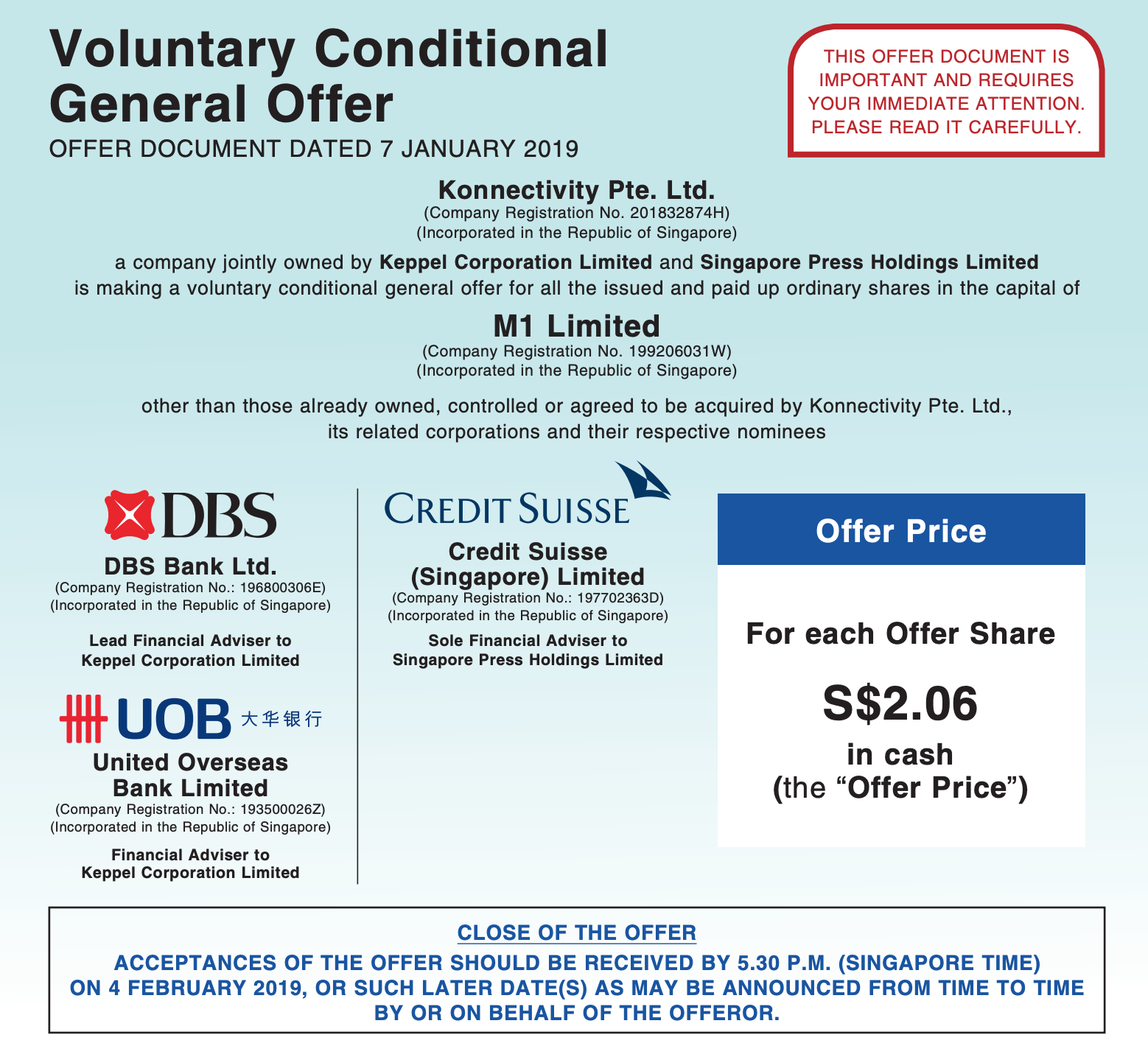

M1 Ltd (M1 SP), the third largest telecom operator in Singapore, is subject to a voluntary conditional offer (VGO) at S$2.06 cash per share from Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP) (KCL-SPH). KCL-SPH said on Tuesday that they wouldn’t increase their S$2.06 offer price “under any circumstances whatsoever.”

KCL-SPH’s stance not to increase their S$2.06 offer price is a clever ploy to the put the ball in Axiata Group (AXIATA MK)’s court. Axiata has three options, in our view. We believe that the probability of a material bid to KCL-SPH’s offer is low with Axiata most likely to retain its stake as a minority shareholder.

Maoyan Entertainment (formerly Entertainment Plus) launched its institutional book building last Friday. We covered the company’s background, industry backdrop, financials, shareholders and the regulatory overhang in our previous two notes.

In this note, we will look at the recent development of the company, based on the data from the prospectus and our channel checks. We will also discuss the valuation of the company.

SamE Common/1P are now below -2σ on a 20D MA. This is almost 120D low. 1P discount to Common is 16.61%. This is the lowest since mid November last year. Div yield difference is also on the decline. It is now 0.7%p on FY19 local street consensus.

It is possible to see short-term price correction on both after the recent mini rally. This’d complicate predictability on price pairing. But we are moving into March OGM cycle. This should put harsher pressure on 1P.

I’d close the previous position. I’d initiate another round of pair trade. This time go long Common and short 1P with a short term horizon.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this week’s HK Connect Discovery, we highlight that Tencent topped the weekly inflow by quantum and its shares held by mainland investors via Stock Connect is at one year low. Stocks exposed to mobile game sector experienced inflow too. In addition, we continue to observe that the mainland investors holding on Yichang HEC continue to rise.

The rest of our event-driven research can be found below.

Best of luck for the new week – Rickin, Venkat and Arun

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

HET has grown its revenue at an impressive 73% CAGR from 2015 to 2017 and has been accompanied by gross margin expansion. The strong growth was supported by improving operating metrics such as an increase in student enrollment and average spending.

However, HET has been making losses and continues to spend more than its net billing. It is unclear whether HET had already achieved break even for its proprietary courses before expanding into its CCtalk platform. But from its high level of expenses, it seems unsustainable for HET to be relying heavily on the sales and marketing spending to get users to purchase online courses.

In this insight, we will look into the company’s financial and operating performance, regulatory risks regarding K12 courses, aggressive spending on sales and marketing, and the performance of other online education companies.

From end of 2008 to end of 2017, Taiwan Semiconductor Manufacturing Company (TSMC) (2330 TT) had a remarkable run with the share price up more than 400%. However, TSMC share price has not fared so well in the past year with its share price down nearly 16% during this period. In this report, we provide a BEAR INVESTMENT CASE for TSMC. We do not believe all its troubles are over. Rather, we expect its sales and earnings to be much lower than the consensus in 2020. The following are the seven major reasons that are likely to negatively impact TSMC’s share price and its financials in the next two years:

The major tipping point period of higher demand for autonomous vehicles (which is likely to drive higher incremental demand for semiconductor products) is not likely until 2023. [Timing of incremental customers demand]

The major tipping point period of higher demand for 5G service (which is likely to drive higher incremental demand for semiconductor products) is not likely until 2021/2022. [Timing of incremental customers demand]

Increasing threats to Apple. [Threats to a major customer]

Major semiconductor memory prices such as DRAM and NANDFlash have been declining in the past few weeks. This could foreshadow a further softening of demand and prices in the entire semiconductor sector, including the foundry. The semiconductor companies increased their capex excessively in 2017 and this is likely to result in further reduced prices in 2019. [Concerns about oversupply/capex]

Collapsing demand for cryptocurrency mining machines. [Concerns about a customer segment]

Taiwan Semiconductor Mfg Co has dominated the foundry segment over the past two decades. With revenues of $33 billion in 2017, the company had a 56% share of the foundry market and was over five times the size of its nearest competitor, Globalfoundries. Under the visionary leadership of Morris Chang, TSMC effectively invented the fabless model. Originally mocked by former AMD CEO Gerry Sanders who once famously quipped that “real men own fabs”, the fabless model has evolved into a thriving ecosystem, one which has facilitated the meteoric rise of some of the biggest names in the semiconductor segment including Apple, Qualcomm and Nvidia.

