I initiated SamE short Common/long 1P trade on Nov 29. This trade delivered the highest yield on Dec 13 at 4.55% with Nov 29 as the reference date. We are now slightly below +1 σ.

Common/1P relative price gap should get narrower. Price wise, 1P discount started at 19.81% on Nov 29 and reached the lowest at 16.38% on Dec 13. It reverted back to 18.69%, down 1.12%p. Market cap wise, Common/1P ratio is still higher than Nov 29. This suggests 1P’s catching up job isn’t over yet.

Div yield difference is still at a record high for 1P. CJ Corp (001040 KS)‘s recent class B pref issuance should be another plus. It will play in favor of those ownership transfer related prefs. I’d continue to hold onto this position until we move into March OGM cycle.

INVESTMENT VIEW: The same macro factors which knocked more than a third off Apple Inc (AAPL US)‘s share price have lifted Gold (GOLD COMDTY) prices by nearly 10% since Sept-18. However, we believe the market narrative could swiftly reverse if the US and China reach a trade agreement in the coming weeks. We would look to press our short on Gold…and even go long Apple.

ROUND TRIP – Temporary staffing company Pasona (2168 JP)‘s shares have completed a year-long ’round trip’ after reaching Overbought territory one year ago following the launch of an ‘engagement campaign’ by the activist investor, Oasis. In May 2018, the company took advantage of its elevated share price to sell 2.3m shares (of which 2m were Treasury Shares), prompting a sharp correction in the share price. In recent months, the shares have languished as the company’s business performance has begun to deteriorate, reaching an 18-month low of 1,008 on 25th December, before rebounding 12% to close the year at ¥1,126.

HOLDCO DISCOUNT – According to the Smartkarma HoldCo Monitor, Pasona has the largest ‘ListCo as a % of Market Cap’ percentage at 365%, and the second-largest ‘Discount to Net Asset Value’ (78%) of the 77 companies that are tracked. With Pasona’s interim results due to be released on Friday 11th, January, the Insight will look at the company’s recent business performance, offer some guidelines for valuing the company and make two stock-specific recommendations. The format follows that of our recent Insight on GMO Internet.

Weimob.com (1260480D CH) is a combination of a SaaS software and an adtech (targeted marketing) business which has started book building to raise gross proceeds of $108-135 million. According to press reports, Weimob is being viewed favourably by investors as it is being offered at a “cheap” valuation of 18-23x 2019 P/E.

However, the valuation of 18-23x 2019 P/E is optically cheap. Our analysis suggests that including capitalised R&D, Weimob is being offered at a material premium to a peer group of major Chinese internet companies. Notably, our forecasts do not adjust for the capitalised contract acquisition costs which would further increase Weimob’s P/E multiple. Consequently, we believe that the proposed IPO price range is unattractive and would sit out this IPO.

Paused for eight months, China’s authority resumed the domestic game approval in December. The first batch of 80 games was approved recently.

Since the last round of game application approval, the stock price of Tencent Holdings (700 HK) has fallen by 26%. Stock price reacted positively to the recent progress of game approval.

In this insight, we try to assess the significance of recent progress with a statistical approach.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

I’ve covered most aspects of the deal in my earlier insight, Weimob Pre-IPO – Can Be Steamrolled by Tencent, Anytime, where I spoke about the over-reliance on Tencent, high attrition rates and acquisition costs for SMBs, and the increasing contribution of its ads business.

In this insight, I’ll provide an update from the latest filings, comment on valuations and run the deal through our IPO framework.

During an invitation-only Architecture Day held on December 11’th 2018, Intel revealed three key strategies aimed at extending Moore’s Law. The first, 3D Logic packaging, aims to increase effective transistor density by scaling up rather than down, similar to the CoWoS technology introduced by Taiwan Semiconductor in 2012. The second, switching to multiple, smaller “chiplet” processor cores, is required to address the thermal and yield challenges precipitated by the progression of ever larger multi-core monolithic processor die and is the key foundation underpinning Advanced Micro Devices‘s Zen-based architecture. The third is a hybrid architecture aimed at reducing power consumption and clearly reminiscent of ARM’s big.LITTLE approach which was first introduced some six years ago and now widely used today in smartphone and tablet SOCs.

At the event, Intel showcased their first product based on these three key concepts and it features a large Core processor combined with four smaller Atom processors, all manufactured on the same piece of silicon, an approach the company refers to as Hybrid x86. Intel confirmed that it will be the basis for a new line of products set to launch in the second half of 2019.

They say that imitation is the sincerest form of flattery and, based on what Intel had to say at its Architecture Day, TSMC, AMD and ARM will likely be flattered in equal measure.

