Mitsubishi has finally given up its hope of convincing Aeon to merge Ministop (9946 JP) with Lawson and is selling its stake in the largest retail group.

There will be no change to the extensive supply relationship between the two companies and Mitsubishi’s food wholesale arm, Mitsubishi Shokuhin (7451 JP).

While Aeon seems to have spurned Mitsubishi for now, it is hard to see how Aeon will progress in the convenience store sector without Mitsubishi’s help. In the short-term Ministop looks like a poor investment but Aeon may have to sell to Mitsubishi eventually and will want a good price for it.

Highlights of significant recent happenings include:

Substantive Deep Dive – Canada’s BlackBerry Ltd (BB CN) seeks to be the go-to provider of web Security: Why we believe investors should look at Blackberry as a way to hedge their exposures to the increasing list of companies who are susceptible to adverse impact from security breaches.

Feeding the Dragon – Chinese buying of US firms brakes abruptly, obliterating the long-term trend, and now Japan has become the second-largest market for outbound M&A globally. Also, South Korean food giant Cj Cheiljedang (097950 KS) is continuing its aggressive expansion into the U.S. market

RELATIVE PRICE SCORE – The Relative Price Score (RPS) measures stock price performance relative to TOPIX and is calculated by comparing the current deviation with the mean absolute deviation of monthly and daily relative share prices. As all companies are, as a result, on a comparable scale, ‘overbought’ and ‘oversold’ outliers and changes in scoring can reveal short-term and longer-term trading opportunities. This insight updates our list of overbought and oversold companies, reviews the best and worst performing companies by RPS over the last two months and adds some specific comments on stocks on each category.

RPS STATISTICS – The Company ‘outlier’ thresholds are set to “+4” for overbought and “-2” for oversold. Currently, of the 3,686 listed companies for which monthly data is available, 91 companies are ‘Overbought’, and 120 are ‘Oversold’ – 2.5% and 3.2%, respectively of the total. For companies with a market capitalisation of over ¥100b, there are 35 ‘Overbought’ and 24 ‘Oversold’ companies.

RPS ‘TOPS’ – In the last two years, 445 companies have achieved an RPS of ‘4’ or more. 80% have seen their RPS fall to below ‘4’ within the following two months. For companies with a market capitalisation higher than ¥100b, the numbers are 95 companies and 63% – demonstrating the superior persistence of large capitalisation companies in this regard. Some examples of RPS mean reversion in the last two months have been Descente (8114 JP), Ariake Japan (2815 JP), Fancl (4921 JP), Bandai Namco (7832 JP), Don Quijote (7532 JP), and Gmo Payment Gateway (3769 JP).

Source: Japan Analytics

RPS ‘BOTTOMS’ – 296 companies have seen their RPS fall to ‘-2’ or below in the last two years. 58% have seen their RPS recover to above ‘-2’ within three to six months. For larger capitalisation companies, the numbers are 72 companies and 67%. Some recent examples of positive RPS mean reversion in the last two months have been LINE Corp (3938 JP) – a ‘contrarians only’ selection in our last Insight, and Tokyo Electric Power (9501 JP).

Source: Japan Analytics

In the DETAIL section below we list the current very overbought (RPS>5), too late to buy (RPS >4<5) and oversold (RPS <-2) stocks as well as the largest two-month positive and negative changes in RPS.

NB – All data is as of January 17th close.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

SLOW & STEADYRECOVERY – From December 25th’s lows of 8% by number and 11% by value, the percentages of Japanese stocks above the weighted sum of moving averages have continued to recover to now 19% by number and 26% by value. Total Market Value has now risen by 11.2% from the Christmas Day low and is overdue a ‘breather’.

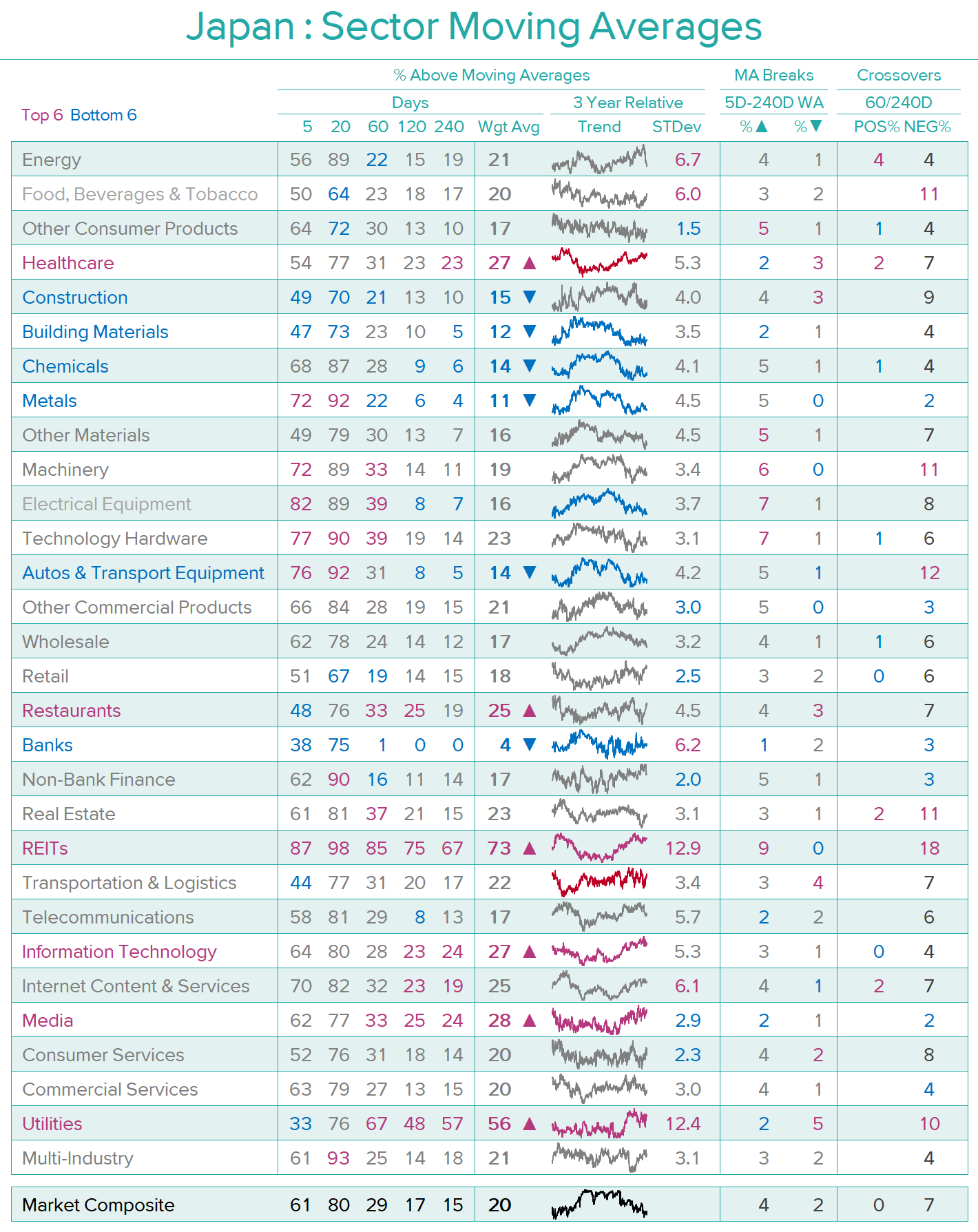

– SECTORS –

LEGEND: The ‘sparklines’ show the three-year trend in the weighted percentage above moving average relative to the Market Composite and the ‘STDev’ column is a measure of the variability of that relative measure. The table also provides averages for the breaks above and breaks below and the positive and negative crossovers.

SECTOR BREAKDOWN – The top six sectors measured by their percentage above the weighted average of 5-240 Days remain domestic and defensive. REITs, Information Technology, Media, Healthcare and Utilities continue from our previous review with Restaurants replacing Transportation. Equally predictable is the bottom half-dozen – Banks, Autos, Metals, Building Materials, and Chemicals remain from two weeks ago, with Construction replacing Autos.

– COMPANIES –

Source: Japan Analytics

COMPANY MOVING AVERAGE OUTLIERS – As with the Market Composite and Sectors, the Moving Average Outlier indicator uses a weighted sum of each company’s share price relative to its 5-day, 20-day, 60-day, 120-day and 240-day moving averages. ‘Extreme’ values are weighted sums greater than 100% and less than -100%. We would caution that this indicator is best used for timing shorter-term reversals and, in many cases, higher highs and lower lows will be seen.

