Frasers Property Ltd (FPL SP)owns 40.95% in FPT and also 39.92% in GOLD. FPT’s director Panote Sirivadhanabhakdi (the son of Charoen Sirivadhanabhakdi), via his majority-controlled vehicleUniventures Public (UV TB), holds 39.28% in GOLD. Panote is also the vice-chairman of GOLD.

Presumably, both FPL and Univentures will tender into the Offer giving FPT a minimum holding of 80.2%. There were no specific minimum acceptance conditions attached to the tender offer mentioned in the announcement.

Should FPP secure 90% of GOLD in the tender offer, it may proceed with its delisting. A voluntary delisting is still achievable with ~80% in the bag, but that is conditional on <10% of shareholders not voting against.

Preconditions to the commencement of the tender offer include the approval from disinterested shareholders in FPP, approval from “relevant contractual parties of GOLD and GOLD’s subsidiaries” and the approval from the Office of Trade Competition Commission.

The fact the Sirivadhanabhakdi family already holds, directly/indirectly ~80% in GOLD, such regulatory approvals should be forthcoming.

This appears a done deal. The only apparent risk is the expected shareholder vote of Univentures wherein Panote will likely need to abstain.

Currently trading at a gross/annualized spread of 1.8%/4.3% assuming early August payment. Very tight, suggesting investors are more likely angling for the back-end.

This week’s offering of Insights across ASEAN@Smartkarmais filled with another eclectic mix of differentiated, substantive and actionable insights from across South East Asia and includes macro, top-down and thematic pieces, as well as actionable equity bottom-up pieces. Please find a brief summary below, with a fuller write up in the detailed section.

Highlights this week include the first individual company report in a Smartkarma Originals series on Indonesian Property from CrossASEAN Insight ProviderJessica Irene on Ciputra Development (CTRA IJ) and the potential for a strong data-driven turnaround over the coming few quarters for Xl Axiata (EXCL IJ) in an Insight from our friends at New Street Research. On the Macro front CrossASEAN economist Prasenjit K. Basu presents some insightful thoughts on the Singapore Economy.

Asian currencies are, in general, well supported by economic fundamentals in the form of external surpluses and interest rate differentials. Indeed, most Asian currencies display an appreciating bias, contrary to perceptions in 2018 when all of them lost ground to the US dollar. Over the last year the underlying external strength has been reflected in Asian currency appreciation against the US dollar.

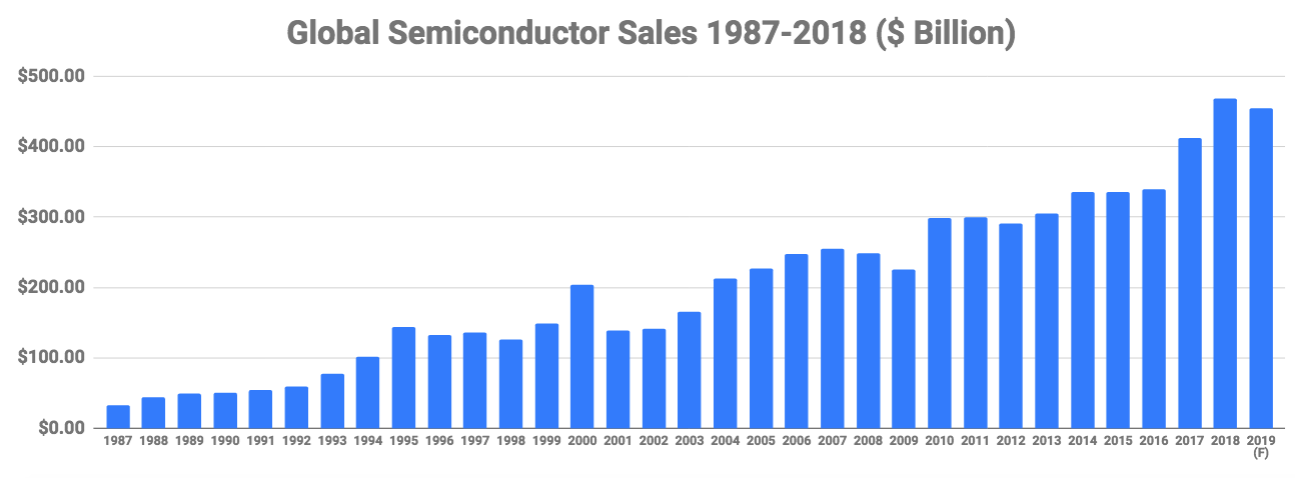

According to SEMI, North American (NA) WFE sales for January 2019 fell to $1.9 billion, down ~10% sequentially and ~20% YoY. This was an abrupt reversal of the recovery trend implied by the December 2018 sales of $2.1 billion and is the biggest monthly sales YoY decline since June 2013.

Just as declining monthly WFE sales preceded the current semiconductor downturn by some six months, the continuation of December’s MoM WFE decline reversal trend was a prerequisite for a second half recovery in the broader semiconductor sector. With that trend well and truly broken, we now anticipate a more delayed, gradual and prolonged recovery, one which is now unlikely to materialise until late third, early fourth quarter 2019.

US private LNG company Venture Global is starting construction on its 10 million ton per annum (mtpa) US LNG export facility in Louisiana after gaining approval from the US Federal Energy Regulatory Commission (FERC). This is positive for the LNG contractor market and we discuss the companies involved in the project.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

This week’s offering of Insights across ASEAN@Smartkarmais filled with another eclectic mix of differentiated, substantive and actionable insights from across South East Asia and includes macro, top-down and thematic pieces, as well as actionable equity bottom-up pieces. Please find a brief summary below, with a fuller write up in the detailed section.

Highlights this week include the first individual company report in a Smartkarma Originals series on Indonesian Property from CrossASEAN Insight ProviderJessica Irene on Ciputra Development (CTRA IJ) and the potential for a strong data-driven turnaround over the coming few quarters for Xl Axiata (EXCL IJ) in an Insight from our friends at New Street Research. On the Macro front CrossASEAN economist Prasenjit K. Basu presents some insightful thoughts on the Singapore Economy.

Asian currencies are, in general, well supported by economic fundamentals in the form of external surpluses and interest rate differentials. Indeed, most Asian currencies display an appreciating bias, contrary to perceptions in 2018 when all of them lost ground to the US dollar. Over the last year the underlying external strength has been reflected in Asian currency appreciation against the US dollar.

According to SEMI, North American (NA) WFE sales for January 2019 fell to $1.9 billion, down ~10% sequentially and ~20% YoY. This was an abrupt reversal of the recovery trend implied by the December 2018 sales of $2.1 billion and is the biggest monthly sales YoY decline since June 2013.

Just as declining monthly WFE sales preceded the current semiconductor downturn by some six months, the continuation of December’s MoM WFE decline reversal trend was a prerequisite for a second half recovery in the broader semiconductor sector. With that trend well and truly broken, we now anticipate a more delayed, gradual and prolonged recovery, one which is now unlikely to materialise until late third, early fourth quarter 2019.

US private LNG company Venture Global is starting construction on its 10 million ton per annum (mtpa) US LNG export facility in Louisiana after gaining approval from the US Federal Energy Regulatory Commission (FERC). This is positive for the LNG contractor market and we discuss the companies involved in the project.

Headwinds linger, but are beginning to lose velocity as consumers defy macro fears.

VIP slowdown should peak by Q3 and begin northward creep as bankrolls replenish.

Valuations today do not yet fully reflect the beginnings of a sector recovery.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Asian currencies are, in general, well supported by economic fundamentals in the form of external surpluses and interest rate differentials. Indeed, most Asian currencies display an appreciating bias, contrary to perceptions in 2018 when all of them lost ground to the US dollar. Over the last year the underlying external strength has been reflected in Asian currency appreciation against the US dollar.

According to SEMI, North American (NA) WFE sales for January 2019 fell to $1.9 billion, down ~10% sequentially and ~20% YoY. This was an abrupt reversal of the recovery trend implied by the December 2018 sales of $2.1 billion and is the biggest monthly sales YoY decline since June 2013.

Just as declining monthly WFE sales preceded the current semiconductor downturn by some six months, the continuation of December’s MoM WFE decline reversal trend was a prerequisite for a second half recovery in the broader semiconductor sector. With that trend well and truly broken, we now anticipate a more delayed, gradual and prolonged recovery, one which is now unlikely to materialise until late third, early fourth quarter 2019.

US private LNG company Venture Global is starting construction on its 10 million ton per annum (mtpa) US LNG export facility in Louisiana after gaining approval from the US Federal Energy Regulatory Commission (FERC). This is positive for the LNG contractor market and we discuss the companies involved in the project.

