to buy a total of 113mn equity shares. This fresh buyback could be an important development and could be an important support for the stock, it is also sensible for other reasons.

There are no major acquisitions in recent times by Infosys Ltd (INFO IN) and if this is likely to be the trend for near future, share buyback is not a bad idea. The company is still struggling with some of the legacy issues and the priority as of now is to streamline the organic growth. We think Infosys Ltd (INFO IN) is also cautious with inorganic growth opportunities as the company had serious issues with acquisitions in the past. What could be another key driver behind this is that in valuation terms, Infosys Ltd (INFO IN) is not very expensive.

During the second half of December 2018, Japan saw two telecom companies list on the Tokyo Stock Exchange: Softbank Corp (9434 JP) and ARTERIA Networks (4423 JP). After years of industry consolidation, which saw several stocks delist, this felt like a Christmas miracle (at least for those watching the sector’s stocks).

It would be hard to find two companies in the same industry that are so different – both in their business models as well as in how their IPOs were positioned to investors. One stock is 100 times larger than the other, but this is not a story of David and Goliath. It is two unique stories in parallel.

While each company took a very different approach to selling its stock, both have suffered from the subsequent broader market weakness, irrespective of company specifics. We can’t say it has been the worst of times, but it certainly has been a tough time with SoftBank Corp down 13% and Arteria down 20% from their IPO prices.

In this Insight we explore how each company approached its IPO and how each has fared since.

After securing a 19.9% stake from Bain in early October and initially pitching A$3.70/share, in a textbook bear hug, KKR (marginally) bumped its indicative offer to A$3.77/share to a get a look under the hood, then following seven weeks of due diligence, backtracked with a lower price of A$3.40/share, citing adverse market conditions.

MYOB Board’s response last week to the reduced offer was to inform KKR that it is not in a position to recommend the revised proposal, however, “it remains in discussions with KKR regarding its proposal”, leaving the door open for ongoing negotiations. KKR for its part, said there were no landmines following the DD process. The price action last Friday suggested the outcome was a coin toss.

Today, KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal and subject to an independent expert concluding the Offer is in the best interest of shareholders. The Offer price assumes no full-year dividend is paid.

The agreement provides a “go shop” provision until the 22 February 2019 – when MYOB is expected to release its FY18 results – to solicit competing proposals.

The Offer appears reasonable when compared to peers and with regards to the 14% decline in the ASX technology index; but conversely, could be construed as being opportunistic.

A Scheme Booklet is expected to be dispatched mid-March with an estimated implementation date of 3 May. Currently trading at a 3.8%/11% gross/annualised spread. 1 January makes a new year and there will be investors who would want to take an agreed deal at 11%.

Improving asset turnover, good risk adjusted price momentum, and relatively strong analyst recommendations relative to its sector

Larger distribution channel through acquisition of DNA Retail Link to add 95 more stores to current 518 stores

New mobile product launches in 4Q18 and COM7’s focus on high margin products, such as Android smartphones, should support high earnings growth which was up 56% YoY in 3Q18

Attractive at a 19CE* PEG of 0.9 versus ASEAN sector at a PEG of 2.7

Risks: Lower-than-expected demand for new IT products, slower-than-expected store expansions

It has been a huge Q4 for Japan capital markets and banking, and the result is some fat fees for global investment bankers on the Takeda/Shire deal, and a Softbank Corp IPO which I’d be totally OK not owning. A result of this activity is the fun in index land.

Amer Sports Oyj (AMEAS FH)announced (ANTA’s is here) an Offer at €40/share (a 39% premium to the undisturbed price of 10 September 2018), and announced that the Board of Directors of Amer Sports has decided to unanimously recommend that Amer Sports’ shareholders accept the Tender Offer. Several major shareholders holding 7.91% have irrevocably undertaken to tender, and Maa-ja vesitekniikan tuki r.y., who hold ~4.29%, have expressed that they view the Tender Offer positively. ANTA indirectly holds 1,679,936 shares (1.4%) as well.

ANTA and consortium appear to have the funding. As suspected and discussed in the original doc, FountainVest is a fair bit smaller than 50%. The equity stakes are, indirectly, 57.95% ANTA, 15.77% FountainVest, 5.63% Tencent Holdings (700 HK), and 20.65% Anamered Investments (Chip Wilson’s vehicle). There is a Shareholders’ Agreement which allows FountainVest the right to effect a Trade Sale if a “Qualified IPO does not take place within 5 years”, which seems reasonable. This effectively means that the company will be put up for sale in 5yrs.

It should be 11.5 weeks from Monday to Tender Offer completion, with 81-83 days between trade settlement and payment for Tender shares. That is ~27.1% annualized as of Friday’s close. This spread should drop at least by half after the Tender Launch scheduled for 20 December. Anti-trust and other authorities’ approval will be required. If ANTA gets over 90% of the shares, they intend to commence mandatory redemption (squeezeout) proceedings.

It should be noted that this deal offers significant leverage to ANTA and even more to the minority investors. ANTA is effectively collateralizing some LBO debt with its own earnings. As ANTA will not consolidate, the only way to see the numbers will be to look through the affiliate income. The saving grace here for everyone may be that it is remote from ANTA, which means transfer pricing will be carefully watched.

NHK reported JDI was in talks to sell about a 33% stake to a Chinese consortium for $440m (probably ¥50bn) which would value the company at about 3.5x (at the time) its current market cap. INCJ is also, apparently, considering support. These moves would go a long way toward restoring the company’s beaten-up balance sheet and the cost cuts should allow the company to survive – although Apple’s struggles still cast a shadow on a return to a strong level of profitability. JDI’s share price shot up 34.6% on the news on Friday.

JDI’s massive share price drop since its listing has been due to its weakened balance sheet and a slow shift to OLED, which this reported funding will go some way to addressing. Mio Kato, CFA‘s view is that JDI has some very promising businesses and the company is undervalued.

JDI still has an unhealthy over-dependence on Apple but they are doing everything they can to dilute the influence, increasing automotive display sales at double-digit rates and maintaining and growing their top market share in that segment, as well as producing more VR and notebook LTPS screens.