In the DETAIL section below, we highlight the current top and bottom twenty-five larger capitalisation outliers, as well as those companies that have seen the most significant positive and negative changes in their outlier percentage in the last two weeks and provide short comments on companies of particular note. UUUM (3990 JP) is currently the most ‘extreme’ positive outlier, and Welcia (3141 JP) the most ‘extreme’ negative outlier

After dropping to a 52-week low of ¥11,405 on January 17 – the day after management announced a large downward revision to sales and profit guidance – Nidec rebounded to close at ¥13,055 on Friday, January 25. The latter price is 30% below the ¥18,525 peak reached a year earlier. Both the shock of the downward revision and the reflexive optimism of believers in the company now seem to have been discounted.

Consolidated sales and profits dropped abruptly in the three months to December and are expected to drop further in 4Q of FY Mar-19 due to weak demand in most regional markets, inventory write-downs and restructuring costs. Nidec is already reconfiguring its global supply chains, shipping products to the U.S. from Mexico and Europe instead of from China and planning to build factories to make motors for electric vehicles in Mexico and Poland in addition to China.

With most of the one-off expenses out of the way, profits should start to recover in FY Mar-20. Sales, on the other hand, seem likely to decline further due to weak unit demand and pricing for HDD spindle motors, falling auto production in China and elsewhere, and weakness in other industrial and commercial markets. Recovery will depend on U.S.-China trade relations and the state of the world economy, and new acquisitions that cannot be predicted. As things stand now, we expect sales to pick up going into FY Mar-21. In the long run, the company should continue to benefit from the electrification of the auto market and factory automation.

At ¥13,055, the shares are selling at 34x management’s EPS guidance for FY Mar-19, 32x our estimate for FY Mar-20 and 30x our EPS estimate for FY Mar-21. Projected EV/EBITDA multiples for the same three years are 18x, 17x and 15x. Price/book value as of the end of December is 3.9x. The dividend yield is less than 1%. Over the past few years, the P/E has found support at 20x, EV/EBITDA at 10x and the PBR at 2.5x. The January 17 low put the shares on 30x management’s new EPS guidance for this fiscal year.

On Friday 25 January 2019, shareholders of Pioneer Corp (6773 JP) voted to implement a self-imposed (self-inflicted?) equity “cramdown” of sorts.

In September, Pioneer and BPAE signed a memorandum of understanding whereby Baring Private Equity Asia would lend money to Pioneer and subsequently inject equity capital and keep the company listed. In December, BPAE and Pioneer management decided that the equity injection would push out then-existing shareholders at a steep discount to the lowest share price the stock had theretofore seen in the company’s 50-year-plus history of being listed.

Now that’s done.

The situation now looks quite a bit like a regular “risk arb” or “wind up” situation, though investors do not have exact understanding of the payment date.

On December 17th 2018, the TSE announced a somewhat strange and unexpected treatment of the TSE-calculated indices for two companies where shares were issued to shareholders of a foreign company where the Japanese company had acquired the foreign company through a Scheme of Arrangement under foreign jurisdiction.

The announcements for TOPIX and JPX Nikkei 400 were made then, and despite the events being entirely similar in construct, but different in month of Scheme Effective Date, they were put in the same month for Mitula and the first tranche of the Takeda inclusion, which was split between two months because of its large impact.

The large IPO last month of Softbank Corp (9434 JP) means there is another large inclusion going effective as of the open of trading on 31 January.

Wednesday is going to be a big day.

If everyone trades their required index amount on the day, it should be a trillion yen plus of flows.

CONSISTENCY PAYS – In troubled markets, investors often seek out companies with greater earnings stability and a history of consistent stock outperformance. Conversely, companies that offer investors more of a rollercoaster ride (Chiyoda Corp (6366 JP) being an excellent recent example) are less rewarding, especially when adjusted for volatility. In an attempt to sort the ‘Steady Eddies’ from the Rollercoaster Rides’, we have created a Consistency Score – a composite based on our Results Score, Forecast/Revision Score, Relative Price Score and Volume Score – which measures the variability, consistency, correlation, and range of each of these scores for every company. Cap-weighted aggregate Consistency Scores are then derived for 321 Peer Groups and 29 Sectors – REITs are excluded from this analysis. Over 3 million data points have been reviewed in creating this analysis. As the old slogan goes – “we do the work, so you don’t have to’.

‘CARP = CONSISTENCY-AT-A-REASONABLE-PRICE‘ – Our findings will not surprise long-term investors in Japanese equities; the simple asset allocation decision to prefer domestic growth over global value has determined the quartile-ranking of many strategies in recent years. Although many of these Sectors, Peer Groups and stocks are now overvalued, we do not expect the underlying business dynamics to change in the years ahead and many excellent investment opportunities remain, especially down the cap-scale. Periodic and often substantial mean reversions in the more cyclical sectors, such as the one that has occurred in the last two days, will offer attractive trading opportunities for more-nimble portfolio managers. Longer-term orientated investors are better-advised to continue to favour ‘consistency-at-a-reasonable-price’. Some of our ‘findings’, as explained in more DETAIL below, are as follows: –

SECTORS – The better investors in Japan over the last two decades have eschewed traditional manufacturing in favour of Services, IT/Internet, Retail, Restaurants and ‘FB&T‘. Only Machinery and Electrical Equipment outperformed the market’s 4% compound annual growth rate (CAGR) over the period.

PEER GROUPS– The most-consistent Peer Groups are found in industries associated with food, drugs, welfare, shelter and amusement. Only five of the top-forty Peer Groups – Online Payment Services, E-Commerce, IT System Services, Telecom Distribution Services and Internet Software & Services belong to the ‘new age’. There are no manufacturing Peer Groups in the top-forty. The best performing Peer Group is Securities Services, and the worst-performing is Investment Management & Advice. Although both havesimilar levels of consistency, the stock exchange has beaten its fund managers by 28% annually since 2005.

COMPANIES – The simple average fourteen-year compound annual share price appreciation for all listed large-cap companies is +5.1%. For all listed companies the average falls to just +0.5%, highlighting the perils of investing in Japan’s small caps. The average share price CAGR for our hindsight-selected top-forty is +18.7%. In contrast, only one of our forty least-consistent companies outperformed the market and the average for the least-consistent forty companies was a negative -3.2%. Unsurprisingly, there are eight banks and six steel companies on the list, along with two glass companies and two shipping lines.

CONSISTENCY HALL OF FAME/SHAME AWARDS – We have selected one company from each of the most and least consistent lists as the winner of a ‘Consistency Award’. Both are highlighted in the chart above. One of them will be as surprising to many readers as it was to us.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Profit Warning for Q4 2018 and Q1 2019: Two Fridays ago, Elon Musk warned that Q4 profits came in lower than Q3’s, despite an 8% QoQ rise in vehicle sales during Q4. He also announced a 7% cut in Tesla’s workforce, as Tesla is now facing “a tiny profit” in Q1 that will be achieved with “great difficulty, effort and some luck”. These are extremely bearish comments from a perennial optimist like Musk. If true, however, it kills the growth story at Tesla. And with the average 15% price cut of the Model 3 in the US and 17% in China, it also shows that Tesla may have misread the demand environment for its high-priced electric sedan.

Model 3 Demand in the US has Clearly Been Exhausted: September 2018 saw peak monthly sales of 22,250 units in the US, which fell to an average monthly rate of 18,039 units in Q4. There are no more wait lists for the Model 3 at current prices: Tesla’s website says delivery can be made in under 2 weeks. In the January 18th profit warning, Musk admitted that Tesla must now sell its lowest-end version for $35,000 from May, or see production fall. At this price, Tesla’s Model 3 probably just breaks even, by our estimates.

Weak Model 3 Launch in Europe: It was hoped that the Model 3’s European launch this March would make up for waning demand in the US. But since opening up configurations for reservation holders on December 7th, Tesla only received 13,773 orders, which is a whopping 24% lower than recent monthly sales in the US. Musk was forced to open up configurations to non-reservation holders, but this led to only 2,436 extra orders over the following 2 weeks. In the US, Tesla opened up the Model 3 floodgates to non-reservation holders 12 months after launching the car. In Europe, it took less than 4 weeks.

No Hopes for Tesla in China Either in 2019: Tesla’s registrations in China for October and November 2018, combined, fell by 72% YoY and overall auto demand is weakening there. Musk proclaimed that Tesla would start production of the Model 3 in Shanghai by 2019-end. The factory site is a barren plot of land (see Figure-5). It took VW 23 months to build its latest factory in China and Toyota’s new Alabama plant will require 28 months. Why should we believe that Tesla only needs 11 months?

