When the Tender Offer / MBO for Kosaido Co Ltd (7868 JP) was announced last month, my first reaction was that this was wrong. It was couched as being management-supportive, had one large independent shareholder agreeing to tender, and the it was touted as an effort to improve the printing and other “info” businesses such as staffing, and similar.

There was no mention of the fact that 94+% of the profits the last few years came from a majority stake in an external company which conducted funeral rites and services across a well-known chain of six large funeral parlours in Tokyo. Neither that company’s name nor the business segment it operates in were mentioned in the document (Japanese only) announcing the intention to conduct the MBO and if you look on the Kosaido website, you have to dig somewhat deeply to figure out that it is even a thing. In the company’s quarterly statements and semi-annual presentations of earnings, there is one line with revenues. One has to go into the fine print of the yukashoken hokokusho to discover more, and if one does, one sees that it is the profitable funeral parlour business which is effectively being purchased at 0.5x book and the rest of the company is being purchased at 1x book.

This is a virtual asset strip in progress. It is the kind of thing which gives activist hedge funds a bad name, but when cloaked in the finery of “Private Equity”, it looks like renewal of a business.

This company is an example of why investors should be spending more time on their stewardship and the governance of their portfolio companies.

It is also why investors should be taking a very close look at the METI request for public comment on what constitutes “Fair M&A.”

It is a decent premium but an underwhelming valuation. Because of the premium, and its smallcap nature, I expect this gets done.

If deals like this start to not get done, that would be a bullish sign. Investors will finally be taking the blinders off to unfair M&A practices.

Shortly afterwards, an activist did come forward. Long-time Japan activist Yoshiaki Murakami bought 5% through his entity Reno KK, and later lifted his stake (combined with affiliates) to 9.55%. I thought the stock had run too far at that point (¥775/share). While still cheap, I did not expect Bain to lift its price by 30+% and I did not expect a white knight to arrive quickly enough. This was discussed in Kosaido: Activism Drives Price 30+% Through Terms.

The New News

In the wee hours of Monday 18 February, with 11 days left to the Tender Offer, toyokeizai.net published an article (partially paywalled) suggesting that the longstanding external auditor Mr. Nakatsuji and lead shareholder Sakurai Mie (descendent of the founder of Kosaido, who originally founded a company called 桜井謄写堂 (Sakurai Transcription) in 1949, which later became Sakurai Kosaido, then just Kosaido) were against the takeover.

THAT is interesting. And the backstory here is even more interesting.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

I should have seen this coming. The asset is juicy enough, and they have a large enough stake, and the company is small enough, that this is an easy trade to do if you can get the funding. It makes eminent sense to be able to put the money down and go for it.

I have covered this minor disaster of an MBO (Management BuyOut) of Kosaido Co Ltd (7868 JP) since it was launched, with the original question of what one could do (other than refuse). Famed/notorious Japanese activist Yoshiaki Murakami and his associated companies started buying in and then the stock quickly cleared the Bain Capital Japan vehicle’s bid price. The deal was extended, then the Bain bid was raised to ¥700/share last week with the minimum threshold set at 50.01% not 66.67% but still the shares had not traded that low, and did not following the news. But Bain played chicken with Murakami and the market in its amended filing, including the words 「公開買付者は、本開買付条件の変更後の本公開買付価格を最終的なものとし、今後、本公開買付価格を一切変更しないことの決定をしております。」which roughly translates to “The Offeror, having changed the terms, has made This Tender Offer Price final, and from this point onward, has decided to absolutely not raise the Tender Offer Price.”

So now Murakami-san has launched a Tender Offer of his own. Murakami-affiliated entities Minami Aoyama Fudosan KK and Reno KK have launched a Tender Offer at ¥750/share to buy a minimum of 9,100,900 shares and a maximum of all remaining shares. The entities currently own 3,355,900 shares (13.47%) between them – up from 11.71% reported up through yesterday [as noted in yesterday’s insight, it looked likely from the volume and trading patterns prior to yesterday’s Large Shareholder Report that they had continued buying].

Buying a minimum of 9,100,900 shares at ¥750/share should be easier for Murakami-san’s bidding entity than buying a minimum of 12,456,800 shares (Bain Capital’s minimum threshold) at ¥700/share, but the Murakami TOB Tender Agent is Mita Securities, which is a lesser-known agent and it is possible that the main agent for the Bain tender (SMBC Securities) could make life difficult for its account holders.

The likelihood that Murakami-san doesn’t have his bid funded or won’t follow through is, in my eyes, effectively zero. Tender Offer announcements are vetted by both the Kanto Local Finance Bureau and the Stock Exchange. You know this has been in the works for a couple of weeks simply because of that aspect. But one of the two documents released today includes an explanation of the process Murakami-san’s companies have gone through to arrive at this bid, and that tells you it may have gone on longer.