One of the reasons why the Nexon’s founder Kim Jung-Joo, who is only 50 years old, is trying to sell his entire stake in Nexon may have been due to the recent allegations about him giving about $380,000 worth of Nexon stock (prior to its listing) to his old high school classmate (who is now a senior public prosecutor) for free. Kim Jung-Joo has repeatedly faced allegations and attended numerous court hearings on this matter in the past two years. He may have gotten a bit tired from all these allegations.

Given the enormous size of this acquisition, the two leading Korean game companies including NCsoft Corp (036570 KS) and Netmarble Games (251270 KS) are not likely to purchase Nexon. Rather, the leading contender to buy Nexon right now is likely to be Tencent Holdings (700 HK). The sheer huge size of this deal will represent one of the largest M&A deals in Asia in 2019.

A big takeaway from our conversations with Indo e-commerce industry sources is that they vouch for Shopee’s (Sea Ltd’s (SE US) e-commerce arm) MS gains story in the country.

Indo e-commerce market has been enjoying super growth period (94% CAGR in 2015-18E) despite three major challenges (logistics, payment and highly subsidized market).

With SE’s fund raising a matter of when, not if (2H20 as most likely timetable), Shopee’s tremendous progress in key metrics (MS, take rate) provides comfort.

Assuming fair valuation of US$3 bn (vs. US$1.4 bn implied in SE’s ADR price) for Shopee, 12-mo PT for SE works out to be US$15.73/ADR, representing 43% upside potential.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The average NAV discount of a basket of 40 Holdcos steadily, and not altogether unsurprisingly, widened throughout the year.

Passive, tech-related and illiquid Holdcos widened most; while cross-border and property Holdcos were the best of the worst.

Illiquid, property, and passive Holdcos’ underperformance (or widening) was more pronounced in the first half. Tech Holdcos primarily widened in the second half.

Below the various NAV discount chart summaries of various baskets are my weekly setup/unwind tables.

This, and other relationships discussed below, trade with: 1) a minimum liquidity threshold of US$1mn on a 90-day moving average; and 2) a minimum 20% ‘market capitalisation’ threshold, whereby the value of the holding/Opco held must be at least 20% of the parent’s market cap.

Maoyan Entertainment, formerly Entertainment Plus (EPLUS HK), is the largest online movie ticketing service provider in China. According to press reports, Maoyan has started pre-marketing to raise $0.3 billion (down from earlier indication of $0.5-1.0 billion) through a Hong Kong IPO. Maoyan is backed by Beijing Enlight Media (300251 CH) (20.0% shareholder), Tencent Holdings (700 HK) (16.3% shareholder) and Meituan Dianping (3690 HK) (8.6% shareholder).

Maoyan is yet another proxy in the battle between Tencent and Alibaba Group Holding (BABA US). However, we believe that challenges abound for Maoyan and would be cautious about participating in the IPO.

LG Uplus Corp (032640 KS) was a clear market winner in 2018 as the stock was up 26% last year versus KOSPI which was down 17%. We think that LG Uplus is likely to continue to outperform the market over the next 12 months. There are many catalysts with this stock but the two most important catalysts on this stock over the next 12 months include the 5G roll-out and the potential acquisition of Cj Hellovision (037560 KS).

LG Uplus experienced a breakout year in 2013 with a steep increase in its share price. LG Uplus’ wireless ARPU increased 13.6% YoY in 2013, driven by higher ARPU 4G/LTE subscribers, which jumped from 4.4 million at end of 2012 to 7.1 million at end of 2013. Similar to the positive impact that the roll-out of 4G services had on LG Uplus’ wireless service ARPU and its share price, we believe that the roll-out of 5G services will have a positive impact on the company’s ARPU and its share price in 2019 and 2020.

At current price of 9,060 won for CJ Hellovision (market cap of 702 billion won), the EV is 1.3 trillion won, which would suggest an EV/EBITDA of 3.9x, using an estimated EBITDA of 272 billion won. If we double the value, the EV/EBITDA multiple would spike to 7.4x. LG Uplus is currently trading at 4.0x EV/EBITDA using 2018 consensus EBITDA estimates. Although it is a normal practice to pay a significant premium in Korea for an acquisition of a large controlling stake in a company, LG Uplus is probably analyzing on every angle to see if it is worth it paying a hefty 7.4x EV/EBITDA multiple for CJ Hellovision.

Minnesotan Authorities declined to charge the founder of JD.

JD’s stock price has already plunged 52% in 2018. We believe JD is a defensive equity for portfolios, as the NASDAQ Composite just plunged 50% at most in the financial crisis of 2008.

Compared to 2014, today’s JD has a higher market share in the larger e-commerce market. However, JD’s stock price is at the same level as the first trading day in 2014.

JD continued to generate operating cash inflows in 2018 as previous years despite of its zero net margins.

We are not concerned about the programmer layoff in December, as we believe JD overly invested in “hi-tech” that will not bring revenues in the near future.