Watch the Competition for Tesla in 2019: Tesla will face true competition this year for its first time as 4 new European EVs hit the market. During Q4 of 2018, Jaguar’s new I-Pace outsold Tesla’s Models S and X, combined, in the Netherlands–Tesla’s number two market after the US. Audi’s e-Tron SUV–due out next month–had over 20,000 orders as of December 7th last year. Porsche’s new Taycan–a powerful rival for Tesla’s Model S–has sold out its first year of production, with most orders coming from Tesla owners. The Models S/X provided 50% of automotive gross profit in the 2H of 2018, by our estimates. A fall in volume will heavily impact profits.

Spending Will Spike in 2019 and Lead to Negative FCF: Tesla was able to squeeze out a profit during the 2H of 2018 largely because of suppressed spending on R&D and infrastructure. In order to roll out the new Shanghai plant and bring the new Model Y to market, both capex and R&D must rise significantly in 2019. Our list of “spending needs” (see Figure-1) shows that capex should nearly double to $4.5bn in 2019. Including debt obligations and payables, Tesla’s total cash needs in 2019 come to $9.3bn, which is over twice its equity. A highly dilutive public share offering appears inevitable.

Why 2019 Could Be the End of Tesla: Tesla proved in 2018 that, even with higher sales volumes and lofty pricing for the Model 3, it could only attain an estimated 2H operating margin of 1.7%, excluding environmental credits, one-offs, and stock-based compensation. 2019 will be incredibly harder as 1) Tesla faces stiff competition for the first time since its inception; 2) a lower-priced Model 3 will not generate enough profit to cover falling profitability of the Models S/X; and 3) most significantly, a steep rise in capex and R&D will lead to higher losses and negative FCF. Tesla may need a bailout by a deep-pocketed suitor this year. But this could only occur at a much lower share price.

Olympus Corporation is currently trading at JPY4,525 per share which we believe is overvalued based on our EV/EBIT valuation. The company generates nearly 80.0% of its revenue from its Medical Business where it is the global market leader for gastrointestinal endoscopes. Despite Olympus’ market share and technology leadership, the segment has been hit by investigations related to its duodenoscopies and has been fined for violating safety regulations. In addition, the Medical Division is also subject to several bribery-related investigations by the US Department of Justice and could risk losing its market share if the allegations are proven given the industry is highly competitive. Meanwhile its Imaging Business which offers cameras and lenses, is operating in a contracting market, where the segment continues to see declining revenues and is loss making.

To add to all of the above, the company is under scrutiny for governance-related issues such as lack of board diversity as well as poor corporate culture. On the positive side, the management has announced a plan to transform its business, including appointing three new (non-Japanese) directors to its board, all due to the pressure from its largest shareholder ValueAct Capital. The Management has mentioned that they will be proposing one of the partners of ValueAct as one of the three new directors at its shareholder meeting in April 2019, which is encouraging. However, that being said, we are yet to witness any tangible improvement in the way the company has conducted itself since the exposure of its accounting fraud in 2011 and has not been able to stay free of controversy. Hence, in our opinion the hefty premium at which the shares are currently trading is not justified suggesting to us that the potential turnaround in governance quality is being priced in too fully at this point. It is uncertain what other skeletons may be in Olympus’ closets and it seems premature to afford the stock a premium valuation.

In the latest data, MVNOs (mobile virtual network operators) have reached 7.0% market share of Japan’s main 3G and LTE (4G) services with over 12m subscribers.

Government support remains robust for the MVNOs. Mr. Suga, the Chief Cabinet Secretary, has suggested that MVNOs, in all forms, should expand to 50% of the market in the future.

As Rakuten (4755 JP) prepares for its full MNO (mobile network operator) service launch later this year, the Rakuten MVNO services continues to execute well, taking market share and building a formidable foundation of subscribers. Rakuten is now Japan’s largest MVNO by customer numbers. We expect Rakuten will struggle to make a reasonable return on its MNO on a standalone basis, but it may strengthen the company’s overall ecosystem and create enough synergies to add positive value to the group.

In this version of the GER weekly events wrap, we assess the recent lock-up expiry for Pinduoduo (PDD US) which may have led to a short squeeze. Secondly, we assess the debt tender for Softbank Group (9984 JP) which may be supporting the equity. Finally, we provide updates on bids for M1 Ltd (M1 SP) and Healthscope Ltd (HSO AU) as well as update a list of upcoming M&A and equity bottom-up catalysts.

The rest of our event-driven research can be found below.

Best of luck for the new week – Rickin, Venkat and Arun

Our thesis on Subaru has maintained for some time that margins were inflated due to under-spending and that these costs would surface in one form or the other over time.

As it turns out, the costs were incurred through recalls as Subaru downgraded its FY OP guidance from ¥300bn to ¥220bn on 5 Nov. What continues to concern us is the constant stream of negative news flow on quality and sustainability-related issues. While the latest announcements do not imply excessive direct costs for the company, they continue to raise the question of whether corners were being cut and thus create doubt about the formerly excellent and still very high OPMs generated by Subaru.

We remain negative on Subaru as we expect margins to remain under pressure and believe top line may stagnate or shrink over the next one to two years.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

RELATIVE PRICE SCORE – The Relative Price Score (RPS) measures stock price performance relative to TOPIX and is calculated by comparing the current deviation with the mean absolute deviation of monthly and daily relative share prices. As all companies are, as a result, on a comparable scale, ‘overbought’ and ‘oversold’ outliers and changes in scoring can reveal short-term and longer-term trading opportunities. This insight updates our list of overbought and oversold companies, reviews the best and worst performing companies by RPS over the last two months and adds some specific comments on stocks on each category.

RPS STATISTICS – The Company ‘outlier’ thresholds are set to “+4” for overbought and “-2” for oversold. Currently, of the 3,686 listed companies for which monthly data is available, 91 companies are ‘Overbought’, and 120 are ‘Oversold’ – 2.5% and 3.2%, respectively of the total. For companies with a market capitalisation of over ¥100b, there are 35 ‘Overbought’ and 24 ‘Oversold’ companies.

RPS ‘TOPS’ – In the last two years, 445 companies have achieved an RPS of ‘4’ or more. 80% have seen their RPS fall to below ‘4’ within the following two months. For companies with a market capitalisation higher than ¥100b, the numbers are 95 companies and 63% – demonstrating the superior persistence of large capitalisation companies in this regard. Some examples of RPS mean reversion in the last two months have been Descente (8114 JP), Ariake Japan (2815 JP), Fancl (4921 JP), Bandai Namco (7832 JP), Don Quijote (7532 JP), and Gmo Payment Gateway (3769 JP).

Source: Japan Analytics

RPS ‘BOTTOMS’ – 296 companies have seen their RPS fall to ‘-2’ or below in the last two years. 58% have seen their RPS recover to above ‘-2’ within three to six months. For larger capitalisation companies, the numbers are 72 companies and 67%. Some recent examples of positive RPS mean reversion in the last two months have been LINE Corp (3938 JP) – a ‘contrarians only’ selection in our last Insight, and Tokyo Electric Power (9501 JP).

Source: Japan Analytics

In the DETAIL section below we list the current very overbought (RPS>5), too late to buy (RPS >4<5) and oversold (RPS <-2) stocks as well as the largest two-month positive and negative changes in RPS.

Courts Asia Ltd (COURTS SP), a leading electrical, consumer electronics and furniture retailer in predominantly Singapore and Malaysia, has announced a voluntary conditional offer from Nojima Corp (7419 JP) at $0.205/share, a 34.9% premium to the last closing price.

The key condition to the Offer is the valid acceptances of 50% of shares out. Singapore Retail Group, with 73.8%, has given an irrevocable to tender. Once tendered, this offer will become unconditional.

CAL’s share price has endured a steady decline since touching $1.14 back in May 2015. It traded above the Offer price as recently as late-July 2018.

However, the controlling shareholder, which has maintained its stake since CAL’s listing in 2012, is cashing in. Nojima has stated it will exercise its right to compulsorily acquisition if acceptances reach 90%; and it does not intend to support any action or take steps to maintain the listing status of the company in the event its suspended due to free float requirements. I would look to cash out also. Consideration under the Offer may be remitted as early as the fourth week of Feb.

Wars in old times were made to get slaves. The modern implement of imposing slavery is debt. Ezra Pound

Governments used public sector balance sheets to bail out private financial institutions and assist private companies to emerge from bankruptcy in the GFC. These actions transferred credit risk from the private to the public sector, yet falling nominal interest rates minimised, and in some cases froze, the cost of servicing the mounting government debt until late 2016. Since then, many borrowers have paid rising interest rates on increasing amounts of debt. Debt service charges are rising faster than nominal GDP in a growing number of nations as a result. It is estimated that the US federal funding requirement will rise from minus US$ 700bn to US$ 2tr in 2022.

The supermarket sector is the most fragmented and uncompetitive of all retail sectors, a situation encouraged by major suppliers and not ideal for consumers.

Despite some effort from the likes of Aeon, consolidation has failed to materialise beyond a few in-group mergers.