TSMC’s success has been predicated upon the company’s so-called Trinity of Strengths, namely process leadership, manufacturing excellence and customer trust. In today’s highly competitive foundry landscape, those strengths have never been more significant.

While the smartphone processor business has been central to TSMC’s growth in recent years with Apple accounting for some 22% of revenues, the company is well positioned to diversify and benefit from high, secular growth trends in IoT, Automotive and AI acceleration. Even more significantly, TSMC is set to compete for the first time with Intel in the lucrative data center market by virtue of its role in manufacturing server chips for Advanced Micro Devices and a growing swathe of ARM-based server initiatives lead by none other than Amazon.

Between 2006 and 2017, TSMC grew at a CAGR of 9.8% in NT$ terms, easily outpacing growth of both the broader semiconductor segment and its foundry peers. For the period 2019-2022, we model TSMC growing at a slightly lower CAGR of 8.36%, but nonetheless more than double the anticipated CAGR for the semiconductor segment as a whole.

From end of 2008 to end of 2017, Taiwan Semiconductor Manufacturing Company (TSMC) (2330 TT) had a remarkable run with the share price up more than 400%. However, TSMC share price has not fared so well in the past year with its share price down nearly 16% during this period. In this report, we provide a BEAR INVESTMENT CASE for TSMC. We do not believe all its troubles are over. Rather, we expect its sales and earnings to be much lower than the consensus in 2020. The following are the seven major reasons that are likely to negatively impact TSMC’s share price and its financials in the next two years:

The major tipping point period of higher demand for autonomous vehicles (which is likely to drive higher incremental demand for semiconductor products) is not likely until 2023. [Timing of incremental customers demand]

The major tipping point period of higher demand for 5G service (which is likely to drive higher incremental demand for semiconductor products) is not likely until 2021/2022. [Timing of incremental customers demand]

Increasing threats to Apple. [Threats to a major customer]

Major semiconductor memory prices such as DRAM and NANDFlash have been declining in the past few weeks. This could foreshadow a further softening of demand and prices in the entire semiconductor sector, including the foundry. The semiconductor companies increased their capex excessively in 2017 and this is likely to result in further reduced prices in 2019. [Concerns about oversupply/capex]

Collapsing demand for cryptocurrency mining machines. [Concerns about a customer segment]

Taiwan Semiconductor Mfg Co has dominated the foundry segment over the past two decades. With revenues of $33 billion in 2017, the company had a 56% share of the foundry market and was over five times the size of its nearest competitor, Globalfoundries. Under the visionary leadership of Morris Chang, TSMC effectively invented the fabless model. Originally mocked by former AMD CEO Gerry Sanders who once famously quipped that “real men own fabs”, the fabless model has evolved into a thriving ecosystem, one which has facilitated the meteoric rise of some of the biggest names in the semiconductor segment including Apple, Qualcomm and Nvidia.

TSMC’s success has been predicated upon the company’s so-called Trinity of Strengths, namely process leadership, manufacturing excellence and customer trust. In today’s highly competitive foundry landscape, those strengths have never been more significant.

While the smartphone processor business has been central to TSMC’s growth in recent years with Apple accounting for some 22% of revenues, the company is well positioned to diversify and benefit from high, secular growth trends in IoT, Automotive and AI acceleration. Even more significantly, TSMC is set to compete for the first time with Intel in the lucrative data center market by virtue of its role in manufacturing server chips for Advanced Micro Devices and a growing swathe of ARM-based server initiatives lead by none other than Amazon.

Between 2006 and 2017, TSMC grew at a CAGR of 9.8% in NT$ terms, easily outpacing growth of both the broader semiconductor segment and its foundry peers. For the period 2019-2022, we model TSMC growing at a slightly lower CAGR of 8.36%, but nonetheless more than double the anticipated CAGR for the semiconductor segment as a whole.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

On November 6th, NTT (Nippon Telegraph & Telephone) (9432 JP)announced a ¥150 billion buyback program, and NTT Docomo Inc (9437 JP)announced that its very large ¥600 billion buyback program presented days before would be done through a single below-market-price Tender Offer where NTT was expected to be the only seller. That left NTT buying shares on market and NTT Docomo buying shares off-market in the immediate future.

The Tender Offer went through as planned (though NTT sold a tiny trifle less than expected).

On January 7th, NTT announced it had repurchased 8.4mm shares for ¥38.8 billion, leaving only ¥15.35 billion to repurchase in this program. That is worth about 7-8 trading days of buying. The buyback is therefore almost done.

A hint as to the future came in a Nikkei article in December. It may be many months before we see more NTT on-market buybacks.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: those with a market capitalization of above USD 5 billion, those with a market capitalization between USD 1 billion and USD 5 billion, and those with a market capitalization between USD 500 million and USD 1 billion.

In this report, we will explain our strategy for trading NCsoft Corp (036570 KS) shares in 2019. NCsoft is expected to launch five new mobile games in 2019 including “Lineage 2M”, “AION 2”, “Blade & Soul 2”, “Blade & Soul M”, and “Blade & Soul S”. These five new games are based on its existing MMORPG franchise games. The company is hoping to release all five of these new mobile games in 1H 2019.

Lineage 2M, which is perhaps the most anticipated mobile game among these five games, is expected to be launched in 2Q19. Traders are starting to gear up for the launch of this important game in the coming months. Many investors are likely to take the “buy on rumor and sell on news” strategy, which in this case the news would refer to the launch of the Lineage 2M game.

Nonetheless, in this case, we believe that because many investors may be getting ready to sell NCsoft near the launch date of Lineage 2M, many savvy investors are likely to sell their shares a few days/weeks earlier than the actual launch date. At this point, the most likely period as to when Lineage 2M may be launched is in May 2019. As a result, a good time to consider selling NCsoft may be sometime in March/April 2019.

In this week’s GER M&A wrap, we highlight the dwindling likelihood of a follow-on deal for Don Quijote Holdings (7532 JP) , which is now trading below terms. Secondly, we take a contrarian view on the M1 Ltd (M1 SP) deal and contend there is less likely to be a bidding war. Finally, we update on rejected by Healius (HLS AU) and provide a comprehensive list of upcoming catalysts for near-term M&A deals.

The rest of our event-driven research can be found below.

