Our overall global outlook remains cautious and continued downward pressure on global equities remains our expectation. One bright spot is EM (more on this below), which continues to give us hope that global equities can bottom out. We provide a technical appraisal of major markets and highlight actionable setups within the global Utilities and Staples Sectors.

Tosei (8923) BUY – a very cheap small cap real estate developer

Hikari Tsushin (9435) BUY – 25% off recent highs, this is essentially a stock business that will continue to add to its installed base and grow profits.

Don Quijote (7532) BUY – oversold on the failure of FamilyMart bid and poor December sales.

Next week promises to be a large catalyst driven week, with Apple Inc (AAPL US), NTT Docomo Inc (9437 JP) and Tesla Motors (TSLA US) expected to report results, among others. We have provided a list below of the key equity catalysts for next week as well as potential drivers for M&A deals and stubs. If you are interested in importing this directly into Outlook or have any further requests, please let us know.

On the back of a growing LNG global trade volume, LNG producers have outperformed the US market and their E&P peers including the oil majors over the last two years. As global LNG production reaches a record 316m tonnes in 2018, a 9.6% increase year on year, new capacity additions set to come online in the next three years will be dominated by the US. This insight will examine how the recent entry of US LNG in the market is transforming the LNG industry and which emerging players are driving the change.

Exhibit 1: LNG Producers Outperform the US Market

Source: Capital IQ. Prices as of 22 of January. Un-weighted indexed composites. Oil Majors: Exxon, Chevron, Shell, BP, Total and ENI. Australia LNG: Woodside Energy, Santos, Oil Search. independent E&Ps: oil and gas upstream companies with market value greater than $300m as of 18 April 2018.

Kabu.com shares were bid limit up all day long and closed at ¥462, which is a 10+ year closing high.

The idea is not a new one. The mobile telecommunications market in Japan is mature, and one of the few ways Type 1 telecom providers can grow is by adding content through the “pipes.”

KDDI already has an investment in an online banking 50/50 joint venture with MUFG called Jibun Bank (“My Bank” or “Myself Bank”) which it launched in 2008. KDDI established a smartphone-based asset management service with Daiwa Securities Group (8601 JP) just under a year ago, where KDDI owns 66.6% and Daiwa 33.4%. This was to attract younger customers to savings products accessible through an app in order to make those customers stickier over the long-term. KDDI also bought into Lifenet Insurance Co (7157 JP) in 2015 through a capital raise, and is now its largest shareholder at just over 25% (a decent (and recent) presentation of the company is here). About six months ago, KDDI injected ¥6bn (link is Japanese) into Japanese financial services company Finatext to help spark their new service of a ¥0 commission brokerage. I would note that Finatext and partner (now sub) NOWCAST launched an algorithmic personal asset management advisory service using for kabu.com Securities in 2016.

Owning a stake in a broker would go a long ways towards providing comprehensive financial services access by smartphone under a KDDI-owned profit umbrella.

Is a deal like this feasible? Reasonable? Likely?

The two companies’ first response was pretty standard. This was the version from KDDI:

KDDI is considering various possibilities in financial business with kabu.com Securities, however, there is no determined facts. [a better translation of the Japanese is “however… no decisions have been made”]

This is pretty standard in Japanese corporate “clarifications.” There are, in fact, no ‘decisions’ unless a board meeting has been convened and put their stamp on it.

But the Japanese market will look at a comment like this and figure that where there is smoke there is fire.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Tactical buy supports are compelling for a bigger upside drive given the successful macro backswing support test and ascent that very often opens the way for the macro cycle to make headway, once a corrective cycle terminates. It is this corrective cycle that shows promise for an entry point.

Japan Post Holdings (JPH) does have a short history of volatile swings and will be the challenge within an ongoing basing cycle. We have well defined levels to trade this range tactically while aligning some strong risk pivot supports to reign in risk.

Macro pivot support will define the long term trend for JPH.

Toppan Printing (7911 JP) is looking to sell 10.5m shares in Recruit Holdings (6098 JP) for about US$263m. Post-placement, Toppan Printing will still have about 6% stake (103m shares) in Recruit Holdings.

The deal scores well on our framework owing to its strong price and earnings momentum and stellar track record. However, it was offset by its relatively expensive valuation compared to peers. The selldown by Toppan Printing is tiny relative to the three-month ADV which the market would likely be able to absorb. The sell down is also long overdue considering that Toppan Printing skipped the 2016 secondary offering in which many shareholders have participated.

In this report, we provide an analysis of our pair trade idea between Amorepacific Group (002790 KS) and Shiseido Co Ltd (4911 JP). Our strategy will be to long Amorepacific Group (APG) and short Shiseido. As mentioned in our report, Korean Stubs Biweekly Sigma σ (#1): The Inaugural Edition, our base case strategy is to achieve gains of 8-10% on this pair trade. Our risk control is to close the trade if it generates 4-5% in combined losses. Cost of commissions are not included in the calculations and closing prices as of January 23rd are used in our pair trade. [Long APG – $0.5 million; Short Shiseido – $0.5 million for total of $1.0 million].

The following are the major catalysts that could boost APG shares higher than Shiseido shares within the next six to twelve months:

Amorepacific Group shares are extremely oversold and forming a base

THAAD is no longer an issue

Amorepacific Group’s NAV discount

Attractive relative valuations

Amorepacific’s new headquarters building distraction out of the way

Chinese tourists are coming back to Korea & slower growth rate of visitors to Japan

A very normal part of the semiconductor cycle is inventory clearance. DRAM makers are starting to discuss this in their earnings calls. What they are NOT telling their investors is how significant this is to the onset of a price collapse, perhaps because they don’t understand it themselves. This Insight will help readers to learn how and why an inventory clearance helps ratchet a budding oversupply into a full-blown glut.

On 21 January 2019, my favorite manufacturer of garbage trucks, vertical carousel parking infrastructure, sea planes, and jetways – Shinmaywa Industries (7224 JP) – announced a share buyback. This was not unusual. The company bought back shares last year and indicated earlier this year it would seek a relatively high return of capital to shareholders. In the last five months of 2018, the company bought back 3.6% of shares outstanding, and cancelled those shares at the end of December 2018).

Indeed, the company on January 9th this year announced a revised dividend forecast for the year ending March 2019. The dividend was lifted by 1 yen.

The company also announced a new policy of shareholder returns for the year starting April 1.

While taking into consideration strategic business investment for the future and the internal reserves required for maintaining and expanding the Company’s management foundation, we are aware that appropriate return of profit to shareholders is an important management issue. In that regard, in our Medium-term Management Plan for the three years to the end of the fiscal year ending March 31, 2021, “Change for Growing, 2020,” (the “Medium-term Management Plan”), which was announced in May 2018, we set up a basic payout ratio on a consolidated basis of 40-50% and carrying out flexible acquisition of treasury shares with a focus on improvement of capital efficiency as basic shareholder return policies.

The company acknowledged the above and announced it would seek to add a commemorative (70th anniversary of incorporation and 100th anniversary of being in business) special dividend of ¥45/share, on top of the normal interim dividend (which is likely to be ¥18-19/share) paid to shareholders as of the end of September 2019.

That was nice, but that was little preparation for the news of 21 January.

On that day, the company announced yet another increase in dividend forecast for the current fiscal year, raising the H2 dividend – which had just been raised from ¥18/share to ¥19/share less than two weeks ago – to ¥27/share.

The company also announced a Tender Offer to buy back 26.666mm its own shares at a roughly 10.5% premium to last trade.

That’s a big tender offer. It is ¥40bn and 29.0% of shares outstanding.

Regular readers of Smartkarma will know that I will have comments on situations like these.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The globe is facing more than an ordinary business cycle.

Joseph C. Sternberg, editorial-page editor and European political-economy columnist for the Wall Street Journal’s European edition, recently interviewed Claudio Borio, head of the Monetaryand Economic Department of the BIS. Mr. Borio said that politicians have relied far too much on central banks, which are constrained by economic theories that offer little meaningful guidance on how to sustain growth and financial stability. The only tool they have is an interest rate that can affect output in the short run but ends up affecting only inflation in the end.

Average monthly savings rates and total savings stocks have long been high in Japan, but savings rates broke all records in June 2018.

In one sense, this was a sign that the government’s six-year effort to increase wages – and thus consumption and inflation – was finally bearing fruit, albeit small not very sweet fruit.

However, anxiety about the future, coupled with a lack of incentive to spend, meant that most of the increases in wages and bonuses stayed in the bank.