Yet pressure on supermarkets to consolidate has been building due to depopulation in the regions, competitive pressures from other food retailers such as convenience stores and drugstore chains, as well as the emerging online food services.

Change is now coming. The biggest industry consolidation yet was announced last month, a precedent-setting alliance between three major supermarkets, Arcs Co Ltd (9948 JP), Valor Holdings (9956 JP) and Retail Partners (8167 JP), carving up a large chunk of the country into three regional fiefdoms.

Nidec has cut FY Mar-19 sales guidance by 9.4%, operating profit guidance by 25.6% and net profit guidance by 23.8% to reflect what management calls unexpectedly weak demand, the need for large inventory adjustments, and anticipated restructuring charges.

Management attributes this to U.S. – China trade friction, but weak demand for hard disc drives (HDDs) caused by excessive date center investment and falling NAND flash memory prices, and declining auto sales in both China and the U.S., appear to have compounded the problem.

Nidec’s share price was up ¥60 (+0.49%) today to ¥12,395, but the announcement was made after the market closed. Management plans to discuss the situation at a press conference starting at 18:30 Tokyo time today.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

A week ago, former Nissan Chief Performance Officer and onetime potential successor to Ghosn and/or Saikawa-san – Jose Munoz – who was put on leave to help Nissan deal with its internal investigation – resigned effective immediately. Some suggest this is the start of a bloodbath of Ghosn loyalists.

Former Nissan CEO and still-CEO at Renault Carlos Ghosn was in court to appeal the decision to not allow him bail. I expect that will end up at the Supreme Court in not too long, but for the moment he might stay in detention for another 7-8 weeks.

Nissan sources said (according to a Reuters report) earlier in the week they would be looking to file suit for damages against Ghosn.

Nissan and Mitsubishi officiallyannounced Friday that as a result of a joint investigation by Nissan and Mitsubishi Motors (7211 JP) into the Nissan-Mitsubishi Alliance entity (Nissan Mitsubishi BV), it was discovered that “Ghosn entered into a personal employment contract with NMBV and that under that contract he received a total of 7,822,206.12 euros (including tax) in compensation and other payments of NMBV funds. Despite the clear requirement that any decisions regarding director compensation and employment contracts specifying compensation must be approved by NMBV’s board of directors, Ghosn entered into the contract without any discussion with the other board members, Nissan CEO Hiroto Saikawa and Mitsubishi Motors CEO Osamu Masuko, to improperly receive the payments.” Saikawa and Masuko were not informed and did not also get paid by the company. The NMBV entity will attempt to recoup the funds from Ghosn. Nissan and Mitsubishi are thinking of dissolving their Dutch alliance entity.

The Nissan panel reviewing Nissan’s governance structure, made up of three independent directors and four external members, met for the first time Sunday. The proposals are due end-March, upon which the board will propose a new management system/structure for approval at the shareholder meeting at end-June 2019. The co-chair said in a comment after today’s meeting that Ghosn perhaps had questionable ethics.

French business newspaper Les Echos carried an “exclusive” interview with Nissan CEO Hiroto Saikawa which was reasonably enlightening, or should have been from a French point of view. In the interview, Saikawa is adamant that he fully supports the Renault-Nissan Alliance saying that it was not just important but “crucial” and he “would do nothing to render it harm”, and that the French state’s stake in Renault “posed no problem at all” because the “French state does not impose in any way on Nissan.” Saikawa-san also noted that he had no intention of ridding Nissan of French/foreign employees.

Renault Director Martin Vial visited Japan with French officials including Emmanuel Moulin – chief of staff to Bruno Le Maire, who is French Minister of the Economy – to meet with Hiroto Saikawa and Japanese officials Wednesday and Thursday. This trip was first reported by Le Figaro in the early hours of Wednesday morning (15 Jan) Asia time, and the point of the trip was reportedly to discuss the changes in governance at the top of Renault which might be coming – i.e. a new chairman as the French state and Renault’s independent directors appear to have decided that another two months of detention for Carlos Ghosn is enough to warrant a change even if they still presume his innocence in the charges brought in Japan. They were also to inquire after Ghosn’s case, though that seemed to have been secondary.

As a sidebar to this trip, Bruno Le Maire came out Wednesday saying that the State had asked the Renault board to hold a board meeting to replace Ghosn, and said that the French state would leave it to Renault’s directors to choose, but also came out and said that Cie Generale Des Etablissement MIchelin (ML FP) CEO Jean-Dominique Senard would be a great choice (though other suggestions are that he might take the role of Chairman as others note that Renault Interim CEO Thierry Bolloré’s role could be made permanent). His comments about Mr. Senard included those suggesting that Mr. Senard adheres to certain ideas of the “social responsibilities” of the company – ideas which Mr. Le Maire shares.

Mr Le Maire also said this week…

“Nous souhaitons la pérennité de l’alliance. La question des participations au sein de l’alliance n’est pas sur la table.”

Another quote from an article which came out Saturday night at midnight Paris time was similar.

“Un rééquilibrage actionnarial, une modification des participations croisées entre Renault et Nissan n’est pas sur la table”, déclare Bruno Le Maire. “Nous sommes attachés au bon fonctionnement de cette alliance qui fait sa force.”

Both quotes say “we” (the French state) seek for the Alliance to continue functioning in a stable manner and changes of the crossholding relationship or ownership rates between the companies were not on the table.

The second appears to be a quote from the Journal du Dimanche (article linked above) which was probably conducted a day or two earlier – and it makes a reference to it having been conducted just after his return from Tokyo (it was not revealed earlier this week that he had made the trip with Mssrs. Vial and Moulin so this is something of a question mark).

All of this was out by Friday. It was all very measured and reassuring.

Then Sunday saw a bombshell dropped… again…

In the Nikkei and Bloomberg, it was revealed that the French visitors to Tokyo had informed Japanese officials of their intention to have Renault appoint the next chairman of Nissan (as apparently the Alliance agreement allows) and of the French State’s intention to seek to integrate Nissan and Renault under the umbrella of a single holding company.

This is interesting for three reasons…

A holding company where the two companies stay listed does nothing that the Alliance does not do now except put a single board in place on top of both companies. That would be a Dutch Foundation structure. A holding company where one of the two companies loses its listing (because it is taken over) would require one of those companies lose a set of shareholders.

A Dutch Foundation (which is effectively the same thing if the two companies stay listed) was an idea which a year ago in the previous kerfuffle last spring about merging was “not an option acceptable to the government” (Les Echos, 7-Mar-18)

This is, once again, the French state seeking to intervene in the governance of Nissan. That’s a no-no according to the Alliance Agreement as modified in December 2015.

This is widely reported in English, Japanese, and French on Sunday.

There is a conciliatory article in Bloomberg with a headline suggesting a French official (Le Maire) downplayed the French comments about a holding company, but that refers to the JDD article, which is probably days old and repeated the same comment he made publicly earlier this week, reported by Les Echos and Le Figaro about a lack of change in cross-holding, but a careful read of the timeline suggests his comments were made in France before someone leaked this to the Nikkei.

Saikawa-san was reported to have said this morning (Monday 21 Jan 2019) that he had not heard about this, but that now was not the time to consider revising capital ties.

One should note, once again, that this is not the CEO or independent Chairman of Renault saying this. It is not the board or Nissan saying this. It is the French state.

What does this all mean? What are the possibilities and ramifications? Read on…

Tracking Traffic/Chinese Express & Logistics is the hub for our research on China’s express parcels and logistics sectors. Tracking Traffic/Chinese Express & Logistics features analysis of monthly Chinese express and logistics data, notes from our conversations with industry players, and links to company and thematic notes.

This month’s issue covers the following topics:

December express parcel pricing fell by over 9% Y/Y. Average pricing per express parcel fell by 9.1% Y/Y, the worst decline since Q216 (excluding January/February figures distorted by the Lunar New Year holiday).

Express parcel revenue growth remained well below 20% last month. Weak pricing dragged sector revenue growth down to 17% in December, the 4th consecutive month of sub-20% growth.

Intra-city pricing (ie, local delivery) was strong in 2018. Relative to weak inter-city pricing (down 3.1% Y/Y in 2018), pricing for intra-city express shipments was firm, rising by 0.1% last year. In fact, average pricing for intra-city express shipments has risen in four of the last five years.

Underlying domestic transport demand remained firm in December. Although demand for inter-city express shipments appears to be moderating (from high levels), underlying transportation activity in December remained firm. The three modes of freight transport we track (rail, highway, air) in aggregate rose 6.6% Y/Y in December, even as the growth of air freight slowed.

We retain a negative view of China’s express industry’s fundamentals: demand growth is slowing and pricing for inter-city shipments appears to be falling faster than costs can be cut, leading to margin compression.