Best of luck for the new week – Rickin, Venkat and Arun

We expect Chinese domestic express demand to continue to moderate in 2019, and in response we expect the express companies to increase their investments in ‘last-mile’ and international delivery, which will probably create a drag on profitability in the medium-term. Although we believe e-commerce giants Alibaba and JD.com would like their growing portfolios of logistics investments to become self-funding sooner rather than later, we foresee somewhat limited investor appetite for more large Chinese logistics IPOs in 2019, since many high-profile offerings have faltered since going public.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In November 2017, Toshiba Corp (6502 JP) bowed to the inevitable and issued shares in order to shore up shareholder equity ahead of the 31 March 2018 deadline where if the company had not announced a positive shareholder equity number, it would have been delisted according to the Enforcement Rules of the Tokyo Stock Exchange.

So it issued ¥600 billion of equity in an accelerated privately-negotiated placement to hedge funds. There was some jawboning later from domestic institutions who had not gotten the show on the deal, but they would do well to remember that when Toshiba was in dire straits earlier that year, and continued listing was not guaranteed because of accounting issues which were later overcome (before the equity issuance), it was the hedge funds who bought dozens of percent of the company – not domestic financial institutions. In any case, the equity was predictably needed, but as a way of making it clear that it would not be forever, the release accompanying the financing said the company would accelerate returns to shareholders once the sale of Toshiba Memory Corporation was complete.

That return of capital to shareholders was announced in June 2018 after the closing of the TMC transaction had been confirmed. Toshiba would buy back ¥700 billion of shares. At the time, that was up to 40% of shares outstanding, but the shares rose as the shares of companies with large buyback plans do, and it took until November to dot the “i”s and cross the “t”s on making sure that the cash in the bank account was deemed distributable capital surplus. On November 8th, a year after announcing the sale of equity, Toshiba announced the start of a Very Large Buyback. A few days later the company announced a large ToSTNeT-3 buyback, offering to buy back all ¥700 billion of shares the following morning at that day’s close. A week later the company had bought back ¥243 billion or more than 35% of the total buyback then announced further purchases would be made in the market.

That’s when the fun began.

For previous recent treatment on the Toshiba buyback, see the following:

We have received requests to provide a calendar of upcoming catalysts for near-term M&A, stubs and erstwhile event-driven names. Below is a list of catalysts over the near-term for such names as below. If you are interested in importing this directly into Outlook or have any further requests, please let us know.

After initially being very skeptical of the China Tower (788 HK) IPO given it is essentially a price take to its three largest shareholders, we changed our view in early December to a more positive outlook. What changed our view has been series of calls and meetings with the company that suggested a more shareholder friendly approach than expected and a real opportunity to reduce capex substantially through the use of “social resources” (e.g. electricity grid, local government sites). These can be used to deliver co-locations without building towers and poles and imply much lower capital intensity at a time when revenue growth will be accelerating as 5G is rolled out. Management has also given more detail on non-Tower business prospects which can generate higher returns (not under the Master Services Agreement). While small now (2% of revenue) they are growing rapidly. With lower capex than initially guided and a more shareholder friendly management (i.e. higher dividends are possible) we reduce the SOE discount and raise our forecasts (again). We remain at BUY with a new target price of HK$2.20

After three-plus months of speculation that Axiata Group (AXIATA MK) was unhappy with the price and might make a counter-offer, no offer has been forthcoming.

After I wrote on the 2nd in M1 Offer Coming – Market Odds Suggest a Bump But… that the reward/risk did not look that great, shares drifted downward from the S$2.09-2.11 area and into the afternoon of the 7th, traded in the S$2.05-2.07 range, which was the first time in months the shares had traded at or below the prospective offer price.

chart source: Investing.com

Some 20mm+ shares (5.5% of the shares out other than the three major holders) traded between 3pm Singapore time on the 7th and a few minutes after the open the day after the announcement. Then part-way through the day, someone bought a large number of shares lifting the share price two spreads for a while. Since then, the shares have settled back down to the $2.07-2.08 range.

Depending on your opinion of the likelihood of a bump, your execution strategy will differ. It’s still not clear that a bump or counterbid will be forthcoming, but at S$2.07, the risks are better than they were higher.

It was reported on January 3rd that Korean founder and heretofore effective controller of Nexon Co Ltd (3659 JP) Mr. Kim Jung-Ju and family, who exercise their ownership of Nexon through near 100% (98.64% according to Douglas Kim) control of NXC Corp (Korea) and NXC’s control of NXMH B.V.B.A (Belgium), planned to sell their stakes in NXC for up to 10 trillion won (US$8.9 billion).

Those two companies – NXC Corp (Korea) and NXMH (Belgium) – own 253.6mm shares and 167.2mm shares respectively, or direct and indirect ownership by NXC of just under a 48% stake in Nexon (3659 JP). Yoo Junghyun (Kim Jung-Ju’s wife) directly holds another 5.12mm shares at last look.

Nexon was founded in Korea in 1994 and moved its headquarters from Seoul to Tokyo in 2005, listing itself on the TSE in December 2011. The company is a well-known gamemaker (over 80 PC and online/mobile games), with famous games such as MapleStory, Dungeon & Fighter, and Counter Strike.

The Korea Economic Daily said in its report on the 3rd of January that Deutsche Bank and Morgan Stanley had been selected as advisors to run a sale process, and a formal non-binding offer to potential bidders was expected next month. A Korea Herald article suggested that “potential buyers, according to industry speculation, include China’s Tencent, Korea’s Netmarble Games, China’s NetEase and Electronic Arts of the US.”

The Big Question

In the second piece, Douglas Kim questions whether Kim Jung-Ju would sell NXC (and NXMH) as reported by the local press, or whether NXC and NXMH would sell their stakes in Japan-listed Nexon, the implication being that if they sold the stake in Nexon, it would mean buyers would get a large stake in a single company, whereas there is a bunch of other stuff floating around in NXC and its subsidiaries.

The other question is whether Tencent or another buyer buying NXC would trigger a mandatory Tender Offer for the shares in Nexon in Japan. The letter of the law in the TOB Rules changed a bit over 10 years ago would indicate not, but there are questions (and precedents) here.

Discussion ensues.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The recent trade talk meeting between the US and Chinese government went into an extended unplanned third day which could be seen as a positive development – a sign that both sides are serious on getting a deal done. President Trump’s recent tweet citing “”Talks with China are going very well!” has been responded positively in Asian equities market. Is it all just that or are there more in the company?

Ideally, own Bandhan Bank (BANDHAN IN) on a deal break, or wait for this deal and its spread to season a bit.

It’s still not clear that a bump or counterbid will be forthcoming in the M1 Ltd (M1 SP) deal, but at S$2.07, the risks are better than they were higher.

Healius (HLS AU) (unsurprisingly) rejects the indicative offer but Jangho is not out of the picture; nor is the possibility of a third party.

Douglas Kim revisited the news that Kim Jung-Joo wants to sell his stake in the Nexon Group. Travis Lundy also chimed in with his read of the situation. The key questions are whether Kim Jung-Ju would sell NXC (and NXMH) – which holds a 48% stake in Nexon Co – as reported by the local press, or whether NXC and NXMH would sell their stakes in Japan-listed Nexon. The implication being that if they sold the stake in Nexon, it would mean buyers would get a large stake in a single company, whereas there is a bunch of other stuff floating around in NXC and its subsidiaries.