So what next? The easy answer is there is now a put at ¥750/share. Unless there is not. Weirder things have happened.

Read on…

For Recent Insights on the Kosaido Situation Published on Smartkarma…

New York based activist investor firm Starboard Value has been intricately involved in shaping the fortunes and futures of two high profile technology companies in recent years, Marvell and Mellanox. The firm first to prominence some five years ago when they were the first among their peers to accomplish the extraordinary feat of replacing the CEO and entire board of Fortune 500 restaurant group Darden, while holding less than 10% of the company’s shares.

In the wake of their Darden coup, the firm has gone from strength to strength. To date the firm has taken positions in a total of 105 publicly listed companies, replacing or adding some 211 directors on over 60 corporate boards.

On March 7’th 2019, Starboard Value announced the acquisition of a 4% stake in US comms infrastructure firm Zayo. In the intervening period, Zayo’s share price has risen by 14% as canny investors scramble to partake in the goodness that will surely be extracted by the activist firm that simply doesn’t take no for an answer.

Itochu planned on buying 7.21 million shares out of the 75.37mm shares which bear voting rights (as of the commencement of the Tender), and 15,115,148mm shares were tendered, which led to a pro-ration rate of 47.7% which was 0.3% below my the middle of my “wide range” expected pro-ration rate of 42-54% and 0.7% beyond the 44-47% tighter range discussed in Descente Descended and Itochu Angle Is More Hostile of 28 February.

Two more central ideas were discussed in that piece:

The hostility shown by Descente management during the Tender Offer had led Itochu to abandon discussions about post-tender management until after the Tender Offer was completed. Both sides indicated a willingness to pick up where things had left off – at Descente’s request – but Descente needed to stew a bit.

The revelation by ANTA Sports in an interview with the CEO in the Nikkei in late February that ANTA supported Itochu meant that the likelihood of Itochu NOT having enough votes to put through its own slate of directors was almost zero. At a combined 47.0% of post-Tender voting rights, if 94% or less of shares were to vote, it would mean Itochu could get the majority of over 50% and determine the entire slate of directors themselves. If there was another shareholder holding a couple of percent which supported Itochu, it would be a done deal even if everyone voted. And that 2-3% existed.

So… the threat that Itochu would hold an EGM to seat new directors to oblige a stronger course for management was a very strong probability. Management who was rabidly opposed to Itochu owning the stake could not very well bow down in front of Itochu post-tender just to save its own hide – not after the employee union and the OB group came out against. President Ishimoto had effectively put himself in an untenable position unless a miracle occurred because Itochu could not legally walk away from its offer, and Ishimoto-san was bad-mouthing Itochu even as they were negotiating during the Tender Offer Period.

It was not, therefore, any surprise that President Ishimoto would step down. The surprise for me was that the news he would go came out as talks commenced over the weekend (but did not “bridge the gap” as the Nikkei reported), before we got to the first business day post-results.

Talks apparently continue with no resolution, and the media reports offer no hint as to what the issues might be.

Recent Insights on the Descente/Wacoal and Itochu/Descente Situations on Smartkarma

On November 13th last year, Linkbal Inc (6046 JP) announced it was looking to move from MOTHERS to the TSE First Section. The stock rallied. At the same time the company said that it was preparing to file an application for the move.

On March 5th, the company announced a forthcoming tachiaigai bunbai offering designed to increase the float. That tachiaigai bunbai offering (designed for retail investors only) takes place this morning after an announcement the company would oversee the offer of 970,000 shares (about 5% of the company but about 180% of the float currently held by public retail investors) at a price of ¥905/share (1,000 shares max per buyer), which is a 3% discount to yesterday’s close of ¥933 yen.

This will get it most of the way towards meeting the requirements, but likely not all the way. An inclusion is still months off. And there would likely be another sale to increase shareholder count by 800-1000 before then, whether in the form of a Public Offering/Uridashi or in the form of another tachiaigai bunbai.

Resona Holdings (8308 JP) key tactical resistance lies at 503.86, a level that if broken could spur a counter trend tactical bounce back to outlined trendline and physical resistance.

The daily cycle does show some underlying tactical support given the RSI has not confirmed recent lows. Any rally would be a counter trend move within the larger degree decline cycle. Buy volumes are not supportive in this rise (deteriorating) underscore the macro bear posture.

If the weekly cycle head and shoulders is true to course, Resona Holdings would face significant downside pressure looking ahead 2 quarters.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

New York based activist investor firm Starboard Value has been intricately involved in shaping the fortunes and futures of two high profile technology companies in recent years, Marvell and Mellanox. The firm first to prominence some five years ago when they were the first among their peers to accomplish the extraordinary feat of replacing the CEO and entire board of Fortune 500 restaurant group Darden, while holding less than 10% of the company’s shares.