The recent negative sales in the Chinese auto industry and Nissan’s case of Carlos Ghosn removal could put additional pressure on the already thin margin of auto supplier industry. One of the Carlos Ghosn early contribution to Nissan was to cut cost and outsource the auto parts maker to a wide variety of suppliers including to Hanon Systems (018880 KS) . Nissan’s new management may want to undo some of Carlos Ghosn’ legacy including changing the selection criteria of parts supplier.

Hanon’s global peers also experienced a decrease in the inventory turnover and most of them have been priced at PER <10 but Hanon is still trading at 24x PER while its sales growth and profitability is still in low single digit? Facing the onset of the slowdown in the Chinese auto industry, won’t it be another headwind for Hanon Systems?

“I’ve been a manager for almost half a century, but this is the first time I’ve seen such a large single-month drop in orders for us. What we witnessed in November and December was just extraordinary.”

Nidec CEO – Shigenobu Nagamori

Source: Japan Analytics

BEAR MARKET RALLY ON CUE – The bear market rally we envisaged has seen the Market Composite recover by nearly 5% this year and 10% from the Christmas Day low of ¥533t. Seven of the last nine trading days have been ‘up’, and the Bank of Japan dutifully intervened on one of the two ‘down’ days – January 16th. The US dollar has also retraced three-quarters of the ¥6.5 decline from December 26th to January as concerns over US-China relations temporarily subsided.

Source: Japan Analytics

5D RSI @75 –The 5-day Relative Strength Index is now at a level that suggests the bulk of this initial move is complete, and a consolidation can be expected in the weeks ahead as the majority of third-quarter earnings are released – particularly if, as we discuss further below, Nidec (6594 JP) has set a trend.

Source: Japan Analytics

VALUE TRADED RATIO – After reaching a three-month high of 64bps on 21st December, the Value Traded Ratio (value traded/total market value) has returned to below-trend levels for the last two days – another indicator of a coming pause in the uptrend.

Source: Japan Analytics

% ABOVE MOVING AVERAGE – The percentage of stocks trading above a weighted sum of five periods of moving averages has recovered to above ’20’ as measured by market value, although the stock count percentage is still below that level. We expect the pattern of 2016 to be replayed here, which suggests an ultimate ‘low’ in the summer of 2019.

Source: Japan Analytics

TORAKU > 80 – On a further positive note, on Friday the 25-day Toraku advance-decline indicator finally recovered to above the ’80’ level, indicating that the December 25th ‘low’ is unlikely to be breached in the short term.

Source: Japan Analytics

THE NIDEC CANARY – Despite the market’s nonchalant reaction to Nidec’s downward revision, the company’s revised forecasts have broader implications. For the first time since March 2017, forecasts for our Market Composite for Operating Income are now lower than the trailing-twelve-month (TTM) Operating Income. Also, the ‘gap’ between forecast Net Income and TTM Net Income is now ¥2.9t – the largest such gap in over ten years. Mr. Market is suggesting that Japanese corporate profits are due to fall by 18% on average, to the level last reached in the first quarter of 2017 – implying bottom-line declines of up to 50% for some key ‘global’ sectors such as Autos, Machinery, Chemicals, Electrical Equipment and Technology Hardware, which together comprise one-third of aggregate Net Income.

Source: Japan Analytics

Note: The Results & Revision Score is the average of our Results Score and Forecasts/Revision Score for each company. Both scores are cap-weighted and have a maximum of +30 and a minimum of -30 for each period. The Results Score is calculated quarterly, using the most recent eight quarters of company data for revenues, operating income and operating margin and measures the rate, degree and consistency of change for each metric. The Forecast/Revision Score is based on Annual and Interim period company forecasts and compares changes from previous forecasts as well as against the trailing twelve-month (TTM) or previous first-half results, with annual forecasts being double-weighted.

LEADING OR LAGGING? – Our cap-weighted Results & Revision Score bottomed at -2.55 in December 2016 and reached a two-decade high on 16th November 2017, two months before the market peak in January 2018. Since October last year, the market has been leading on the downside. If we are to repeat the relatively-mild cyclical downturn of 2016, the Results & Revision Score will turn negative at the time of the full-year results and forecasts for the new fiscal year, which, for the majority of companies, will be released in May. We expect the market to retest the lows of April 2017 and December 2018 around that time.

OUTLOOK & RECOMMENDATIONS

We continue to recommend an underweight position in Japan in global portfolios.

The equity market decline at the end of last year was well in advance of the underlying trends in the economy and corporate profits; the recent 10% rally has corrected that imbalance. Nevertheless, the global cycle has turned down sharply, and many economies will be in a recession by the end of this quarter.

The Japanese economy is still enjoying a robust domestically-driven growth cycle and is close to full employment. As Nidec and Yaskawa Electric have demonstrated and as other companies will soon confirm, Japan’s globally-orientated manufacturing companies are not immune to global trends. Although some of the coming downturn in earnings has been well-discounted, our Results & Revision Score has yet to turn negative. Accordingly, we expect the market to retest the December 2018 low, probably in May when the FY2020 forecasts are announced.

In the near term, we continue to favour undervalued domestically-orientated companies in the Information Technology, Internet, Media and Telecommunications sectors.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Since our bearish Insight on Tokyo Kiraboshi Financial Group (7173 JP) issued in November 2018, Tokyo Kiraboshi FG (7173 JP): Shooting Star, the stock’s subsequent performance has fully justified our pessimism, with the share price finishing CY2018 down 47.7% year-on-year (YoY). Having touched a low of ¥1,504 on Christmas Day, the shares have recovered 10.1% to ¥1,656 as of Friday’s close: slightly better than the Topix Bank Index, which closed on Friday at 154.44, up 9.0% over the same period. Trading on a forward-looking price/earnings multiple of 12.5x (using the bank’s current FY3/2019 guidance) and a price/book ratio of 0.21x, TKFG looks cheap. This is deceptive. Adjusting the group’s earnings per share (EPS) for the ¥55 billion (US$507 million) in two still-outstanding preference share issues pushes the PER to over 18x: hardly a bargain. Meanwhile, the group’s RoA and RoE ratios are woefully low, loan growth has collapsed since end-March 2018, deposits have fallen alarmingly, and main bank subsidiary Kiraboshi Bank is struggling to keep its net return on funds deployed (NRFD) in positive territory. A stock best avoided.

After 6.5bn+ shares came off lockup last week (by Travis Lundy’s estimate), Xiaomi made a placement equal to about 1% of shares outstanding at a sharp discount to the close. This follows a block of 120mm shares last Thursday at HK$8.80 (at a 13+% discount); Apoletto reported a distribution (sale) of 594+mm shares on January 9th to reduce their total position across all funds from 9.25% to 4.99%; and there was a block placement launched earlier in the week for 231mm shares for sale between HK$9.28 and HK$9.60.

While as much as 1bn shares may have already transacted (assuming most of the 594mm shares distributed by Apoletto have been sold in the market), there were ~6.5 billion shares which could be sold and an additional 1bn+ of additional conversions designed to be sold.

In another 6 months, there will be another 4bn+ shares which come off LockUp. In total, that is up to 10-11bn shares coming off lockup between a week ago and 6 months from now. That is four times the total IPO size, and 70-80% of the total position coming off lock-up has an average in-price of HK$2.00 or less. Apoletto’s average in-price was HK$9.72.

Travis is also skeptical that the company’s capital deserves a premium to peers, and is not entirely convinced that the pre-IPO profit forecasts are going to be met in the medium-term. In the meantime, a lot of the current capital structure base is looking to get out.

Nota Bene: Bloomberg’s 3bn-shares-to-come-off-lockup number was confirmed by Travis (the day he published the piece linked below) with the people who tallied the info for the CACS function. They had neglected to count a certain group of shareholders. The actual number will be well north of 6 billion shares.

After the close of trading on the 15 January, NTT announced it had repurchased 3.395mm shares for ¥15.349bn in the first 7 trading days of the month, purchasing 10.9% of the volume traded. This announcement was bang in line with Travis’ insight the prior day, where he anticipated the buybacks would soon be done.

The push to buy shares on-market at NTT vs off-market at NTT Docomo has had some effect but not a huge effect. The NTT/Docomo price ratio is a bit more than 5% off its late October 2018 lows prior to the “Docomo Shock”, but the ratio is off highs. Off the lows, the Stub Trade has done really well.

NTT DoCoMo bought back ¥600bn of shares from NTT at the end of 2018. That means NTT DoCoMo could buy back perhaps ¥300-400bn of shares from the market over the next year or so before ‘feeling the need’ to buy back shares from NTT again. NTT will likely buy back at least ¥160bn of NTT shares from the government in FY19 starting April 1st, which means there will be room to buy back another ¥100bn from the government before not having any more room to do so.