There still remains excess capacity in the industry due to Chinese government subsidies for display panel manufacturers and an over-ambitious build-out of both LTPS and OLED capacity. This is not going to improve drastically anytime soon but some of the planned OLED capacity expansions are being pushed out and much of the LTPS capacity increases have already been completed.

After Pioneer revealed in September it had sold its Tohoku Pioneer subsidiary to Denso Corp (6902 JP) for ¥10.9bn, it announced an MOU with Barings and went into debt to them. That seemed like “the end of the line” for the company. Pioneer needed a sponsor, but it was going to stay listed. Last week,Pioneer announced a “Partnership” with Baring Private Equity Asia which is a revitalization plan of ¥102bn. The deal offers minority shareholders an exit. The announcement does not mention investors are effectively being asked to approve their own squeezeout at 25% below the last price.

In the deal as presented, shareholders are being asked to approve an exit price 75% below 52-week highs which came AFTER the capital reduction in summer 2017, and after the sale of assets earlier this year, sell their shares at roughly one-third of existing book value per share, and sell its 3D LiDAR business and technology for… zero.

There are caveats. ALL of Pioneer’s net equity is intangibles. It has payables higher than receivables as of the end of September, and ¥25bn in net debt (increased by the ¥25bn lent by Baring). The company has roughly 2.5x EBITDA in inventory, and in a company which is losing money by being in business, inventory as marked is not as good as cash. The company has close to ~¥30bn in underfunded pension liabilities.

Travis does not expect a public activist outcry. Activists who wanted to buy into this have already done so. Any who do going forward have no vote because the record date for the vote was 7 December.

On December 3rd, the boards of both Hindustan Unilever (HUVR IN) (“HUL”) and GlaxoSmithKkine (“GSKCH”) approved a merger (subject to regulatory and shareholder approval) – at an exchange ratio of 4.39 HUL shares for every 1 GSKCH share – in a £3.1 bn deal. Combining with GSKCH should see HUL leapfrog both Britannia Industries (BRIT IN)and Nestle India (NEST IN)in food and refreshment revenue, and put it roughly on level pegging with ITC Ltd (ITC IN).

Approvals should be a foregone conclusion. With neither Unilever or GSK required to abstain, the 75% shareholder approval threshold is all but a lock. GSKCH’s shareholders get the benefit of HUL’s vast distribution network, while HUL gets a better understanding of the pharma channel.

Regulatory approval should not be an issue. 90% of cases handled by India’s anti-trust body CCI have been approved without the requirement for any modification. There is minimal overlap here – this is HUL’s big splash to build a sustainable and profitable food and refreshment business in India. Greater opposition would be expected if either BRIT, NEST or ITC made a tilt for GSKCH.

The transaction should be completed in one year, subject to regulatory and shareholder approvals. It’s a long-dated, but low-risk deal. Expect the tight spread to remain tight – this deal may close faster than the “expected” one-year timeframe.

Red Hat has set a meeting date of January 16, 2019 for shareholders to vote on the merger agreement withIntl Business Machines (IBM US), and related matters. Red Hat also set a record date of December 11th, 2018 for shareholders entitled to vote on the deal.

The fact the meeting date has been set means the SEC chose not to review the merger proxy (a less common occurrence than a review) and notified the companies of this decision within the expected 10 calendar days.

While the Company issued the press release, a new proxy has not yet been filed. John DeMasi expects we will see a definitive merger proxy filed within the next few days. Since the HSR U.S. antitrust 30 day waiting period will not expire until December 21st, he doesn’t expect an update on HSR in the definitive proxy, and it still appears the EC Competition filing has not been made according to the EC website.

John believes the deal is still on track for a Q2/Q3 2019 close and believes the risk/reward looks attractive here.

Reportedly, preliminary discussions are underway between NineEntertainment Co Holdings (NEC AU) and MRN’s second-largest shareholder, John Singleton. This development is not entirely unsurprising; it appears formal discussions were deferred until the Nine/Fairfax Media (FXJ AU) merger was formally completed (which occurred on 7 December). Nine acquired Fairfax’s 54.5% stake in MRN in the merger, discussed in my insight Nine & Fairfax – Integrated Advertising.

Also reported in the press, Nine has offered $2/share (a 9.3% premium to the closing price of A$1.83 on December 4th), with Singleton (a willing seller) believed to be holding out for $2.15/share. In a further twist, Alan Jones, with 1.27% of MRN, is understood to have certain conditions/clauses attached to that stake, which may make an offer tabled by Nine potentially untenable.

MRN was trading between A$1.20 and A$1.60 during the first half of the year. Following the announcement of the Nine-Fairfax merger in July, the share price reached a high of A$2.18. While the expected offer price of A$2.00 is 8.3% lower than this lifetime high, it is still 26% higher than the stock’s undisturbed price of A$1.59 before the Nine-Fairfax merger deal was announced.

Nine is interested in mopping up shares in MRN it does not already own. John Singleton is a seller, at the right price. Nine’s CEO Hugh Marks is keen to move quickly, not just taking full control of MRN, but also divesting assets that do not focus on digital subscriptions, mass audiences andnational advertisers. It’s now a question of how much Nine is willing to pay, and the added benefits therein to Nine from a privatisation compared to its current majority and consolidating stake.

While Inc and Healthcare are not cross-linked by any shareholding, Healthcare is ostensibly Celltrion’s internal sales arm. Their fundamentals and prices should be (& are) highly correlated.

Sanghyun initiated a pair trade (short Celltrion / long Healthcare) on Oct 22. The ongoing FSS investigation is hammering both, Healthcare more so as it is more directly exposed. But given what happened to Samsung Biologics Co., (207940 KS), it is very unlikely that this will be a serious risk.

Sigma Healthcare had seen its share price fall 70% in 18 months after its relationship with MyChemist/Chemist Warehouse went sour in 2017, then their existing contract was not renewed for post-June 2019. This appears to be because Sigma did not want to continue trading under overly-generous (to MC/CW) terms and capital usage.