At the same time, while the majority hoarded, brands and retailers at both the luxury and discount ends of the market are reporting a record year, and discount retailers, in particular, are worthy long-term investments.

This demonstrates the further polarisation of the retail market but inventive marketing and solid cost performance will still unlock those wallets in premium mass markets too.

MUFG initially bought 19.9 percent of Bank Danamon from Singapore state investor Temasek Holdings 15.875 trillion rupiah ($1.17 billion), then valuing the Indonesian lender at around $6 billion.

Step 2 saw the OJK give the OK (BDMN announcement in English) for MUFG to up its holding to 40% – the statutory maximum under the prevailing OJK regulation No.56/POJK 03/2016 – and the Indonesian Financial Services Authority (OJK), seemingly granted permission for MUFG to go above 40% in Bank Danamon when OJK deputy commissioner for banking, Heru Kristyana, wrote in a message to a Reuters journalist (article here) on August 3rd last year “They (MUFG) can have a larger stake than 40 percent once the merger (with Bank Nusantara) has gone through and as long as they meet provisions and requirements.”

As Johannes Salim, CFA pointed out in his interesting insight Bank Danamon: Fundamentals Revisited Plus Thoughts on M&A in March last year, the revised OJK regulation No.56/POJK 03/2016 placed the authority for determining whether or not a foreign acquiror could go above 40% squarely on the OJK – no BI approval would be necessary.

Indonesia has a “Single Presence Policy” (OJK Regulation No. 39/2017) which requires that a foreign owner may not hold more than one control stake in a bank. In order to get to Step 3 which would be to acquire the remaining 33.8% of Danamon from Temasek affiliates (Asia Financial Indonesia and its affiliates), MUFG would need to merge its presence in Bank Nusantara Parahyangan (BBNP IJ) (also known as “BNP”) where it holds more than three-quarters of the shares (and has controlled since 2007) with Danamon.

The New News

This morning’s paper carried a giant notice in bahasa announcing the planned merger between BDMN and BNP with shareholder vote for both banks 26 March 2019 (record date 1 March) and effective date 1 May 2019. The Boards of Directors and Boards of Commissioners of each bank

“view that this Merger will increase the value of the company because it is a positive move for stakeholders, including the shareholders of Bank Danamon,” and

“have proposed to their shareholders to agree with the resolution on the proposed Merger in each of their respective GMS.”

Indonesian takeover procedures generally require a Mandatory Takeover Offer procedure when someone goes over a 50% holding. But banks being bought by foreigners are a different category and bank takeovers are regulated by the OJK. In addition, the structure of such takeovers creates short-term options (for holders) and possibly longer-term obligations for the acquiror which are a little unusual, but provide for a very interesting opportunity in this case.

The start of the year has been bullish on the Korean and Japanese stock markets. KOSPI is up 4% and Nikkei is up 3% YTD. Some of the most beaten down stocks in the last 3 months of 2018 in Korea and Japan have been rebounding nicely YTD. In the past week, the following reports that are relevant for Japan and Korea have received a lot of interest:

Finally, it was announced that Trump plans to meet North Korea’s Kim Jong-Un in late February in Vietnam. It has been nearly seven months since their last meeting in Singapore and there has been no progress in terms of nuclear weapons inspection or dismantling of its nuclear weapons and ICBM missiles. In April 2009, North Korea reactivated its nuclear facilities, after more than two years of North Korea promising to not to restart its nuclear programs. They lied and got away with it. And it seems like they are replaying this story-line once again.

Last week on 17 January, printing and HR services company and funeral parlor operator Kosaido Co Ltd (7868 JP)announced that Bain Capital Private Equity would conduct an MBO on its shares via Tender Offer, with a minimum threshold for success of acquiring 66.67% of the shares outstanding. The Tender Offer commenced on 18 January and goes through 1 Mach 2019. The Tender Offer Price is ¥610/share, which is a 43.8% premium to the close of the day before the announcement and a 59.7% premium to the one-month VWAP up through the day before the announcement.

The company’s board of directors announced it supported the deal.

Terms & Schedule

Terms & Schedule of Hitachi Tender Offer for Yungtay Engineering

Tender Offer Price

JPY 610

Tender Offer Start Date

18 January 2019

Tender Offer Close Date

1 March 2019

Tender Agent

SMBC Securities

Maximum Shares To Buy

24,913,439 shares

MINIMUM Shares To Buy

16,609,000 shares

Currently Owned Shares

100 shares

Irrevocable Undertakings

Sawada Holdings’ 3,088,500 shares or 12.40% (includes the holdings at both Sawada Holdings and HS Securities).

This deal is probably reasonably straightforward.

It is a big premium to last trade, and a multi-year high.

There is one large holder publicly willing to sell and I expect the cross-holders would be willing to sell too.

Management is involved and supportive.

Except it is being done (and recommended) at a 44% discount to Tangible Book Value Per Share after the directors managed to work Bain up from a 49% discount to TBVPS.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

It seems that Panasonic Corp (6752 JP) is planning for long term growth by concentrating on building its relationship with Toyota Motor (7203 JP) while witnessing its key customer, Tesla Motors (TSLA US), drifts away. Toyota and Panasonic are in discussion to form a JV by 2020E with the aim of mass manufacturing EV batteries with possible benefits from cost-cutting efforts. We mentioned in Tesla Drifting Away Could Leave Panasonic Struggling to Gain Traction in China, that Tesla is looking for Chinese local players to source its factory in China upon the refusal from Panasonic to join hands with them in investing in their Chinese factory. Panasonic, which seemed to have felt the pressure mounting from Tesla potentially distancing itself from them, given that the majority of their battery sales are currently dependent on Tesla, is now preparing itself for the future by building long terms plans with its not-so-new customer, Toyota. Panasonic entered a partnership agreement with Toyota back in 2017 to develop EV batteries including their traditional prismatic batteries while also aiming to develop new battery solutions for the growing and evolving EV market. Thus, its plan to form a JV with Toyota by 2020E displays the confidence Panasonic has in Toyota while also indicating that the former is paving a path for some steady growth in its battery business being supported by one of the leading automakers.

China Meidong Auto (1268 HK) has been on a rollercoaster ride in 2018. The stock price of Meidong started 2018 around 2.7 HKD and recently has been trading around 2.9 HKD.

Nice and steady ride? Not exactly, as it has swung from 4.3 HKD in June to 2.6 HKD in August. After analyzing how NPAT estimates evolved over the past year there should be no justifications for these wild swings.

Meidong is likely to report solid FY18 results by late March vs industry peers which are expected to report a weak 2H18. While BMW dealers have been reportedly suffering in China during 2018, Meidong was fortunate to have other luxury brands pick up the slack.

FY19 should be another growth year for Meidong as 1) recently acquired BMW showrooms contribute their maiden results and 2) other luxury brands continue to perform despite overall doom and gloom in the Chinese auto market. Should the Chinese government launch car replacement stimulus measures this would be icing on the cake.

Fair Value lowered slightly from 4.7 HKD to 4.4 HKD (10x 2019E) on lower 2019 profit estimates, which leaves 52% upside excluding dividends.

The shares are very cheap. They trade at 0.9x book but there is some Y22bn in unrealised profit on land/buildings (vs. the market cap of Y46bn). If adjusted for this, the shares are less that half book. Meanwhile the dividend has been steadily increasing (both payout ratio and in absolute terms). To 11/19 the payout ratio will be 23% and the dividend will rise to Y37 from Y30 last year. At today’s price of Y950, the yield is thus 3.9%. And the shares trade on multiple of 6x. They rose significantly last year on the back of Morgan Stanley BUY note (from Y800 to Y1,500) but with the market’s correction and the tightening of bank lending to individuals (which has no impact on them), the shares have fallen back to Y950. For those looking for a cheap domestic small cap name, this is worth looking at.

Japan’s B2C e-commerce industry is growing sales volumes close to 10% YoY each year, but the level of online activity remains behind other developed markets. Globally, e-commerce volumes are growing around 20% per year. The Japanese government does not want Japan to be left behind and wishes to see more domestic e-commerce activity as well as strong growth in cross-border e-commerce.

Domestic giants Rakuten (4755 JP) and Yahoo Japan (4689 JP) are growing faster than the overall market. So is global powerhouse Amazon.com (AMZN US) in Japan. Together the three represent nearly half of the market today, up from 40% 4 years ago.

Both Rakuten (4755 JP) and Yahoo Japan (4689 JP) have seen profit margins squeezed in recent years, most notably by increasing competition, including from profit insensitive Amazon Japan. We believe e-commerce profit margins will remain under pressure and note managements’ efforts to diversify.