There could be an NTT buyback from the market in FY2019, and one should expect that for the company to buy back shares from the government again, if NTT follows the pattern shown to date, there should be another ¥400-500bn of buybacks from the market over the next two years, and if EPS threatens a further fall on NTT DoCoMo earnings weakness, NTT might boost the buyback to make up for that.

The very large sale by NTT of NTT Docomo shares this past December will free up a significant amount of Distributable Capital Surplus.

On a three-year basis, Travis would rather own NTT than NTT Docomo. But he expects the drift on the ratio will not be overwhelming unless NTT does “something significant”.

Singaporean real-estate group Capitaland has entered into a SPA to buy Ascendas-Singbridge (ASB) from its controlling shareholder, Temasek. The proposed acquisition values ASB at an enterprise value of S$10.9bn and equity value of S$6.0bn. Capitaland will fund the acquisition through 50% cash and 50% in shares (862.3mn shares @$3.25/share – ~17% dilution). Capitaland-ASB will have a pro-forma AUM of S$116bn, making it the largest real estate investment manager in Asia and the ninth largest global real estate manager.

Hitachi Ltd (6501 JP)announced it had received approvals from the relevant government authorities, and its Tender Offer for Yungtay (at TWD 60/share) has now launched. The Tender Offer will go through March 7th 2019 with the target of reaching 100% ownership. Son of the founder, former CEO, and Honorary Chairman Hsu Tso-Li (Chou-Li) of Yungtay has agreed to tender his 4.27% holding. The main difference between the offer details as discussed in Going Up! Hitachi Tender for Yungtay Engineering (1507 TT) back in October, is a minimum threshold for success of reaching just over one-third of the shares outstanding, with a minimum to buy of 88,504,328 shares (21.66%, including the 4.27% to be tendered by Hsu Tso-Li).

This deal looks pretty straightforward, but the stock has been trading reasonably tight to terms, with annualized spreads on a reasonable expectation of closing date in the 3.5-4.5% annualized range for a decent part of December, rising into early January before seeing a jump in price and drop in annualized on the second trading day of the year. This shows some expectation of a fight and a bump.

To avoid that fight and bump – the Baojia Group, which supported Hsu Tso-Ming’s board revolt last summer (discussed in the previous insight), has reportedly accumulated a 10% stake – Hitachi has lowered its minimum threshold to complete the deal to get to one-third plus a share. Given that it controls 11.7% itself as the largest shareholder, and has another 4.3% from the chairman in the bag, that means it needs about 17.3% of the remaining 84% to be successful.

Because the minimum is only about 21% of the float, this deal has quite decent odds of getting up unless someone makes a more serious run for it. As an arb, Travis sees a small chance of a bump because of some potential harassment value by Hsu Tso-Ming’s friends at Baojia Group. Hitachi has already taken that into account with the lowering of the minimum, but it is possible that enough noise can be created to obtain a bump.

Courts, a leading electrical, consumer electronics and furniture retailer predominantly in Singapore and Malaysia, has announced a voluntary conditional offer from Japanese big box electronics retailer Nojima Corp (7419 JP) at $0.205/share, a 34.9% premium to the last closing price. The key condition to the Offer is the valid acceptances of 50% of shares out. Singapore Retail Group, with 73.8%, has given an irrevocable to tender. Once tendered, this offer will become unconditional. The question is whether minorities should hold on.

Barings/Topaz-controlled Singapore Retail Group are exiting, having not altered their shareholding since CAL’s 2012 listing. If Nojima receives acceptances from 90% of shareholders, it will move to compulsory delisting of the shares. If the Offer closes with Nojima holding >75% of shares, it could still launch an exit/delisting offer pursuant to Rule 1307 and Rule 1308.

Long-suffering shareholders may wish to hold on for a potential turnaround should Nojima extract expected synergies. But this looks like a decent opportunity (of sorts) to also exit along with the controlling shareholder.

The board of Navitas, a global education provider, has unanimously backed a revised bid by 18.4% shareholder BGH Consortium of A$5.825/share, 6% higher than its previous rejected offer and a 34% premium to undisturbed price.

The revised proposal drops the “lock out” conditions attached to BGH Consortium’s previous offer, enabling BGH to support a superior proposal. BGH has also been granted an exclusivity period until the 18 Feb.

Panalpina Welttransport announced that it had received an unsolicited, non-binding proposal from DSV A/S (DSV DC) to acquire the company at a price of CHF 170 per share, consisting of 1.58 DSV shares and CHF 55 in cash for each Panalpina share. The offer comes at a premium of 24% to Panalpina’s closing share price of CHF 137.5 as of 11 January 2019 and 31% to the 60-day VWAP of CHF 129.5 as of 11 January 2019. Following the announcement, Panalpina’s shares surged above the terms of the offer implying that the market was anticipating a higher bid from DSV or one of its competitors.

Investors lashed out at Panalpina’s board last year (after years of griping by some of the top holders), eventually forcing the main shareholder to support the installation of a new chairman of the board.

The stock is clearly in play. And the sector is seeing ongoing consolidation. DSV’s approach to Panalpina comes just months after it failed in an attempt to buy Switzerland’sCeva Logistics AG (CEVA SW). Media reports suggested Switzerland’s Kuehne & Nagel are also rumoured to be considering an offer for Panalpina.

Panalpina’s largest shareholder, Ernst Goehner Foundation, owns a stake of approximately 46%. If EGS wants to see OPMs up at global standards level – in the area of DSV and KNIN – then they may need to see someone else manage the assets. If EGS is steadfastly against Panalpina losing its independence, a deal will not get done. That said, if a deal does not get done because the board reflects the interest of EGS, that proves the board is not as independent as previously claimed. But one must imagine there is a right price for everything.

Earlier this month, Bristol Myers Squibb Co (BMY US)and Celgene announced a definitive agreement for BMY to acquire Celgene in a $74bn cash and stock deal. The headline price of $102.43 per Celgene share plus one CVR (contingent value right) is a 53.7% premium to CELG’s closing price of $66.64 on January 2, 2019, before assigning any value to the CVR. The CVR has a binary outcome: it will either be worth zero or will be worth a $9 cash payment upon the FDA approval of three drugs.

While there don’t appear to be any major problems in commercial products, it remains to be seen whether the antitrust authorities go further into the pipeline to determine whether potential competition from drugs still in clinical trials could present issues in the future.

Overall, the merger agreement appears fairly standard, but it does (also) require BMY shareholder approval which typically overlays a higher risk premium. For John DeMasi, the attraction for this arb is the current risk/reward.

ANTYA Investments Inc. chimes in on the deal and considers it unlikely that a suitor for CELG emerges at a higher price, whereas rumours of suitors for BMY abound, and would therefore make a long bet on BMY.

On the 10 January, PAH announced CKI had entered into a placing agreement to sell 43.8mn shares (2.05% of shares out) at HK$52.93/share (a 4.7% discount to last close), reducing CKI’s holding in PAH to 35.96%. This is CKI’s first stake sale in PAH since the 2015 restructuring of the Li Ka Shing group of companies, and it has been over three years since the CKI/PAH scheme merger was blocked by minority shareholders. It is also around two months since FIRB blocked CKI/PAH/CKA/CKHH in its scheme offer for APA Group (APA AU).

I don’t see a sale of PAH as being a realistic outcome – this is more likely an opportunity to take some money (the placement is just US$328mn) off the table. CKI remains intertwined with PAH via their utility JVs in Australia, Europe and UK, and in most investments, together they have absolute control.

I would also not discount a merger re-load. The pushback in 2015 was that the (revised) merger ratio of 1.066x (PAH/CKI) was too low and took advantage of CKI’s outperformance prior to the announcement. That ratio is now around 0.9x. A relaunched deal at ~1x would probably get up – the average since the deal-break is 1.02x and the 12-month average is 0.95x. And a merger ratio at these levels would ensure Ck Hutchison Holdings (1 HK)‘s holding into the merged entity would be <50%, so it would not be required to consolidate. This recent sell-down does not, however, elevate the near-term chances of a renewed merger.

The takeaway is that the stub is very choppy, it often (but not always) widens after the full-year results, and the highest implied stub/EBITDA occurred outside of FY16, its most profitable year. The downward trend since January last year reflects the anticipated ~17% decline in EBITDA for FY18 to ₩148bn, its lowest level in the past four years.

Sanghyun mentioned that there are signs of improving fundamentals for local cosmetics stocks (as reflected in CapIQ) and that Holdcos have traditionally been more susceptible to fundamental changes. This should augur a shift to the upside in the implied stub.

I see the discount to NAV at 27%, right on the 2STD line and compares to a 12-month average of 3%. This looks like an interesting set-up level.