In September, API started buying shares in Sigma Healthcare on the market when they were down by half from the July 2017 news, buying just under 5% before approaching Sigma with an Indicative Proposal to Merge in a Scheme. Sigma responded saying it was willing to engage with API, but API did not respond in the subsequent months it appears. Thursday API bought half of Allan Gray’s stake to lift its own stake to 13.95%, then it publicly announced the same Indicative Proposal.

So now we wait. There is a business review in progress. Full year results for Sigma are due in March. ACCC clearance may take until mid-year.

The deal is at a nice premium – 46.8% to the one-month average, and 69% to the day before. It was about 10% better than where API started buying.

But it may not be good enough. The deal offers some cash, but also offers expensive scrip. API appears to need this deal as much as some would say Sigma does.

Sigma is in the process of doing a zero-based full business review with Accenture and indications are that everyone thinks the company is worth a lot more than where it was trading last week.

This deal looks like it has a big premium but it may not be enough.

Huatai Securities Co Ltd (A) (601688 CH)(and Huatai H) announced that the CSRC had given the company approval to list up to (but not more than) 82,515,000 GDRs. The English language LSE announcement of the “Intention to Float” can be found here and here. Each GDR represents 10 A shares, that is up to RMB13.7bn at the (then) last traded price of the A shares prior to the announcement. If all the shares were issued that would be about 10% of the share capital of Huatai (pre-issuance). This GDR launches the London side of the London-Shanghai Connect. A prospectus is expected in the new year.

Assuming the GDRs trade similarly to the Hs, or even 1% of their maximum issuance quantity, and assuming they have a similar discount to the As as do the Hs, the GDRs will not likely trade more volume than the H Shares.

It is not clear WHY the GDRs would, over time, maintain a tighter discount to the A Shares than the H Shares would …. Except for the fungibility. Which may be the only reason to hold the GDRs at a 20% discount when you can get the H-shares at a 30+% discount. But the system may not be ready to handle GDR creation by mainland domestic investors trying to export capital, even at a discount.

The whole deal comes across as somewhat iffy. It is not clear why the deal needs to be done other than to fill a political need to get the ball rolling. But one wonders why the London-Shanghai Connect ball actually needs to be rolled.

Naspers’ recent underperformance against Tencent has resulted in the discount to NAV widening to near-on 12 months lows. While Naspers remains a function of what happens to Tencent, it offers potentially interesting long-term prospects.

This pseudo-venture capital company is taking steps to narrow the valuation gap via the reduction in its Tencent stake, the sale of successful investments (Flipkart and tbogroup), the listing of profitable entities (Multichoice), the investment in specific areas (classifieds, online retail, payments businesses and food delivery), working to reduce its exposure to the Johannesburg Stock Exchange, and perhaps pursue a dual listing outside of SA, such as Hong Kong. To me, Naspers’ risk profile appears attractive here.

New Street Research‘s Alastair Jones views the most recent Naspers results as broadly positive with continued progress in profitability from its e-commerce assets. He also believes that, given moves to unbundle the pay-TV assets in 2019, there is scope for the NAV discount to narrow. The current low/negative valuation for the unlisted assets ignores their significant value.

Curtis Lehnert recommends a Toyota Industries’ set-up at current levels which are in excess of -2 Standard Deviations below the long-term average, while Toyota Industries is trading at a 35% discount to his NAV – Toyota Industries’ stake in Toyota Motor accounts for 60%).

The group boasts the #1 global market share in forklifts with an estimated 20% market share. Toyota Industries’ closest competitor in the materials handling business is KION Group AG (KGX GR); however, Curtis estimates the market is implying 0.83x for these ops, 28% lower than Kion’s 1.15x.

Newton’s Three Laws of Motion And How They Pertain to Index Inclusions

Travis Lundy noted that Newton’s Third Law, commonly understood that for every action there is always an equal and opposed reaction, applies in some measure to index inclusions.

For every index upweight, there is an equal and opposite downweight.

Travis published his H/A Spread Monitor Project offering a brief look at recent changes in H-Share and A-Share spreads, Southbound flow and impact, and where the spreads are trading within their own historical ranges. My share class monitor provides a snapshot of the premium/discounts for 215 share classifications around the region. Ke Yan, CFA, FRM issued his Discover HK Connect series, to help understand the flow of southbound trades via the Hong Kong Connect.

The 1P (005385 KS)/ 2P (005387 KS) dividend yield difference of 0.53% is close to a year high. Of interest is the recently announced hydrogen cell investment, which may be considered a signal that the HMG-government relation has vastly improved. This potentially suggests that any HMG restructuring may get accelerated, which would be positive for 1P. (link to Sanghyun’s insight: Hyundai Motor Share Class: Time for 1P to Catch Up)

OTHER M&A UPDATES

Trade Me (TME NZ)and Apax Partners have entered into a scheme implementation agreement. Apax Funds have increased their offer price to $6.45/share (from $6.40) since the indicative proposal, following the completion of their due diligence. The Board has unanimously backed the offer. A booklet containing information relating to the scheme is expected to be mailed to Trade Me shareholders in March 2019. The Board expects that Trade Me shareholders will have the opportunity to vote on the scheme at a meeting in April 2019. If all the conditions are satisfied, the scheme is expected to be implemented in the second quarter of 2019. Hellman & Friedman was not expected to materially counter and promptly pulled out of the race.

Cityneon Holdings (CITN SP). West Knighton now has 98.6% of shares out and will move to compulsory acquire shares it does not own. The closing date has been extended until the 26 December.

Sinotrans Shipping (368 HK). As expected from the onset, shareholders approved the privatisation. Turnout was low – around 47.6% of shareholders entitled to vote, did so. Friday was the last day of trading. Cheques are expected to be dispatched on or before the 22 Jan 2019.

Stanmore Coal (SMR AU)‘s has released the Target Statement. The board continues to recommend shareholders reject the $0.95/share unsolicited Golden Investments. The IFA has a fair value range of $1.48-$1.90/share. Shares closed at A$1.04 on Friday.