Based on historical Price / GMV, we believe there is an upside of 270% for JD’s stock price.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

ROUND TRIP – Temporary staffing company Pasona (2168 JP)‘s shares have completed a year-long ’round trip’ after reaching Overbought territory one year ago following the launch of an ‘engagement campaign’ by the activist investor, Oasis. In May 2018, the company took advantage of its elevated share price to sell 2.3m shares (of which 2m were Treasury Shares), prompting a sharp correction in the share price. In recent months, the shares have languished as the company’s business performance has begun to deteriorate, reaching an 18-month low of 1,008 on 25th December, before rebounding 12% to close the year at ¥1,126.

HOLDCO DISCOUNT – According to the Smartkarma HoldCo Monitor, Pasona has the largest ‘ListCo as a % of Market Cap’ percentage at 365%, and the second-largest ‘Discount to Net Asset Value’ (78%) of the 77 companies that are tracked. With Pasona’s interim results due to be released on Friday 11th, January, the Insight will look at the company’s recent business performance, offer some guidelines for valuing the company and make two stock-specific recommendations. The format follows that of our recent Insight on GMO Internet.

Weimob.com (1260480D CH) is a combination of a SaaS software and an adtech (targeted marketing) business which has started book building to raise gross proceeds of $108-135 million. According to press reports, Weimob is being viewed favourably by investors as it is being offered at a “cheap” valuation of 18-23x 2019 P/E.

However, the valuation of 18-23x 2019 P/E is optically cheap. Our analysis suggests that including capitalised R&D, Weimob is being offered at a material premium to a peer group of major Chinese internet companies. Notably, our forecasts do not adjust for the capitalised contract acquisition costs which would further increase Weimob’s P/E multiple. Consequently, we believe that the proposed IPO price range is unattractive and would sit out this IPO.

Paused for eight months, China’s authority resumed the domestic game approval in December. The first batch of 80 games was approved recently.

Since the last round of game application approval, the stock price of Tencent Holdings (700 HK) has fallen by 26%. Stock price reacted positively to the recent progress of game approval.

In this insight, we try to assess the significance of recent progress with a statistical approach.

I’ve covered most aspects of the deal in my earlier insight, Weimob Pre-IPO – Can Be Steamrolled by Tencent, Anytime, where I spoke about the over-reliance on Tencent, high attrition rates and acquisition costs for SMBs, and the increasing contribution of its ads business.

In this insight, I’ll provide an update from the latest filings, comment on valuations and run the deal through our IPO framework.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

During an invitation-only Architecture Day held on December 11’th 2018, Intel revealed three key strategies aimed at extending Moore’s Law. The first, 3D Logic packaging, aims to increase effective transistor density by scaling up rather than down, similar to the CoWoS technology introduced by Taiwan Semiconductor in 2012. The second, switching to multiple, smaller “chiplet” processor cores, is required to address the thermal and yield challenges precipitated by the progression of ever larger multi-core monolithic processor die and is the key foundation underpinning Advanced Micro Devices‘s Zen-based architecture. The third is a hybrid architecture aimed at reducing power consumption and clearly reminiscent of ARM’s big.LITTLE approach which was first introduced some six years ago and now widely used today in smartphone and tablet SOCs.

At the event, Intel showcased their first product based on these three key concepts and it features a large Core processor combined with four smaller Atom processors, all manufactured on the same piece of silicon, an approach the company refers to as Hybrid x86. Intel confirmed that it will be the basis for a new line of products set to launch in the second half of 2019.

They say that imitation is the sincerest form of flattery and, based on what Intel had to say at its Architecture Day, TSMC, AMD and ARM will likely be flattered in equal measure.

One of the reasons why the Nexon’s founder Kim Jung-Joo, who is only 50 years old, is trying to sell his entire stake in Nexon may have been due to the recent allegations about him giving about $380,000 worth of Nexon stock (prior to its listing) to his old high school classmate (who is now a senior public prosecutor) for free. Kim Jung-Joo has repeatedly faced allegations and attended numerous court hearings on this matter in the past two years. He may have gotten a bit tired from all these allegations.

Given the enormous size of this acquisition, the two leading Korean game companies including NCsoft Corp (036570 KS) and Netmarble Games (251270 KS) are not likely to purchase Nexon. Rather, the leading contender to buy Nexon right now is likely to be Tencent Holdings (700 HK). The sheer huge size of this deal will represent one of the largest M&A deals in Asia in 2019.

A big takeaway from our conversations with Indo e-commerce industry sources is that they vouch for Shopee’s (Sea Ltd’s (SE US) e-commerce arm) MS gains story in the country.

Indo e-commerce market has been enjoying super growth period (94% CAGR in 2015-18E) despite three major challenges (logistics, payment and highly subsidized market).

With SE’s fund raising a matter of when, not if (2H20 as most likely timetable), Shopee’s tremendous progress in key metrics (MS, take rate) provides comfort.