The upcoming earnings season will provide a once-a-year window into Japan’s e-commerce industry. Amazon.com (AMZN US) will announce its full year results on 31 January 2019, and the company’s filings include annual sales figures for its Japan operations.

13 months ago, real estate operator TOC Co Ltd (8841 JP) – known for decades in Tokyo as the owner/operator of the largest single building in Tokyo by floor space – launched a Tender Offer to buy up to 20mm shares or 16.4% of the shares outstanding. Effissimo, Mizuho Bank, Mitsubishi UFJ Bank, and Mitsui Sumitomo Bank had each apparently approached the company indicating they were interested in selling.

The Tender Offer resulted in Effissimo selling 17,916,900 shares, leaving them with 4.599mm shares. Combined, other parties sold 800,000 shares.

On the 21st of March 2018, TOC announced it would cancel 33 million shares out (they already had ~14mm shares of Treasury stock prior to launching the Tender Offer). Later they launched another buyback program and the company has 1.847mm shares of Treasury stock as of now, out of 103.88mm shares outstanding.

Yesterday after the close, the company announced a ToSTNeT-3 Buyback this morning, to buy up to 4.6 million shares or 4.49% of shares outstanding at ¥778/share.

That makes the previous argument stronger, not weaker.

To not reinvent the wheel, the second insight is the one with the deep dive information about the company and its assets.

A review of the opportunity continues below.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Below are several recent updates on Japanese retail and consumer markets that, while not meriting in-depth Insights of their own, are important trends impacting retail stocks.

TPP: profit and loss for Japan

The Trans-Pacific Partnership trade deal came into effect in late December, immediately cutting import tariffs across much of Southeast Asia. Despite some claims that this will help consumers, the cuts are most likely to benefit trading firms and leading food wholesalers like Mitsubishi Shokuhin (7451 JP) and Itochu Shokuhin (2692 JP) rather than result in lower retail prices.

Mash and Jun to start premium online lifestyle mall in October

Two leading lifestyle and fashion firms, Mash Holdings and Jun, will together launch a new challenger in the fashion and lifestyle online market in October. This is a threat to the premium end of ZOZO’s (3092 JP) marketplace as well as the nascent Stripe Department, a joint venture between Softbank (9434 JP) and Stripe International, an unlisted fashion retailer.

A flat fashion market

A comprehensive recent survey of fashion industry managers suggests they are less optimistic about the outlook for 2019 compared to a year ago, weighed down with worries about depopulation, global trade, and changing consumer sentiment. More optimistically, many are investing in e-commerce as well as preparing to expand overseas.

Organic foods growing in popularity

After something of a false start back in the 1990s, organic fresh food is now moving out of a limited niche and into the mainstream, benefiting Oisix Ra Daichi (3182 JP) in particular.

Muji really is no name in China

Ryohin Keikaku’s (7453 JP) Muji is popular in China, but trademark conflicts, easy replication, as well as new emulator brands, all mean the “no brand” brand is not assured of continued success in the market.

We run through our views on the main themes that will impact the oil and gas market in 2019 and the stocks to play these through. We outline the 10 key themes including oil demand, US oil supply growth, OPEC+ policy, base production decline rates, exploration potential and the outlook for new project final investment decisions. We also look at the refining market, LNG supply and demand, the M&A prospects and the impact of the energy transition. We outline 12 stocks (7 bullish and 5 bearish calls) that we think you can play the themes through.

We examine some of the key drivers of the oil price and on the whole we are relatively bullish as although we see some risk to demand growth forecasts in 2019, in the absence of a recession we think that supply has more room to surprise to the downside. Geopolitics and financial markets will play a huge role in prices. We think that US oil supply growth will be lower y/y in 2019, OPEC+ compliance with cuts will be high and maybe helped by unplanned disruptions and base production will decline more rapidly than forecast. Companies will accelerate the sanctioning of new projects in 2019 and also will increase exploration spending, despite a number of years of poor success rates – overall the trend should be positive for the offshore oil service companies. We expect strong LNG supply growth in 2019 to hit spot pricing but still expect a large number of projects to be sanctioned helping the LNG engineering and construction companies. It will be a very interesting year for the refining industry as new regulations limiting shipping sulphur emissions should lead to a spike in diesel and to some extent gasoline margins towards the end of the year, helping complex refiners. Major oil companies will continue to embrace renewables as investors continue to push for companies to plan for the energy transition.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Starting with placements this week, we had a relatively small Recruit Holdings (6098 JP) block sold by Toppan Printing (7911 JP). The stock traded below its deal price of JPY2,762 for the most part of the first-day post-placement. It bounced back on Friday to close just 0.6% above its deal price. We were bullish about the placement because it was a tiny deal relative to its three-month ADV.

There was also a small Ihh Healthcare (IHH MK) secondary block on Thursday after markets have closed. The deal was about US$80m and got priced at MYR5.56, the bottom-end of the price range.

For deals that have launched, there are Maoyan Entertainment (EPLUS HK) and Chalet Hotels. Maoyan will be pricing on the 28th of January while Chalet Hotels will open its book on the 29th of January and swiftly close on the 31st.

Earlier this week, we also heard that Dexin China, a property developer mostly based on Zhejiang Province, was seeking listing approval to list in Hong Kong whereas Global Switch, a UK-based data center operator, will meet banks next week in London to choose arrangers for a Hong Kong IPO of about US$1bn in 2019.

Other than that, another pharma company, Jubilant Pharma, is looking to list on the US market after getting tepid interests from investors for an SGX listing. It was initially looking to raise about US$500m. Fang Holdings Limited (SFUN US), a Chinese real estate internet portal, has also submitted a confidential filing to the SEC for a proposed spin-off of its research unit, China Index Holdings.

Accuracy Rate:

Our overall accuracy rate is 71.9% for IPOs and 63.8% for Placements

(Performance measurement criteria is explained at the end of the note)

No new IPO filings

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

In our base case, we do not expect the trade war between the US and China to end soon. The next bilateral meeting between Liu He and US Trade Representative Robert Lighthizer is scheduled at the end of this month. If the Chinese side is hoping to placate the US with promises to purchase US commodities, this is unlikely to be sufficient to achieve a lasting improvement in the relationship. We are sceptical that the Chinese leadership will agree to launch structural reforms under pressure from the US.

Elsewhere, we are concerned with growing geopolitical and security risks in Nigeria where both presidential and parliamentary elections are scheduled in February. The relations between Turkey and the US have also soured ahead of the Turkish local elections. In Poland, the assassination of the Gdansk mayor put the polarisation of the society into the spotlight ahead of the parliamentary elections due this autumn. There are signs that the US is about to ramp up pressure on Russia after newly elected Democratic House members filled their seats earlier this month.

On January 24’th 2019, SEMI announced that Wafer Fab Equipment (WFE) billings for North America-based manufacturers of semiconductor equipment amounted to $2.11 billion worldwide in December 2018. This represents an 8.5% MoM increase, although still lower YoY by 12.1%. December’s data marks the reversal of a six month long downtrend in monthly billings, a bullish signal that the WFE segment has bottomed and better times lie ahead.

This latest billings data coincides with WFE bellwether Lam Research (LRCX US)‘s latest earnings report which slightly exceeded guidance with revenues of $2.5 billion, up 8.7% sequentially. On the call, company executives stated that first quarter CY 2019 would mark the trough from a gross margin perspective, strongly implying that it would be the same for revenues.

LRCX shares surged 15.7% in overnight trading triggering a rising tide that lifted large swathes of semiconductor stocks, particularly those within the WFE sector. Two swallows don’t necessarily mean it’s Spring, but for now, the markets are betting that it does.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

After dropping to a 52-week low of ¥11,405 on January 17 – the day after management announced a large downward revision to sales and profit guidance – Nidec rebounded to close at ¥13,055 on Friday, January 25. The latter price is 30% below the ¥18,525 peak reached a year earlier. Both the shock of the downward revision and the reflexive optimism of believers in the company now seem to have been discounted.

Consolidated sales and profits dropped abruptly in the three months to December and are expected to drop further in 4Q of FY Mar-19 due to weak demand in most regional markets, inventory write-downs and restructuring costs. Nidec is already reconfiguring its global supply chains, shipping products to the U.S. from Mexico and Europe instead of from China and planning to build factories to make motors for electric vehicles in Mexico and Poland in addition to China.