CCASS

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

After securing a 19.9% stake from Bain in early October and initially pitching A$3.70/share, in a textbook bear hug, KKR (marginally) bumped its indicative offer to A$3.77/share to a get a look under the hood, then following seven weeks of due diligence, backtracked with a lower price of A$3.40/share, citing adverse market conditions.

MYOB Board’s response last week to the reduced offer was to inform KKR that it is not in a position to recommend the revised proposal, however, “it remains in discussions with KKR regarding its proposal”, leaving the door open for ongoing negotiations. KKR for its part, said there were no landmines following the DD process. The price action last Friday suggested the outcome was a coin toss.

Today, KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal and subject to an independent expert concluding the Offer is in the best interest of shareholders. The Offer price assumes no full-year dividend is paid.

The agreement provides a “go shop” provision until the 22 February 2019 – when MYOB is expected to release its FY18 results – to solicit competing proposals.

The Offer appears reasonable when compared to peers and with regards to the 14% decline in the ASX technology index; but conversely, could be construed as being opportunistic.

A Scheme Booklet is expected to be dispatched mid-March with an estimated implementation date of 3 May. Currently trading at a 3.8%/11% gross/annualised spread. 1 January makes a new year and there will be investors who would want to take an agreed deal at 11%.

Improving asset turnover, good risk adjusted price momentum, and relatively strong analyst recommendations relative to its sector

Larger distribution channel through acquisition of DNA Retail Link to add 95 more stores to current 518 stores

New mobile product launches in 4Q18 and COM7’s focus on high margin products, such as Android smartphones, should support high earnings growth which was up 56% YoY in 3Q18

Attractive at a 19CE* PEG of 0.9 versus ASEAN sector at a PEG of 2.7

Risks: Lower-than-expected demand for new IT products, slower-than-expected store expansions

Tracking Traffic/Chinese Express & Logistics is the hub for our research on China’s express parcels and logistics sectors. Tracking Traffic/Chinese Express & Logistics features analysis of monthly Chinese express and logistics data, notes from our conversations with industry players, and links to company and thematic notes.

This month’s issue covers the following topics:

November express parcel pricing remained weak. Average pricing per express parcel fell by 7.8% Y/Y to just 11.06 RMB per piece. November’s average price represents a new all-time low for the industry, and November’s Y/Y decline was the steepest monthly decline in over two years (excluding Lunar New Year months, which tend to be distorted by the timing of the holiday).

Express parcel revenue growth dipped below 15% last month. Weak per-parcel pricing pulled express sector Y/Y revenue growth down to just 14.6% in November, the worst on record (again excluding distorted Lunar New Year comparisons). Chinese e-commerce demand has slowed and we suspect ‘O2O’ initiatives, under which online purchases are fulfilled via local stores, are also undermining express demand growth.

Intra-city pricing (ie, local delivery) remains firm relative to inter-city. Relative to weak inter-city express pricing (where ZTO Express (ZTO US) and the other listed express companies compete), pricing for local, intra-city express deliveries remained firm. In the first 11 months of 2018, express pricing rose 1.7% Y/Y versus a -2.9% decline in inter-city shipments (international pricing fell sharply, -14.5% Y/Y). Relatively firm pricing on local shipments may make it hard for local food delivery companies like Meituan Dianping (3690 HK) and Alibaba Group Holding (BABA US) ‘s ele.me to beat down unit operating costs.

Underlying domestic transport demand held up well again in November. Although demand for speedy, relatively expensive express service (and air freight) appears to be moderating, demand for rail and highway freight transport has held up well. The relative strength of rail and water transport (slow, cheap, industry-facing) versus express and air freight (fast, expensive, consumer-oriented) suggests a couple of things: a) upstream industrial activity is stronger than downstream retail activity and b) the people in charge of paying freight are shifting to cheaper modes of transport when possible.

We retain a negative view of China’s express industry’s fundamentals: demand growth is slowing and pricing appears to be falling faster than costs can be cut. Overall domestic transportation demand, however, remains solid and shows no signs of slowing.

Elastic NV (ESTC US) has been one of the best tech IPOs globally in 2018. Its current price is $62.53, up 74% from its IPO price of $36. Elastic’s share price has been holding up very nicely since its IPO on October 5th, 2018. Meanwhile, from October 5th to December 21st 2018, many tech stocks have experienced brutal declines. Elastic’s ability to outperform the top US tech stocks in a very difficult environment for the stock market sets the stage for a continued out-performance once the stock market starts to stabilize.

Since the IPO, the company reported better than expected second quarter results (quarter ending October 31, 2018) on December 4th. The company’s adjusted net loss in FY2Q19 was $0.38 per share, beating analysts’ consensus estimate by 9 cents. It generated revenue of $63.6 million, up 72% YoY. Calculated billings were also strong at $88.5 million, up 73% YoY.

The company’s guidance for FY3Q19 (quarter ending January 31, 2019) is to generate revenue in the range of $64 million to $66 million, representing a 56% YoY growth rate at the midpoint of the guidance. It expects to generate operating margin of negative 28% to negative 30% in FY3Q19.

A combination of major investors shifting their assets away from FAANG and semiconductor stocks has resulted in some improved performance of many software related stocks in recent months relative to other major tech stocks. In general, these stocks face less negative impact from a prolonged trade war between China and the US. Plus, theyare not as exposed to the higher cycle volatility as the semiconductor related stocks. In many respects, Elastic shares many business similarities with these software driven companies, and thus has been more immune from the decline in the stock prices since early October. We remain positive on Elastic NV (ESTC US).

A last-minute lump of coal in the stocking from accounting software and services provider MYOB Group Ltd (MYO AU)?

Kohlberg Kravis Roberts has reduced its indicative offer to $3.40 from $3.77 after sifting through MYOB’s books, with MYOB announcing:

Following completion of due diligence and finalisation of debt funding commitments, KKR has revised the offer price to $3.40 per share. … The board has informed KKR that it is not in a position to recommend the revised proposal, however it remains in discussions with KKR regarding its proposal. (my emphasis)

KKR’s revised non-binding proposal is scheduled to expire at 5pm Friday, providing a day and change for MYOB to sound out shareholders as to the next move. Either the lower tilt is grudgingly accepted, or MYOB rejects and KKR walks away (for now), or goes hostile.