Assuming fair valuation of US$3 bn (vs. US$1.4 bn implied in SE’s ADR price) for Shopee, 12-mo PT for SE works out to be US$15.73/ADR, representing 43% upside potential.

The average NAV discount of a basket of 40 Holdcos steadily, and not altogether unsurprisingly, widened throughout the year.

Passive, tech-related and illiquid Holdcos widened most; while cross-border and property Holdcos were the best of the worst.

Illiquid, property, and passive Holdcos’ underperformance (or widening) was more pronounced in the first half. Tech Holdcos primarily widened in the second half.

Below the various NAV discount chart summaries of various baskets are my weekly setup/unwind tables.

This, and other relationships discussed below, trade with: 1) a minimum liquidity threshold of US$1mn on a 90-day moving average; and 2) a minimum 20% ‘market capitalisation’ threshold, whereby the value of the holding/Opco held must be at least 20% of the parent’s market cap.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Maoyan Entertainment, formerly Entertainment Plus (EPLUS HK), is the largest online movie ticketing service provider in China. According to press reports, Maoyan has started pre-marketing to raise $0.3 billion (down from earlier indication of $0.5-1.0 billion) through a Hong Kong IPO. Maoyan is backed by Beijing Enlight Media (300251 CH) (20.0% shareholder), Tencent Holdings (700 HK) (16.3% shareholder) and Meituan Dianping (3690 HK) (8.6% shareholder).

Maoyan is yet another proxy in the battle between Tencent and Alibaba Group Holding (BABA US). However, we believe that challenges abound for Maoyan and would be cautious about participating in the IPO.

LG Uplus Corp (032640 KS) was a clear market winner in 2018 as the stock was up 26% last year versus KOSPI which was down 17%. We think that LG Uplus is likely to continue to outperform the market over the next 12 months. There are many catalysts with this stock but the two most important catalysts on this stock over the next 12 months include the 5G roll-out and the potential acquisition of Cj Hellovision (037560 KS).

LG Uplus experienced a breakout year in 2013 with a steep increase in its share price. LG Uplus’ wireless ARPU increased 13.6% YoY in 2013, driven by higher ARPU 4G/LTE subscribers, which jumped from 4.4 million at end of 2012 to 7.1 million at end of 2013. Similar to the positive impact that the roll-out of 4G services had on LG Uplus’ wireless service ARPU and its share price, we believe that the roll-out of 5G services will have a positive impact on the company’s ARPU and its share price in 2019 and 2020.

At current price of 9,060 won for CJ Hellovision (market cap of 702 billion won), the EV is 1.3 trillion won, which would suggest an EV/EBITDA of 3.9x, using an estimated EBITDA of 272 billion won. If we double the value, the EV/EBITDA multiple would spike to 7.4x. LG Uplus is currently trading at 4.0x EV/EBITDA using 2018 consensus EBITDA estimates. Although it is a normal practice to pay a significant premium in Korea for an acquisition of a large controlling stake in a company, LG Uplus is probably analyzing on every angle to see if it is worth it paying a hefty 7.4x EV/EBITDA multiple for CJ Hellovision.

Minnesotan Authorities declined to charge the founder of JD.

JD’s stock price has already plunged 52% in 2018. We believe JD is a defensive equity for portfolios, as the NASDAQ Composite just plunged 50% at most in the financial crisis of 2008.

Compared to 2014, today’s JD has a higher market share in the larger e-commerce market. However, JD’s stock price is at the same level as the first trading day in 2014.

JD continued to generate operating cash inflows in 2018 as previous years despite of its zero net margins.

We are not concerned about the programmer layoff in December, as we believe JD overly invested in “hi-tech” that will not bring revenues in the near future.

Based on historical Price / GMV, we believe there is an upside of 270% for JD’s stock price.

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of fully-diluted shares (current shares out + 26.826mm Options + ~2.1mm Award shares).

The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The other terms and conditions of this deal will be set out in the offer document which is expected to be despatched in mid-January 2019 (14-21 days from 28 December).

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.10 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

Weimob.com (1260480D CH) is a combination of a SaaS software and an adtech (targeted marketing) business. It is backed by Tencent Holdings (700 HK), which is 3% shareholder and its largest customer. Weimob has started book building to raise gross proceeds of $108-135 million. Cornerstone investors which include a close associate of Tencent and Huifu Payment Limited (1806 HK) have agreed to purchase $42 million worth of shares in the offering.

The prospectus provides 1H18 results and selective disclosure on the first nine months of 2018. Overall, we believe that Weimob’s fundamentals are mixed and any prospective IPO multiple needs to be adjusted for the material capitalisation of expenses.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

This Insight builds on our previous Insight, India Generic Drugs: US Antitrust Inquiry Widens by discussing estimated potential liabilities and details contained in court filings. Public comments by one of the plaintiffs (47 states) suggest the defendants’ aggregate liability could exceed US$6 billion, the largest previous settlement on record. There is not enough information to apportion potential liability by company, but some companies are better-positioned to bear the cost of a settlement than others. The process could drag on for an undetermined period of time (which helps the defendants). At the same time, the overhang will keep a lid on generic drug prices in the US market.