With most of the one-off expenses out of the way, profits should start to recover in FY Mar-20. Sales, on the other hand, seem likely to decline further due to weak unit demand and pricing for HDD spindle motors, falling auto production in China and elsewhere, and weakness in other industrial and commercial markets. Recovery will depend on U.S.-China trade relations and the state of the world economy, and new acquisitions that cannot be predicted. As things stand now, we expect sales to pick up going into FY Mar-21. In the long run, the company should continue to benefit from the electrification of the auto market and factory automation.

At ¥13,055, the shares are selling at 34x management’s EPS guidance for FY Mar-19, 32x our estimate for FY Mar-20 and 30x our EPS estimate for FY Mar-21. Projected EV/EBITDA multiples for the same three years are 18x, 17x and 15x. Price/book value as of the end of December is 3.9x. The dividend yield is less than 1%. Over the past few years, the P/E has found support at 20x, EV/EBITDA at 10x and the PBR at 2.5x. The January 17 low put the shares on 30x management’s new EPS guidance for this fiscal year.

On Friday 25 January 2019, shareholders of Pioneer Corp (6773 JP) voted to implement a self-imposed (self-inflicted?) equity “cramdown” of sorts.

In September, Pioneer and BPAE signed a memorandum of understanding whereby Baring Private Equity Asia would lend money to Pioneer and subsequently inject equity capital and keep the company listed. In December, BPAE and Pioneer management decided that the equity injection would push out then-existing shareholders at a steep discount to the lowest share price the stock had theretofore seen in the company’s 50-year-plus history of being listed.

Now that’s done.

The situation now looks quite a bit like a regular “risk arb” or “wind up” situation, though investors do not have exact understanding of the payment date.

On December 17th 2018, the TSE announced a somewhat strange and unexpected treatment of the TSE-calculated indices for two companies where shares were issued to shareholders of a foreign company where the Japanese company had acquired the foreign company through a Scheme of Arrangement under foreign jurisdiction.

The announcements for TOPIX and JPX Nikkei 400 were made then, and despite the events being entirely similar in construct, but different in month of Scheme Effective Date, they were put in the same month for Mitula and the first tranche of the Takeda inclusion, which was split between two months because of its large impact.

The large IPO last month of Softbank Corp (9434 JP) means there is another large inclusion going effective as of the open of trading on 31 January.

Wednesday is going to be a big day.

If everyone trades their required index amount on the day, it should be a trillion yen plus of flows.

CONSISTENCY PAYS – In troubled markets, investors often seek out companies with greater earnings stability and a history of consistent stock outperformance. Conversely, companies that offer investors more of a rollercoaster ride (Chiyoda Corp (6366 JP) being an excellent recent example) are less rewarding, especially when adjusted for volatility. In an attempt to sort the ‘Steady Eddies’ from the Rollercoaster Rides’, we have created a Consistency Score – a composite based on our Results Score, Forecast/Revision Score, Relative Price Score and Volume Score – which measures the variability, consistency, correlation, and range of each of these scores for every company. Cap-weighted aggregate Consistency Scores are then derived for 321 Peer Groups and 29 Sectors – REITs are excluded from this analysis. Over 3 million data points have been reviewed in creating this analysis. As the old slogan goes – “we do the work, so you don’t have to’.

‘CARP = CONSISTENCY-AT-A-REASONABLE-PRICE‘ – Our findings will not surprise long-term investors in Japanese equities; the simple asset allocation decision to prefer domestic growth over global value has determined the quartile-ranking of many strategies in recent years. Although many of these Sectors, Peer Groups and stocks are now overvalued, we do not expect the underlying business dynamics to change in the years ahead and many excellent investment opportunities remain, especially down the cap-scale. Periodic and often substantial mean reversions in the more cyclical sectors, such as the one that has occurred in the last two days, will offer attractive trading opportunities for more-nimble portfolio managers. Longer-term orientated investors are better-advised to continue to favour ‘consistency-at-a-reasonable-price’. Some of our ‘findings’, as explained in more DETAIL below, are as follows: –

SECTORS – The better investors in Japan over the last two decades have eschewed traditional manufacturing in favour of Services, IT/Internet, Retail, Restaurants and ‘FB&T‘. Only Machinery and Electrical Equipment outperformed the market’s 4% compound annual growth rate (CAGR) over the period.

PEER GROUPS– The most-consistent Peer Groups are found in industries associated with food, drugs, welfare, shelter and amusement. Only five of the top-forty Peer Groups – Online Payment Services, E-Commerce, IT System Services, Telecom Distribution Services and Internet Software & Services belong to the ‘new age’. There are no manufacturing Peer Groups in the top-forty. The best performing Peer Group is Securities Services, and the worst-performing is Investment Management & Advice. Although both havesimilar levels of consistency, the stock exchange has beaten its fund managers by 28% annually since 2005.

COMPANIES – The simple average fourteen-year compound annual share price appreciation for all listed large-cap companies is +5.1%. For all listed companies the average falls to just +0.5%, highlighting the perils of investing in Japan’s small caps. The average share price CAGR for our hindsight-selected top-forty is +18.7%. In contrast, only one of our forty least-consistent companies outperformed the market and the average for the least-consistent forty companies was a negative -3.2%. Unsurprisingly, there are eight banks and six steel companies on the list, along with two glass companies and two shipping lines.

CONSISTENCY HALL OF FAME/SHAME AWARDS – We have selected one company from each of the most and least consistent lists as the winner of a ‘Consistency Award’. Both are highlighted in the chart above. One of them will be as surprising to many readers as it was to us.

In December 2017, Mitsubishi UFJ Financial (8306 JP) launched a complicated three-step process to acquire up to 40%, then up to 73.8% (or more) in BDMN, five years after DBS’ aborted attempt to obtain a majority in the same bank. Mid-week, local papers announced the planned merger between BDMN and BNP with shareholder vote for both banks 26 March 2019 (record date 1 March) and effective date 1 May 2019.

It looks like this is almost completely bedded down. MUFG has a good relationship with Indonesian regulators and it would not have arrived at this Step 3 without pretty clear pre-approval indicated.

The result is an effective Tender Offer Trade at IDR 9,590/share for the float of BDMN. With shares up 8% the day of the announcement, there was another 6+% left for payment in three months and a week which comes out to 25.4% annualized in IDR terms through the close. Travis thought this is an excellent return for the risk here.

Indonesian takeover procedures generally require a Mandatory Takeover Offer procedure when someone goes over a 50% holding. But banks being bought by foreigners are a different category and bank takeovers are regulated by the OJK. The upshot is that if you tender, you will get the Tender Offer consideration. And if EVERY public shareholder tenders, MUFG will have to conduct a selldown of 7.5% within a very short period, and a selldown of 20% within 2 years or up to 5 years (a virtual IPO when it comes), in order to meet the free float requirements.

ESR has now declared its Offer for Propertylink “to be best and final“, and the Offer has been extended until the 28 February (unless further extended). After adjusting for the interim distribution of A$0.036/share (ex-date 28 December; payment 31 January), the amount payable by ESR under the Offer is A$1.164/share, cash. The Target Statement issued back on the 20 November included a “fair and reasonable” opinion from KPMG, together with unanimous PLG board support.

The next key event is CNI’s shareholder vote on the 31 January. This is not a vote to decide on tendering the shares held by CNI in PLG into ESR’s offer; but to give CNI’s board the authorisation to tender (or not to tender) its 19.5% stake in PLG.

Although no definitive decision has been made public by CNI, calling the EGM to get shareholder approval and attaching a “fair & reasonable” opinion from an independent expert (Deloitte) to CNI’s EGM notice, can be construed as sending a strong signal CNI’s board will ultimately tender in its shares. According to the AFR (paywalled), CNI’s John Mcbain said: “We want to make sure when we do decide to vote, if we get shareholder approval, the timing is with us“.

Assuming the resolution passes, CNI’s board decision on PLG shares will take place shortly afterwards. My bet is this turns unconditional the first week of Feb. The consideration under the Offer would then be paid 20 business days after the Offer becomes unconditional. Currently trading with completion in mind at a gross/annualised spread of 0.8%/6.7%, assuming payment the first week of March.

The company announced a Tender Offer to buy back 26.666mm of its own shares at a roughly 10.5% premium to last trade. That’s a big tender offer. It is ¥40bn and 29.0% of shares outstanding. Shinmaywa prepared this well because they rearranged their holding grouping to be all held under corporate entities (in many situations, they hold under personal names). For some of us, that should have been a clue.