Either way, with MYOB’s VWAP above the revised proposal on all but 6 days since the initial announcement on the 8 October and $3.47/share on average, there won’t be a lot of Ho Ho Ho’ing.

Shares are down 11% as I type, implying 13% upside and 11% downside (using the ASX performance-adjusted price) or ~18% downside when pegged to peers. That’s not an attractive risk/reward heading into year-end.

On December 18th, the Korean government announced numerous measures to reduce fine dust levels, including a significant increase in the number of hydrogen powered vehicles, including expandinghydrogen vehicles to 65,000 units by 2022 (cumulative).

The Korean government wants to encourage the growth of hydrogen powered economy and position the country as one of the global leaders in this segment. The Korean government plans to spend about 3.5 trillion won to support the Korean auto industry. The Korean government’s new plan is to expand the hydrogen vehicles to 65,000 units by 2022, which is a big increase from the previous plan of expanding the hydrogen vehicles to 15,000 units by 2022.

The Hyundai Motor Group also recently announced a grand plan to expand its fuel cell vehicles with the announcement of its ‘FCEV Vision 2030.’ The Hyundai Motor Group plans to increase its annual production capacity for fuel cell systems to 0.7 million units by 2030, with plans to invest about $7 billion in the next 10 years to develop hydrogen fuel cell systems.

There is an extensive history of writing on the NTT (Nippon Telegraph & Telephone) (9432 JP) family (and indeed Japan telecom sector) buybacks – their modalities and methods, impacts, legal and accounting requirements, competition, push-me-pull-you effect, etc.

One of the longstanding features of buybacks for NTT is that NTT is subject to the NTT Law which requires (for the moment) that the government hold at least one-third of the shares outstanding in NTT.

Today, the Nikkei carried an article noting that the Japanese government’sFY2019 budget currently being formed proposes a sale of JPY 160bn of shares to help fund any revenue impact from the upcoming consumption tax rate hike from 8% to 10% next October. The article helpfully notes that they plan on selling when NTT is buying back shares.

This news is not unexpected to Smartkarma readers of the ongoing series. And there are implications and read-throughs.

Although we were bearish on the IPO initially and turned increasingly so following the relatively poor reception among retailers that was discussed in Softbank IPO: Signs Point to Risk of Early IPO Price Break, we were still a touch surprised at the extent of the drop today, with the stock finishing down 14.53% to close at the lows with 271.5m shares changing hands. With a rising dividend yield and looming buying from passive funds on the on hand and a potentially large overhang from retailers who may have been looking to flip for a profit on the other, we discuss what would turn us more bullish below.

Softbank Group (9984 JP)’s market cap has consistently traded below its NAV. A popular expectation was that the Softbank Corp (9434 JP) IPO should be a catalyst to narrow the conglomerate discount (holdco discount). On its trading debut today, SoftBank Corp’s shares fell 14.5% from its IPO price of JPY1,500 to JPY1,282 per share – the worst first-day decline ever for a major IPO in Japan since the Japan Display (6740 JP) IPO in 2014.

In our previous research, we stated that the SoftBank Corp IPO is unlikely to meaningfully narrow SoftBank’s holdco discount. Our updated SoftBank SoTP analysis which reflects SoftBank Corp’s trading debut suggests that SoftBank’s holdco discount has not meaningfully narrowed.

We believe that TME is fairly valued based on peer companies’ price / sales ratios.

The Chinese internet peer companies as comparison bases in valuation have declined significantly more than indices, we believe it is not a concern that indices declined further.

We believe that the main business of music will grow strongly in 2019 and 2020 due to the rapid growth of both the paying user base and ARPU (Average Revenues per User per month).

It has been a huge Q4 for Japan capital markets and banking, and the result is some fat fees for global investment bankers on the Takeda/Shire deal, and a Softbank Corp IPO which I’d be totally OK not owning. A result of this activity is the fun in index land.

Amer Sports Oyj (AMEAS FH)announced (ANTA’s is here) an Offer at €40/share (a 39% premium to the undisturbed price of 10 September 2018), and announced that the Board of Directors of Amer Sports has decided to unanimously recommend that Amer Sports’ shareholders accept the Tender Offer. Several major shareholders holding 7.91% have irrevocably undertaken to tender, and Maa-ja vesitekniikan tuki r.y., who hold ~4.29%, have expressed that they view the Tender Offer positively. ANTA indirectly holds 1,679,936 shares (1.4%) as well.

ANTA and consortium appear to have the funding. As suspected and discussed in the original doc, FountainVest is a fair bit smaller than 50%. The equity stakes are, indirectly, 57.95% ANTA, 15.77% FountainVest, 5.63% Tencent Holdings (700 HK), and 20.65% Anamered Investments (Chip Wilson’s vehicle). There is a Shareholders’ Agreement which allows FountainVest the right to effect a Trade Sale if a “Qualified IPO does not take place within 5 years”, which seems reasonable. This effectively means that the company will be put up for sale in 5yrs.

It should be 11.5 weeks from Monday to Tender Offer completion, with 81-83 days between trade settlement and payment for Tender shares. That is ~27.1% annualized as of Friday’s close. This spread should drop at least by half after the Tender Launch scheduled for 20 December. Anti-trust and other authorities’ approval will be required. If ANTA gets over 90% of the shares, they intend to commence mandatory redemption (squeezeout) proceedings.

It should be noted that this deal offers significant leverage to ANTA and even more to the minority investors. ANTA is effectively collateralizing some LBO debt with its own earnings. As ANTA will not consolidate, the only way to see the numbers will be to look through the affiliate income. The saving grace here for everyone may be that it is remote from ANTA, which means transfer pricing will be carefully watched.

NHK reported JDI was in talks to sell about a 33% stake to a Chinese consortium for $440m (probably ¥50bn) which would value the company at about 3.5x (at the time) its current market cap. INCJ is also, apparently, considering support. These moves would go a long way toward restoring the company’s beaten-up balance sheet and the cost cuts should allow the company to survive – although Apple’s struggles still cast a shadow on a return to a strong level of profitability. JDI’s share price shot up 34.6% on the news on Friday.

