In this briefing:

- Bank Danamon Goes Ex-Rights

- Memory Chips and the Elasticity Myth

- Hitachi Chemical (4217) Bad News All in the Price. Outlook on 12 Month View Is Bright. BUY

- Nexon M&A: Amazon & Comcast Enter the Race – It Ain’t Over Till Its Over!

- Procurri: Exit DeClout, Enter Novo Tellus. Company Remains Highly Undervalued at 4.4x 2018 EV/EBITDA

1. Bank Danamon Goes Ex-Rights

The process of the merger between Bank Danamon Indonesia (BDMN IJ) and Mitsubishi Ufj Financial (8306 JP)‘s local unit Bank Nusantara Parahyangan (BBNP IJ) is proceeding apace.

Today, the shares go ex-rights for shareholders looking to both vote on March 26th and, assuming the vote goes through, to elect to receive cash of IDR 9,590 instead of continuing to hold shares. BDMN shares are trading down, as expected.

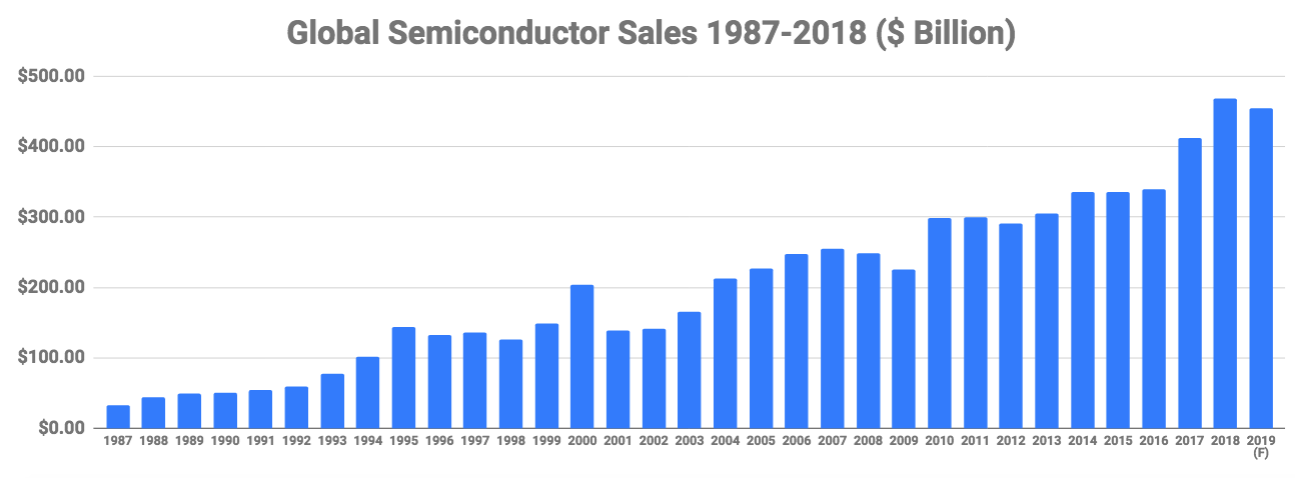

2. Memory Chips and the Elasticity Myth

During recent earnings calls memory chip makers have postulated that the market will return to higher margins once price elasticity causes demand to increase. This popular myth needs to be treated with great skepticism since, as this Insight will reveal, short-term price elasticity has a negligible impact upon memory chip sales if it has any impact at all.

3. Hitachi Chemical (4217) Bad News All in the Price. Outlook on 12 Month View Is Bright. BUY

After the recent inspection issues, the company clearly needs to tighten compliance issues and is now talking about improving profitability over the next two years by getting rid of low profit and none core businesses. Given the current valuations, the mid-term outlook and the renewed focus on profitability we would look to buy here. The internal issues that have hit the share price in the past appear behind them. We would look for an operating profit of about Y50bn to 3/20 which would put the shares on an EV/ebitda multiple of about 5x. The shares yield 3% and still trade at book.

4. Nexon M&A: Amazon & Comcast Enter the Race – It Ain’t Over Till Its Over!

In a surprising move, it was reported after the market close today that Amazon.com Inc (AMZN US) (market cap of US$804 billion) and Comcast (US$176 billion) will enter the race and have submitted initial bids to acquire Nexon Co Ltd (3659 JP)/NXC Corp.

The entrance of Amazon and Comcast is a major positive surprise and it should have a strong positive impact on Nexon’s share price. Prior to the entrance of Amazon and Comcast in this M&A battle, the market was firmly leaning towards the consortium including Tencent, Netmarble Games, and MBK Partners to acquire NXC Corp/Nexon.

Now, Amazon and Comcast’s entrance into this M&A battle has made it a lot more exciting and uncertain. Nexon Co Ltd (3659 JP)‘s share price is up 19% YTD but its share price trend has been flattening out in February. In the next few weeks, we expect further boost to Nexon’s share price (15%+), mainly because a lot more investors will think that the Tencent consortium, Amazon, and Comcast will try to pay higher price to acquire NXC Corp/Nexon. Kudos to Nexon shareholders!

5. Procurri: Exit DeClout, Enter Novo Tellus. Company Remains Highly Undervalued at 4.4x 2018 EV/EBITDA

Procurri Corporation (PROC SP) released FY18 results which showed the company growing revenues to 220M SGD (+21% vs FY17), EBITDA to 19.7M SGD (+185% vs FY17), PBT to 10.1M SGD (vs 2.3M loss in 2017) and a small net profit of 5.3M SGD which was artificially low because of an astronomical 47% tax rate. The high tax rate should reverse in 2H19 which would show the reported profitability of Procurri improve substantially.

Procurri remains deep value trading at just 4.4x 2018 EV/EBITDA and 0.4x 2018 EV/Sales. If we adjust the FY18 net profit figure(assume 30% tax rate vs 47%) the shares trade at a P/E multiple of just 13x.

The shareholder register of Procurri has seen a dramatic change YTD with multiple announcements on SGX. The most significant development is the entry of Singapore PE fund Novo Tellus acquiring a 29.6% stake on 19/2/19. Consequently this means that the biggest corporate overhang on Procurri (read: the control by Declout Ltd (DLL SP) ) is now almost over with their stake reduced to 17% from 47% previously.

Novo Tellus paid 0.33 SGD for the 29.6% stake which should now be a floor valuation for Procurri going forward.

Given the well-publicized track record of Novo Tellus at SGX listed Aem Holdings (AEM SP) the question is if Novo Tellus sees another multi-bagger in the making?

While a “10-bagger” type return like AEM is unlikely at Procurri, doubling the market cap from 90M to 180M SGD would not be impossible as Procurri continues to grow in FY19 and the depressed multiple expands modestly.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.