An activist has come forward, and the external statutory auditor and lead shareholder (wife of founder) are against the offer, but Kosaido Co Ltd (7868 JP) situation still fits pretty cleanly in the “Too Hard” bucket for now.

Since announcing its foray into the deeper waters of being the fourth Type I Mobile Network Operator in Japan, Rakuten’s shares have taken a mighty hit. But the focus in this insight is on ride-sharing company Lyft. In March 2015, Rakuten CEO Hiroshi Mikitani announced that Rakuten had invested US$300mn in Lyft, giving it a 11.9% stake after Series E round in May 2015. Recent articles suggest that Rakuten remains the top investor.

As best as Travis Lundy can tell, from sources who track this, Rakuten is the single largest shareholder in Lyft, with a holding in the 10.4-12.0% range. That would suggest a position value of US$900mn-$1.2bn based on the last funding round in June 2018. At a $25bn pre-money IPO valuation, that would be worth US$1.5-2.0bn for a likely pre-tax IPO uplift of US$590-800mn.

A report late Thursday Asia time suggested the Lyft roadshow would start the week of March 18th, which would mean the S-1 will be available two weeks before that. Investors will know more about Rakuten’s ownership of Lyft by the end of next week or very early the following week. Travis would want to be long for now.

DHICO announced a larger-than-expected ₩608.4bn rights offer. ₩543bn is expected to be raised through common shares at a preliminary price of ₩6,390; and ₩65bn via RCPS at a preliminary price of ₩6,970. This is a combined 72.56% capital increase a 42.05% share dilution. Concurrently, Doosan E&C announced a ₩420bn rights offer at a preliminary price of ₩1,255, a 15% discount to last close.

For DHICO, Mar 27 is the ex-rights day for both Common and RCPS. Subscription rights (for the Common) will be listed and trade on Apr 19~25. May 2 is final pricing. May 8 is subscription and May 16 is payment. New Common shares will be listed on May 29.

For E&C, the final price will be fixed on Apr 30. Whichever is higher – ₩1,255 or Apr 26~30 VWAP at a 40% discount – will be the final offering price. Mar 27 will be the ex-rights day. Subscription rights will be listed and traded on Apr 18~24. New shares will be listed on May 24.

₩1,255 is a lot more aggressive than generally viewed. DHICO owns nearly two thirds of E&C. With a 20% oversubscription, nearly ₩300bn will likely come from DHICO, essentially buttressing E&C at an even heftier price. Which is probably why the market is being less harsh on E&C relative to DHICO.

The 247-4 Form is out with a tender offer period between 26 Feb-1 April, and payment on the 4th April. The frustrating part is how Delta’s FY18 dividend of Bt2.30 is treated. On one hand, it says the Bt71 Offer price is final unless there is a MAC. Further into the Offer doc, it mentions the Offeror “reserves the right” to reduce the offer price if a dividend is paid. DELTA’s IR believes the dividend will be added, but it is not crystal clear.

Furthermore, there is no minimum acceptance condition, as potentially flagged earlier, which means there is no possibility of fast-tracking payment. Some precedent voluntary offers included a minimum acceptance, which provides an expedited payment should investors who tender shares AND revoke their right to withdraw – provided that minimum is fulfilled.

Shares traded up after the document came out, shrugging off the ambiguity in the document. Currently trading at a gross/annualised return of 1.1%/11%. The dividend is subject to a 10% tax for non-residents.

The previous Friday, the Offerors for M1 announced that their Offer had been declared Unconditional In All Respects as the tendered amount was 57.04% and the total held by concert parties was 76.35%. Axiata Group (AXIATA MK)made an announcement to the Bursa Malaysia that it had accepted the Offer as required because it was a significant asset disposal. Going unconditional has triggered an extension of the Closing Date to 4 March 2019.

If you want to fight this with an appraisal, you can. Travis doesn’t see the point. If you want to hold on to the stock in order to block full squeezeout and play chicken with the big boys, you can, but it requires a relatively big ticket (roughly 6.73% of the shares out).

So Travis recommends taking the money. It was better to take the money in early January and re-deploy, rather than wait for the close of the offer. He would accept now and sees no upside from waiting.

When the Tender Offer / MBO for Kosaido was announced last month, Travis’ first reaction was that this was wrong, concluding this was a virtual asset strip in progress, and suggested that the only way this was likely to not get done is if some brave activist came forward.

Shortly afterwards, an activist did come forward. Yoshiaki Murakami’s bought 5% through his entity Reno KK, and later lifted his stake (combined with affiliates) to 9.55%. Travis thought the stock had run too far at that point (¥775/share). While still cheap, he did not expect Bain to lift its price by 30+%, nor a white knight to arrive quickly enough.

This week a media article suggested longstanding external statutory auditor Mr. Nakatsuji and lead shareholder Sakurai Mie were against the takeover.

The possibility this deal fails because the “put protection” of the deal price at ¥610 is no longer solid has gone up. Conversely, the probability that Bain and the MBO have to come in with a price adjustment higher has gone up. Travis is inclined to remain bearish in the medium-term as there is a significant likelihood there is no alternative solution during the Tender Offer period itself.

After announcing earlier this month a number of indicative non-binding bids were received for a “whole of company transaction”, the AFR is now reporting (paywalled) that Lone Star has also joined the battle for Aveo Group (AOG AU). (A Case for Privatising Aveo)

Saputo Inc (SAP CN) and Dairy Crest announced an all-cash deal where Saputo will buy Dairy Crest for 620p/share, to be implemented through a Scheme of Arrangement with an expected close in Q2 2019. This appears to tick all the necessary boxes. Friendly, horizontal integration, and limited job losses. Shares are trading through terms early (he published at 628.5p), perhaps on expectations the wide open register means shareholders can try to hold out for a higher price.

At almost 14x EV/EBITDA on a TTM basis and a bit lower on a March 2019 FY-end basis, it is a high enough multiple to not be insulting for a dairy company, and may keep other suitors away.

Dairy Crest’s directors have given irrevocable notice to accept, and the directors’ advisors (Greenhill & Co) have deemed the Offer “fair and reasonable.”

One extra turn of EV/EBITDA would lift the takeover price just under 10%. That would clear out most of the naysayers who bought in the frothier “we’re going to be an asset-light branded goods company” days of 2015-2017. Doable, but as it is an agreed deal, Travis doesn’t see the need to push it.

In its prior letter to Ophir on the 14 January, Petrus recommended selling the South-East Asian (SEA) assets to Medco, with a low-end fair value, before synergies, of £0.64/share, through to £1.42/share on a blue sky basis. It also argued that Ophir should negotiate with the Equatorial Guinea ministry (the regulator that terminated the Fortuna license, resulting in write-offs of US$610mn) to be compensated for its $700mn investment and the unfair seizure of the license, otherwise it would set a precedent for other international operators doing business in EG.

Petrus has now rounded on Schrader over perceived mismanagement of the EG licence, and a lack of professionalism in not soliciting and considering offers for Ophir from other buyers. Petrus’ beef is not an outlier – alternative hedge fund Sand Grove has increased its exposure, via cash-settled derivatives, to 17.28% (as at 13 February); while Ian Hannam, who advised Ophir’s board on its 2013 right issue, is understood to have also written to Ophir’s interim CEO Alan Booth and the board saying Medco’s offer is too low.

Overall, Petrus’ assertions that Ophir is being sold at “sub optimal terms” appear valid, most notably on the EG compensation and the illogical operations update earlier this month. The alternative push to sell the SEA assets separately, as that has been Medco’s core focus, not international operations, also makes sense.

Last month, DSV A/S (DSV DC) made a public proposal of a takeover for cash and scrip valued at CHF 170/share, which came at a 24% premium to last and +31% vs 1-month VWAP. The #2, #3, and long-time #4 shareholders are firmly and publicly in the camp of trying to get something done. 45.9%-shareholder Ernst Göhner Foundation is sending mixed signals – do they want a higher price? Or do they want to wait and let Panalpina grow by its own consolidator strategy?

Panalpina has now confirmed that it in preliminary talks with Kuwait-listed logistics company Agility Public Warehouse. A Bloomberg report suggested a deal could be reached as early as this past week for Agility’s logistics business. The same article suggested the Göhner Foundation is supportive of the new talks. Agility’s press release was much more non-committal.

DSV has also announced a new all cash CHF 180/share offer for Panalpina; although the original cash and scrip offer was then worth CHF 184.5/share, which is an even better premium to pre-offer terms. One wonders whether cash-only would suit the Foundation; the DSV press release seemed to respond to that.