Duzonbizon (012510 KS) (also spelled “Douzonbizon”), is a leading beneficiary of the expanding cloud based CRM software market in Korea. The Korean public cloud market is expected to grow from 2.0 trillion won in 2018 to 2.4 trillion won in 2019. In the case of the domestic public cloud market, SaaS will continue to be strong. One of the catalysts that could positively impact the cloud industry in Korea is that there could be a change in the regulations which may allow many of the government related offices to start using private cloud services starting in 2019.

The company has very little competition in the Lite ERP segment, where it has a near monopoly position. The customers that use this product are typically small companies with annual sales of less than 10 billion won to 20 billion won. Other major competitors have not chosen to aggressively fight against Duzonbizon in this segment. The company’s cloud business is based on providing cloud-based ERP products. The company has been able to significantly increase its total sales by providing the ERP products as a cloud based service. The customers can reduce costs on servers and personnel by relying on the company’s cloud based ERP software and services.

Duzonbizon is currently trading at 29x P/E (2019E) and 24x P/E (2020E), using consensus earnings estimates. The company’s P/E valuation multiples have been rising in the past several years and the valuation multiples have ranged in the 20-40x. While the company’s valuation multiples are relatively higher than the KOSPI market average, they are lower than the global CRM software leaders such as Salesforce.Com Inc (CRM US), which is currently trading at 49x P/E. Despite the recent volatility in Duzonbizon’s share price in the past few months, we are positive on the stock over the next one year and we think the stock could climb by an additional 20-30% over the next year. We believe that the company has a very strong business moat with a very loyal customer base. We want to start 2019 recommending a solid, emerging growth company in the Korean tech space and so we believe that Duzonbizon is a good company to start off with.

It is our view, that come hell or high-water, in 2019, Tesla Motors (TSLA US) will establish itself as the pre-eminent large-cap growth stock. Those that are short would cover the position at a loss and those that are long are looking at another Apple Inc (AAPL US) or Amazon.com Inc (AMZN US) in the making. The ride may be volatile, but will be worth it.

Nintendo reported their 2QFY03/19 in October with results showing growth at both the top line and bottom line albeit not living up to consensus expectations. Top line grew by 4.0% YoY to JPY388.9bn in 1H03/19 while OP grew by 53.9% YoY to JPY61.4bn. OP in the last quarter (2QFY03/19) was the second highest the company has experienced over the last five years. This growth has been mainly driven by the sales of Nintendo Switch hardware which sold just over 5m units in 1HFY03/19. However, YoY growth remained at 3.4% compared to 4.9m units sold in 1HFY03/18. This has left investors worried about Nintendo’s aggressive target of selling 20m units of the Switch for FY03/19. Of this target, the company has managed to achieve only around 25.0% in 1H. Nintendo’s financial performance follows a seasonal trend with the December quarter showing stronger performance due to increased sales during Christmas. While the company’s current quarter is likely to show strong results, we remain skeptical about the company reaching the aforementioned target for FY03/19.

Switch Sales Have Caused an Improvement in Nintendo’s OP….

Source: Capital IQ

….Despite a Slowdown in the Growth of Units Sales

Source: Nintendo website

Nintendo’s Last Quarter Has Also Failed to Live Up To Consensus Expectations

Hyosung Corporation (004800 KS) had fallen 16% just in two days. Holdco is now at a 50% discount to NAV. This is a 10%p drop from 10 days ago (Dec 19). Holdco price must have been overly corrected. The ongoing police investigation on Cho Hyun-joon’s alleged crime won’t lead to a delisting. 10%p drop in discount to NAV must be a price divergence, not a sensible price correction.

Trade volume remained steady. Local hedge funds led the selling on Dec 27. Even they changed their position the following day. No short selling spike has been seen either. Hyosung is one of the highest yielding div holdco stocks. Hyosung Capital liquidation and Anyang Plant revaluation would be another short-term plus.

I’d exploit this price divergence. It would soon revert to the Dec 19 discount level. It should at least stay at the peer average.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The share price of Recruit Holdings (6098 JP) has fallen by around 30% over the past three months from an all-time high of JPY3,826 (on 1st October 2018) to JPY2,705 on 24th December 2018. Prior to this, Recruit’s share price saw a strong upward rally during May-September following the company’s announcement that it would acquire Glassdoor Inc. (the company which operates the employment information website glassdoor.com).