In the wake of their Darden coup, the firm has gone from strength to strength. To date the firm has taken positions in a total of 105 publicly listed companies, replacing or adding some 211 directors on over 60 corporate boards.

On March 7’th 2019, Starboard Value announced the acquisition of a 4% stake in US comms infrastructure firm Zayo. In the intervening period, Zayo’s share price has risen by 14% as canny investors scramble to partake in the goodness that will surely be extracted by the activist firm that simply doesn’t take no for an answer.

Itochu planned on buying 7.21 million shares out of the 75.37mm shares which bear voting rights (as of the commencement of the Tender), and 15,115,148mm shares were tendered, which led to a pro-ration rate of 47.7% which was 0.3% below my the middle of my “wide range” expected pro-ration rate of 42-54% and 0.7% beyond the 44-47% tighter range discussed in Descente Descended and Itochu Angle Is More Hostile of 28 February.

Two more central ideas were discussed in that piece:

The hostility shown by Descente management during the Tender Offer had led Itochu to abandon discussions about post-tender management until after the Tender Offer was completed. Both sides indicated a willingness to pick up where things had left off – at Descente’s request – but Descente needed to stew a bit.

The revelation by ANTA Sports in an interview with the CEO in the Nikkei in late February that ANTA supported Itochu meant that the likelihood of Itochu NOT having enough votes to put through its own slate of directors was almost zero. At a combined 47.0% of post-Tender voting rights, if 94% or less of shares were to vote, it would mean Itochu could get the majority of over 50% and determine the entire slate of directors themselves. If there was another shareholder holding a couple of percent which supported Itochu, it would be a done deal even if everyone voted. And that 2-3% existed.

So… the threat that Itochu would hold an EGM to seat new directors to oblige a stronger course for management was a very strong probability. Management who was rabidly opposed to Itochu owning the stake could not very well bow down in front of Itochu post-tender just to save its own hide – not after the employee union and the OB group came out against. President Ishimoto had effectively put himself in an untenable position unless a miracle occurred because Itochu could not legally walk away from its offer, and Ishimoto-san was bad-mouthing Itochu even as they were negotiating during the Tender Offer Period.

It was not, therefore, any surprise that President Ishimoto would step down. The surprise for me was that the news he would go came out as talks commenced over the weekend (but did not “bridge the gap” as the Nikkei reported), before we got to the first business day post-results.

Talks apparently continue with no resolution, and the media reports offer no hint as to what the issues might be.

Recent Insights on the Descente/Wacoal and Itochu/Descente Situations on Smartkarma

On November 13th last year, Linkbal Inc (6046 JP) announced it was looking to move from MOTHERS to the TSE First Section. The stock rallied. At the same time the company said that it was preparing to file an application for the move.

On March 5th, the company announced a forthcoming tachiaigai bunbai offering designed to increase the float. That tachiaigai bunbai offering (designed for retail investors only) takes place this morning after an announcement the company would oversee the offer of 970,000 shares (about 5% of the company but about 180% of the float currently held by public retail investors) at a price of ¥905/share (1,000 shares max per buyer), which is a 3% discount to yesterday’s close of ¥933 yen.

This will get it most of the way towards meeting the requirements, but likely not all the way. An inclusion is still months off. And there would likely be another sale to increase shareholder count by 800-1000 before then, whether in the form of a Public Offering/Uridashi or in the form of another tachiaigai bunbai.

Resona Holdings (8308 JP) key tactical resistance lies at 503.86, a level that if broken could spur a counter trend tactical bounce back to outlined trendline and physical resistance.

The daily cycle does show some underlying tactical support given the RSI has not confirmed recent lows. Any rally would be a counter trend move within the larger degree decline cycle. Buy volumes are not supportive in this rise (deteriorating) underscore the macro bear posture.

If the weekly cycle head and shoulders is true to course, Resona Holdings would face significant downside pressure looking ahead 2 quarters.

Originally scheduled to close March 1st, near the end of February 2019, Bain Capital Japan’s acquisition vehicle (BCJ-34) extended the ¥610/share Tender Offer MBO deadline by 11 days from March 1st to March 11th. Of course, that was something of a moot point – by that time, the shares hadn’t traded at less than a 15% premium to terms for a week after well-known local activist Yoshiaki Murakami’s vehicle Reno KK and affiliates had taken a stake of just below 10%.

On the 8th of March, BCJ-34 raised its Tender Offer Price by 14.8% to ¥700/share and extended the Tender Offer by almost two weeks to the 25th of March. It also lowered the amount which needs to be bought to 50.1% from 66.67%. In that amended filing the buyer included words 「公開買付者は、本開買付条件の変更後の本公開買付価格を最終的なものとし、今後、本公開買付価格を一切変更しないことの決定をしております。」which roughly translates to “The Offeror, having changed the terms, has made This Tender Offer Price final, and from this point onward, has decided to absolutely not raise the Tender Offer Price.”