The other question is whether Tencent Holdings (700 HK) or another buyer buying NXC would trigger a mandatory Tender Offer for the shares in Nexon in Japan. The letter of the law in the TOB Rules would indicate not, but Travis reckons Yes. If the Kim family sold their stake in NXC Corporation to a buyer, he thinks it is HIGHLY likely that the buyer would be obliged (by Japanese authorities) to conduct a tender offer for the shares of Nexon that they wanted to buy.

As a trade, this does not look like a great risk arb bet (where you make a bet that a company will get taken over) at first glance if the total trade for NXC is going to be ₩10tn. It would be a good trade if the ₩10tn number were made up of say ₩3tn of assets (in NXC), then the assumption that the current market price adding ₩7tn of assets to arrive at that total of ₩10tn would be an “estimate” of current value rather than an estimate of what it would take to get the deal done, and current market value is a significant premium to book (where NXC has heretofore reported its financials and Nexon). In that case, one might imagine that a bidding war could result in a higher price for Nexon, and an easy exit at ¥2000+/share.

Either way it would be a chunk of change which would make many buyers – even buyers from China thought to be quite wealthy – balk. A priori, Travis would want to own Nexon vs Tencent, Electronic Arts (EA US), Netease Inc (Adr) (NTES US), and others, but it is not necessarily a comfortable trade.

Konnectivity Pte. Ltd officially announced the launch of its Offer to by M1 Ltd (M1 SP). The Close is 4 February, but the Offer is not Final.

If you think there will not be a bump and the deal may or may not go through at S$2.06, unless you are so big that your selling would dramatically impact the price, the right trade here is to sell in the market.

If you think there is a possibility of a bump as the Offeror seeks to a) get Axiata to tender and b) to get everyone else to tender so they can delist and squeeze out minorities, but if no bump there is a quasi-certainty that Konnectivity Pte will gain 50%+1 share at S$2.06, then buying at S$2.07 is not a bad trade depending on your likelihood of bump and bump price.

If Konnectivity bump, they have two choices: Bump a little bit and declare final so that everyone who played for a bump decides to sell (that might mean a bump to S$2.15 or so); or bump a lot and get Axiata out.

Travis believes a bump is certainly possible but also thinks this deal gets done if there is no bump. If Axiata countered at, say S$2.15, he would be inclined to buy at S$2.15 to expect a further counter by Konnectivity.

Bandhan Bank (BANDHAN IN)(“BBL”) and GRUH announced together on January 7th that their respective boards have considered and approved a Scheme of Amalgamation where Bandhan Bank will be the acquiring entity and GRUH Finance will become the acquired entity. At the exchange ratio of 568 Bandhan Bank shares per 1000 GRUH Finance shares, GRUH Finance’s price currently translates to a PER and PBV of 51.8x and 12.5x respectively which is significantly higher than the average for its comparable peers (PER=14.9x; PBV=2.0x).

This is a great deal forHousing Development Finance Corporation (HDFC IN)which currently owns 57.8% of GRUH Finance. It will own 15% of the merged entity. Considering HDFC Ltd already owns 19.72% as the promoter of HDFC bank and that RBI does not allow the promoter of one bank to hold more than 10% in another bank as a promoter, HDFC Ltd will have to divest a stake that is at least equivalent to 5% of the merged entity.

This deal is perhaps less good for Bandhan shareholders. GRUH is being purchased expensively, and minorities are getting hit. This is possibly so that the promoter can get closer to the obligation to the RBI to drop his stake to 40%. That ‘excuse’ is widespread in the media but may not bear up under scrutiny.

Travis thinks both names could have further to fall and sees no compelling reason to expect growth to surprise on the previously expected upside as branch openings are frozen. A deal break would not solve that, but a shareholder disentanglement on the Bandhan side would.

As widely expected, Healius’s board rejected the unsolicited and conditional proposal from Jangho Group Co Ltd A (601886 CH) at A$3.25/share.Pricing under the proposal is okay, at best, valuing Healius roughly in sync with Sonic Healthcare (SHL AU), its nearest peer. Optically, the indicative offer is underwhelming, 20% below the recent high in March last year, and below where Jangho was accumulating its stake in early 2016.

Operationally, Healius is not without issue, including increasing salaries, failure to secure key contracts, an inability to retain doctors at its medical centres, and the forced resignation of its CEO two years ago after he was charged by ASIC.

An offer from Jangho would also fall under FIRB’s remit, specifically sensitive patient data in the hands of a foreign owner, and it is up for debate whether maintaining such information in a secure site in Australia (as applied in Jangho’s acquisition of Vision Eye in 2015) will alleviate these concerns.

This deal is unlikely to get up under the current terms following the board rejection, but I do expect Jangho to bump its offer; or a third party to enter the fray. On a risk/reward basis I still tilt positive at a 18% gross spread (and up 7% from the post-rejection closing price) to the indicative offer.

For those who like plain vanilla, PCI announced Pagani Holding (an SPV indirectly owned by Platinum Equity Advisors) had made a S$1.33/share cash offer for the company by way of a scheme. Chuan Hup Holdings (CH SP), which holds 76.7% in PCI, has given an irrevocable undertaking to vote its stake in favour of the scheme resolution. So this is a done deal. The more interesting facet here is that Chuan Hup is currently trading at discount to its net cash after factoring in the proceeds from the sale of PCI shares.

As anticipated in my insight (DNO Closes In On Faroe) last week, DNO ASA (DNO NO)bumped its Offer for Faroe, which has now been declared unconditional. Tendered shares get paid in 14 days. The final closing date of the offer is the 6 February.

The 5.3% bump to GBP 1.60/share shortly followed a prior announcement from DNO which referenced a statement made the previous day by the Norwegian Petroleum Directorate of a 30% reserves downgrade at Faroe’s Oda field from 47.2mn MMboe to 32.7 MMboe.

The Final Offer price represents a premium of 52.4% to Faroe‘s share price of GBP 1.05 at the close of business on 3 April 2018, and values Faroe at ~£641.7mn. Despite open hostilities to the initial offer, Faroe’s board has now accepted the increased Offer and recommends shareholders tender.

DNO now owns or has 76.49% acceptances so can now make preparations to move to delist Faroe. If total acceptances exceed 90% of the voting rights, DNO will exercise its rights to compulsorily acquire the remaining Faroe shares not tendered, also at GBP 1.60/share.

The company bought back 16% of volume in the month (in December), and 15% of rolling 4-week ADV if only the first 20 days were days on which the company bought – which based on execution prices seems likely.

Travis expects a similar rate to continue and expects the lower trading volumes seen in December to continue. The period of excitement is over until Toshiba gives people a reason to get excited.

Travis is not particularly bullish Q3 results or Q4 forecasts for the company and the stock has rebounded perhaps more than the market has off lows. With Apple Inc (AAPL US) guiding suppliers to lower iPhone production yet again, TMC could run into a soft spot.

The key stub assets include South Springs, one of the largest golf resorts in Korea, and brand royalty, each accounting for around 7-8% of NAV. The remaining, immaterial ops include an ad agency, an “Amazon Fresh”-like fresh food delivery start-up, management consulting, dividends, and rent.

This looks like a decent stub-setup, with a likelihood of the discount narrowing from here – typically, the Korean Holdcos trade within a 20-40% discount band – rather than clearing 60%. And there is no tender offer overhang in 2019. But apart from the optics, there are no obvious catalysts at the stub level for the nine-month discount-widening trend to reverse.