It is not clear what would drive the Foundation to give up its control. And Panalpina’s measly share price reaction to the all-cash offer suggest there is considerable skepticism out there. But at some price, Panalpina’s board looks pretty stupid to not accept the cash.

If you do not think a deal with DSV has any chance of getting up, Panalpina shares are a sell here. If they overpay for Agility and cannot improve their own margins well past historical highs in a market trending weaker, then the shares could drop.

Using Curtis’ figures, the implied stub is at its lowest level since a brief downward spike in February 2015, and you would have to go back to April 2014 to find a lower level.

The push back on this setup is that the auto operations have recorded marginally, yet sequential profit declines in FY16 and FY17; while recording three sequential quarterly declines up to December 2018. The big question is whether Mahindra can regain market share as it kick-starts a new model cycle.

In contrast, Sanghyun believes the Holdco is still undervalued relative to the Sub by about 10%. Plugging in Sanghyun’s numbers, I back out a discount to NAV of 45% against a one-year average of 30%, with a 12-month range of -51.5% to 15.5% (premium).

Back on the 13 December 2018, Can One announced a proposed MGO for Kian Joo at RM3.10/share, a 52.7% premium to last close. This required Can One shareholders’ approval which was received on the 14 February. Can One’s current 33% stake in Kian Joo accounts for ~86% of its market cap. The offer doc should be out, on or before the 7 March, with payment either late March (along with the first close of the Offer), or early April, depending on when the offer turns unconditional. The offer is conditional on 50% acceptance. Both sides are illiquid.

This looks like a decent exit for Kian Joo shareholders. Apart from EPF with 10.1%, former NED Teow China See is the only other shareholder with >5% with 8.9%.

For Can One, this is an aggressive pitch to make Kian Joo a subsidiary amidst an uncertain economic backdrop, while potential synergies may be offset via higher interest costs.

There are still two schools of thought on the HMG restructuring. One is that Glovis/Mobis are merged into a holdco entity. Or Glovis becomes the holdco with Mobis→ HM→ Kia Motors Corp (000270 KS) below. Since late 3Q18, there has been increased speculation on the latter. This has pushed up Glovis’ price relative to Mobis.

Each outcome is beset with its own set of issues. For Glovis to be the sole holdco, it has to come up with nearly ₩2tn to buy Kia’s Mobis stake, probably through new, and burdensome, debt. Glovis may also face the risk of forced holdco conversion, creating an issue with Kia as a “great grandson” subsidiary.

This speculation pushing up Glovis relative to Mobis has yet to be substantiated/justified, suggesting Glovis is overbought. Sanghyun expects a mean reversion, and recommends a long Mobis and short Glovis.

Navitas Ltd (NVT AU) has agreed to extend the exclusivity period granted to the BGH consortium to 1 March (from 18 Feb), in order to allow additional time for BGH to complete a limited set of remaining due diligence investigations.

Netcomm Wireless (NTC AU) has received $1.10 cash offer (53% premium to last close) from Casa Systems (CASA US) via a Scheme. The deal values Netcomm at ~US$114m. The scheme is subject to FIRB and shareholder approval. Stewart David Paul James, a NED, holds 12.3% and is the major shareholder. The announcement states that each Netcomm director intends to vote the Netcomm shares held by them in favour of the scheme – subject to a +ve IFA opinion and in the absence of a competing offer. This includes Stewart’s stake.

MYOB Group Ltd (MYO AU)announced no superior proposal emerged after concluding its ’go shop’ period for rival offers to KKR’s takeover proposal. At a gross/annualised spread of 0.9%/4.8%, assuming early May payment, this looks to be trading a bit tight.

CCASS

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Issuance of the new shares and common stock to be delisted from the Tokyo Stock Exchange

C

Japan

Descente

Off-Mkt

14-Mar

Tender Offer Close Date

C

Japan

JIEC

Off-Mkt

18-Mar

Tender Offer Close Date

C

Japan

Veriserve

Off-Mkt

18-Mar

Tender Offer Close Date

C

Japan

ND Software

Off-Mkt

25-Mar

Tender Offer Close Date

C

Japan

Showa Shell

Scheme

1-Apr

Close of merger

E

Japan

U-Shin

Off-Market

17-Apr

Tender Offer Close Date

C

NZ

Trade Me Group

Scheme

5-Mar

First Court Date

C

Singapore

Courts Asia Limited

Scheme

15-Mar

Offer Close Date

C

Singapore

M1 Limited

Off Mkt

4-Mar

Closing date of offer

C

Singapore

PCI Limited

Scheme

February

Release of Scheme Booklet

E

Taiwan

Yungtay Engineering

Off Mkt

17-Mar

Closing date of offer

C

Thailand

Delta Electronics

Off Mkt

26-Feb

Tender Offer Open

C

Finland

Amer Sports

Off Mkt

7-Mar

Offer Period Expires

C

Norway

Oslo Børs VPS

Off Mkt

4-Mar

Nasdaq Offer Close Date

C

Switzerland

Panalpina Welttransport

Off Mkt

27-Feb

Binding offer to be announced

E

US

Red Hat, Inc.

Scheme

March/April

Deal lodged for approval with EU Regulators

C

Source: Company announcements. E = our estimates; C =confirmed

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

According to SEMI, North American (NA) WFE sales for January 2019 fell to $1.9 billion, down ~10% sequentially and ~20% YoY. This was an abrupt reversal of the recovery trend implied by the December 2018 sales of $2.1 billion and is the biggest monthly sales YoY decline since June 2013.

Just as declining monthly WFE sales preceded the current semiconductor downturn by some six months, the continuation of December’s MoM WFE decline reversal trend was a prerequisite for a second half recovery in the broader semiconductor sector. With that trend well and truly broken, we now anticipate a more delayed, gradual and prolonged recovery, one which is now unlikely to materialise until late third, early fourth quarter 2019.

US private LNG company Venture Global is starting construction on its 10 million ton per annum (mtpa) US LNG export facility in Louisiana after gaining approval from the US Federal Energy Regulatory Commission (FERC). This is positive for the LNG contractor market and we discuss the companies involved in the project.

An activist has come forward, and the external statutory auditor and lead shareholder (wife of founder) are against the offer, but Kosaido Co Ltd (7868 JP) situation still fits pretty cleanly in the “Too Hard” bucket for now.

Since announcing its foray into the deeper waters of being the fourth Type I Mobile Network Operator in Japan, Rakuten’s shares have taken a mighty hit. But the focus in this insight is on ride-sharing company Lyft. In March 2015, Rakuten CEO Hiroshi Mikitani announced that Rakuten had invested US$300mn in Lyft, giving it a 11.9% stake after Series E round in May 2015. Recent articles suggest that Rakuten remains the top investor.

As best as Travis Lundy can tell, from sources who track this, Rakuten is the single largest shareholder in Lyft, with a holding in the 10.4-12.0% range. That would suggest a position value of US$900mn-$1.2bn based on the last funding round in June 2018. At a $25bn pre-money IPO valuation, that would be worth US$1.5-2.0bn for a likely pre-tax IPO uplift of US$590-800mn.

A report late Thursday Asia time suggested the Lyft roadshow would start the week of March 18th, which would mean the S-1 will be available two weeks before that. Investors will know more about Rakuten’s ownership of Lyft by the end of next week or very early the following week. Travis would want to be long for now.

DHICO announced a larger-than-expected ₩608.4bn rights offer. ₩543bn is expected to be raised through common shares at a preliminary price of ₩6,390; and ₩65bn via RCPS at a preliminary price of ₩6,970. This is a combined 72.56% capital increase a 42.05% share dilution. Concurrently, Doosan E&C announced a ₩420bn rights offer at a preliminary price of ₩1,255, a 15% discount to last close.

For DHICO, Mar 27 is the ex-rights day for both Common and RCPS. Subscription rights (for the Common) will be listed and trade on Apr 19~25. May 2 is final pricing. May 8 is subscription and May 16 is payment. New Common shares will be listed on May 29.

For E&C, the final price will be fixed on Apr 30. Whichever is higher – ₩1,255 or Apr 26~30 VWAP at a 40% discount – will be the final offering price. Mar 27 will be the ex-rights day. Subscription rights will be listed and traded on Apr 18~24. New shares will be listed on May 24.

₩1,255 is a lot more aggressive than generally viewed. DHICO owns nearly two thirds of E&C. With a 20% oversubscription, nearly ₩300bn will likely come from DHICO, essentially buttressing E&C at an even heftier price. Which is probably why the market is being less harsh on E&C relative to DHICO.