That’s that, but since then, the shares have not traded as low as the newly raised Tender Offer Price.

With one week to go, Aoyama Fudosan yesterdat announced it had lifted its stake to 747,800 shares or 3.00% of shares out, which brings the combined Reno KK/Aoyama Fudosan stake to 11.71%.

Given the 1.1mm shares traded since the 11th (i.e. shares which if Murakami-san had bought he would not have to report until the 19th (today)) and that the share price was up sharply in decent volume this afternoon, it would not be difficult to imagine a higher stake being reported in the days ahead.

Murakami-san is not going away. This is starting to look a bit like another Murakami situation of recent. And that one turned out well.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Carlyle, along with SBI, plans to sell the rest of its stake in Aruhi Corp (7198 JP) for around US$280m.

Aruhi listed in Dec 2017, when Carlyle sold 18m shares. This is the second and final tranche of shares owned by Carlyle. The total sale accounts for 41% of the company’s outstanding shares making it a relatively large deal to digest.

However, the shares have done well since listing and the stock scores well on our framework. Valuations appear reasonable, if the company is able to achieve its mid-term targets.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The declining and ageing population in Japan has been a major cause for concern to many Japanese companies.

Fancl Corp (4921 JP), is a relatively small player in the Japanese cosmetics and nutritional supplements space who is expected to benefit from the declining and ageing population.

Compared to the peer average, EV/Sales discount narrowed down significantly over the course of the last year. But we believe the discount remains the same on a growth adjusted basis.

Still too small for institutional investors to notice. But we expect them to start noticing the company over the coming years.

One of the cheapest stocks on a long term forward multiple, as we expect FANCL to sustain its high growth over a long period of time.

We are not sure if Fancl Corp (4921 JP) can ever be in the same league as Shiseido or Kao, but we certainly believe the company doesn’t deserve to be about 10% of the size of Shiseido. Thus, we have a very long-term bullish view on FANCL and expect to see the company’s market cap to double over the next 5-7 years

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The declining and ageing population in Japan has been a major cause for concern to many Japanese companies.

Fancl Corp (4921 JP), is a relatively small player in the Japanese cosmetics and nutritional supplements space who is expected to benefit from the declining and ageing population.

Compared to the peer average, EV/Sales discount narrowed down significantly over the course of the last year. But we believe the discount remains the same on a growth adjusted basis.

Still too small for institutional investors to notice. But we expect them to start noticing the company over the coming years.

One of the cheapest stocks on a long term forward multiple, as we expect FANCL to sustain its high growth over a long period of time.

We are not sure if Fancl Corp (4921 JP) can ever be in the same league as Shiseido or Kao, but we certainly believe the company doesn’t deserve to be about 10% of the size of Shiseido. Thus, we have a very long-term bullish view on FANCL and expect to see the company’s market cap to double over the next 5-7 years

On Thursday the 14th Feb 2019, Pepper Food Service (3053 JP) announced its results for FY2018 and the guidance for both 1HFY2019 and FY2019. The company managed to grow its revenue by an impressive 75.3% YoY outperforming its own estimate by 6.4%.

However, the gross profit only grew by 69.9% during the year as the gross margin slipped 137bps in FY2018 driven by higher energy prices and wages. Higher wages were due to active recruitment of foreign workers within the food service industry which created a supply shortage. To tackle increasing costs, towards the end of the year, Ikinari Steak restaurants increased the prices of its steak. We believe the margin recovery witnessed in 4Q2018 was a direct result of this price increase.

Gross Margin Showing Signs of Recovery

Source: Company Disclosures

Pepper Food Services saw its EBIT margin decline by 20bps to 6.1% in FY2018, as revenue growth offset most of the gross margin drop through gains from operating leverage. However, its restaurants in New York City continued to underperform. The company expected those restaurants to turn a corner and start contributing to the overall EBIT from FY2018, however, those restaurants failed miserably and continued to drag the overall EBIT margin down. Hence, the company failed to meet its EBIT margin forecast with EBIT falling 4.6% short of company guidance.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Itochu planned on buying 7.21 million shares out of the 75.37mm shares which bear voting rights (as of the commencement of the Tender), and 15,115,148mm shares were tendered, which led to a pro-ration rate of 47.7% which was 0.3% below my the middle of my “wide range” expected pro-ration rate of 42-54% and 0.7% beyond the 44-47% tighter range discussed in Descente Descended and Itochu Angle Is More Hostile of 28 February.

Two more central ideas were discussed in that piece:

The hostility shown by Descente management during the Tender Offer had led Itochu to abandon discussions about post-tender management until after the Tender Offer was completed. Both sides indicated a willingness to pick up where things had left off – at Descente’s request – but Descente needed to stew a bit.