The main purpose of this effort is to get rid of Murakami-san, but Travis’ back of the napkin suggests just a 25% gain for Murakami, which is small beer for an investor bullish on the company’s prospects.

The outright long prospects do not impress. There are a lot of companies in the market with 3+% dividend rates and low PERs which are illiquid. The company will go into a net debt situation. That will likely cap future buybacks to the limit of spending this year’s net income. That would be big, but Travis expects with a high dividend, buybacks will be less likely.

Overall the business is OK, but it is unlikely to grow dramatically enough to warrant an ROE and margins which would make a price of 1.3-1.5x book appropriate in the near-term. Travis expects the tender offer to go through, and expects the price to be a bit “sticky” at this level near-term.

Huarong-CMB network [HCN] play New Sports announced a cash or scrip offer, with the cash alternative of $0.435/share priced at a premium of 3.57% to last close. The Offeror (China Goldjoy (1282 HK) – another HCN play) has entered into an SPA to acquire 37.18% of shares out. Upon successful completion of the SPA, Goldjoy will hold 66.44% and be required to make an unconditional general offer for all remaining shares.

The key condition to the SPA is Goldjoy’s shareholder approval. This should be a simple majority and the major shareholder, Yao Jianhui, has 41.9% in Goldjoy according to HKEx and page 23 of the Offer announcement.

Despite the potential issues faced by New Sports, this is a very real deal, with financing in place for the cash option.

The idea is not a new one. The mobile telecommunications market in Japan is mature, and one of the few ways Type 1 telecom providers can grow is by adding content through the “pipes.” KDDI needs non-telecom revenue channels. KDDI has a bank, and life insurance, and some investment in asset management channels. It needs more, and better. A broker with a bank attached is a pretty good way to get long-term investment and savings products to customers.

Kabu.com is not the best one out there in terms of bang for buck. But KDDI already has a JV with kabu.com majority shareholder MUFG and another with kabu.com. If you could buy an online broker, you might choose to buy Rakuten or SBI, but you can’t. You have to buy the rest of the company with them.

Kabu.com shares were bid limit up all day long after the Nikkei article and closed at ¥462, which is a 10+ year closing high. You have to believe that KDDI is willing to pay a knock-out price to get this trade done. They may, but that is the bet. But Travis sees no impediment to the deal getting done.

Printing and HR services company and funeral parlor operator Kosaido announced that Bain Capital Private Equity would conduct an MBO on its shares via Tender Offer, with a minimum threshold for success of acquiring 66.67% of the shares outstanding. The Tender Offer commenced on 18 January and goes through 1 Mach 2019. The Tender Offer Price is ¥610/share, which is a 43.8% premium to the close of the day before the announcement and a 59.7% premium to the one-month VWAP up through the day before the announcement.

While the pretense will be that the deal is designed to grow the funeral parlor business (which, given the demographics, should be a decent business over time), this is a virtual asset strip in progress. It is the kind of thing which gives activist hedge funds a bad name, but when cloaked in the finery of “Private Equity”, it looks like renewal of a business.

It is a decent premium but an underwhelming valuation. Because of the premium, and its smallcap nature, Travis expect this gets done. If deals like this start to not get done, that would be a bullish sign. Investors will finally be taking the blinders off to unfair M&A practices.

This is a small deal. It is meaningless in the grand scheme of things. But it is a deal which should not have been done at this price because better governance would have meant the stock traded at better than 0.4x book before the announcement.

Bristol Myers Squibb Co (BMY US) announced earnings for 4Q18 this morning followed by a conference call. Most metrics beat street expectations but the withdrawal of its application for Opdivo + low-dose Yervoy for first-line (NSCLC) lung cancer patients with high tumour mutation burdens after discussions with the FDA weighed on shares of BMY today. But for arbs who have the CELG/BMY spread set up, the positive comments on the Celgene acquisition provided further assurance of BMY’s commitment to the deal.

There was, however, no discussion, in the prepared remarks or the Q&A, of the status of antitrust filings (nor was the question asked in the Q&A). The U.S. Hart-Scott-Rodino antitrust filing should have been made with the FTC/DoJ by January 16th, 2019 according to the terms of the merger agreement, although this has not been publicly confirmed. The EU Competition web site does not show a competition filing having been made, and I would not have expected one so soon after the announcement of the deal.

Closing prices equate to annualised rates of return of ~20% / ~26.5%, respectively, by John DeMasi‘s calcs, which is very attractive.

Travis succinctly summarised the ongoing saga of governance and control that is the Renault/Nissan Alliance and speculates on the next chapter.

Carlos Ghosn is likely in more trouble. The release last Friday by Nissan and Mitsubishi makes clear that Ghosn effectively signed contracts to pay himself a very large sum of money from the funds of the Nissan-Mitsubishi Alliance treasury in ways which contravened the rules established for that Joint Venture.

The other news was that French visitors to Tokyo allegedly informed Japanese officials of their intention to have Renault appoint the next chairman of Nissan (as apparently, the Alliance agreement allows) and of the French State’s intention to seek to integrate Nissan and Renault under the umbrella of a single holding company. This is, the French state seeking to intervene in the governance of Nissan. That’s a no-no according to the Alliance Agreement.

Nissan CAN react to any Renault breach of Nissan’s governance by purchasing shares to render Renault’s shares voteless. It can, for example, purchase economic exposure to Renault shares in the form of a cash-settled derivative, where it had neither voting rights nor the access to obtain them.It can do so quickly enough to react to anything that Renault can do by surprise, but it would be a clear breach of the Alliance Agreement to do so quickly.

Travis reckons Renault and Nissan will not deliberately blow up their Alliance – they will work through their issues slowly and painfully. This will cause uncertainty among investors. IF the two companies ever sort out their relationship and decide to merge, the combined entity is cheap. Very cheap. If they blow up their Alliance, they are both going to turn out to be expensive.

Earlier this week, TOC announced a ToSTNeT-3 Buyback, to buy up to 4.6mn shares or 4.49% of shares outstanding at ¥778/share. With this latest buyback, TOC has bought back 30% of shares outstanding in the past 14 months after selling a large asset before that. This has resulted in 49.5% of the votes held by the Ohtani family and their namesake companies, another 30% will be held by cross-holders who are loyal to the family, about 8-9% of the company will be owned by passive investors, and 11-13% of shares will be held by everyone else.

The company’s largest and most famous asset is a near-50-year-old building. There have been suggestions of redevelopment (discussed in more depth here). The two family members controlling almost 50% of the shares (plus the New Otani Company parent) are 72 and 66yrs old respectively. A 10-year redevelopment project might outlast them. The project might be better off in other hands.

The company has very long-held real estate assets – some of which are fully-depreciated and have very low land price book values. The share price is trading below Tangible Book Value. The shares trade at roughly 8x EBIT, which is very inexpensive for deeply undervalued and still earning real estate assets.

The stock is illiquid, trading US$1.25mm/day on a three-month average, and sometimes a lot less, but there is considerable asset backing to these shares. Travis would want to be long here.

Both Intouch Holdings (INTUCH TB) and Thaicom Pcl (THCOM TB) gained ~10% earlier in the week in response to rumours of a government takeout of Thaicom. I estimate the discount to NAV at ~23%, versus an average of 28%, around its narrowest inside a year. The implied stub is at its narrowest inside a year. It was a decent move, translating to a Bt15.2bn lift in Intouch’s market cap, ~4.5x the value of the holding in Thaicom. That alone would suggest Intouch had been overbought.

That the Thai State-run CAT Telecom may take over Thaicom has a ring of truth to it. The military/government uses Thaicom, the only satellite operator in Thailand, and perhaps it is not (finally) comfortable with Singapore’s indirect interest in Thaicom via Singtel (ST SP)‘s stake in Intouch. It is an election year.

The rumoured price tag is Bt8.50/share or ~28% premium to the undisturbed price. Even a takeover premium north of 50% has no material impact on Intouch, as Thaicom accounts for 2% of NAV/GAV. However, selling Thaicom will further clean up what is already a very straightforward single-stock Holdco structure.

Optically Intouch has run its course in response to these Thaicom rumours – Intouch has denied any definitive approach/agreement – however, if a sale unfolds, this may help nudge the discount marginally lower from here.

Should CAT buy out Intouch’s stake, would it be required to make an Offer for all remaining shares? As the stake is above one of the key thresholds, (that is, 25%, 50% or 75% of its the total voting rights) it would be required to conduct a mandatory tender offer. But CAT may be afforded a partial offer, if Thaicom shareholders approve.