The 247-4 Form is out with a tender offer period between 26 Feb-1 April, and payment on the 4th April. The frustrating part is how Delta’s FY18 dividend of Bt2.30 is treated. On one hand, it says the Bt71 Offer price is final unless there is a MAC. Further into the Offer doc, it mentions the Offeror “reserves the right” to reduce the offer price if a dividend is paid. DELTA’s IR believes the dividend will be added, but it is not crystal clear.

Furthermore, there is no minimum acceptance condition, as potentially flagged earlier, which means there is no possibility of fast-tracking payment. Some precedent voluntary offers included a minimum acceptance, which provides an expedited payment should investors who tender shares AND revoke their right to withdraw – provided that minimum is fulfilled.

Shares traded up after the document came out, shrugging off the ambiguity in the document. Currently trading at a gross/annualised return of 1.1%/11%. The dividend is subject to a 10% tax for non-residents.

The previous Friday, the Offerors for M1 announced that their Offer had been declared Unconditional In All Respects as the tendered amount was 57.04% and the total held by concert parties was 76.35%. Axiata Group (AXIATA MK)made an announcement to the Bursa Malaysia that it had accepted the Offer as required because it was a significant asset disposal. Going unconditional has triggered an extension of the Closing Date to 4 March 2019.

If you want to fight this with an appraisal, you can. Travis doesn’t see the point. If you want to hold on to the stock in order to block full squeezeout and play chicken with the big boys, you can, but it requires a relatively big ticket (roughly 6.73% of the shares out).

So Travis recommends taking the money. It was better to take the money in early January and re-deploy, rather than wait for the close of the offer. He would accept now and sees no upside from waiting.

When the Tender Offer / MBO for Kosaido was announced last month, Travis’ first reaction was that this was wrong, concluding this was a virtual asset strip in progress, and suggested that the only way this was likely to not get done is if some brave activist came forward.

Shortly afterwards, an activist did come forward. Yoshiaki Murakami’s bought 5% through his entity Reno KK, and later lifted his stake (combined with affiliates) to 9.55%. Travis thought the stock had run too far at that point (¥775/share). While still cheap, he did not expect Bain to lift its price by 30+%, nor a white knight to arrive quickly enough.

This week a media article suggested longstanding external statutory auditor Mr. Nakatsuji and lead shareholder Sakurai Mie were against the takeover.

The possibility this deal fails because the “put protection” of the deal price at ¥610 is no longer solid has gone up. Conversely, the probability that Bain and the MBO have to come in with a price adjustment higher has gone up. Travis is inclined to remain bearish in the medium-term as there is a significant likelihood there is no alternative solution during the Tender Offer period itself.

After announcing earlier this month a number of indicative non-binding bids were received for a “whole of company transaction”, the AFR is now reporting (paywalled) that Lone Star has also joined the battle for Aveo Group (AOG AU). (A Case for Privatising Aveo)

Saputo Inc (SAP CN) and Dairy Crest announced an all-cash deal where Saputo will buy Dairy Crest for 620p/share, to be implemented through a Scheme of Arrangement with an expected close in Q2 2019. This appears to tick all the necessary boxes. Friendly, horizontal integration, and limited job losses. Shares are trading through terms early (he published at 628.5p), perhaps on expectations the wide open register means shareholders can try to hold out for a higher price.

At almost 14x EV/EBITDA on a TTM basis and a bit lower on a March 2019 FY-end basis, it is a high enough multiple to not be insulting for a dairy company, and may keep other suitors away.

Dairy Crest’s directors have given irrevocable notice to accept, and the directors’ advisors (Greenhill & Co) have deemed the Offer “fair and reasonable.”

One extra turn of EV/EBITDA would lift the takeover price just under 10%. That would clear out most of the naysayers who bought in the frothier “we’re going to be an asset-light branded goods company” days of 2015-2017. Doable, but as it is an agreed deal, Travis doesn’t see the need to push it.

In its prior letter to Ophir on the 14 January, Petrus recommended selling the South-East Asian (SEA) assets to Medco, with a low-end fair value, before synergies, of £0.64/share, through to £1.42/share on a blue sky basis. It also argued that Ophir should negotiate with the Equatorial Guinea ministry (the regulator that terminated the Fortuna license, resulting in write-offs of US$610mn) to be compensated for its $700mn investment and the unfair seizure of the license, otherwise it would set a precedent for other international operators doing business in EG.

Petrus has now rounded on Schrader over perceived mismanagement of the EG licence, and a lack of professionalism in not soliciting and considering offers for Ophir from other buyers. Petrus’ beef is not an outlier – alternative hedge fund Sand Grove has increased its exposure, via cash-settled derivatives, to 17.28% (as at 13 February); while Ian Hannam, who advised Ophir’s board on its 2013 right issue, is understood to have also written to Ophir’s interim CEO Alan Booth and the board saying Medco’s offer is too low.

Overall, Petrus’ assertions that Ophir is being sold at “sub optimal terms” appear valid, most notably on the EG compensation and the illogical operations update earlier this month. The alternative push to sell the SEA assets separately, as that has been Medco’s core focus, not international operations, also makes sense.

Last month, DSV A/S (DSV DC) made a public proposal of a takeover for cash and scrip valued at CHF 170/share, which came at a 24% premium to last and +31% vs 1-month VWAP. The #2, #3, and long-time #4 shareholders are firmly and publicly in the camp of trying to get something done. 45.9%-shareholder Ernst Göhner Foundation is sending mixed signals – do they want a higher price? Or do they want to wait and let Panalpina grow by its own consolidator strategy?

Panalpina has now confirmed that it in preliminary talks with Kuwait-listed logistics company Agility Public Warehouse. A Bloomberg report suggested a deal could be reached as early as this past week for Agility’s logistics business. The same article suggested the Göhner Foundation is supportive of the new talks. Agility’s press release was much more non-committal.

DSV has also announced a new all cash CHF 180/share offer for Panalpina; although the original cash and scrip offer was then worth CHF 184.5/share, which is an even better premium to pre-offer terms. One wonders whether cash-only would suit the Foundation; the DSV press release seemed to respond to that.

It is not clear what would drive the Foundation to give up its control. And Panalpina’s measly share price reaction to the all-cash offer suggest there is considerable skepticism out there. But at some price, Panalpina’s board looks pretty stupid to not accept the cash.

If you do not think a deal with DSV has any chance of getting up, Panalpina shares are a sell here. If they overpay for Agility and cannot improve their own margins well past historical highs in a market trending weaker, then the shares could drop.

Using Curtis’ figures, the implied stub is at its lowest level since a brief downward spike in February 2015, and you would have to go back to April 2014 to find a lower level.

The push back on this setup is that the auto operations have recorded marginally, yet sequential profit declines in FY16 and FY17; while recording three sequential quarterly declines up to December 2018. The big question is whether Mahindra can regain market share as it kick-starts a new model cycle.

In contrast, Sanghyun believes the Holdco is still undervalued relative to the Sub by about 10%. Plugging in Sanghyun’s numbers, I back out a discount to NAV of 45% against a one-year average of 30%, with a 12-month range of -51.5% to 15.5% (premium).

Back on the 13 December 2018, Can One announced a proposed MGO for Kian Joo at RM3.10/share, a 52.7% premium to last close. This required Can One shareholders’ approval which was received on the 14 February. Can One’s current 33% stake in Kian Joo accounts for ~86% of its market cap. The offer doc should be out, on or before the 7 March, with payment either late March (along with the first close of the Offer), or early April, depending on when the offer turns unconditional. The offer is conditional on 50% acceptance. Both sides are illiquid.

This looks like a decent exit for Kian Joo shareholders. Apart from EPF with 10.1%, former NED Teow China See is the only other shareholder with >5% with 8.9%.

For Can One, this is an aggressive pitch to make Kian Joo a subsidiary amidst an uncertain economic backdrop, while potential synergies may be offset via higher interest costs.

There are still two schools of thought on the HMG restructuring. One is that Glovis/Mobis are merged into a holdco entity. Or Glovis becomes the holdco with Mobis→ HM→ Kia Motors Corp (000270 KS) below. Since late 3Q18, there has been increased speculation on the latter. This has pushed up Glovis’ price relative to Mobis.

Each outcome is beset with its own set of issues. For Glovis to be the sole holdco, it has to come up with nearly ₩2tn to buy Kia’s Mobis stake, probably through new, and burdensome, debt. Glovis may also face the risk of forced holdco conversion, creating an issue with Kia as a “great grandson” subsidiary.

This speculation pushing up Glovis relative to Mobis has yet to be substantiated/justified, suggesting Glovis is overbought. Sanghyun expects a mean reversion, and recommends a long Mobis and short Glovis.