The revelation by ANTA Sports in an interview with the CEO in the Nikkei in late February that ANTA supported Itochu meant that the likelihood of Itochu NOT having enough votes to put through its own slate of directors was almost zero. At a combined 47.0% of post-Tender voting rights, if 94% or less of shares were to vote, it would mean Itochu could get the majority of over 50% and determine the entire slate of directors themselves. If there was another shareholder holding a couple of percent which supported Itochu, it would be a done deal even if everyone voted. And that 2-3% existed.

So… the threat that Itochu would hold an EGM to seat new directors to oblige a stronger course for management was a very strong probability. Management who was rabidly opposed to Itochu owning the stake could not very well bow down in front of Itochu post-tender just to save its own hide – not after the employee union and the OB group came out against. President Ishimoto had effectively put himself in an untenable position unless a miracle occurred because Itochu could not legally walk away from its offer, and Ishimoto-san was bad-mouthing Itochu even as they were negotiating during the Tender Offer Period.

It was not, therefore, any surprise that President Ishimoto would step down. The surprise for me was that the news he would go came out as talks commenced over the weekend (but did not “bridge the gap” as the Nikkei reported), before we got to the first business day post-results.

Talks apparently continue with no resolution, and the media reports offer no hint as to what the issues might be.

Recent Insights on the Descente/Wacoal and Itochu/Descente Situations on Smartkarma

On November 13th last year, Linkbal Inc (6046 JP) announced it was looking to move from MOTHERS to the TSE First Section. The stock rallied. At the same time the company said that it was preparing to file an application for the move.

On March 5th, the company announced a forthcoming tachiaigai bunbai offering designed to increase the float. That tachiaigai bunbai offering (designed for retail investors only) takes place this morning after an announcement the company would oversee the offer of 970,000 shares (about 5% of the company but about 180% of the float currently held by public retail investors) at a price of ¥905/share (1,000 shares max per buyer), which is a 3% discount to yesterday’s close of ¥933 yen.

This will get it most of the way towards meeting the requirements, but likely not all the way. An inclusion is still months off. And there would likely be another sale to increase shareholder count by 800-1000 before then, whether in the form of a Public Offering/Uridashi or in the form of another tachiaigai bunbai.

Resona Holdings (8308 JP) key tactical resistance lies at 503.86, a level that if broken could spur a counter trend tactical bounce back to outlined trendline and physical resistance.

The daily cycle does show some underlying tactical support given the RSI has not confirmed recent lows. Any rally would be a counter trend move within the larger degree decline cycle. Buy volumes are not supportive in this rise (deteriorating) underscore the macro bear posture.

If the weekly cycle head and shoulders is true to course, Resona Holdings would face significant downside pressure looking ahead 2 quarters.

Originally scheduled to close March 1st, near the end of February 2019, Bain Capital Japan’s acquisition vehicle (BCJ-34) extended the ¥610/share Tender Offer MBO deadline by 11 days from March 1st to March 11th. Of course, that was something of a moot point – by that time, the shares hadn’t traded at less than a 15% premium to terms for a week after well-known local activist Yoshiaki Murakami’s vehicle Reno KK and affiliates had taken a stake of just below 10%.

On the 8th of March, BCJ-34 raised its Tender Offer Price by 14.8% to ¥700/share and extended the Tender Offer by almost two weeks to the 25th of March. It also lowered the amount which needs to be bought to 50.1% from 66.67%. In that amended filing the buyer included words 「公開買付者は、本開買付条件の変更後の本公開買付価格を最終的なものとし、今後、本公開買付価格を一切変更しないことの決定をしております。」which roughly translates to “The Offeror, having changed the terms, has made This Tender Offer Price final, and from this point onward, has decided to absolutely not raise the Tender Offer Price.”

That’s that, but since then, the shares have not traded as low as the newly raised Tender Offer Price.

With one week to go, Aoyama Fudosan yesterdat announced it had lifted its stake to 747,800 shares or 3.00% of shares out, which brings the combined Reno KK/Aoyama Fudosan stake to 11.71%.

Given the 1.1mm shares traded since the 11th (i.e. shares which if Murakami-san had bought he would not have to report until the 19th (today)) and that the share price was up sharply in decent volume this afternoon, it would not be difficult to imagine a higher stake being reported in the days ahead.

Murakami-san is not going away. This is starting to look a bit like another Murakami situation of recent. And that one turned out well.

On March 6th, a day before the Hitachi Ltd (6501 JP) Taiwan elevator business Tender Offer for just over a third of Yungtay Engineering (1507 TT) was expected to close, the closing date was extended to 22 April, notably because the acquiring entity had not yet received Taiwan Ministry of Economy Investment Commission approval for the foreign investment, and the Fair Trading Commission had not yet given the green light, so there was no hope of getting it done by the next day in accordance with Taiwan’s Public Acquisition of Public Company Shares Administrative Law Article 18 Para 2. The proposed purchase price was unchanged at NT$60.