The Offer for Selangor Properties (SPR MK)has been bumped again, to RM6.30 from RM6.00. The original Offer was pitched at RM5.70/share. This latest proposal is a 55% premium to the undisturbed price and 10% above the initial bid. This is starting to look reasonable, at 0.89x P/B. On balance, this will probably now get up. (link to my earlier insight: Selangor Props – Privatisation Offer Does Not Reflect Full Value)

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Trawling through >1500 global banks, based on the last quarter of reported Balance Sheets, we apply the discipline of the PH Score™ , a value-quality fundamental momentum screen, plus a low RSI screen, and a low Franchise Valuation (FV) screen to deliver our latest rankings for global banks.

While not all of top decile 1 scores are a buy – some are value traps while others maybe somewhat small and obscure and traded sparsely- the bottom decile names should awaken caution. We would be hard pressed to recommend some of the more popular and fashionable names from the bottom decile. Names such as ICICI Bank Ltd (ICICIBC IN) , Credicorp of Peru, Bank Central Asia (BBCA IJ) and Itau Unibanco Holding Sa (ITUB US) are EM favourites. Their share prices have performed well for an extended period and thus carry valuation risk. They represent pricey quality in some cases. They are not priced for disappointment but rather for hope. Are the constituents of the bottom decile not fertile grounds for short sellers?

Why pay top dollar for a bank franchise given risks related to domestic (let alone global) politics and the economy? Some investors and analysts have expressed “inspiration” for developments in Brazil and Argentina. But Brazilian bonds are now trading as if the country is Investment Grade again. (This is relevant for banks especially). Guedes and co. may deliver on pension/social security reform. If so, prices will become even more inflated. But what happens if they don’t deliver on reform? Why pay top dollar for hope given the ramp up in prices already? Argentina is an even more fragile “hope narrative”. More of a “Hope take 2”. Similar to Brazil, bank Franchise Valuations are elevated. While the current account adjustment and easing inflation are to be expected, the political and social scene will be a challenge. LATAM seems to be “hot” again with investment bankers talking of resilience. But resilience is different from valuation. Banks from Chile, Peru, and Colombia feature in the bottom decile too. If an investor wants to be in these markets and desires bank exposure, surely it makes sense to look for the best value on offer. Grupo Aval Acciones y Valores (AVAL CB) may represent one such opportunity.

Our bottom decile rankings feature a great deal of banks from Indonesia. In a promising market such as Indonesia, given bank valuations, one needs to tread extremely carefully to not end up paying over the odds, to not pay for extrapolation. In addition, India is a susceptible jurisdiction for any bank operating there – no bank is “superhuman” and especially not at the prices on offer for the popular private sector “winners”. Saudi Arabia is another market that suddenly became popular last year. We are mindful of valuations and FX.

Does it not make more sense to look at opportunity in the top decile? While some of the names here will be too small or illiquid (mea culpa), there are genuine portfolio candidates. South Korea stands out in the rankings. Woori Bank (WF US) is top of the rankings after a share price plunge related to a stock overhang but this will pass. Hana Financial (086790 KS) , Industrial Bank of Korea (IBK LX) and DGB Financial Group (139130 KS) are portfolio candidates. Elsewhere, Russia and Vietnam rightly feature while Sri Lanka and Pakistan contribute some names despite very real political and macro risks. We would caution on some of the relatively small Chinese names but recommend the big 4 versus EM peers – they are not expensive. In fact some of the big 4 feature in decile 2 of our rankings. There are many Japanese banks here too. And many, like some Chinese lenders, are cheap for a reason. While the technical picture for Japanese banks is bearish, at some stage selective weeding out of opportunity within Japan’s banking sector may be rewarding. The megabanks are certainly not dear. Europe is another matter. Despite valuations, we are cautious on French lenders and on German consolidation narratives – did a merger of 2 weak banks ever deliver shareholder value? The inclusion of two Romanian banks in the top decile is somewhat of a headscratcher. These are perfectly investable opportunities but share prices have been poor of late.

Mitsubishi has finally given up its hope of convincing Aeon to merge Ministop (9946 JP) with Lawson and is selling its stake in the largest retail group.

There will be no change to the extensive supply relationship between the two companies and Mitsubishi’s food wholesale arm, Mitsubishi Shokuhin (7451 JP).

While Aeon seems to have spurned Mitsubishi for now, it is hard to see how Aeon will progress in the convenience store sector without Mitsubishi’s help. In the short-term Ministop looks like a poor investment but Aeon may have to sell to Mitsubishi eventually and will want a good price for it.

Highlights of significant recent happenings include:

Substantive Deep Dive – Canada’s BlackBerry Ltd (BB CN) seeks to be the go-to provider of web Security: Why we believe investors should look at Blackberry as a way to hedge their exposures to the increasing list of companies who are susceptible to adverse impact from security breaches.

Feeding the Dragon – Chinese buying of US firms brakes abruptly, obliterating the long-term trend, and now Japan has become the second-largest market for outbound M&A globally. Also, South Korean food giant Cj Cheiljedang (097950 KS) is continuing its aggressive expansion into the U.S. market

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Average monthly savings rates and total savings stocks have long been high in Japan, but savings rates broke all records in June 2018.

In one sense, this was a sign that the government’s six-year effort to increase wages – and thus consumption and inflation – was finally bearing fruit, albeit small not very sweet fruit.

However, anxiety about the future, coupled with a lack of incentive to spend, meant that most of the increases in wages and bonuses stayed in the bank.

At the same time, while the majority hoarded, brands and retailers at both the luxury and discount ends of the market are reporting a record year, and discount retailers, in particular, are worthy long-term investments.

This demonstrates the further polarisation of the retail market but inventive marketing and solid cost performance will still unlock those wallets in premium mass markets too.

MUFG initially bought 19.9 percent of Bank Danamon from Singapore state investor Temasek Holdings 15.875 trillion rupiah ($1.17 billion), then valuing the Indonesian lender at around $6 billion.

Step 2 saw the OJK give the OK (BDMN announcement in English) for MUFG to up its holding to 40% – the statutory maximum under the prevailing OJK regulation No.56/POJK 03/2016 – and the Indonesian Financial Services Authority (OJK), seemingly granted permission for MUFG to go above 40% in Bank Danamon when OJK deputy commissioner for banking, Heru Kristyana, wrote in a message to a Reuters journalist (article here) on August 3rd last year “They (MUFG) can have a larger stake than 40 percent once the merger (with Bank Nusantara) has gone through and as long as they meet provisions and requirements.”

As Johannes Salim, CFA pointed out in his interesting insight Bank Danamon: Fundamentals Revisited Plus Thoughts on M&A in March last year, the revised OJK regulation No.56/POJK 03/2016 placed the authority for determining whether or not a foreign acquiror could go above 40% squarely on the OJK – no BI approval would be necessary.

Indonesia has a “Single Presence Policy” (OJK Regulation No. 39/2017) which requires that a foreign owner may not hold more than one control stake in a bank. In order to get to Step 3 which would be to acquire the remaining 33.8% of Danamon from Temasek affiliates (Asia Financial Indonesia and its affiliates), MUFG would need to merge its presence in Bank Nusantara Parahyangan (BBNP IJ) (also known as “BNP”) where it holds more than three-quarters of the shares (and has controlled since 2007) with Danamon.

The New News

This morning’s paper carried a giant notice in bahasa announcing the planned merger between BDMN and BNP with shareholder vote for both banks 26 March 2019 (record date 1 March) and effective date 1 May 2019. The Boards of Directors and Boards of Commissioners of each bank

“view that this Merger will increase the value of the company because it is a positive move for stakeholders, including the shareholders of Bank Danamon,” and

“have proposed to their shareholders to agree with the resolution on the proposed Merger in each of their respective GMS.”

Indonesian takeover procedures generally require a Mandatory Takeover Offer procedure when someone goes over a 50% holding. But banks being bought by foreigners are a different category and bank takeovers are regulated by the OJK. In addition, the structure of such takeovers creates short-term options (for holders) and possibly longer-term obligations for the acquiror which are a little unusual, but provide for a very interesting opportunity in this case.

The start of the year has been bullish on the Korean and Japanese stock markets. KOSPI is up 4% and Nikkei is up 3% YTD. Some of the most beaten down stocks in the last 3 months of 2018 in Korea and Japan have been rebounding nicely YTD. In the past week, the following reports that are relevant for Japan and Korea have received a lot of interest:

Finally, it was announced that Trump plans to meet North Korea’s Kim Jong-Un in late February in Vietnam. It has been nearly seven months since their last meeting in Singapore and there has been no progress in terms of nuclear weapons inspection or dismantling of its nuclear weapons and ICBM missiles. In April 2009, North Korea reactivated its nuclear facilities, after more than two years of North Korea promising to not to restart its nuclear programs. They lied and got away with it. And it seems like they are replaying this story-line once again.