With SamE’s1P discount to Common at 16.61%, the lowest since mid-November last year, Sanghyun recommends to go long Common and short 1P with a short term horizon.

LEAP Holdings Group Ltd (1499 HK)announced an MGO at $0.1585/share vs. the last close of $0.39, but above Anthony Wong’s (the seller) in-price of $0.1236/share. Like Wong, this new Offeror has no experience in LEAP’s business. The Offeror is primarily a vehicle owned by Xu Mingxing, who has experience in blockchain technology. However, a more detailed overview of the Offeror can be found on page 14 of the HKEx link, which provides details of no less than 15 individuals with stakes into the Offeror.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Issuance of the new shares and common stock to be delisted on the Tokyo Stock Exchange

C

Japan

Showa Shell Sekiyu Kk

Scheme

1-Apr

Merger Effective

C

Japan

Idemitsu Kosan

Scheme

1-Apr

Merger Effective

C

NZ

Trade Me Group

Scheme

29-Jan

Scheme Booklet provided to the Takeovers Panel

C

Singapore

Courts Asia Limited

Scheme

8-Feb

Despatch of offer document

C

Singapore

M1 Limited

Off Mkt

18-Feb

Closing date of offer

C

Singapore

PCI Limited

Scheme

Jan/Feb

Dispatch of scheme doc

E

Thailand

Delta Electronics

Off Mkt

28-Jan

SAMR Approval

E

Finland

Amer Sports

Off Mkt

28-Feb

Offer Period Expires

C

Norway

Oslo Børs VPS

Off Mkt

Jan

Offer process to commence

E

Switzerland

Panalpina Welttransport

Off Mkt

27-Feb

Binding offer to be Announced

E

UK

Shire plc

Scheme

22-Jan

Settlement date

C

US

iKang Healthcare

Scheme

Jan

Offer close date, (failing which) 31-Jan-2019 – Termination Date

C

US

Red Hat, Inc.

Scheme

March/April

Deal lodged for approval with EU Regulators

C

Source: Company announcements. E = Smartkarma estimates; C =confirmed

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

If you are a follower of the Asian stock markets, one of the “rules of thumb” is to carefully follow the investments trails of the “superman” Li Ka-Shing, who has recently publicly declared that he supports Bakkt. On December 31st, 2018, Bakkt raised $182.5 million from high profile investors including Li Ka-Shing backed Horizon Ventures, M12 (Microsoft’s venture capital arm), Intercontinental Exchange (owner of the New York Stock Exchange), Alan Howard, and the Boston Consulting Group.

Starbucks and Bakkt have yet to mention exactly when Starbucks will allow consumers to use Bitcoin to purchase coffee at their stores. In terms of timing, we believe that the probable time frame is likely to be sometime in 4Q 2019 to 2020 when Starbucks will start allowing their consumers to start using Bitcoin at some of their stores. This will represent a crucial positive tipping point for Bitcoin in the next two years.

Softbank Group (9984 JP) released the results of its 750mn USD tender for its Euro and USD commercial paper, which could also portend further support for the equity ahead of results next Wednesday. More details below.

We think the market is underestimating global LNG supply in the early to mid-2020s from current facilities: initially we look at Australia, which became the world’s largest LNG exporter on a monthly basis in November (~80mtpa or 25% of global supply). Our analysis of Australian LNG supply suggests that production in the early to mid-2020s will be much higher than market expectations of falling production, as fields move into decline. Overall we think this is negative longer-term for the LNG market as supply could supply to the upside but it is a relative positive for the Australian LNG companies.

We think production could grow to around 95mtpa by the mid-2020s due to substantial upside to the nameplate capacity on existing facilities, tie-backs and new developments keeping existing facilities full and utilizing new brownfield LNG trains. Australia’s key advantages versus LNG projects elsewhere are the low offshore upstream operating costs, cheap shipping costs to Asia, an investor friendly environment and having a huge installed base of LNG infrastructure and associated cashflows.

With its nationwide fiber optic network infrastructure, NTT continues to dominate the fixed line broadband market in Japan with 68% market share. In this Insight we explore the fixed line broadband market in Japan today and how it is evolving, especially with the increasing dominance of “collaboration” offerings that bundle fiber with mobile services.

Mobile services are getting a lot of attention today, especially in the run up to 5G launches over the coming 12 months, but without fiber backhaul, 5G would be a nonstarter. In this Insight we investigate what 5G will bring and what is needed to support it as well as the telcos’ latest plans.

NTT is not just an incumbent telecom operator, it’s also a key player for future technologies and provides the physical infrastructure and architecture for many of the industries new services.With all the talk about 5G it is sometimes easy to forget that fixed line networks are still necessary. With NTT’s strong fiber-based network and its collaborations with NTT Docomo and many other partners in mobile and data, we believe NTT is well positioned to be a key and winning player in the evolving telecom and technology space.

Profit Warning for Q4 2018 and Q1 2019: Two Fridays ago, Elon Musk warned that Q4 profits came in lower than Q3’s, despite an 8% QoQ rise in vehicle sales during Q4. He also announced a 7% cut in Tesla’s workforce, as Tesla is now facing “a tiny profit” in Q1 that will be achieved with “great difficulty, effort and some luck”. These are extremely bearish comments from a perennial optimist like Musk. If true, however, it kills the growth story at Tesla. And with the average 15% price cut of the Model 3 in the US and 17% in China, it also shows that Tesla may have misread the demand environment for its high-priced electric sedan.

Model 3 Demand in the US has Clearly Been Exhausted: September 2018 saw peak monthly sales of 22,250 units in the US, which fell to an average monthly rate of 18,039 units in Q4. There are no more wait lists for the Model 3 at current prices: Tesla’s website says delivery can be made in under 2 weeks. In the January 18th profit warning, Musk admitted that Tesla must now sell its lowest-end version for $35,000 from May, or see production fall. At this price, Tesla’s Model 3 probably just breaks even, by our estimates.

Weak Model 3 Launch in Europe: It was hoped that the Model 3’s European launch this March would make up for waning demand in the US. But since opening up configurations for reservation holders on December 7th, Tesla only received 13,773 orders, which is a whopping 24% lower than recent monthly sales in the US. Musk was forced to open up configurations to non-reservation holders, but this led to only 2,436 extra orders over the following 2 weeks. In the US, Tesla opened up the Model 3 floodgates to non-reservation holders 12 months after launching the car. In Europe, it took less than 4 weeks.

No Hopes for Tesla in China Either in 2019: Tesla’s registrations in China for October and November 2018, combined, fell by 72% YoY and overall auto demand is weakening there. Musk proclaimed that Tesla would start production of the Model 3 in Shanghai by 2019-end. The factory site is a barren plot of land (see Figure-5). It took VW 23 months to build its latest factory in China and Toyota’s new Alabama plant will require 28 months. Why should we believe that Tesla only needs 11 months?

Watch the Competition for Tesla in 2019: Tesla will face true competition this year for its first time as 4 new European EVs hit the market. During Q4 of 2018, Jaguar’s new I-Pace outsold Tesla’s Models S and X, combined, in the Netherlands–Tesla’s number two market after the US. Audi’s e-Tron SUV–due out next month–had over 20,000 orders as of December 7th last year. Porsche’s new Taycan–a powerful rival for Tesla’s Model S–has sold out its first year of production, with most orders coming from Tesla owners. The Models S/X provided 50% of automotive gross profit in the 2H of 2018, by our estimates. A fall in volume will heavily impact profits.

Spending Will Spike in 2019 and Lead to Negative FCF: Tesla was able to squeeze out a profit during the 2H of 2018 largely because of suppressed spending on R&D and infrastructure. In order to roll out the new Shanghai plant and bring the new Model Y to market, both capex and R&D must rise significantly in 2019. Our list of “spending needs” (see Figure-1) shows that capex should nearly double to $4.5bn in 2019. Including debt obligations and payables, Tesla’s total cash needs in 2019 come to $9.3bn, which is over twice its equity. A highly dilutive public share offering appears inevitable.