JDI’s massive share price drop since its listing has been due to its weakened balance sheet and a slow shift to OLED, which this reported funding will go some way to addressing. Mio Kato, CFA‘s view is that JDI has some very promising businesses and the company is undervalued.

JDI still has an unhealthy over-dependence on Apple but they are doing everything they can to dilute the influence, increasing automotive display sales at double-digit rates and maintaining and growing their top market share in that segment, as well as producing more VR and notebook LTPS screens.

There still remains excess capacity in the industry due to Chinese government subsidies for display panel manufacturers and an over-ambitious build-out of both LTPS and OLED capacity. This is not going to improve drastically anytime soon but some of the planned OLED capacity expansions are being pushed out and much of the LTPS capacity increases have already been completed.

After Pioneer revealed in September it had sold its Tohoku Pioneer subsidiary to Denso Corp (6902 JP) for ¥10.9bn, it announced an MOU with Barings and went into debt to them. That seemed like “the end of the line” for the company. Pioneer needed a sponsor, but it was going to stay listed. Last week,Pioneer announced a “Partnership” with Baring Private Equity Asia which is a revitalization plan of ¥102bn. The deal offers minority shareholders an exit. The announcement does not mention investors are effectively being asked to approve their own squeezeout at 25% below the last price.

In the deal as presented, shareholders are being asked to approve an exit price 75% below 52-week highs which came AFTER the capital reduction in summer 2017, and after the sale of assets earlier this year, sell their shares at roughly one-third of existing book value per share, and sell its 3D LiDAR business and technology for… zero.

There are caveats. ALL of Pioneer’s net equity is intangibles. It has payables higher than receivables as of the end of September, and ¥25bn in net debt (increased by the ¥25bn lent by Baring). The company has roughly 2.5x EBITDA in inventory, and in a company which is losing money by being in business, inventory as marked is not as good as cash. The company has close to ~¥30bn in underfunded pension liabilities.

Travis does not expect a public activist outcry. Activists who wanted to buy into this have already done so. Any who do going forward have no vote because the record date for the vote was 7 December.

On December 3rd, the boards of both Hindustan Unilever (HUVR IN) (“HUL”) and GlaxoSmithKkine (“GSKCH”) approved a merger (subject to regulatory and shareholder approval) – at an exchange ratio of 4.39 HUL shares for every 1 GSKCH share – in a £3.1 bn deal. Combining with GSKCH should see HUL leapfrog both Britannia Industries (BRIT IN)and Nestle India (NEST IN)in food and refreshment revenue, and put it roughly on level pegging with ITC Ltd (ITC IN).

Approvals should be a foregone conclusion. With neither Unilever or GSK required to abstain, the 75% shareholder approval threshold is all but a lock. GSKCH’s shareholders get the benefit of HUL’s vast distribution network, while HUL gets a better understanding of the pharma channel.

Regulatory approval should not be an issue. 90% of cases handled by India’s anti-trust body CCI have been approved without the requirement for any modification. There is minimal overlap here – this is HUL’s big splash to build a sustainable and profitable food and refreshment business in India. Greater opposition would be expected if either BRIT, NEST or ITC made a tilt for GSKCH.

The transaction should be completed in one year, subject to regulatory and shareholder approvals. It’s a long-dated, but low-risk deal. Expect the tight spread to remain tight – this deal may close faster than the “expected” one-year timeframe.

Red Hat has set a meeting date of January 16, 2019 for shareholders to vote on the merger agreement withIntl Business Machines (IBM US), and related matters. Red Hat also set a record date of December 11th, 2018 for shareholders entitled to vote on the deal.

The fact the meeting date has been set means the SEC chose not to review the merger proxy (a less common occurrence than a review) and notified the companies of this decision within the expected 10 calendar days.

While the Company issued the press release, a new proxy has not yet been filed. John DeMasi expects we will see a definitive merger proxy filed within the next few days. Since the HSR U.S. antitrust 30 day waiting period will not expire until December 21st, he doesn’t expect an update on HSR in the definitive proxy, and it still appears the EC Competition filing has not been made according to the EC website.

John believes the deal is still on track for a Q2/Q3 2019 close and believes the risk/reward looks attractive here.

Reportedly, preliminary discussions are underway between NineEntertainment Co Holdings (NEC AU) and MRN’s second-largest shareholder, John Singleton. This development is not entirely unsurprising; it appears formal discussions were deferred until the Nine/Fairfax Media (FXJ AU) merger was formally completed (which occurred on 7 December). Nine acquired Fairfax’s 54.5% stake in MRN in the merger, discussed in my insight Nine & Fairfax – Integrated Advertising.

Also reported in the press, Nine has offered $2/share (a 9.3% premium to the closing price of A$1.83 on December 4th), with Singleton (a willing seller) believed to be holding out for $2.15/share. In a further twist, Alan Jones, with 1.27% of MRN, is understood to have certain conditions/clauses attached to that stake, which may make an offer tabled by Nine potentially untenable.

MRN was trading between A$1.20 and A$1.60 during the first half of the year. Following the announcement of the Nine-Fairfax merger in July, the share price reached a high of A$2.18. While the expected offer price of A$2.00 is 8.3% lower than this lifetime high, it is still 26% higher than the stock’s undisturbed price of A$1.59 before the Nine-Fairfax merger deal was announced.

Nine is interested in mopping up shares in MRN it does not already own. John Singleton is a seller, at the right price. Nine’s CEO Hugh Marks is keen to move quickly, not just taking full control of MRN, but also divesting assets that do not focus on digital subscriptions, mass audiences andnational advertisers. It’s now a question of how much Nine is willing to pay, and the added benefits therein to Nine from a privatisation compared to its current majority and consolidating stake.

While Inc and Healthcare are not cross-linked by any shareholding, Healthcare is ostensibly Celltrion’s internal sales arm. Their fundamentals and prices should be (& are) highly correlated.