Kingboard, which hasn’t been in the news since it sold its 9.6% stake in Cathay Pacific Airways (293 HK) to Qatar Airways back in November 2017, is coming up “expensive” on my monitor, after KBC’s mid-week price outperformance over KBL.

The new news this week is that KBC announced it is acquiring a handful of floors of the Overseas Trust Bank Building here in Hong Kong. Pricing looks okay with reference to property sold nearby, but probably towards the high-end for mid-floor office space in Wan Chai.

This is a connected transaction as the seller of the properties is Hallgain Investments – a vehicle largely owned by senior management of KBC – which owns 39.02% of KBC. The net rental on the properties is $1.35mn or a yield of 0.15%, which hardly augurs a case to go long the stub.

I compiled a summary of the 93 M&A transactions, with a collective deal size of ~US$215bn, published on Smartkarma in 2018, and analysed which sectors attracted the most interest: (Mostly Asia) M&A in 2018: What Was Hot, And What Was Not

The premium for Swire’s As over the Bs – [19 HK/(5* 87 HK)] – continues to increase and is now at its highest since October 2003.

Source: CapIQ; RHS represents HK$mn

I tackled this share class last August (Swire’s Interims and Bifurcating Dual Class) when the premium was 18%. Since September 2015, the two classes of shares can be unified leaving John Swire & Sons with 55% of the equity (& 63.7% of the vote). The pushback then, and now, is why bother? And the HKEx giving permission to Xiaomi Corp (1810 HK) to list with dual-class shares lessens the chance of such a unification.

Logically though, this premium should narrow (eventually one would expect) and investors are betting on this. The $ value traded for the Bs on Wednesday was the highest since mid-December 2017, and the third highest $ value traded in 21 years. And volume for the Bs has been increasing recently, having doubled in size in the past year compared to the 5-year average.

As an aside, Swire’s discount to NAV (adjusting for the privatisation of HAECO) is trading at it narrowest inside a year:

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

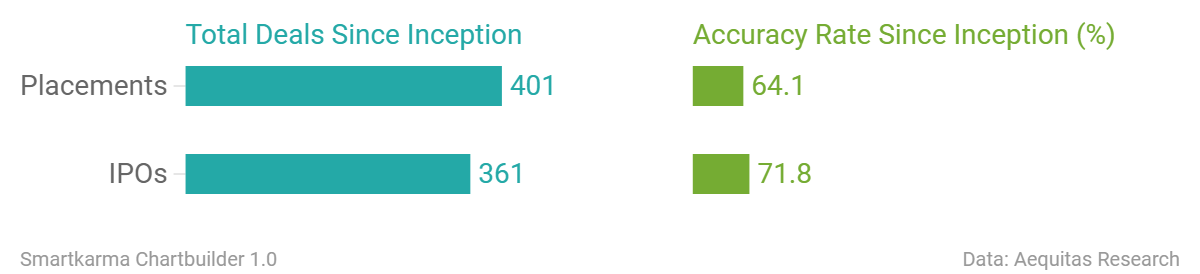

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Despite a shaky 2018 Q4 market and the disappointing Softbank Corp (9434 JP)‘s IPO, we have been getting a steady stream of newsflow on upcoming IPOs.

Starting with upcoming IPOs, Chengdu Expressway Company Limited (1785 HK) and Weimob.com (2013 HK) will be listing next week on Tuesday, 15th January. Weimob was priced at the low end of its price range while Chengdu Expressway’s IPO was at a fixed price of HK$2.20. We are bearish on both IPOs. Weimob is overly reliant on Tencent for its SaaS and Ads business and, at the same time, Tencent will only own less than 3% stake after listing. Whereas Chengdu Expressway has been a well-managed company but valuation implies limited upside. Trading liquidity will likely remain tepid as like Qilu Expressway Co Ltd (1576 HK) which listed mid last year.

In the pipeline, we are hearing that Kepei Education (KEPEI HK) will likely open its book next Monday. We will be following up with a note on valuation. In other IPOs that are coming in this quarter, Helenbergh China and Zhongliang, both property developers, are looking to IPO in this quarter. Viva Biotech Shanghai Ltd (1577881D HK) is also looking to list in Hong Kong Q2 while Urban Commons, a US property developer, is planning a US$500m REIT IPO in Singapore.

Activity seems healthy for the ECM space, but sentiment has not been the best as seen from Xiaomi’s high profile IPO that took a hit just as its lockup expired. Its share price has corrected from a high of HK$22.20 to just above HK$10.34 this Friday. This should not have been a big surprise since many have already pointed out that its valuation should really have been closer to that of a hardware business and we pointed out that the IPO’s trajectory would likely be similar to Razer.

This reminds us of a particular listing last year, Razer Inc (1337 HK) , and, in fact, both bear quite a handful of similarities. Strong portfolio of investors, hardware business with software capabilities, expensive valuations, and etc. The stock did well at first but has come back down to earth since then.

Accuracy Rate:

Our overall accuracy rate is 72% for IPOs and 64% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

China Tobacco International (Hong Kong, US$100m)

China East Education (Hong Kong, US$400m)

Ebang International (Hong Kong, re-filed)

MicuRx Pharma (Hong Kong, re-filed)

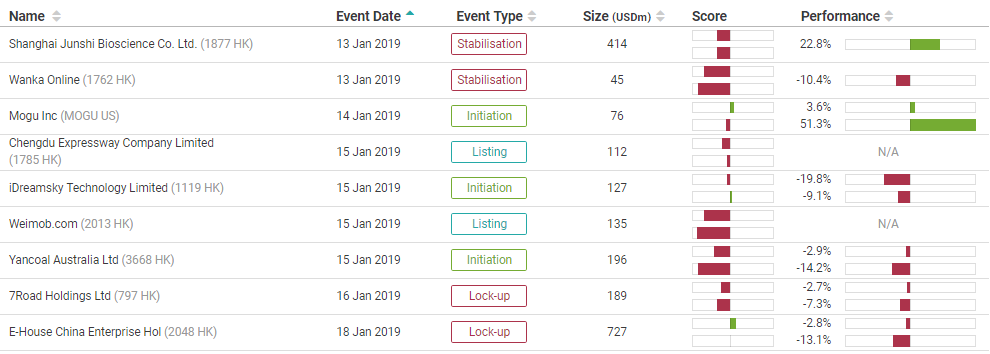

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

In the three months to December, MonotaRO’s domestic (parent company) sales continued to grow at an annual rate close to 25%, indicating that full-year consolidated results should be close to management’s guidance and our own estimates. This also suggests that our 18% sales growth forecast for 2019 could be conservative.

Parent company data for December show sales up 18.4% year-on-year in nominal terms, but up 24.6% when adjusted for the number of working days in the month. The figures for November were 27.3% growth in nominal terms, but 21.3% adjusted.

In the three months to December, adjusted sales were up 24.2%, a slight improvement from 23.9% growth in 3Q. In FY Dec-18 as a whole, reported parent company sales were up 24.4% to ¥105.3 billion, slightly exceeding management’s ¥104.1 billion guidance.

At ¥2,523 (Friday, January 11, close), the shares have dropped 25% since October. They are now selling at 61x our EPS estimate for FY Dec-18, 54x our estimate for FY Dec-19 and 47x our estimate for FY Dec-20. Price/sales multiples for the same three years are 5.7x, 4.8x and 4.2x.

Consolidated results for FY Dec-18 are due to be announced by the end of January.