While there have been noises in the market that both Otis and Schindler, which are reported to hold roughly 5-6% each (last year’s shareholder list included UT Park View which United Technologies (UTX US)‘s 10-K showed was a wholly-owned sub) were willing to offer more than Hitachi’s offered NT$60 (and MOPS filings indicate the board approval meeting in end-January referenced a NT$63 potential bid), there was no competitive bid made public and to the authorities by five business days prior to the first bid close (which would have been 26 Feb) as per the same law Article 7 Para 2.

Since then, there have also been other ructions. While terms remain unchanged, it is worthwhile looking into what has been going on. This is still interesting and because of its various inputs, slightly disconcerting to some, and the modalities continue to surprise me.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Musashino Bank (8336 JP) was one of the last regional banks to announce 3Q FY3/2019 results, and they were a nasty surprise: a consolidated net loss for the nine months to 31 December 2018, caused by heavy reserving in Q3 (October-December 2018) against the bank’s exposure to the troubled Akebono Brake Industry Co (7238 JP) . While the bank has slashed its full-year net profit guidance from ¥11.1 billion to ¥4.5 billion, this would still require an heroic level of profits in Q4 which the bank has never before achieved. The share price has fallen over 31% in the last twelve months. Valuations at current levels are still high (FY3/2019 PER is 17.6x) and we consider the share price to be vulnerable to further weakness. Caveat emptor (May the buyer beware) !

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Musashino Bank (8336 JP) was one of the last regional banks to announce 3Q FY3/2019 results, and they were a nasty surprise: a consolidated net loss for the nine months to 31 December 2018, caused by heavy reserving in Q3 (October-December 2018) against the bank’s exposure to the troubled Akebono Brake Industry Co (7238 JP) . While the bank has slashed its full-year net profit guidance from ¥11.1 billion to ¥4.5 billion, this would still require an heroic level of profits in Q4 which the bank has never before achieved. The share price has fallen over 31% in the last twelve months. Valuations at current levels are still high (FY3/2019 PER is 17.6x) and we consider the share price to be vulnerable to further weakness. Caveat emptor (May the buyer beware) !

COMPREHENSIVE INCOME – Since 2011, a Statement of Comprehensive Income (CSI) has been a mandatory addition to the Income Statement for Japanese companies reporting under Japanese GAAP (J-GAAP). CSI has long been a part of US-GAAP and is also an integral part of the IFRS reporting standards. A critical difference is that under J-GAAP, items of Other Comprehensive Income (OCI) are added or subtracted from Net Assets and do not impact Shareholder’s Equity which is the denominator for Return on Equity (RoE). Under US-GAAP and IFRS the amounts are deducted from Shareholder’s Equity and, therefore, as an increasing number of Japanese companies are switching to IFRS, these items cannot be ignored and can often lead to significant changes in RoE calculations.

VALUATION DIFFERENCES – In an earlier Insight Japan: What to Buy & Sell if the ¥ Rises to 90, we used the Foreign Currency Translation Adjustment item in Other Comprehensive Income to determine companies’ sensitivity to changes in exchange rates. In this Insight, we look at the Valuation Differences item which is more fully described as “Unrealised Gains/Losses on Available-for-Sale Securities”. With many Japanese companies running in effect long/short equity funds (see our recent Insight on Toppan Printing: Money for Nothing), the quarterly portfolio ‘marks’ are a useful performance update. The extent to which shareholders should condone these efforts at ‘cash management’ is a wider topic which has been covered by Travis Lundy. Some companies, such as Tokyo Broadcasting System (9401 JP), have already seen ‘attention’ from activist investors, while others, such as Toyota Industries (6201 JP) and Japan Petroleum Exploration (1662 JP), feature in the Smartkarma HoldCo Monitor and are familiar to this audience. For the others, at the very least, we can start the exercise of ‘naming and shaming’ to encourage more scrutiny in the future.

Source: Japan Analytics

WORST QUARTER FOR VALUATION DIFFERENCES SINCE FY2017 Q2 – The aggregate of the Valuation Differences for all 3,574 listed non-financial companies for the most recent quarter was -¥85b, the worst result since 2017 Q2. As not all of the securities valued are domestic equity, the correlation with the Japanese equity market is not exact and movements in the US$/¥ exchange rate also play a role. Only a small percentage of companies have significant valuation differences. In the most recent quarter, only 29 companies saw a positive change of more than ¥1b. However, 637 saw a negative change or at least -¥1b. In the DETAIL section below we shall look at the top twenty-five companies by negative and positive change relative to both shareholder’s equity and market capitalisation and make some brief comments on a number of companies, including Japan Petroleum Exploration (1662 JP), Tokyo Broadcasting System (9401 JP), Toyota Industries (6201 JP), Mitsubishi Materials (5711 JP) , Vital KSK (3151 JP), Bank Of Kyoto (8369 JP), Toppan Printing (7911 JP), and Inabata (8098 JP).