We expect Recruit’s consolidated revenue to grow 7.7% and 6.5% YoY in FY03/19E and FY03/20E respectively, driven by the acquisition of Glassdoor and steady growth in Japanese staffing operations, partially offset by a likely slowdown in global labour market activity. We also expect Recruit’s consolidated EBITDA margin to improve by around 50bps due to higher margin from Glassdoor.

Despite the recent dip in share price and steady topline and bottom line growth over the forecast period, at a FY2 EV/EBITDA multiple of 14.0x, Recruit doesn’t look particularly attractive to us. Recruit’s internet advertising business and employment business peers, Yahoo Japan (4689 JP) and Persol Holdings (2181 JP) are trading at FY2 EV/EBITDAs of 7.7x and 9.6x respectively.

Although Uber aims to be an Amazon for transport, we will focus on the ride-hailing market in part 3 of this series. Here, we try to answer the following questions:

What are the indicative ride-hailing market shares of Uber vs Lyft in North America?

What is Uber’s share in other key countries?

What are the lawsuits investors should watch out for?

How do Uber’s revenue drivers compare with Lyft’s?

What are the timelines and key figures for both companies’ IPOs?

This is the third note in a series about the expected 2019 IPO of global ride-hailing giant Uber Technologies (0084207D US) and Lyft. Please read the earlier two pieces in the series for better contexts:

As the colder winter weather is felt and the icy blast of industry tariff cuts continues to chill sentiment, we seek some respite (at least mentally) in the warmer climes of Okinawa. Okinawa Cellular is a unique company. It’s a small cap telecom network operator in Japan with a focus on the sub-tropical islands of Okinawa Prefecture. As part of the KDDI group, the company benefits from its parent’s economies of scale, but with its local presence, it also benefits from being the hometown hero.

Because the stock is relatively small, from an investment perspective it runs into liquidity constraints that the other telcos do not have, so it’s a different type of investment but one that we think is worth looking at. Over the past 12 months Okinawa Cellular’s stock has fallen by 12.3%, but over the past year the stock has delivered a return in the middle of its peer group and has outperformed the broad TOPIX by about 5.5%. Like most telcos, Okinawa Cellular is also ramping its dividend payments, and the current yield is about 3.5%.

THE GMO INTERNET (9449 JP) STORY – GMO internet (GMO-i) has attracted much attention in the last eighteen months from an unusual trinity of value, activist and ‘cryptocurrency’ equity investors.

VALUE– Many traditional, but mostly foreign, value investors have seen the persistent negative difference between GMO-i’s market capitalisation and the value of the company’s holdings in its eight listed consolidated subsidiaries as an opportunity to invest in GMO-i with a considerable ‘margin of safety’.

ACTIVIST – Since July 2017, the activist investor, Oasis, has waged a so-far-unsuccessful campaign with the aim of improving GMO’s corporate governance, removing takeover defences, addressing a ‘secularly undervalued stock price we are not able to tolerate’ (sic), and redefining the role and influence of the company’s Chairman, President, Representative Director and largest shareholder, Masatoshi Kumagai.

‘CRYPTO!’ – In December 2017, GMO-i committed to spending more than ¥35b or 10% of non-current assets. The aim was threefold: to set up a bitcoin ‘mining’ headquarters in Switzerland (with the ‘mining’ operations being carried out at an undisclosed location in Scandinavia), to develop proprietary state-of-the-art 7nm-node ‘mining chips’, and, in due course, to sell GMO-branded and developed ‘mining’ machines. The move was hailed in the ‘crypto’ fraternity as GMO-i became the largest non-Chinese and the first well-established Internet conglomerate to make a major investment in ‘cryptocurrency’ infrastructure.

OUTSTANDING – Following the December 2017 announcement, trading volumes spiked into ‘Overtraded’ territory – as measured by our Volume Score. Many investors saw GMO-i shares as a safer way of gaining exposure to ‘cryptocurrencies’, even as the price of bitcoin began to subside. By early June 2018, GMO-i’s shares had reached a closing price of ¥3,020: up 157% from the low of the prior year and outperforming TOPIX by 135%. Whatever the primary driver of this outstanding performance, each of our trio of investor groups no doubt felt vindicated in their approach to the stock.

CRYPTO CLOSURE – On December 25th 2018, GMO-i’s shares reached a new 52-week low of ¥1,325, a decline of 56% from the June high. Year to date, GMO-i shares have now declined by 31%, underperforming TOPIX by nine percentage points. On the same day, GMO-i announced that the company would post an extraordinary ¥35.5b loss for the fourth quarter, incurring an impairment loss of ¥11.5b in relation to the closure of the Swiss ‘mining’ headquarters and a loss of ¥24b to cover the closure of the ‘mining chip’ and ‘mining machine’ development, manufacturing and sales businesses. GMO-i will continue to ‘mine’ bitcoin from its Tokyo headquarters and intends to relocate the ‘mining’ centre from Scandinavia to (sic) ‘a region that will allow us to secure cleaner and less expensive power supply, but we have not yet decided the details’. Unlisted subsidiary GMO Coin’s ‘cryptocurrency’ exchange will also continue to operate, and the previously-announced plans to launch a ¥-based ‘stablecoin’ in 2019 will proceed. In the two trading days following this announcement, the shares have recovered 13% to ¥1,505.