Why 2019 Could Be the End of Tesla: Tesla proved in 2018 that, even with higher sales volumes and lofty pricing for the Model 3, it could only attain an estimated 2H operating margin of 1.7%, excluding environmental credits, one-offs, and stock-based compensation. 2019 will be incredibly harder as 1) Tesla faces stiff competition for the first time since its inception; 2) a lower-priced Model 3 will not generate enough profit to cover falling profitability of the Models S/X; and 3) most significantly, a steep rise in capex and R&D will lead to higher losses and negative FCF. Tesla may need a bailout by a deep-pocketed suitor this year. But this could only occur at a much lower share price.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Olympus Corporation is currently trading at JPY4,525 per share which we believe is overvalued based on our EV/EBIT valuation. The company generates nearly 80.0% of its revenue from its Medical Business where it is the global market leader for gastrointestinal endoscopes. Despite Olympus’ market share and technology leadership, the segment has been hit by investigations related to its duodenoscopies and has been fined for violating safety regulations. In addition, the Medical Division is also subject to several bribery-related investigations by the US Department of Justice and could risk losing its market share if the allegations are proven given the industry is highly competitive. Meanwhile its Imaging Business which offers cameras and lenses, is operating in a contracting market, where the segment continues to see declining revenues and is loss making.

To add to all of the above, the company is under scrutiny for governance-related issues such as lack of board diversity as well as poor corporate culture. On the positive side, the management has announced a plan to transform its business, including appointing three new (non-Japanese) directors to its board, all due to the pressure from its largest shareholder ValueAct Capital. The Management has mentioned that they will be proposing one of the partners of ValueAct as one of the three new directors at its shareholder meeting in April 2019, which is encouraging. However, that being said, we are yet to witness any tangible improvement in the way the company has conducted itself since the exposure of its accounting fraud in 2011 and has not been able to stay free of controversy. Hence, in our opinion the hefty premium at which the shares are currently trading is not justified suggesting to us that the potential turnaround in governance quality is being priced in too fully at this point. It is uncertain what other skeletons may be in Olympus’ closets and it seems premature to afford the stock a premium valuation.

In the latest data, MVNOs (mobile virtual network operators) have reached 7.0% market share of Japan’s main 3G and LTE (4G) services with over 12m subscribers.

Government support remains robust for the MVNOs. Mr. Suga, the Chief Cabinet Secretary, has suggested that MVNOs, in all forms, should expand to 50% of the market in the future.

As Rakuten (4755 JP) prepares for its full MNO (mobile network operator) service launch later this year, the Rakuten MVNO services continues to execute well, taking market share and building a formidable foundation of subscribers. Rakuten is now Japan’s largest MVNO by customer numbers. We expect Rakuten will struggle to make a reasonable return on its MNO on a standalone basis, but it may strengthen the company’s overall ecosystem and create enough synergies to add positive value to the group.

In this version of the GER weekly events wrap, we assess the recent lock-up expiry for Pinduoduo (PDD US) which may have led to a short squeeze. Secondly, we assess the debt tender for Softbank Group (9984 JP) which may be supporting the equity. Finally, we provide updates on bids for M1 Ltd (M1 SP) and Healthscope Ltd (HSO AU) as well as update a list of upcoming M&A and equity bottom-up catalysts.

The rest of our event-driven research can be found below.

Best of luck for the new week – Rickin, Venkat and Arun

Our thesis on Subaru has maintained for some time that margins were inflated due to under-spending and that these costs would surface in one form or the other over time.

As it turns out, the costs were incurred through recalls as Subaru downgraded its FY OP guidance from ¥300bn to ¥220bn on 5 Nov. What continues to concern us is the constant stream of negative news flow on quality and sustainability-related issues. While the latest announcements do not imply excessive direct costs for the company, they continue to raise the question of whether corners were being cut and thus create doubt about the formerly excellent and still very high OPMs generated by Subaru.

We remain negative on Subaru as we expect margins to remain under pressure and believe top line may stagnate or shrink over the next one to two years.

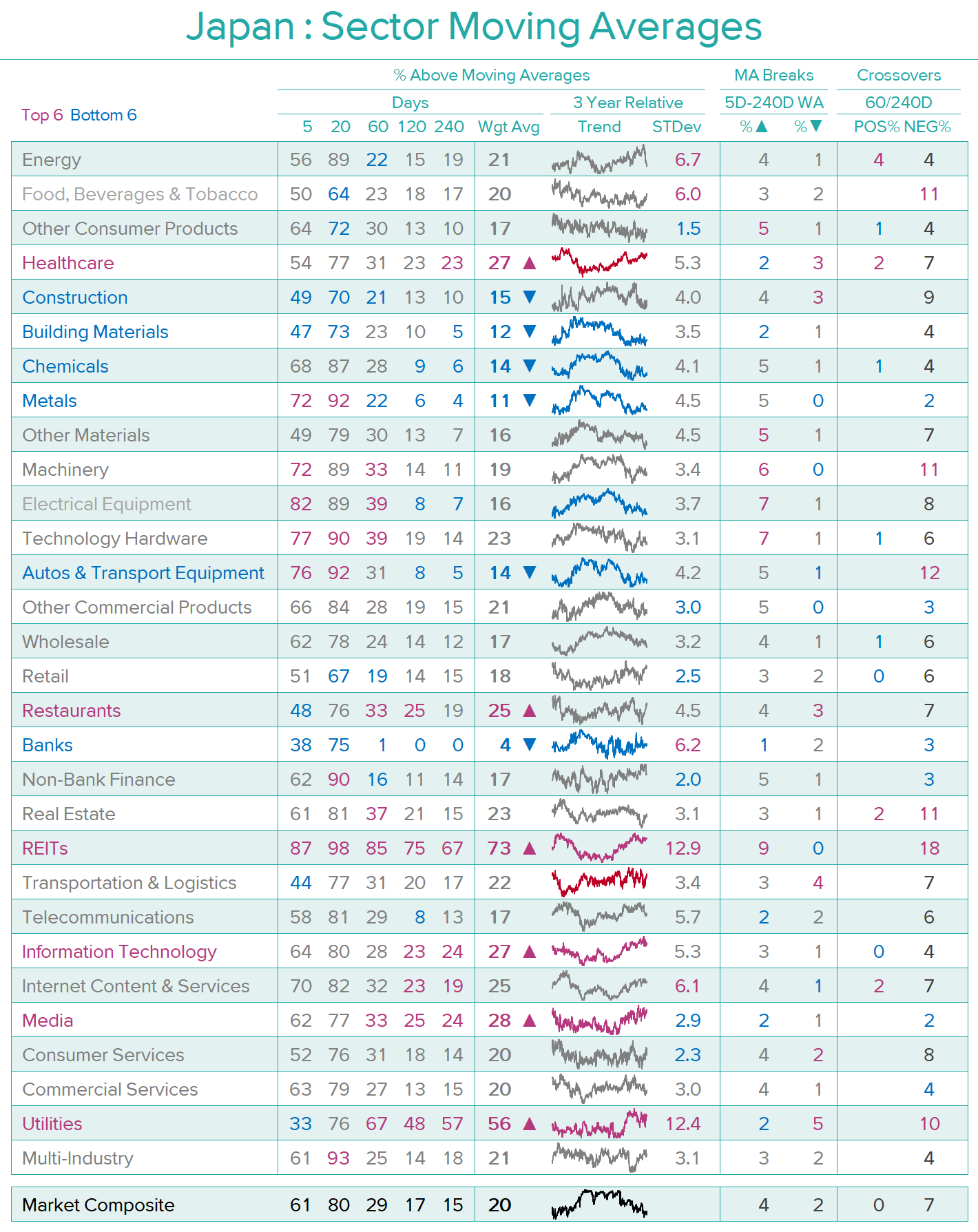

SLOW & STEADYRECOVERY – From December 25th’s lows of 8% by number and 11% by value, the percentages of Japanese stocks above the weighted sum of moving averages have continued to recover to now 19% by number and 26% by value. Total Market Value has now risen by 11.2% from the Christmas Day low and is overdue a ‘breather’.

– SECTORS –

LEGEND: The ‘sparklines’ show the three-year trend in the weighted percentage above moving average relative to the Market Composite and the ‘STDev’ column is a measure of the variability of that relative measure. The table also provides averages for the breaks above and breaks below and the positive and negative crossovers.

SECTOR BREAKDOWN – The top six sectors measured by their percentage above the weighted average of 5-240 Days remain domestic and defensive. REITs, Information Technology, Media, Healthcare and Utilities continue from our previous review with Restaurants replacing Transportation. Equally predictable is the bottom half-dozen – Banks, Autos, Metals, Building Materials, and Chemicals remain from two weeks ago, with Construction replacing Autos.

– COMPANIES –

Source: Japan Analytics

COMPANY MOVING AVERAGE OUTLIERS – As with the Market Composite and Sectors, the Moving Average Outlier indicator uses a weighted sum of each company’s share price relative to its 5-day, 20-day, 60-day, 120-day and 240-day moving averages. ‘Extreme’ values are weighted sums greater than 100% and less than -100%. We would caution that this indicator is best used for timing shorter-term reversals and, in many cases, higher highs and lower lows will be seen.