Sanghyun initiated a pair trade (short Celltrion / long Healthcare) on Oct 22. The ongoing FSS investigation is hammering both, Healthcare more so as it is more directly exposed. But given what happened to Samsung Biologics Co., (207940 KS), it is very unlikely that this will be a serious risk.

Sigma Healthcare had seen its share price fall 70% in 18 months after its relationship with MyChemist/Chemist Warehouse went sour in 2017, then their existing contract was not renewed for post-June 2019. This appears to be because Sigma did not want to continue trading under overly-generous (to MC/CW) terms and capital usage.

In September, API started buying shares in Sigma Healthcare on the market when they were down by half from the July 2017 news, buying just under 5% before approaching Sigma with an Indicative Proposal to Merge in a Scheme. Sigma responded saying it was willing to engage with API, but API did not respond in the subsequent months it appears. Thursday API bought half of Allan Gray’s stake to lift its own stake to 13.95%, then it publicly announced the same Indicative Proposal.

So now we wait. There is a business review in progress. Full year results for Sigma are due in March. ACCC clearance may take until mid-year.

The deal is at a nice premium – 46.8% to the one-month average, and 69% to the day before. It was about 10% better than where API started buying.

But it may not be good enough. The deal offers some cash, but also offers expensive scrip. API appears to need this deal as much as some would say Sigma does.

Sigma is in the process of doing a zero-based full business review with Accenture and indications are that everyone thinks the company is worth a lot more than where it was trading last week.

This deal looks like it has a big premium but it may not be enough.

Huatai Securities Co Ltd (A) (601688 CH)(and Huatai H) announced that the CSRC had given the company approval to list up to (but not more than) 82,515,000 GDRs. The English language LSE announcement of the “Intention to Float” can be found here and here. Each GDR represents 10 A shares, that is up to RMB13.7bn at the (then) last traded price of the A shares prior to the announcement. If all the shares were issued that would be about 10% of the share capital of Huatai (pre-issuance). This GDR launches the London side of the London-Shanghai Connect. A prospectus is expected in the new year.

Assuming the GDRs trade similarly to the Hs, or even 1% of their maximum issuance quantity, and assuming they have a similar discount to the As as do the Hs, the GDRs will not likely trade more volume than the H Shares.

It is not clear WHY the GDRs would, over time, maintain a tighter discount to the A Shares than the H Shares would …. Except for the fungibility. Which may be the only reason to hold the GDRs at a 20% discount when you can get the H-shares at a 30+% discount. But the system may not be ready to handle GDR creation by mainland domestic investors trying to export capital, even at a discount.

The whole deal comes across as somewhat iffy. It is not clear why the deal needs to be done other than to fill a political need to get the ball rolling. But one wonders why the London-Shanghai Connect ball actually needs to be rolled.

Naspers’ recent underperformance against Tencent has resulted in the discount to NAV widening to near-on 12 months lows. While Naspers remains a function of what happens to Tencent, it offers potentially interesting long-term prospects.

This pseudo-venture capital company is taking steps to narrow the valuation gap via the reduction in its Tencent stake, the sale of successful investments (Flipkart and tbogroup), the listing of profitable entities (Multichoice), the investment in specific areas (classifieds, online retail, payments businesses and food delivery), working to reduce its exposure to the Johannesburg Stock Exchange, and perhaps pursue a dual listing outside of SA, such as Hong Kong. To me, Naspers’ risk profile appears attractive here.

New Street Research‘s Alastair Jones views the most recent Naspers results as broadly positive with continued progress in profitability from its e-commerce assets. He also believes that, given moves to unbundle the pay-TV assets in 2019, there is scope for the NAV discount to narrow. The current low/negative valuation for the unlisted assets ignores their significant value.

Curtis Lehnert recommends a Toyota Industries’ set-up at current levels which are in excess of -2 Standard Deviations below the long-term average, while Toyota Industries is trading at a 35% discount to his NAV – Toyota Industries’ stake in Toyota Motor accounts for 60%).

The group boasts the #1 global market share in forklifts with an estimated 20% market share. Toyota Industries’ closest competitor in the materials handling business is KION Group AG (KGX GR); however, Curtis estimates the market is implying 0.83x for these ops, 28% lower than Kion’s 1.15x.

Newton’s Three Laws of Motion And How They Pertain to Index Inclusions

Travis Lundy noted that Newton’s Third Law, commonly understood that for every action there is always an equal and opposed reaction, applies in some measure to index inclusions.

For every index upweight, there is an equal and opposite downweight.

Travis published his H/A Spread Monitor Project offering a brief look at recent changes in H-Share and A-Share spreads, Southbound flow and impact, and where the spreads are trading within their own historical ranges. My share class monitor provides a snapshot of the premium/discounts for 215 share classifications around the region. Ke Yan, CFA, FRM issued his Discover HK Connect series, to help understand the flow of southbound trades via the Hong Kong Connect.

The 1P (005385 KS)/ 2P (005387 KS) dividend yield difference of 0.53% is close to a year high. Of interest is the recently announced hydrogen cell investment, which may be considered a signal that the HMG-government relation has vastly improved. This potentially suggests that any HMG restructuring may get accelerated, which would be positive for 1P. (link to Sanghyun’s insight: Hyundai Motor Share Class: Time for 1P to Catch Up)

OTHER M&A UPDATES

Trade Me (TME NZ)and Apax Partners have entered into a scheme implementation agreement. Apax Funds have increased their offer price to $6.45/share (from $6.40) since the indicative proposal, following the completion of their due diligence. The Board has unanimously backed the offer. A booklet containing information relating to the scheme is expected to be mailed to Trade Me shareholders in March 2019. The Board expects that Trade Me shareholders will have the opportunity to vote on the scheme at a meeting in April 2019. If all the conditions are satisfied, the scheme is expected to be implemented in the second quarter of 2019. Hellman & Friedman was not expected to materially counter and promptly pulled out of the race.

Cityneon Holdings (CITN SP). West Knighton now has 98.6% of shares out and will move to compulsory acquire shares it does not own. The closing date has been extended until the 26 December.