RAIDING THE LISTCO PIGGY BANK – As we shall relate, this is the second time since listing that GMO-i has written off a significant new business venture which the company had commenced only a short time before. In both cases, the company was forced to sell stakes in its listed consolidated subsidiaries to offset the resulting losses. On this occasion, the sale of shares in GMO Financial (7177 JP) (GMO-F) on September 25 2018, and GMO Payment Gateway (3769 JP) (GMO-PG) on December 17 2018, raised a combined ¥55.6b and, after the deduction of the yet-to-be-determined tax on the realised gains, should more than offset the ‘crypto’ losses. According to CFO Yasuda, any surplus from this exercise will be used to pay down debt. Also discussed below and in keeping with this GMO-i ‘MO’, in 2015, the company twice sold shares in its listed subsidiaries to ‘smooth out’ less-than-desirable operating results.

In the DETAIL section below we will cover the following topics:-

I: THE GMO-i TRACK RECORD – TOP-DOWN v. BOTTOM UP

BOTTOM LINE No. 1: NET INCOME

BOTTOM LINE No.2 – COMPREHENSIVE INCOME

II: THE GMO-i BUSINESS MODEL – THROWING JELLY AT THE WALL

III: THE GMO-i BALANCE SHEET – NOT SO HAPPY RETURNS

IV: THE GMO-i CASH FLOW – DEBT-FUNDED CASH PILE

V: THE GMO-i VALUATION – TWO METHODS > SAME RESULT

VALUATION METHOD No.1 – THE ‘LISTCO DISCOUNT’

VALUATION METHOD No.2 – RESIDUAL INCOME

CONCLUSION – For those unable or unwilling to read further, we conclude that GMO-i ‘rump’ is a grossly-overrated business. Despite having started and spun off several valuable GMO Group entities, CEO Kumagai bears responsibility for two decades of serial and very poorly-timed ‘mal-investments’. As a result, the stock market has, except for the ‘cryptocurrency’-induced frenzy of the first six months of 2018, historically not accorded GMO-i any premium for future growth, and has correctly looked beyond the ‘siren song’ of the ‘HoldCo discount’. According to the two valuation methodologies described below, the company is, however, fairly valued at the current share price of ¥1,460. Investors looking for a return to the market-implied 3% perpetual growth rate of mid–2018 are likely to be as disappointed as those wishing for BTC to triple from here.

● We notice that Anjuke’s Oct.-Nov. traffic declined. We attribute this decline to the tightening of registration requirement in various cities, which will reduce the number of housing leads on WUBA platform;

● We, however, believe new home business will deliver strong revenue for WUBA this year, contributing Rmb2bn in revenues by our estimate;

● We rate the stock Buy and cut TP from US$84 to US$79.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

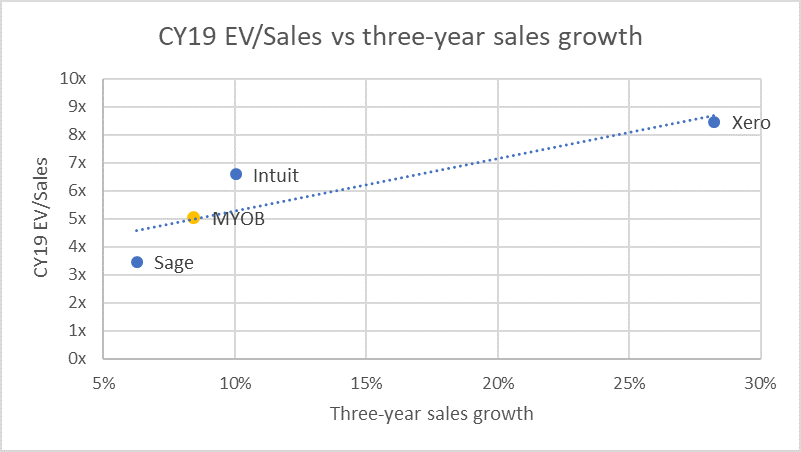

On 24 December, MYOB Group Ltd (MYO AU) announced that it entered into a scheme implementation agreement under which KKR will acquire MYOB at $3.40 per share, which is 10% lower than 2 November offer price of A$3.77. MYOB claims its decision to recommend KKR’s lower offer was based on current market uncertainty, long-term nature of its strategic growth plans and the go-shop provisions of the deal.