Last week on 17 January, printing and HR services company and funeral parlor operator Kosaido Co Ltd (7868 JP)announced that Bain Capital Private Equity would conduct an MBO on its shares via Tender Offer, with a minimum threshold for success of acquiring 66.67% of the shares outstanding. The Tender Offer commenced on 18 January and goes through 1 Mach 2019. The Tender Offer Price is ¥610/share, which is a 43.8% premium to the close of the day before the announcement and a 59.7% premium to the one-month VWAP up through the day before the announcement.

The company’s board of directors announced it supported the deal.

Terms & Schedule

Terms & Schedule of Hitachi Tender Offer for Yungtay Engineering

Tender Offer Price

JPY 610

Tender Offer Start Date

18 January 2019

Tender Offer Close Date

1 March 2019

Tender Agent

SMBC Securities

Maximum Shares To Buy

24,913,439 shares

MINIMUM Shares To Buy

16,609,000 shares

Currently Owned Shares

100 shares

Irrevocable Undertakings

Sawada Holdings’ 3,088,500 shares or 12.40% (includes the holdings at both Sawada Holdings and HS Securities).

This deal is probably reasonably straightforward.

It is a big premium to last trade, and a multi-year high.

There is one large holder publicly willing to sell and I expect the cross-holders would be willing to sell too.

Management is involved and supportive.

Except it is being done (and recommended) at a 44% discount to Tangible Book Value Per Share after the directors managed to work Bain up from a 49% discount to TBVPS.

Meanwhile, Descente has brought in Wacoal (3591 JP) as a white knight and made a splash in the business media about its recent success.

Itochu insists that Descente needs Itochu’s management skills, particularly to build a stronger business in China and other overseas markets, and says the only way to make Descente listen is to buy more stock – more than its current nearly 30%.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

China Meidong Auto (1268 HK) has been on a rollercoaster ride in 2018. The stock price of Meidong started 2018 around 2.7 HKD and recently has been trading around 2.9 HKD.

Nice and steady ride? Not exactly, as it has swung from 4.3 HKD in June to 2.6 HKD in August. After analyzing how NPAT estimates evolved over the past year there should be no justifications for these wild swings.

Meidong is likely to report solid FY18 results by late March vs industry peers which are expected to report a weak 2H18. While BMW dealers have been reportedly suffering in China during 2018, Meidong was fortunate to have other luxury brands pick up the slack.

FY19 should be another growth year for Meidong as 1) recently acquired BMW showrooms contribute their maiden results and 2) other luxury brands continue to perform despite overall doom and gloom in the Chinese auto market. Should the Chinese government launch car replacement stimulus measures this would be icing on the cake.

Fair Value lowered slightly from 4.7 HKD to 4.4 HKD (10x 2019E) on lower 2019 profit estimates, which leaves 52% upside excluding dividends.

The shares are very cheap. They trade at 0.9x book but there is some Y22bn in unrealised profit on land/buildings (vs. the market cap of Y46bn). If adjusted for this, the shares are less that half book. Meanwhile the dividend has been steadily increasing (both payout ratio and in absolute terms). To 11/19 the payout ratio will be 23% and the dividend will rise to Y37 from Y30 last year. At today’s price of Y950, the yield is thus 3.9%. And the shares trade on multiple of 6x. They rose significantly last year on the back of Morgan Stanley BUY note (from Y800 to Y1,500) but with the market’s correction and the tightening of bank lending to individuals (which has no impact on them), the shares have fallen back to Y950. For those looking for a cheap domestic small cap name, this is worth looking at.

Japan’s B2C e-commerce industry is growing sales volumes close to 10% YoY each year, but the level of online activity remains behind other developed markets. Globally, e-commerce volumes are growing around 20% per year. The Japanese government does not want Japan to be left behind and wishes to see more domestic e-commerce activity as well as strong growth in cross-border e-commerce.

Domestic giants Rakuten (4755 JP) and Yahoo Japan (4689 JP) are growing faster than the overall market. So is global powerhouse Amazon.com (AMZN US) in Japan. Together the three represent nearly half of the market today, up from 40% 4 years ago.

Both Rakuten (4755 JP) and Yahoo Japan (4689 JP) have seen profit margins squeezed in recent years, most notably by increasing competition, including from profit insensitive Amazon Japan. We believe e-commerce profit margins will remain under pressure and note managements’ efforts to diversify.

The upcoming earnings season will provide a once-a-year window into Japan’s e-commerce industry. Amazon.com (AMZN US) will announce its full year results on 31 January 2019, and the company’s filings include annual sales figures for its Japan operations.

13 months ago, real estate operator TOC Co Ltd (8841 JP) – known for decades in Tokyo as the owner/operator of the largest single building in Tokyo by floor space – launched a Tender Offer to buy up to 20mm shares or 16.4% of the shares outstanding. Effissimo, Mizuho Bank, Mitsubishi UFJ Bank, and Mitsui Sumitomo Bank had each apparently approached the company indicating they were interested in selling.

The Tender Offer resulted in Effissimo selling 17,916,900 shares, leaving them with 4.599mm shares. Combined, other parties sold 800,000 shares.

On the 21st of March 2018, TOC announced it would cancel 33 million shares out (they already had ~14mm shares of Treasury stock prior to launching the Tender Offer). Later they launched another buyback program and the company has 1.847mm shares of Treasury stock as of now, out of 103.88mm shares outstanding.

Yesterday after the close, the company announced a ToSTNeT-3 Buyback this morning, to buy up to 4.6 million shares or 4.49% of shares outstanding at ¥778/share.

That makes the previous argument stronger, not weaker.

To not reinvent the wheel, the second insight is the one with the deep dive information about the company and its assets.

The globe is facing more than an ordinary business cycle.

Joseph C. Sternberg, editorial-page editor and European political-economy columnist for the Wall Street Journal’s European edition, recently interviewed Claudio Borio, head of the Monetaryand Economic Department of the BIS. Mr. Borio said that politicians have relied far too much on central banks, which are constrained by economic theories that offer little meaningful guidance on how to sustain growth and financial stability. The only tool they have is an interest rate that can affect output in the short run but ends up affecting only inflation in the end.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Toppan Printing (7911 JP) is looking to sell 10.5m shares in Recruit Holdings (6098 JP) for about US$263m. Post-placement, Toppan Printing will still have about 6% stake (103m shares) in Recruit Holdings.

The deal scores well on our framework owing to its strong price and earnings momentum and stellar track record. However, it was offset by its relatively expensive valuation compared to peers. The selldown by Toppan Printing is tiny relative to the three-month ADV which the market would likely be able to absorb. The sell down is also long overdue considering that Toppan Printing skipped the 2016 secondary offering in which many shareholders have participated.

In this report, we provide an analysis of our pair trade idea between Amorepacific Group (002790 KS) and Shiseido Co Ltd (4911 JP). Our strategy will be to long Amorepacific Group (APG) and short Shiseido. As mentioned in our report, Korean Stubs Biweekly Sigma σ (#1): The Inaugural Edition, our base case strategy is to achieve gains of 8-10% on this pair trade. Our risk control is to close the trade if it generates 4-5% in combined losses. Cost of commissions are not included in the calculations and closing prices as of January 23rd are used in our pair trade. [Long APG – $0.5 million; Short Shiseido – $0.5 million for total of $1.0 million].

The following are the major catalysts that could boost APG shares higher than Shiseido shares within the next six to twelve months:

Amorepacific Group shares are extremely oversold and forming a base

THAAD is no longer an issue

Amorepacific Group’s NAV discount

Attractive relative valuations

Amorepacific’s new headquarters building distraction out of the way

Chinese tourists are coming back to Korea & slower growth rate of visitors to Japan

A very normal part of the semiconductor cycle is inventory clearance. DRAM makers are starting to discuss this in their earnings calls. What they are NOT telling their investors is how significant this is to the onset of a price collapse, perhaps because they don’t understand it themselves. This Insight will help readers to learn how and why an inventory clearance helps ratchet a budding oversupply into a full-blown glut.

On 21 January 2019, my favorite manufacturer of garbage trucks, vertical carousel parking infrastructure, sea planes, and jetways – Shinmaywa Industries (7224 JP) – announced a share buyback. This was not unusual. The company bought back shares last year and indicated earlier this year it would seek a relatively high return of capital to shareholders. In the last five months of 2018, the company bought back 3.6% of shares outstanding, and cancelled those shares at the end of December 2018).

Indeed, the company on January 9th this year announced a revised dividend forecast for the year ending March 2019. The dividend was lifted by 1 yen.

The company also announced a new policy of shareholder returns for the year starting April 1.