SHAREHOLDER ACTION REQUIRED – A large number of Japanese companies continue to hold large investment portfolios and the various iterations of Japan’s Corporate Governance Code have tried to nudge companies towards reducing such holdings. The latest version which was released in June 2018 and was well-covered by Travis Lundy in his excellent Insight – Japan’s Corporate Governance Code Amendments – A Much Bigger Stick for Activists and Stewards. The relevant provision is as follows: –

Source: Tokyo Stock Exchange -Japan’s Corporate Governance Code

As Travis then noted: –

This is Big News. It means there is considerable friction, and explanatory embarrassment, in continuing to hold cross-holdings.

Every year requires a reassessment of the financial benefits and the return on capital measured against the cost of capital. This will not be pretty.

Requiring a set of policies on voting shares probably means setting standards which would not be lesser than the standards they adhere to in their own business. And it would require the possibility they might vote against management.

It would be much easier to just get rid of the Cross-Shareholdings. The boards of the major banks, which each hold hundreds of cross-shareholding positions, will need to reassess each of the positions on an economic basis and business basis every single year. Expect this to change quickly. This is the perfect excuse for banks and corporates to say “Shōganai”, and sell.

SO FAR, NOT MUCH – In the seven months the revised code has been in effect, this ‘bigger stick’ has yielded few results as companies continue to hold onto their portfolios and file ‘boilerplate’ statements in the Corporate Governance filings. The author and leading promoter of the Governance Code, Nicholas Benes, has just made an interesting proposal on his blog entitled How to Demolish Japan’s Wall of Yes-Man Allegiant Shareholders which we have reproduced in full at the end of the DETAIL section below.

We recommend that all institutional shareholders of Japanese equities take note and follow Mr Benes’ suggestion to vote against the two most senior executive directors (usually, the CEO and Chairman) up for re-election if the total “policy shareholdings” held by a company exceed 25% of the amount of net assets less cash.

PEAK CYCLE EARNINGS – In our Winter Results & Revisions Flash Insight of yesterday, we noted that Japanese listed corporate earnings, after nine consecutive ‘up’ quarters, peaked on December 26th, two days before the market reached a twenty-month low having declined 22.5% in the preceding three months. Forecast earnings peaked on November 7th and have led reported earnings to the downside since August last year.

Source: Japan Analytics

ONE-YEAR LAG – Reported and forecast earnings are a lagging indicator and, in this instance, lagged by just under one year. Our preferred leading indicator, the Results & Revision Score which includes earnings momentum factors, peaked on 11th November 2017, 44 trading days ahead of the peak in the Market Composite. As of Friday’s close and with 99% of this quarters’ announcements made, the Results & Revisions Score is at a new 21-month. The score has now fallen by 70% and has halved since October 26th last year. We will cover the outlook in more detail in our upcoming quarterly Results and Revision review. However, the last two cycles (2009 and 2016) saw ‘trough’ scores of -9.6 and -2.1, respectively. There is ample room on the downside as export volumes continue to decline and the increase in the consumption tax in October tips Japan into a recession by year-end.

Source: Japan Analytics

SIDEWAYS – The market has moved sideways through the reporting window rising 0.7% in Yen terms and falling 0.7% in US$ terms. The weakness in the currency has helped offset the slide in profits.

MARKET/SECTOR STRATEGY- We continue to recommend an underweight position in Japan in global portfolios and favour undervalued domestically-orientated companies in the Information Technology, Internet, Media, and Telecommunications sectors. We would avoid or short the financial sectors Banks, Non-Bank Finance and Multi-Industry (Japan Post). We would underweight the Auto and Other Consumer Products sectors as consumer spending contracts further in the US, Europe, China and in Japan later in the year.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Musashino Bank (8336 JP) was one of the last regional banks to announce 3Q FY3/2019 results, and they were a nasty surprise: a consolidated net loss for the nine months to 31 December 2018, caused by heavy reserving in Q3 (October-December 2018) against the bank’s exposure to the troubled Akebono Brake Industry Co (7238 JP) . While the bank has slashed its full-year net profit guidance from ¥11.1 billion to ¥4.5 billion, this would still require an heroic level of profits in Q4 which the bank has never before achieved. The share price has fallen over 31% in the last twelve months. Valuations at current levels are still high (FY3/2019 PER is 17.6x) and we consider the share price to be vulnerable to further weakness. Caveat emptor (May the buyer beware) !