Navitas Ltd (NVT AU) has agreed to extend the exclusivity period granted to the BGH consortium to 1 March (from 18 Feb), in order to allow additional time for BGH to complete a limited set of remaining due diligence investigations.

Netcomm Wireless (NTC AU) has received $1.10 cash offer (53% premium to last close) from Casa Systems (CASA US) via a Scheme. The deal values Netcomm at ~US$114m. The scheme is subject to FIRB and shareholder approval. Stewart David Paul James, a NED, holds 12.3% and is the major shareholder. The announcement states that each Netcomm director intends to vote the Netcomm shares held by them in favour of the scheme – subject to a +ve IFA opinion and in the absence of a competing offer. This includes Stewart’s stake.

MYOB Group Ltd (MYO AU)announced no superior proposal emerged after concluding its ’go shop’ period for rival offers to KKR’s takeover proposal. At a gross/annualised spread of 0.9%/4.8%, assuming early May payment, this looks to be trading a bit tight.

CCASS

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

NextDecade Corp (NEXT US) recently announced that it started offering long-term contracts indexed to the crude Brent in order to attract more LNG buyers. This follows the agreement reached by Tellurian Inc (TELL US) with Vitol back in December to index a long term contract with the Asian LNG price benchmark JKM. While typically US LNG projects are indexed to the Henry Hub, declining crude oil and LNG prices seem to have diminished the appeal of the Henry Hub pricing compared to the oil indexation. This insight takes a look at the latest trends in the LNG markets to assess which companies are taking the lead in the race to bring to FID in 2019 their proposed LNG projects.

Exhibit 1: NextDecade adds Brent indexation to its commercial offering

Source: NextDecade Corporate Presentation February 2019

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

US private LNG company Venture Global is starting construction on its 10 million ton per annum (mtpa) US LNG export facility in Louisiana after gaining approval from the US Federal Energy Regulatory Commission (FERC). This is positive for the LNG contractor market and we discuss the companies involved in the project.

An activist has come forward, and the external statutory auditor and lead shareholder (wife of founder) are against the offer, but Kosaido Co Ltd (7868 JP) situation still fits pretty cleanly in the “Too Hard” bucket for now.

Since announcing its foray into the deeper waters of being the fourth Type I Mobile Network Operator in Japan, Rakuten’s shares have taken a mighty hit. But the focus in this insight is on ride-sharing company Lyft. In March 2015, Rakuten CEO Hiroshi Mikitani announced that Rakuten had invested US$300mn in Lyft, giving it a 11.9% stake after Series E round in May 2015. Recent articles suggest that Rakuten remains the top investor.

As best as Travis Lundy can tell, from sources who track this, Rakuten is the single largest shareholder in Lyft, with a holding in the 10.4-12.0% range. That would suggest a position value of US$900mn-$1.2bn based on the last funding round in June 2018. At a $25bn pre-money IPO valuation, that would be worth US$1.5-2.0bn for a likely pre-tax IPO uplift of US$590-800mn.

A report late Thursday Asia time suggested the Lyft roadshow would start the week of March 18th, which would mean the S-1 will be available two weeks before that. Investors will know more about Rakuten’s ownership of Lyft by the end of next week or very early the following week. Travis would want to be long for now.

DHICO announced a larger-than-expected ₩608.4bn rights offer. ₩543bn is expected to be raised through common shares at a preliminary price of ₩6,390; and ₩65bn via RCPS at a preliminary price of ₩6,970. This is a combined 72.56% capital increase a 42.05% share dilution. Concurrently, Doosan E&C announced a ₩420bn rights offer at a preliminary price of ₩1,255, a 15% discount to last close.

For DHICO, Mar 27 is the ex-rights day for both Common and RCPS. Subscription rights (for the Common) will be listed and trade on Apr 19~25. May 2 is final pricing. May 8 is subscription and May 16 is payment. New Common shares will be listed on May 29.

For E&C, the final price will be fixed on Apr 30. Whichever is higher – ₩1,255 or Apr 26~30 VWAP at a 40% discount – will be the final offering price. Mar 27 will be the ex-rights day. Subscription rights will be listed and traded on Apr 18~24. New shares will be listed on May 24.

₩1,255 is a lot more aggressive than generally viewed. DHICO owns nearly two thirds of E&C. With a 20% oversubscription, nearly ₩300bn will likely come from DHICO, essentially buttressing E&C at an even heftier price. Which is probably why the market is being less harsh on E&C relative to DHICO.

The 247-4 Form is out with a tender offer period between 26 Feb-1 April, and payment on the 4th April. The frustrating part is how Delta’s FY18 dividend of Bt2.30 is treated. On one hand, it says the Bt71 Offer price is final unless there is a MAC. Further into the Offer doc, it mentions the Offeror “reserves the right” to reduce the offer price if a dividend is paid. DELTA’s IR believes the dividend will be added, but it is not crystal clear.

Furthermore, there is no minimum acceptance condition, as potentially flagged earlier, which means there is no possibility of fast-tracking payment. Some precedent voluntary offers included a minimum acceptance, which provides an expedited payment should investors who tender shares AND revoke their right to withdraw – provided that minimum is fulfilled.

Shares traded up after the document came out, shrugging off the ambiguity in the document. Currently trading at a gross/annualised return of 1.1%/11%. The dividend is subject to a 10% tax for non-residents.

The previous Friday, the Offerors for M1 announced that their Offer had been declared Unconditional In All Respects as the tendered amount was 57.04% and the total held by concert parties was 76.35%. Axiata Group (AXIATA MK)made an announcement to the Bursa Malaysia that it had accepted the Offer as required because it was a significant asset disposal. Going unconditional has triggered an extension of the Closing Date to 4 March 2019.

If you want to fight this with an appraisal, you can. Travis doesn’t see the point. If you want to hold on to the stock in order to block full squeezeout and play chicken with the big boys, you can, but it requires a relatively big ticket (roughly 6.73% of the shares out).

So Travis recommends taking the money. It was better to take the money in early January and re-deploy, rather than wait for the close of the offer. He would accept now and sees no upside from waiting.

When the Tender Offer / MBO for Kosaido was announced last month, Travis’ first reaction was that this was wrong, concluding this was a virtual asset strip in progress, and suggested that the only way this was likely to not get done is if some brave activist came forward.

Shortly afterwards, an activist did come forward. Yoshiaki Murakami’s bought 5% through his entity Reno KK, and later lifted his stake (combined with affiliates) to 9.55%. Travis thought the stock had run too far at that point (¥775/share). While still cheap, he did not expect Bain to lift its price by 30+%, nor a white knight to arrive quickly enough.

This week a media article suggested longstanding external statutory auditor Mr. Nakatsuji and lead shareholder Sakurai Mie were against the takeover.

The possibility this deal fails because the “put protection” of the deal price at ¥610 is no longer solid has gone up. Conversely, the probability that Bain and the MBO have to come in with a price adjustment higher has gone up. Travis is inclined to remain bearish in the medium-term as there is a significant likelihood there is no alternative solution during the Tender Offer period itself.

After announcing earlier this month a number of indicative non-binding bids were received for a “whole of company transaction”, the AFR is now reporting (paywalled) that Lone Star has also joined the battle for Aveo Group (AOG AU). (A Case for Privatising Aveo)

Saputo Inc (SAP CN) and Dairy Crest announced an all-cash deal where Saputo will buy Dairy Crest for 620p/share, to be implemented through a Scheme of Arrangement with an expected close in Q2 2019. This appears to tick all the necessary boxes. Friendly, horizontal integration, and limited job losses. Shares are trading through terms early (he published at 628.5p), perhaps on expectations the wide open register means shareholders can try to hold out for a higher price.

At almost 14x EV/EBITDA on a TTM basis and a bit lower on a March 2019 FY-end basis, it is a high enough multiple to not be insulting for a dairy company, and may keep other suitors away.

Dairy Crest’s directors have given irrevocable notice to accept, and the directors’ advisors (Greenhill & Co) have deemed the Offer “fair and reasonable.”

One extra turn of EV/EBITDA would lift the takeover price just under 10%. That would clear out most of the naysayers who bought in the frothier “we’re going to be an asset-light branded goods company” days of 2015-2017. Doable, but as it is an agreed deal, Travis doesn’t see the need to push it.

In its prior letter to Ophir on the 14 January, Petrus recommended selling the South-East Asian (SEA) assets to Medco, with a low-end fair value, before synergies, of £0.64/share, through to £1.42/share on a blue sky basis. It also argued that Ophir should negotiate with the Equatorial Guinea ministry (the regulator that terminated the Fortuna license, resulting in write-offs of US$610mn) to be compensated for its $700mn investment and the unfair seizure of the license, otherwise it would set a precedent for other international operators doing business in EG.