We believe that KKR’s revised offer is opportunistic, but MYOB’s shareholders are caught between a rock and a hard place. Shareholders can take a short-term view and grudgingly accept the revised offer. Alternatively, shareholders can take a long-term view by rejecting the offer and hope MYOB’s strategic growth plans and a market recovery can reverse the inevitable share price collapse.

As per reports, Infosys Ltd (INFO IN) may consider a proposal for a share buyback of $1.60 billion very soon. The buyback announcement is likely to be made on January 11 when the company board meets to consider the 3Q FY19 results. Before this, in November 2017, Infosys Ltd (INFO IN) had announced a buyback and spent Rs130 bn to buy a total of 113mn equity shares. This fresh buyback could be an important development and could be an important support for the stock, it is also sensible for other reasons.

There are no major acquisitions in recent times by Infosys Ltd (INFO IN) and if this is likely to be the trend for near future, share buyback is not a bad idea. The company is still struggling with some of the legacy issues and the priority as of now is to streamline the organic growth. We think Infosys Ltd (INFO IN) is also cautious with inorganic growth opportunities as the company had serious issues with acquisitions in the past. What could be another key driver behind this is that in valuation terms, Infosys Ltd (INFO IN) is not very expensive.

During the second half of December 2018, Japan saw two telecom companies list on the Tokyo Stock Exchange: Softbank Corp (9434 JP) and ARTERIA Networks (4423 JP). After years of industry consolidation, which saw several stocks delist, this felt like a Christmas miracle (at least for those watching the sector’s stocks).

It would be hard to find two companies in the same industry that are so different – both in their business models as well as in how their IPOs were positioned to investors. One stock is 100 times larger than the other, but this is not a story of David and Goliath. It is two unique stories in parallel.

While each company took a very different approach to selling its stock, both have suffered from the subsequent broader market weakness, irrespective of company specifics. We can’t say it has been the worst of times, but it certainly has been a tough time with SoftBank Corp down 13% and Arteria down 20% from their IPO prices.

In this Insight we explore how each company approached its IPO and how each has fared since.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

One of the reasons why the Nexon’s founder Kim Jung-Joo, who is only 50 years old, is trying to sell his entire stake in Nexon may have been due to the recent allegations about him giving about $380,000 worth of Nexon stock (prior to its listing) to his old high school classmate (who is now a senior public prosecutor) for free. Kim Jung-Joo has repeatedly faced allegations and attended numerous court hearings on this matter in the past two years. He may have gotten a bit tired from all these allegations.

Given the enormous size of this acquisition, the two leading Korean game companies including NCsoft Corp (036570 KS) and Netmarble Games (251270 KS) are not likely to purchase Nexon. Rather, the leading contender to buy Nexon right now is likely to be Tencent Holdings (700 HK). The sheer huge size of this deal will represent one of the largest M&A deals in Asia in 2019.

A big takeaway from our conversations with Indo e-commerce industry sources is that they vouch for Shopee’s (Sea Ltd’s (SE US) e-commerce arm) MS gains story in the country.

Indo e-commerce market has been enjoying super growth period (94% CAGR in 2015-18E) despite three major challenges (logistics, payment and highly subsidized market).

With SE’s fund raising a matter of when, not if (2H20 as most likely timetable), Shopee’s tremendous progress in key metrics (MS, take rate) provides comfort.

Assuming fair valuation of US$3 bn (vs. US$1.4 bn implied in SE’s ADR price) for Shopee, 12-mo PT for SE works out to be US$15.73/ADR, representing 43% upside potential.

The average NAV discount of a basket of 40 Holdcos steadily, and not altogether unsurprisingly, widened throughout the year.

Passive, tech-related and illiquid Holdcos widened most; while cross-border and property Holdcos were the best of the worst.

Illiquid, property, and passive Holdcos’ underperformance (or widening) was more pronounced in the first half. Tech Holdcos primarily widened in the second half.

Below the various NAV discount chart summaries of various baskets are my weekly setup/unwind tables.

This, and other relationships discussed below, trade with: 1) a minimum liquidity threshold of US$1mn on a 90-day moving average; and 2) a minimum 20% ‘market capitalisation’ threshold, whereby the value of the holding/Opco held must be at least 20% of the parent’s market cap.

Maoyan Entertainment, formerly Entertainment Plus (EPLUS HK), is the largest online movie ticketing service provider in China. According to press reports, Maoyan has started pre-marketing to raise $0.3 billion (down from earlier indication of $0.5-1.0 billion) through a Hong Kong IPO. Maoyan is backed by Beijing Enlight Media (300251 CH) (20.0% shareholder), Tencent Holdings (700 HK) (16.3% shareholder) and Meituan Dianping (3690 HK) (8.6% shareholder).

Maoyan is yet another proxy in the battle between Tencent and Alibaba Group Holding (BABA US). However, we believe that challenges abound for Maoyan and would be cautious about participating in the IPO.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.