MonotaRO is the only pure-play e-commerce MRO (Maintenance, Repair and Operation) investment in the Japanese stock market. With over 10,000 SKUs (stock keeping units – i.e., individual items, including gloves, hand and power tools, hardware, painting supplies, etc.) for sale to construction companies, manufacturers, auto repair shops and other customers, the company is both driving and benefitting from the growth of Japan’s B2B MRO market. Overseas subsidiaries in South Korea, Indonesia and China, which account for about 4% of consolidated sales, are not yet profitable.

We highlighted in a recent note Chris Hoare‘s positive outlook for China Tower (788 HK). Our view takes into account the 5G build-out commencing this year, improved capex efficiency from using “social resources”, the rapid growth in non-tower businesses that lie outside the Master Services Agreement (MSA), and the valuation benefit from what looks like surprisingly investor friendly management.

This note focuses on four key issues facing the Chinese telcos in 2019:

5G capex (March) (this is by far the most important),

Regulatory newsflow (February/ March),

Operating trend improvements (August), and

Emerging business opportunities driving future growth (August).

We remain positive on the telcos which trade at low multiples. China Unicom (762 HK) continues to trade at a discount, yet is most exposed to the positive story emerging at China Tower. We switch our top pick among the telcos from China Mobile (941 HK) back to China Unicom as a result. Alastair Jones thinks China Telecom’s (728 HK) premium multiple is at risk if management execution on the cost base doesn’t improve. It is our least preferred telco at this stage. Overall, we expect China Tower to outperform all telcos and it is our top pick. The upgrade to China Tower flows through the telcos (valuation and costs) and our new target prices are as follows: China Unicom to HK$14.4, China Telecom to HK$5.4 and China Mobile to HK$96.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

An undisclosed institutional shareholder of Xiaomi Corp (1810 HK) is looking to sell 231m shares of the company for approximately US$273m.

There will likely to be more selling pressure in the near term. The 594m shares sold down by Apoletto and the anonymous shareholder who sold at a 14% discount does not inspire confidence. Furthermore, there will be even more overhang to come from the twelve-month lock-up expiry. The deal also scores poorly on our framework owing to its expensive valuation and the lack of information on the seller.

Weimob.com (2013 HK) IPO was priced at the low-end at HKD2.80/share. The retail tranche was 0.79x covered while the institutional tranche was slightly over-subscribed.

I’ve covered most aspects of the deal in my earlier insights:

In this insight, I’ll provide an update on the deal dynamics, valuations and provide a table with the implied valuations at different share price levels.

Take out an ad in a magazine or pay a one of the Wondergirls to post an Instagram photo of herself using our makeup? How do we get Americans and Europeans to want our bubble tea sleeping packs and panda-shaped palettes? All valid questions for K-beauty companies in the midst of a global expansion.

Source: Internet – Chosungah Beauty

Korean beauty products powerhouse, Amorepacific is going through some growing pains at the moment. In the 3Q18 the group reported a YoY sales increase of 6% but OP tumbled 24% due to increased personnel and marketing costs. In a management policy statement last week, Chairman Suh outlined the problems the group is encountering as it copes with reaching customers in a world where online and offline customer interaction is changing.

The stub is now trading at its widest discount to NAV in at least 3 years and has reached 22% discount to its Sum of the Parts NAV by my calculations. This level represents a level 1.5 standard deviations below its long-term average and also offers compelling value.

In this insight I will detail:

an actionable market-neutral trade idea

an analysis of the various business units of Amorepacific

reasons for the under-performance of Amorepacific parent and a sign of a rebound

a recap of ALL my stub trade ideas on Smartkarma, including track record of performance

Tim Cook passed the buck to the weak sales in China. However, we believe China’s retailing is running well based on our visits to shopping malls with Apple stores.

Luxury goods sold better in China than all other major markets in the world in 2018.

We believe that the price reduction in Mainland China is just taking market share from Apple Stores in Hong Kong, but not from competitors.

We also believe that the app review process is the fatal shortcoming for AAPL.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We are bullish on the Chunbo Co. IPO. Our base case valuation of the company suggests a market cap of 448.4 billion won or44,845 won, which would be 19.5% higher than the mid-point of the bankers’ IPO price band of 37,500 won. We used an estimated P/E of 21.1x (30% premium to the comps’ average P/E of 16.2x) and an estimated net profit of 21.2 billion won in 2019 to derive our base case valuation.

Chunbo Co Ltd (278280 KS) is a provider of fine chemical materials in Korea, is planning to start its institutional bookbuilding of its IPO starting January 21st. Its chemical materials are used in numerous industries including the display, semiconductors, rechargeable batteries, and medical. The IPO base deal size is between $78 million to $89 million.

Chunbo is more profitable and generates higher returns on equity than its peers. For example, Chunbo’s operating margin and ROE averaged 20.7% and 22.0%, respectively in 2016 and 2017. In comparison, the peers’ operating margin and ROE averaged 12.3% and 15.2%, respectively in 2016 and 2017.

Xiaomi Corp (1810 HK) is likely to break HK$10 this morning again after a placement equal to about 1% of shares outstanding was proposed to buyers last night at a sharp discount to the close. This insight attempts to nail down the shape and size of the ongoing overhang.

After the HK Stock Exchange announced in late April 2018 that it would permit companies with Weighted Voting Rights (WVRs) to list on the HKEx, after sticking to the one-share one-vote principle for years (losing the Alibaba Group Holding (BABA US) listing to NASDAQ in the process), Xiaomi Corp (1810 HK) quickly raised its hand with the prospect of a US$10bn IPO and a US$100bn market cap – heady numbers even for a fast-growing company. This was quickly followed by the launch of the China Depositary Receipt program which saw a quick establishment and even quicker acceptance of a Xiaomi application, potentially setting up a situation where demand was pulled from HK to China.

Then investors got cold feet, and what was a $100bn valuation dropped to $90bn then $70bn. The CSRC also pushed back on the possible CDR issuance to such an extent that Xiaomi withdrew its application, and then pricing delivered a valuation of approximately US$50bn at a sharply reduced IPO price of HK$17/share.

Day1 saw a 6% fall on the open and the shares closed down 1%. After the Day 1 close, fast-track inclusion into the Hang Seng indices was a pleasant and somewhat unexpected surprise for IPO buyers and responded by rising almost 12% on Day 2 on sharply higher volume. MSCI did not follow suit (it had not been expected) but several days later on inclusion day, the stock was 25% higher than the IPO price. 10 days later the over-allotment option had been fully-exercised.

Xiaomi last year grew its ecosystem and its hardware base, but saw lower market share in China (13%) than in 2017 (14%) according to several sources, including Counterpoint Research quoted in the media. The company, which has targeted 50% of revenue from overseas is now just shy of that mark at 44% after ramping up sales in India, Europe, and MENA.

Global weakness in handsets on mobile tech led by Apple did not spare Xiaomi, but MOST notable was the sharp drop in the share price in December from HK$14.30-50 area to just below HK$13 at year end. The first day of the new year saw the shares fall 5.5%, and the next day the price fell another 3.6%. The shares fell a little more in the next few days but somewhat stabilised until the morning of the 8th.

Then the volume picked up. The lockup had expired.

data: capitalIQ, exchange data

In five days, the shares have traded 880mm shares, and that is before a large placement proposed after the close on 15th January.