Petrus has now rounded on Schrader over perceived mismanagement of the EG licence, and a lack of professionalism in not soliciting and considering offers for Ophir from other buyers. Petrus’ beef is not an outlier – alternative hedge fund Sand Grove has increased its exposure, via cash-settled derivatives, to 17.28% (as at 13 February); while Ian Hannam, who advised Ophir’s board on its 2013 right issue, is understood to have also written to Ophir’s interim CEO Alan Booth and the board saying Medco’s offer is too low.

Overall, Petrus’ assertions that Ophir is being sold at “sub optimal terms” appear valid, most notably on the EG compensation and the illogical operations update earlier this month. The alternative push to sell the SEA assets separately, as that has been Medco’s core focus, not international operations, also makes sense.

Last month, DSV A/S (DSV DC) made a public proposal of a takeover for cash and scrip valued at CHF 170/share, which came at a 24% premium to last and +31% vs 1-month VWAP. The #2, #3, and long-time #4 shareholders are firmly and publicly in the camp of trying to get something done. 45.9%-shareholder Ernst Göhner Foundation is sending mixed signals – do they want a higher price? Or do they want to wait and let Panalpina grow by its own consolidator strategy?

Panalpina has now confirmed that it in preliminary talks with Kuwait-listed logistics company Agility Public Warehouse. A Bloomberg report suggested a deal could be reached as early as this past week for Agility’s logistics business. The same article suggested the Göhner Foundation is supportive of the new talks. Agility’s press release was much more non-committal.

DSV has also announced a new all cash CHF 180/share offer for Panalpina; although the original cash and scrip offer was then worth CHF 184.5/share, which is an even better premium to pre-offer terms. One wonders whether cash-only would suit the Foundation; the DSV press release seemed to respond to that.

It is not clear what would drive the Foundation to give up its control. And Panalpina’s measly share price reaction to the all-cash offer suggest there is considerable skepticism out there. But at some price, Panalpina’s board looks pretty stupid to not accept the cash.

If you do not think a deal with DSV has any chance of getting up, Panalpina shares are a sell here. If they overpay for Agility and cannot improve their own margins well past historical highs in a market trending weaker, then the shares could drop.

Using Curtis’ figures, the implied stub is at its lowest level since a brief downward spike in February 2015, and you would have to go back to April 2014 to find a lower level.

The push back on this setup is that the auto operations have recorded marginally, yet sequential profit declines in FY16 and FY17; while recording three sequential quarterly declines up to December 2018. The big question is whether Mahindra can regain market share as it kick-starts a new model cycle.

In contrast, Sanghyun believes the Holdco is still undervalued relative to the Sub by about 10%. Plugging in Sanghyun’s numbers, I back out a discount to NAV of 45% against a one-year average of 30%, with a 12-month range of -51.5% to 15.5% (premium).

Back on the 13 December 2018, Can One announced a proposed MGO for Kian Joo at RM3.10/share, a 52.7% premium to last close. This required Can One shareholders’ approval which was received on the 14 February. Can One’s current 33% stake in Kian Joo accounts for ~86% of its market cap. The offer doc should be out, on or before the 7 March, with payment either late March (along with the first close of the Offer), or early April, depending on when the offer turns unconditional. The offer is conditional on 50% acceptance. Both sides are illiquid.

This looks like a decent exit for Kian Joo shareholders. Apart from EPF with 10.1%, former NED Teow China See is the only other shareholder with >5% with 8.9%.

For Can One, this is an aggressive pitch to make Kian Joo a subsidiary amidst an uncertain economic backdrop, while potential synergies may be offset via higher interest costs.

There are still two schools of thought on the HMG restructuring. One is that Glovis/Mobis are merged into a holdco entity. Or Glovis becomes the holdco with Mobis→ HM→ Kia Motors Corp (000270 KS) below. Since late 3Q18, there has been increased speculation on the latter. This has pushed up Glovis’ price relative to Mobis.

Each outcome is beset with its own set of issues. For Glovis to be the sole holdco, it has to come up with nearly ₩2tn to buy Kia’s Mobis stake, probably through new, and burdensome, debt. Glovis may also face the risk of forced holdco conversion, creating an issue with Kia as a “great grandson” subsidiary.

This speculation pushing up Glovis relative to Mobis has yet to be substantiated/justified, suggesting Glovis is overbought. Sanghyun expects a mean reversion, and recommends a long Mobis and short Glovis.

Navitas Ltd (NVT AU) has agreed to extend the exclusivity period granted to the BGH consortium to 1 March (from 18 Feb), in order to allow additional time for BGH to complete a limited set of remaining due diligence investigations.

Netcomm Wireless (NTC AU) has received $1.10 cash offer (53% premium to last close) from Casa Systems (CASA US) via a Scheme. The deal values Netcomm at ~US$114m. The scheme is subject to FIRB and shareholder approval. Stewart David Paul James, a NED, holds 12.3% and is the major shareholder. The announcement states that each Netcomm director intends to vote the Netcomm shares held by them in favour of the scheme – subject to a +ve IFA opinion and in the absence of a competing offer. This includes Stewart’s stake.

MYOB Group Ltd (MYO AU)announced no superior proposal emerged after concluding its ’go shop’ period for rival offers to KKR’s takeover proposal. At a gross/annualised spread of 0.9%/4.8%, assuming early May payment, this looks to be trading a bit tight.

CCASS

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

NextDecade Corp (NEXT US) recently announced that it started offering long-term contracts indexed to the crude Brent in order to attract more LNG buyers. This follows the agreement reached by Tellurian Inc (TELL US) with Vitol back in December to index a long term contract with the Asian LNG price benchmark JKM. While typically US LNG projects are indexed to the Henry Hub, declining crude oil and LNG prices seem to have diminished the appeal of the Henry Hub pricing compared to the oil indexation. This insight takes a look at the latest trends in the LNG markets to assess which companies are taking the lead in the race to bring to FID in 2019 their proposed LNG projects.

Exhibit 1: NextDecade adds Brent indexation to its commercial offering

Source: NextDecade Corporate Presentation February 2019

London-based investors are turning cautiously optimistic on China’s growth outlook amid the latest easing measures in January

There is still little awareness about the rising deflation risk

Interest in the trade war has subsided

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

An activist has come forward, and the external statutory auditor and lead shareholder (wife of founder) are against the offer, but Kosaido Co Ltd (7868 JP) situation still fits pretty cleanly in the “Too Hard” bucket for now.

Since announcing its foray into the deeper waters of being the fourth Type I Mobile Network Operator in Japan, Rakuten’s shares have taken a mighty hit. But the focus in this insight is on ride-sharing company Lyft. In March 2015, Rakuten CEO Hiroshi Mikitani announced that Rakuten had invested US$300mn in Lyft, giving it a 11.9% stake after Series E round in May 2015. Recent articles suggest that Rakuten remains the top investor.

As best as Travis Lundy can tell, from sources who track this, Rakuten is the single largest shareholder in Lyft, with a holding in the 10.4-12.0% range. That would suggest a position value of US$900mn-$1.2bn based on the last funding round in June 2018. At a $25bn pre-money IPO valuation, that would be worth US$1.5-2.0bn for a likely pre-tax IPO uplift of US$590-800mn.

A report late Thursday Asia time suggested the Lyft roadshow would start the week of March 18th, which would mean the S-1 will be available two weeks before that. Investors will know more about Rakuten’s ownership of Lyft by the end of next week or very early the following week. Travis would want to be long for now.

DHICO announced a larger-than-expected ₩608.4bn rights offer. ₩543bn is expected to be raised through common shares at a preliminary price of ₩6,390; and ₩65bn via RCPS at a preliminary price of ₩6,970. This is a combined 72.56% capital increase a 42.05% share dilution. Concurrently, Doosan E&C announced a ₩420bn rights offer at a preliminary price of ₩1,255, a 15% discount to last close.

For DHICO, Mar 27 is the ex-rights day for both Common and RCPS. Subscription rights (for the Common) will be listed and trade on Apr 19~25. May 2 is final pricing. May 8 is subscription and May 16 is payment. New Common shares will be listed on May 29.

For E&C, the final price will be fixed on Apr 30. Whichever is higher – ₩1,255 or Apr 26~30 VWAP at a 40% discount – will be the final offering price. Mar 27 will be the ex-rights day. Subscription rights will be listed and traded on Apr 18~24. New shares will be listed on May 24.