Sinotrans Shipping (368 HK). As expected from the onset, shareholders approved the privatisation. Turnout was low – around 47.6% of shareholders entitled to vote, did so. Friday was the last day of trading. Cheques are expected to be dispatched on or before the 22 Jan 2019.

Stanmore Coal (SMR AU)‘s has released the Target Statement. The board continues to recommend shareholders reject the $0.95/share unsolicited Golden Investments. The IFA has a fair value range of $1.48-$1.90/share. Shares closed at A$1.04 on Friday.

CCASS

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

IPO listings this week have mostly been within our expectation. Mobvista (1860 HK), Natural Food International H (1837 HK), and Fosun Tourism (1992 HK) have all struggled to hold on to their IPO price on the first day of trading. Unfortunately, WuXi AppTec Co (2359 HK) has also struggled on this first day despite our expectation that the company should be trading at a relatively smaller 19% A-H premium which would imply about 11% upside based on Ke Yan, CFA, FRM‘s sensitivity analysis and Wuxi Apptec’s A share Friday close price.

In the US, Tencent Music Entertainment (TME US) performed well within our expectation. The company’s share price opened about 9% above IPO price. As Sumeet Singh has mentioned in his insight, Tencent Music IPO – Firework – Trading Strategies, this is unlikely going to be a bumper IPO and short-term investors could take profit at high single-digit to low double-digit returns on debut. Indeed, after a decent debut, TME has collapsed below its IPO price, probably due to investors taking profit as the broad market traded poorly on Friday.

Next week, all eyes will be on Softbank Corp (9434 JP)‘s debut and Mio Kato, CFA summarised in his note some of the reasons why Softbank Corp could perform poorly in the near term. Bookbuild results have been mixed. Bloomberg report suggested that Softbank’s international bookbuild was 2-3x oversubscribed while retail offering was at almost 2x. However, Nikkei Asian Review’s article reported that it has been a struggle to sell the IPO shares to retail investors. In any case, we will put out a note next week on our thoughts on bookbuild, updated valuation of peers, and how we think the IPO will likely trade after the recent series of events.

Our overall accuracy rate is 72% for IPOs and 64% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings this week

Shanghai Henlius Biotech (Hong Kong, ~US$500m)

Ingrid Millet (Hong Kong, re-filed)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

AsiaInfo Tech priced its IPO at HKD 10.50/share and will start trading today. Prior to the trading debut, in this short note, we summarize the latest information with updates on our valuation.

Bloomberg reported Softbank Corp (9434 JP)‘s international bookbuild was 2 – 3x covered while retail offering was at almost 2x. There were other reports of bookrunners struggling to sell shares to retail investors.

In this insight, we will look at how peers and market have performed since bookbuild and provide a sensitivity table with implied valuations for different price points and thoughts on the price range for near-term trading.

We have already covered most aspects of Softbank Corp (9434 JP) ‘s IPO in our previous insights:

Over the weekend I published Softbank Corp, Takeda, and Newton’s Three Laws of Motion. Newton’s Three Laws helpfully guide one to understanding the nature of interaction of forces and bodies and the motion which results. Later, Euler’s laws of motion applied a framework for rigid and continuum bodies, and since then “action at a distance” has been replaced be Einstein’s Theory of General Relativity.

After I wrote the bit about one part of the index impact, FTSE unhelpfully changed their mind on timing based on an unhelpful change by the LSE. On Monday, the TSE exercised its discretion – clearly stated in the TOPIX Index Guidebook on p4 (2nd sentence of the opening paragraph) as something it may do – to go its own course in how it will adapt index changes to the first couple of increases in share count due to mergers with foreign corporations.

If an event not specified in this document occurs, or if TSE determines that it is difficult to use the methods described in this document, TSE may use an alternative method of index calculation as it deems appropriate.

So with the changes at FTSE and now TOPIX and JPX Nikkei 400, we no longer have quite the same clarity of forces on the bodies, and therefore less clarity on the resulting motion. The LSE’s announced market change appears to have led the MSCI to change its deletion date for Shire as well, now also (along with FTSE) deleting Shire at the close of the 21st (announcement early this AM Asia time).

Investors have prepared based on the idea that there was a reasonably tight relationship – helped because it was a lot of force applied in a short period (selling and buying all done in a short period in January) between the particles. Now that relationship is being stretched. A lot.

The problem resembles that which Einstein famously pooh-poohed as “Spooky Action At a Distance”. Schrödinger called this entanglement – and it turns out to be one of the weirder branches of quantum mechanics – a field broken wide open by Bell’s Theorem a decade after Einstein shuffled off this mortal coil* – and about which John Wheeler famously said, “If you are not completely confused by quantum mechanics, you do not understand it.”

I cheerfully say quantum mechanics completely baffles me.

I less cheerfully say this whole episode with Takeda and index providers has baffled me too.

But it is important to note that the timing and implications are vastly different than expected just two trading days ago. And the difference is worth thinking about. When the FTSE/MSCI net sell of risk was just 3 days apart, there was a clear connection across that three day distance. Now, the 6-10 week spread of time between the FTSE/MSCI events, the weird two weeks of SETSqx illiquid purgatory just as everyone is full up of risk, then the walk through the Valley of the Shadow of Flowback before we get the first really good net index inclusion to cover the Shire risk people have been dumping for months means that the certainty of understanding the movement of the particle on the other side is substantially lower.

If it all works out well, it might just be Spooky Action At a Distance.

*And there, of course, you have the third Hamlet reference this month… I haz all your Shakespeares!

Hitachi Ltd (6501 JP) announced the acquisition of an 80.1% stake in ABB Ltd (ABBN VX)’s power grids business for $6.4 billion. ABB will retain the remaining stake in the divested unit, which is valued at an EV of $11 billion. ABB’s power grids is a global #1 player and makes transformers, long distance electricity-transmission systems and energy storage units.

Setting aside the huge cultural and integration challenges, we believe that Hitachi’s acquisition of ABB’s power grids is a bold but a risky move.

Satellite companies attempting to convince the Federal Communications Commission to allow them to sell C-band spectrum they license from the U.S. have begun talks to secure customers, sources told CTFN.