A rising pro-market tide has lifted the big-cap banks, but now it is time to be more selective. We see further potential for stock re-rating among the Brazilian banks, as the new Bolosonaro administration executes its pro-market policies.

Our top pick is Banco Do Brasil Sa (BdoBAS3 BZ) , with a target price of BRL57, which implies 19% re-rating potential. We believe that Banco do Brasil (BdoB) shareholders are set to benefit from less of a “social programme” agenda which in turn should help improve ROE going forward.

Yet the PBV discount between BdoB and its private sector peers – especially against Itaú Unibanco at 52% – has barely narrowed, and we believe that the discount has potential to narrow further as BdoB’s ROE expands and narrows the gap with its private sector peers.

Following Yaskawa’s second downward revision at 3Q earnings, we are shifting towards a more positive stance on the stock, even from a long-term perspective. We had been negative on the stock from late 2017 and as the stock tumbled we maintained that it was still too early buy for the long-term, though by mid-late 2018 we did (incorrectly) feel that there was the potential for a short term rally due to the severity of underperformance.

With the stock selling off harshly in the recent market fall but rebounding following its weak earnings we feel that much of the bad news is now priced in and expectations have corrected to the point where this is once again interesting on the long side.

Three key emerging risks to the Starbucks’ growth story: 1) New entrant poses a threat to China growth story; 2) New CEO is missing the magic of the beans; and 3) New Uber partnership could erode Starbucks’ brand equity.

In our January 8 research note, we cautioned that Starbucks had outperformed the NASDAQ by 37% since we turned positive on August 8 but we were concerned about two new developments that we viewed as red flags: shelving of Reserve coffee bar expansion and aggressive China expansion plans of Luckin Coffee. While we do not believe this represents a short opportunity, we do believe it foreshadows emerging risks to Starbucks’ long-term growth story.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

HOYA Corporation is currently trading at JPY6,867 per share which we believe is fairly valued based on our SOTP valuation. The company operates with a few stable businesses and holds solid shares in the markets in which it operates. The company generates nearly 50.0% of its revenue from its core business of selling eyeglass lenses and contact lenses. The advancement in eyeglass and contact lenses technology, the growth in global population with vision-related issues due to increased use of PCs, smartphones and tablets and an ageing population will drive demand for eyeglasses and contact lenses. Although the company’s IT Segment which generates around 33.0% of company revenue is growing slowly, the management has aggressively managed the costs to improve the segment’s pre-tax profit margin to over 40.0%. While the Lifecare segment remains the engine of revenue growth for HOYA, it focuses on the IT segment for profitability. HOYA has grown its businesses, mainly the Lifecare segment through value adding M&A deals. The company has announced that it has entered into definitive agreements to acquire US-based Mid Labs and Germany-based Fritz by the end of FY19 (March 2019). The proposed acquisitions could help HOYA to expand its footprint in the global retinal market and further its Lifecare growth. The company has a strong balance sheet with a debt-to-equity ratio of 0.3% as of 2QFY19 with cash and cash equivalents worth JPY252.3bn (35.2% of total assets).

According to our analysis, HOYA operates solid businesses with impressive ROE and positive FCF, however, we believe, the market has already factored most of this into the share price. Therefore, we believe HOYA is worth looking at on the long side if its management continues to find value adding M&A deals which complement its existing lines of business or new business opportunities which would be transformative for HOYA. Our valuation is neutral, but we favour HOYA within the sector as it has held up relatively well despite the tech sell off due to its attractive health care business and shareholder friendliness which was perhaps underappreciated while the market was in its bull phase.

Kingboard Chemical (148 HK)gets a boost after buying properties from its major shareholder, however, the implied yield is uninspiring.

Preceding my comments on BGF and KBC are the weekly setup/unwind tables for Asia-Pacific Holdcos.

These relationships trade with a minimum liquidity threshold of US$1mn on a 90-day moving average, and a % market capitalisation threshold – the $ value of the holding/opco held, over the parent’s market capitalisation, expressed as a % – of at least 20%.

HDC Holdings (012630 KS) and HDC-OP (294870 KS) price gap is now at a nearly record high. Holdco discount is now 60% to NAV. On a 20D MA, Holdco and Sub are currently below -1 σ.

I initiated a stub trade on the duo on Dec 11. It paid off on a short term horizon until the duo reached within -0.5~0 σ on a 20D MA. Yield peaked at 4.6% on Dec 14. If you approached with a longer term horizon, things wouldn’t have been as enjoyable.

The only possibly explainable factor for the recent price divergence is HDC I-Controls’ need to dump a 1.78% Holdco stake. 1.78% overhang risk is not enough to sustain this much divergence and current 60% Holdco discount.

The duo has again entered < -1 σ territory at yesterday’s closing prices. I’d first make another short-term stub trade. I’d hold onto the position until they reach within -0.5~0 σ on a 20D MA with a loss cut at -5%. But a little longer term approach to hunt for a higher yield wouldn’t be a bad idea at this point.

M1 Ltd (M1 SP), the third largest telecom operator in Singapore, is subject to a bid. On 7 January 2019, Konnectivity launched a voluntary conditional offer (VGO) at S$2.06 cash per share. Konnectivity is jointly owned by Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP).

M1’s shares are trading a touch above the VGO price of S$2.06 per share as the market is betting that Axiata Group (AXIATA MK) may ride in with its competing offer. However, we believe that shareholders should accept the offer as Axiata is unlikely to engage in a bidding war due to several factors.

According to a local media outlet called Chosun Daily, it stated that one of the bankers in the deal (Deutsche Bank), already sent teaser letters of this deal to Tencent Holdings (700 HK) and KKR and in the teaser letter, it mentioned about potentially selling nearly 47% of Nexon Co Ltd (3659 JP) (Japan).

The question about whether or not Kim Jung-Joo decides to sell NXC Corp (Korea) or Nexon Co Ltd (3659 JP) (Japan) has important consequences not just for him and his family but also to the minority shareholders of Nexon Co Ltd (3659 JP). If Kim Jung-Joo decides to sell NXC Corp (Korea), there may not be much upside for the minority shareholders of Nexon Co Ltd (3659 JP) since current regulations do not require the buyers to pay potentially additional control premium to the minority shareholders as well.

However, if Kim Jung-Joo decides to sell Nexon Co Ltd (3659 JP) (Japan), there may be an opportunity for the minority shareholders to gain from an additional control premium. We think that this is one of the reasons why Nexon Co Ltd (3659 JP) shares are up 13% YTD as some of the investors may think that there could be a higher probability that Kim Jung-Joo ends up selling Nexon Co Ltd (3659 JP) (Japan), instead of NXC Corp (Korea).

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

After an impulsive rise from the 110.5k dual bottom, Naver Corp (035420 KS) has formed a bull wedge that is expected to see a nice rally and perform over the Korean market.

RSI also shows a compelling set up for a rise.

Buy volumes are starting to improve and supportive.

Targets are 8% and 14% higher from current levels.

Macro pivot resistance will cap rally attermpts in Q1.

Since its founding in 1960 the Housing Development Board (HDB) has constructed over 1.1 million dwelling units across Singapore. Currently, over 80% of the Singapore population lives in HDB built housing. With the bulk of these buildings having been constructed between 1960-1988 many of them are up for extensive renewal and renovation works. Construction companies should benefit from this trend, as should the micro-cap Ips Securex Holdings (IPSS SP), a reseller of equipment that modifies HDBs with emergency monitoring systems for senior citizens.