₩1,255 is a lot more aggressive than generally viewed. DHICO owns nearly two thirds of E&C. With a 20% oversubscription, nearly ₩300bn will likely come from DHICO, essentially buttressing E&C at an even heftier price. Which is probably why the market is being less harsh on E&C relative to DHICO.

The 247-4 Form is out with a tender offer period between 26 Feb-1 April, and payment on the 4th April. The frustrating part is how Delta’s FY18 dividend of Bt2.30 is treated. On one hand, it says the Bt71 Offer price is final unless there is a MAC. Further into the Offer doc, it mentions the Offeror “reserves the right” to reduce the offer price if a dividend is paid. DELTA’s IR believes the dividend will be added, but it is not crystal clear.

Furthermore, there is no minimum acceptance condition, as potentially flagged earlier, which means there is no possibility of fast-tracking payment. Some precedent voluntary offers included a minimum acceptance, which provides an expedited payment should investors who tender shares AND revoke their right to withdraw – provided that minimum is fulfilled.

Shares traded up after the document came out, shrugging off the ambiguity in the document. Currently trading at a gross/annualised return of 1.1%/11%. The dividend is subject to a 10% tax for non-residents.

The previous Friday, the Offerors for M1 announced that their Offer had been declared Unconditional In All Respects as the tendered amount was 57.04% and the total held by concert parties was 76.35%. Axiata Group (AXIATA MK)made an announcement to the Bursa Malaysia that it had accepted the Offer as required because it was a significant asset disposal. Going unconditional has triggered an extension of the Closing Date to 4 March 2019.

If you want to fight this with an appraisal, you can. Travis doesn’t see the point. If you want to hold on to the stock in order to block full squeezeout and play chicken with the big boys, you can, but it requires a relatively big ticket (roughly 6.73% of the shares out).

So Travis recommends taking the money. It was better to take the money in early January and re-deploy, rather than wait for the close of the offer. He would accept now and sees no upside from waiting.

When the Tender Offer / MBO for Kosaido was announced last month, Travis’ first reaction was that this was wrong, concluding this was a virtual asset strip in progress, and suggested that the only way this was likely to not get done is if some brave activist came forward.

Shortly afterwards, an activist did come forward. Yoshiaki Murakami’s bought 5% through his entity Reno KK, and later lifted his stake (combined with affiliates) to 9.55%. Travis thought the stock had run too far at that point (¥775/share). While still cheap, he did not expect Bain to lift its price by 30+%, nor a white knight to arrive quickly enough.

This week a media article suggested longstanding external statutory auditor Mr. Nakatsuji and lead shareholder Sakurai Mie were against the takeover.

The possibility this deal fails because the “put protection” of the deal price at ¥610 is no longer solid has gone up. Conversely, the probability that Bain and the MBO have to come in with a price adjustment higher has gone up. Travis is inclined to remain bearish in the medium-term as there is a significant likelihood there is no alternative solution during the Tender Offer period itself.

After announcing earlier this month a number of indicative non-binding bids were received for a “whole of company transaction”, the AFR is now reporting (paywalled) that Lone Star has also joined the battle for Aveo Group (AOG AU). (A Case for Privatising Aveo)

Saputo Inc (SAP CN) and Dairy Crest announced an all-cash deal where Saputo will buy Dairy Crest for 620p/share, to be implemented through a Scheme of Arrangement with an expected close in Q2 2019. This appears to tick all the necessary boxes. Friendly, horizontal integration, and limited job losses. Shares are trading through terms early (he published at 628.5p), perhaps on expectations the wide open register means shareholders can try to hold out for a higher price.

At almost 14x EV/EBITDA on a TTM basis and a bit lower on a March 2019 FY-end basis, it is a high enough multiple to not be insulting for a dairy company, and may keep other suitors away.

Dairy Crest’s directors have given irrevocable notice to accept, and the directors’ advisors (Greenhill & Co) have deemed the Offer “fair and reasonable.”

One extra turn of EV/EBITDA would lift the takeover price just under 10%. That would clear out most of the naysayers who bought in the frothier “we’re going to be an asset-light branded goods company” days of 2015-2017. Doable, but as it is an agreed deal, Travis doesn’t see the need to push it.

In its prior letter to Ophir on the 14 January, Petrus recommended selling the South-East Asian (SEA) assets to Medco, with a low-end fair value, before synergies, of £0.64/share, through to £1.42/share on a blue sky basis. It also argued that Ophir should negotiate with the Equatorial Guinea ministry (the regulator that terminated the Fortuna license, resulting in write-offs of US$610mn) to be compensated for its $700mn investment and the unfair seizure of the license, otherwise it would set a precedent for other international operators doing business in EG.

Petrus has now rounded on Schrader over perceived mismanagement of the EG licence, and a lack of professionalism in not soliciting and considering offers for Ophir from other buyers. Petrus’ beef is not an outlier – alternative hedge fund Sand Grove has increased its exposure, via cash-settled derivatives, to 17.28% (as at 13 February); while Ian Hannam, who advised Ophir’s board on its 2013 right issue, is understood to have also written to Ophir’s interim CEO Alan Booth and the board saying Medco’s offer is too low.

Overall, Petrus’ assertions that Ophir is being sold at “sub optimal terms” appear valid, most notably on the EG compensation and the illogical operations update earlier this month. The alternative push to sell the SEA assets separately, as that has been Medco’s core focus, not international operations, also makes sense.

Last month, DSV A/S (DSV DC) made a public proposal of a takeover for cash and scrip valued at CHF 170/share, which came at a 24% premium to last and +31% vs 1-month VWAP. The #2, #3, and long-time #4 shareholders are firmly and publicly in the camp of trying to get something done. 45.9%-shareholder Ernst Göhner Foundation is sending mixed signals – do they want a higher price? Or do they want to wait and let Panalpina grow by its own consolidator strategy?

Panalpina has now confirmed that it in preliminary talks with Kuwait-listed logistics company Agility Public Warehouse. A Bloomberg report suggested a deal could be reached as early as this past week for Agility’s logistics business. The same article suggested the Göhner Foundation is supportive of the new talks. Agility’s press release was much more non-committal.

DSV has also announced a new all cash CHF 180/share offer for Panalpina; although the original cash and scrip offer was then worth CHF 184.5/share, which is an even better premium to pre-offer terms. One wonders whether cash-only would suit the Foundation; the DSV press release seemed to respond to that.

It is not clear what would drive the Foundation to give up its control. And Panalpina’s measly share price reaction to the all-cash offer suggest there is considerable skepticism out there. But at some price, Panalpina’s board looks pretty stupid to not accept the cash.

If you do not think a deal with DSV has any chance of getting up, Panalpina shares are a sell here. If they overpay for Agility and cannot improve their own margins well past historical highs in a market trending weaker, then the shares could drop.

Using Curtis’ figures, the implied stub is at its lowest level since a brief downward spike in February 2015, and you would have to go back to April 2014 to find a lower level.

The push back on this setup is that the auto operations have recorded marginally, yet sequential profit declines in FY16 and FY17; while recording three sequential quarterly declines up to December 2018. The big question is whether Mahindra can regain market share as it kick-starts a new model cycle.

In contrast, Sanghyun believes the Holdco is still undervalued relative to the Sub by about 10%. Plugging in Sanghyun’s numbers, I back out a discount to NAV of 45% against a one-year average of 30%, with a 12-month range of -51.5% to 15.5% (premium).

Back on the 13 December 2018, Can One announced a proposed MGO for Kian Joo at RM3.10/share, a 52.7% premium to last close. This required Can One shareholders’ approval which was received on the 14 February. Can One’s current 33% stake in Kian Joo accounts for ~86% of its market cap. The offer doc should be out, on or before the 7 March, with payment either late March (along with the first close of the Offer), or early April, depending on when the offer turns unconditional. The offer is conditional on 50% acceptance. Both sides are illiquid.

This looks like a decent exit for Kian Joo shareholders. Apart from EPF with 10.1%, former NED Teow China See is the only other shareholder with >5% with 8.9%.

For Can One, this is an aggressive pitch to make Kian Joo a subsidiary amidst an uncertain economic backdrop, while potential synergies may be offset via higher interest costs.

There are still two schools of thought on the HMG restructuring. One is that Glovis/Mobis are merged into a holdco entity. Or Glovis becomes the holdco with Mobis→ HM→ Kia Motors Corp (000270 KS) below. Since late 3Q18, there has been increased speculation on the latter. This has pushed up Glovis’ price relative to Mobis.

Each outcome is beset with its own set of issues. For Glovis to be the sole holdco, it has to come up with nearly ₩2tn to buy Kia’s Mobis stake, probably through new, and burdensome, debt. Glovis may also face the risk of forced holdco conversion, creating an issue with Kia as a “great grandson” subsidiary.