In the DETAIL section below, we highlight the current top and bottom twenty-five larger capitalisation outliers, as well as those companies that have seen the most significant positive and negative changes in their outlier percentage in the last two weeks and provide short comments on companies of particular note. UUUM (3990 JP) is currently the most ‘extreme’ positive outlier, and Welcia (3141 JP) the most ‘extreme’ negative outlier

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Mitsubishi has finally given up its hope of convincing Aeon to merge Ministop (9946 JP) with Lawson and is selling its stake in the largest retail group.

There will be no change to the extensive supply relationship between the two companies and Mitsubishi’s food wholesale arm, Mitsubishi Shokuhin (7451 JP).

While Aeon seems to have spurned Mitsubishi for now, it is hard to see how Aeon will progress in the convenience store sector without Mitsubishi’s help. In the short-term Ministop looks like a poor investment but Aeon may have to sell to Mitsubishi eventually and will want a good price for it.

Highlights of significant recent happenings include:

Substantive Deep Dive – Canada’s BlackBerry Ltd (BB CN) seeks to be the go-to provider of web Security: Why we believe investors should look at Blackberry as a way to hedge their exposures to the increasing list of companies who are susceptible to adverse impact from security breaches.

Feeding the Dragon – Chinese buying of US firms brakes abruptly, obliterating the long-term trend, and now Japan has become the second-largest market for outbound M&A globally. Also, South Korean food giant Cj Cheiljedang (097950 KS) is continuing its aggressive expansion into the U.S. market

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In December 2017, Mitsubishi UFJ Financial (8306 JP) launched a complicated three-step process to acquire up to 40%, then up to 73.8% (or more) in BDMN, five years after DBS’ aborted attempt to obtain a majority in the same bank. Mid-week, local papers announced the planned merger between BDMN and BNP with shareholder vote for both banks 26 March 2019 (record date 1 March) and effective date 1 May 2019.

It looks like this is almost completely bedded down. MUFG has a good relationship with Indonesian regulators and it would not have arrived at this Step 3 without pretty clear pre-approval indicated.

The result is an effective Tender Offer Trade at IDR 9,590/share for the float of BDMN. With shares up 8% the day of the announcement, there was another 6+% left for payment in three months and a week which comes out to 25.4% annualized in IDR terms through the close. Travis thought this is an excellent return for the risk here.

Indonesian takeover procedures generally require a Mandatory Takeover Offer procedure when someone goes over a 50% holding. But banks being bought by foreigners are a different category and bank takeovers are regulated by the OJK. The upshot is that if you tender, you will get the Tender Offer consideration. And if EVERY public shareholder tenders, MUFG will have to conduct a selldown of 7.5% within a very short period, and a selldown of 20% within 2 years or up to 5 years (a virtual IPO when it comes), in order to meet the free float requirements.

ESR has now declared its Offer for Propertylink “to be best and final“, and the Offer has been extended until the 28 February (unless further extended). After adjusting for the interim distribution of A$0.036/share (ex-date 28 December; payment 31 January), the amount payable by ESR under the Offer is A$1.164/share, cash. The Target Statement issued back on the 20 November included a “fair and reasonable” opinion from KPMG, together with unanimous PLG board support.

The next key event is CNI’s shareholder vote on the 31 January. This is not a vote to decide on tendering the shares held by CNI in PLG into ESR’s offer; but to give CNI’s board the authorisation to tender (or not to tender) its 19.5% stake in PLG.

Although no definitive decision has been made public by CNI, calling the EGM to get shareholder approval and attaching a “fair & reasonable” opinion from an independent expert (Deloitte) to CNI’s EGM notice, can be construed as sending a strong signal CNI’s board will ultimately tender in its shares. According to the AFR (paywalled), CNI’s John Mcbain said: “We want to make sure when we do decide to vote, if we get shareholder approval, the timing is with us“.

Assuming the resolution passes, CNI’s board decision on PLG shares will take place shortly afterwards. My bet is this turns unconditional the first week of Feb. The consideration under the Offer would then be paid 20 business days after the Offer becomes unconditional. Currently trading with completion in mind at a gross/annualised spread of 0.8%/6.7%, assuming payment the first week of March.

The company announced a Tender Offer to buy back 26.666mm of its own shares at a roughly 10.5% premium to last trade. That’s a big tender offer. It is ¥40bn and 29.0% of shares outstanding. Shinmaywa prepared this well because they rearranged their holding grouping to be all held under corporate entities (in many situations, they hold under personal names). For some of us, that should have been a clue.

The main purpose of this effort is to get rid of Murakami-san, but Travis’ back of the napkin suggests just a 25% gain for Murakami, which is small beer for an investor bullish on the company’s prospects.

The outright long prospects do not impress. There are a lot of companies in the market with 3+% dividend rates and low PERs which are illiquid. The company will go into a net debt situation. That will likely cap future buybacks to the limit of spending this year’s net income. That would be big, but Travis expects with a high dividend, buybacks will be less likely.

Overall the business is OK, but it is unlikely to grow dramatically enough to warrant an ROE and margins which would make a price of 1.3-1.5x book appropriate in the near-term. Travis expects the tender offer to go through, and expects the price to be a bit “sticky” at this level near-term.

Huarong-CMB network [HCN] play New Sports announced a cash or scrip offer, with the cash alternative of $0.435/share priced at a premium of 3.57% to last close. The Offeror (China Goldjoy (1282 HK) – another HCN play) has entered into an SPA to acquire 37.18% of shares out. Upon successful completion of the SPA, Goldjoy will hold 66.44% and be required to make an unconditional general offer for all remaining shares.

The key condition to the SPA is Goldjoy’s shareholder approval. This should be a simple majority and the major shareholder, Yao Jianhui, has 41.9% in Goldjoy according to HKEx and page 23 of the Offer announcement.

Despite the potential issues faced by New Sports, this is a very real deal, with financing in place for the cash option.

The idea is not a new one. The mobile telecommunications market in Japan is mature, and one of the few ways Type 1 telecom providers can grow is by adding content through the “pipes.” KDDI needs non-telecom revenue channels. KDDI has a bank, and life insurance, and some investment in asset management channels. It needs more, and better. A broker with a bank attached is a pretty good way to get long-term investment and savings products to customers.

Kabu.com is not the best one out there in terms of bang for buck. But KDDI already has a JV with kabu.com majority shareholder MUFG and another with kabu.com. If you could buy an online broker, you might choose to buy Rakuten or SBI, but you can’t. You have to buy the rest of the company with them.

Kabu.com shares were bid limit up all day long after the Nikkei article and closed at ¥462, which is a 10+ year closing high. You have to believe that KDDI is willing to pay a knock-out price to get this trade done. They may, but that is the bet. But Travis sees no impediment to the deal getting done.

Printing and HR services company and funeral parlor operator Kosaido announced that Bain Capital Private Equity would conduct an MBO on its shares via Tender Offer, with a minimum threshold for success of acquiring 66.67% of the shares outstanding. The Tender Offer commenced on 18 January and goes through 1 Mach 2019. The Tender Offer Price is ¥610/share, which is a 43.8% premium to the close of the day before the announcement and a 59.7% premium to the one-month VWAP up through the day before the announcement.

While the pretense will be that the deal is designed to grow the funeral parlor business (which, given the demographics, should be a decent business over time), this is a virtual asset strip in progress. It is the kind of thing which gives activist hedge funds a bad name, but when cloaked in the finery of “Private Equity”, it looks like renewal of a business.

It is a decent premium but an underwhelming valuation. Because of the premium, and its smallcap nature, Travis expect this gets done. If deals like this start to not get done, that would be a bullish sign. Investors will finally be taking the blinders off to unfair M&A practices.

This is a small deal. It is meaningless in the grand scheme of things. But it is a deal which should not have been done at this price because better governance would have meant the stock traded at better than 0.4x book before the announcement.

Bristol Myers Squibb Co (BMY US) announced earnings for 4Q18 this morning followed by a conference call. Most metrics beat street expectations but the withdrawal of its application for Opdivo + low-dose Yervoy for first-line (NSCLC) lung cancer patients with high tumour mutation burdens after discussions with the FDA weighed on shares of BMY today. But for arbs who have the CELG/BMY spread set up, the positive comments on the Celgene acquisition provided further assurance of BMY’s commitment to the deal.