Outgoing PM Lee Hsien Loong (LHL) was very outspoken about the need to upgrade HDBs and make them safer for many of SG’s “pioneers” and senior citizens during his speech at the 2018 National Day Parade (NDP). With a general election coming later this year (date TBC) investors in IPS can be hopeful that the company should be awarded some new contracts and finally end the three-year de-rating which has taken the stock from 0.32 SGD in December 2015 to 0.055 SGD recently.

IPS is cheap with a market cap of only 27M SGD (20M USD) but can only start to re-rate on new major contract announcements.

A year ago we began publishing Tracking Traffic/Chinese Tourism as the hub for all of our research on China’s tourism sector. This monthly report features analysis of Chinese tourism data, notes from our conversations with industry participants, and links to recent company news and thematic pieces. Our aim is to highlight important trends in China’s tourism sector (and changes to those trends).

In this issue readers can find:

A review of China’s outbound tourist traffic in November, which strengthened: Lifted by extraordinarily strong growth in visits to Hong Kong and, to a lesser extent, Macau, Chinese outbound travel demand rebounded strongly in the seven regional destinations we track. But the fact that November’s growth was led overwhelmingly by Hong Kong and Macau — destinations close enough for weekend or day trips from population centers in Southern China — suggests Chinese tourists’ purse strings are still tight.

An analysis of November domestic Chinese travel activity, which turned weaker: November data from China’s three leading airlines and the Ministry of Transport show moderating domestic travel demand. For combined rail, highway, and air travel, November demand grew by less than 3% Y/Y. Along with the change in destination mix for outbound travel (that favors ‘nearby’ destinations), it now appears domestic demand has weakened, too.

Links to other recent news & research on Chinese tourism: Readers can check out our quick takes on Macau’s December GGR figure, preliminary GTV and revenue figures released by Ctrip.Com International (Adr) (CTRP US), declining US visa issuance to Chinese tourists, and Qatar Airways’ new investment in a leading Chinese airline.

Although we remain positive on the long-term growth of Chinese tourism, it’s clear that near-term demand has weakened substantially. We continue to take a negative view of travel intermediaries like Ctrip, which face intensifying competition from many sources. We are more positive on the prospects of actual owners of Chinese travel and tourism assets, like hotel chain Huazhu Group (HTHT US) and Air China Ltd (H) (753 HK).

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The Japanese telecom market was more volatile in 2018 than anticipated. However, Chris Hoare remains broadly positive on the sector for 2019. While pressure on the revenue line is intensifying, we do do not expect a price war to break out. In fact, we look for volatility to ease as the year progresses. Operators point to opex reductions and handset subsidy reductions to offset revenue weakness. We think that earnings are likely to surprise on to the upside. Over time we also look for dividend payout ratios to gradually rise, with the Softbank Corp (9434 JP) (KK) listing the long term catalyst. For Softbank Group (9984 JP) (SB) we look for market confidence to improve on the Vision Fund strategy, as profitable exits/up-valuations of assets such as Uber are announced.

The sector is recovering from NTT Docomo’s (9437 JP) price cut announcements but we don’t think they will slash prices (cuts will be selective). Our top pick is now KDDI (9433 JP) which could actually benefit from Rakuten’s (4755 JP) entry (as the roaming partner). DoCoMo is most affected but there are plenty of cost cutting opportunities. NTT (Nippon Telegraph & Telephone) (9432 JP) has optimistic guidance with substantial opex and capex cost cuts planned. Our order of preference for the stocks is now: KDDI (Buy), followed in order by NTT (Buy), SB Group (Buy), DoCoMo (Buy) and SB Corp (Neutral). We do not currently cover Rakuten.

Would Wal Mart Stores (WMT US) have paid USD16 bn last year for Flipkart, a leading online Indian retailer, if the recent clarification on India’s policy on FDI in e-commerce were in place back then? Foreign owned online retailers in India ( Amazon.com Inc (AMZN US) , Wal Mart Stores (WMT US) and Alibaba Group Holding (BABA US) ) will need to rejig their operating models and may face prospects of slower growth and even more distant breakeven targets, if the Indian Government is indeed determined to enforce its policy that e-commerce ‘Marketplaces’ operate only as platforms for third party vendors. Unsurprisingly, Amazon.com Inc (AMZN US) and Wal Mart Stores (WMT US) have reportedly teamed up to lobby the government on these regulations.

The Indian Government had posted a one-page circular on Dec 26th giving further clarifications to its existing policy on foreign owned e-commerce entities. The detailing of policy specifics seems to be an attempt to enforce the existing policy restrictions on foreign owned online retailers; compliance has so far been sketchy. India do not allow majority foreign ownership in multi brand retail stores and online retailers are allowed to operate only as ‘Marketplaces’ and not as B2C entities. With national elections due in next few months, the Government cannot ignore demands from domestic lobby groups to reign in free play by deep pocketed foreign operators that have been hurting local retailers.

In the detailed note below, we present (1) an overview of the regulatory framework and restrictions under which online retailers operate in India (2) the updated policy and its impact on operating models of Amazon and Walmart in India (3) expectations for India’s e-commerce players. Also, there is a likely gainer from all these – a listed Indian player aspiring to trump global majors in India’s online retail turf.

The founding team comes mostly from Tencent, which might explain Tencent’s large stake in the company. Growth for the company has been stupendous despite the jittery markets, with margin financing adding to the top-line growth.

While its low costs will help it to steal clients from the more traditional brokers, other new low-cost brokers seem to be offering similar services at comparable rates. In addition, the company is not licensed or regulated by any entities in China, despite the majority of its client base being Chinese nationals. Furthermore, the company plans to expand into newer overseas market where it doesn’t seem to have much of a cost advantage.

Tencent Music Entertainment (TME US)‘s social entertainment services (discretionary consumption in nature) face more headwinds due to ongoing China (macro) consumption slowdown.

Moreover, high consensus earnings expectation would make material earnings downgrade a major narrative for TME throughout 2019, in our opinion.

We initiative coverage on TME with Short/Sell recommendation, with 12-mo PT of US$9.80/ADR (representing a 25% downside potential).

After gaining 22.5% over seven trading days back in mid-September, Pci Ltd (PCI SP)responded to an SGX query over this price action that “it has been approached by a third party in connection with a potential transaction in relation to the securities of the Company. The discussions are on-going …“.

All was revealed on 4th January 2019, when PCI announced that Pagani Holding (a SPV indirectly owned by Platinum Equity Advisors) had made a S$1.33/share cash offer for the company by way of a scheme.

Chuan Hup Holdings (CH SP), which holds 76.7% in PCI, has given an irrevocable undertaking to vote its stake in favour of the scheme resolution, and to reject or vote against any competing offers. PCI’s executive chairman, Peh Kwee Chim, is Chuan Hup’s majority owner.

The price presents a ~18% premium to the last close, but a 49% premium to the “undisturbed” price back in early September and a 60% premium over the 12-month VWAP. The Offer values PCI at US$195mn.

With the 75%-for scheme condition satisfied and a lifetime-high takeover price, this is a done deal, and is duly reflected in the gross/annualised spread of 2.3%/6.8%, assuming mid-May completion.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.