This speculation pushing up Glovis relative to Mobis has yet to be substantiated/justified, suggesting Glovis is overbought. Sanghyun expects a mean reversion, and recommends a long Mobis and short Glovis.

Navitas Ltd (NVT AU) has agreed to extend the exclusivity period granted to the BGH consortium to 1 March (from 18 Feb), in order to allow additional time for BGH to complete a limited set of remaining due diligence investigations.

Netcomm Wireless (NTC AU) has received $1.10 cash offer (53% premium to last close) from Casa Systems (CASA US) via a Scheme. The deal values Netcomm at ~US$114m. The scheme is subject to FIRB and shareholder approval. Stewart David Paul James, a NED, holds 12.3% and is the major shareholder. The announcement states that each Netcomm director intends to vote the Netcomm shares held by them in favour of the scheme – subject to a +ve IFA opinion and in the absence of a competing offer. This includes Stewart’s stake.

MYOB Group Ltd (MYO AU)announced no superior proposal emerged after concluding its ’go shop’ period for rival offers to KKR’s takeover proposal. At a gross/annualised spread of 0.9%/4.8%, assuming early May payment, this looks to be trading a bit tight.

CCASS

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

NextDecade Corp (NEXT US) recently announced that it started offering long-term contracts indexed to the crude Brent in order to attract more LNG buyers. This follows the agreement reached by Tellurian Inc (TELL US) with Vitol back in December to index a long term contract with the Asian LNG price benchmark JKM. While typically US LNG projects are indexed to the Henry Hub, declining crude oil and LNG prices seem to have diminished the appeal of the Henry Hub pricing compared to the oil indexation. This insight takes a look at the latest trends in the LNG markets to assess which companies are taking the lead in the race to bring to FID in 2019 their proposed LNG projects.

Exhibit 1: NextDecade adds Brent indexation to its commercial offering

Source: NextDecade Corporate Presentation February 2019

We revise down EPG’s net profit forecast by 10-12% in 2019-21E. However, we still maintain our positive outlook toward its FY20-21E earnings driven by growth in every business units: 1) sales and margins recovery for EPP segment (22% of revenue in FY9M19) from changing its product mix toward more on food packaging; 2) consistent revenue growth for automotive and thermal insulators (50% and 28% sales contribution). The new target price at Bt9.90 derived from its 2-years average trading range of 23xPE’19E.

A slash down in earnings to factor in lower-than-expected sales growth in Aeroflex and EPP. Meanwhile, raising up SG&A to sales ratio to reflects operation enhancement program in Australia.

Turn bearish view toward on TJM which contributed 12% in total revenue in 9MFY19 (April-December 2018), due to difficulty in running businesses given high labor cost in Australia and production scale that still far behind the rival.

EPP’s gross margin was already bottomed out and expect to normalize on the back of low material price sourced in 4Q18, and, higher contribution from high margin products on food segment.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

PLAT reported 4Q18 net profit of Bt198m (-3%YoY, +6%QoQ) and in-line with our expectation.

Slow sales growth (+3%YoY) due to the delay in opening The Market Bangkok project from Dec 18 to 14 Feb 2019 caused a YoY drop in 4Q18 performance. In summary, 2018 earnings grew 2%YoY driven by 5%YoY in sales growth. We also believe current share price already priced in this delay.

Despite a drop in 4Q18 earnings YoY, we expect strong recovery in 1H19 earnings driven by opening The Market Bangkok (70% booked).

We maintain our positive view toward its outlook back by the rise in average rental rate trend after long term contracts expiration in 2020-2021E.

Announced an annual dividend payment of Bt0.2 (XD on 4 Mar), which is equivalent to 2.6% upcoming dividend yield.

We maintain BUY rating with a target price of Bt9.4 based on DCF (10.8%WACC, 0% TG)*.

Plans regarding Samsung and Huawei’s foldable smartphones are out. The companies, which happen to be two of the largest contenders in the smartphone landscape are expected to unveil their foldable smartphone prototypes this month. In 4Q2018, Samsung, coming in first place, held a market share of 18.7% while Huawei, in third place, held a market share of 16.1%. Both companies are following different strategies when it comes to their foldable phone models.

The concept of foldable phones revolves around devices that can be folded into the size of a smartphone or opened up in to the size of a tablet. Huawei is said to be planning to introduce their foldable smartphone with 5G compatibility while Samsung is planning to release their foldable model with 4G compatibility. The market leader aims to leverage the expertise it has gained on its display technologies in its foldable smartphones.

MAJOR 4Q18 net profit was Bt259m (+247%YoY, +26%QoQ). The impressive earnings was driven by solid guests admission (+97%YoY).

4Q18 revenue was Bt3.0bn (+59%YoY, +44% QoQ). Interesting movies lineup was the factor, pushing admission revenue (+88%YoY) and concession revenue (+70%YoY).

Gross profit margin was strong at 37.6% from 28.7% in 4Q17 and 30.8% in 3Q18, thank to the higher contribution of concession revenue, which has decent margin.

SG&A to sales was under control at 27.0%, compared to 34.3% in 4Q17 and 26.7% in 3Q18.

We maintain a BUY rating on MAJOR with 2019E target price of Bt31.00, derived from a PER of 24.2x, which is +1 SD of its 3-year trading average. We expect MAJOR to continuously deliver robust earnings in 2019E, given the fascinating movies lineup and advertising sales model changing from direct selling to selling through agencies.

With Form 247-3 (Intention to Make a Tender Offer) and the FY18 dividend (Bt2.30/share) for Delta Electronics Thai (DELTA TB)having been announced, this insight briefly provides an updated indicative timetable for investors.

The next key date is the submission of Form 247-4, the Tender Offer for Securities, which will provide full details of the Offer.

Date to be on the registry to receive full-year dividend

As announced

22-Mar-19

Last day for revocation of shares

20th day of Tender Offer1

29-Mar-19

Close of Offer

Assuming 25 business days tender period

2-Apr-19

AGM

As announced

3-Apr-19

Consideration paid under the Offer

Assume 3 business days after close of Offer

11-Apr-19

Payment of FY18 dividend

As announced2

Source: Delta, my estimates 1 assuming the shareholder has not forfeited the right to revoke 2 the dividend is subject to a 10% WHT for non-residents.

This above indicative timetable assumes a conditional offer based on a minimum acceptance level of at least 50%. Payment under the offer may indeed be earlier, as explained below, which also ties in with a shareholders’ right to revoke shares tendered.

In addition, investors should not tender once the offer opens – assuming the tender period commences on the 25 February – but wait until their shares are on the registry as at 4 March to receive the FY18 dividend.

Currently trading at a 2.2%/22% gross/annualised spread. Bear in mind the dividend is subject to 10% tax.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

An activist has come forward, and the external statutory auditor and lead shareholder (wife of founder) are against the offer, but Kosaido Co Ltd (7868 JP) situation still fits pretty cleanly in the “Too Hard” bucket for now.

Since announcing its foray into the deeper waters of being the fourth Type I Mobile Network Operator in Japan, Rakuten’s shares have taken a mighty hit. But the focus in this insight is on ride-sharing company Lyft. In March 2015, Rakuten CEO Hiroshi Mikitani announced that Rakuten had invested US$300mn in Lyft, giving it a 11.9% stake after Series E round in May 2015. Recent articles suggest that Rakuten remains the top investor.

As best as Travis Lundy can tell, from sources who track this, Rakuten is the single largest shareholder in Lyft, with a holding in the 10.4-12.0% range. That would suggest a position value of US$900mn-$1.2bn based on the last funding round in June 2018. At a $25bn pre-money IPO valuation, that would be worth US$1.5-2.0bn for a likely pre-tax IPO uplift of US$590-800mn.

A report late Thursday Asia time suggested the Lyft roadshow would start the week of March 18th, which would mean the S-1 will be available two weeks before that. Investors will know more about Rakuten’s ownership of Lyft by the end of next week or very early the following week. Travis would want to be long for now.

DHICO announced a larger-than-expected ₩608.4bn rights offer. ₩543bn is expected to be raised through common shares at a preliminary price of ₩6,390; and ₩65bn via RCPS at a preliminary price of ₩6,970. This is a combined 72.56% capital increase a 42.05% share dilution. Concurrently, Doosan E&C announced a ₩420bn rights offer at a preliminary price of ₩1,255, a 15% discount to last close.

For DHICO, Mar 27 is the ex-rights day for both Common and RCPS. Subscription rights (for the Common) will be listed and trade on Apr 19~25. May 2 is final pricing. May 8 is subscription and May 16 is payment. New Common shares will be listed on May 29.