COMPREHENSIVE INCOME – Since 2011, a Statement of Comprehensive Income (CSI) has been a mandatory addition to the Income Statement for Japanese companies reporting under Japanese GAAP (J-GAAP). CSI has long been a part of US-GAAP and is also an integral part of the IFRS reporting standards. A critical difference is that under J-GAAP, items of Other Comprehensive Income (OCI) are added or subtracted from Net Assets and do not impact Shareholder’s Equity which is the denominator for Return on Equity (RoE). Under US-GAAP and IFRS the amounts are deducted from Shareholder’s Equity and, therefore, as an increasing number of Japanese companies are switching to IFRS, these items cannot be ignored and can often lead to significant changes in RoE calculations.

VALUATION DIFFERENCES – In an earlier Insight Japan: What to Buy & Sell if the ¥ Rises to 90, we used the Foreign Currency Translation Adjustment item in Other Comprehensive Income to determine companies’ sensitivity to changes in exchange rates. In this Insight, we look at the Valuation Differences item which is more fully described as “Unrealised Gains/Losses on Available-for-Sale Securities”. With many Japanese companies running in effect long/short equity funds (see our recent Insight on Toppan Printing: Money for Nothing), the quarterly portfolio ‘marks’ are a useful performance update. The extent to which shareholders should condone these efforts at ‘cash management’ is a wider topic which has been covered by Travis Lundy. Some companies, such as Tokyo Broadcasting System (9401 JP), have already seen ‘attention’ from activist investors, while others, such as Toyota Industries (6201 JP) and Japan Petroleum Exploration (1662 JP), feature in the Smartkarma HoldCo Monitor and are familiar to this audience. For the others, at the very least, we can start the exercise of ‘naming and shaming’ to encourage more scrutiny in the future.

Source: Japan Analytics

WORST QUARTER FOR VALUATION DIFFERENCES SINCE FY2017 Q2 – The aggregate of the Valuation Differences for all 3,574 listed non-financial companies for the most recent quarter was -¥85b, the worst result since 2017 Q2. As not all of the securities valued are domestic equity, the correlation with the Japanese equity market is not exact and movements in the US$/¥ exchange rate also play a role. Only a small percentage of companies have significant valuation differences. In the most recent quarter, only 29 companies saw a positive change of more than ¥1b. However, 637 saw a negative change or at least -¥1b. In the DETAIL section below we shall look at the top twenty-five companies by negative and positive change relative to both shareholder’s equity and market capitalisation and make some brief comments on a number of companies, including Japan Petroleum Exploration (1662 JP), Tokyo Broadcasting System (9401 JP), Toyota Industries (6201 JP), Mitsubishi Materials (5711 JP) , Vital KSK (3151 JP), Bank Of Kyoto (8369 JP), Toppan Printing (7911 JP), and Inabata (8098 JP).

SHAREHOLDER ACTION REQUIRED – A large number of Japanese companies continue to hold large investment portfolios and the various iterations of Japan’s Corporate Governance Code have tried to nudge companies towards reducing such holdings. The latest version which was released in June 2018 and was well-covered by Travis Lundy in his excellent Insight – Japan’s Corporate Governance Code Amendments – A Much Bigger Stick for Activists and Stewards. The relevant provision is as follows: –

Source: Tokyo Stock Exchange -Japan’s Corporate Governance Code

As Travis then noted: –

This is Big News. It means there is considerable friction, and explanatory embarrassment, in continuing to hold cross-holdings.

Every year requires a reassessment of the financial benefits and the return on capital measured against the cost of capital. This will not be pretty.

Requiring a set of policies on voting shares probably means setting standards which would not be lesser than the standards they adhere to in their own business. And it would require the possibility they might vote against management.

It would be much easier to just get rid of the Cross-Shareholdings. The boards of the major banks, which each hold hundreds of cross-shareholding positions, will need to reassess each of the positions on an economic basis and business basis every single year. Expect this to change quickly. This is the perfect excuse for banks and corporates to say “Shōganai”, and sell.

SO FAR, NOT MUCH – In the seven months the revised code has been in effect, this ‘bigger stick’ has yielded few results as companies continue to hold onto their portfolios and file ‘boilerplate’ statements in the Corporate Governance filings. The author and leading promoter of the Governance Code, Nicholas Benes, has just made an interesting proposal on his blog entitled How to Demolish Japan’s Wall of Yes-Man Allegiant Shareholders which we have reproduced in full at the end of the DETAIL section below.

We recommend that all institutional shareholders of Japanese equities take note and follow Mr Benes’ suggestion to vote against the two most senior executive directors (usually, the CEO and Chairman) up for re-election if the total “policy shareholdings” held by a company exceed 25% of the amount of net assets less cash.

PEAK CYCLE EARNINGS – In our Winter Results & Revisions Flash Insight of yesterday, we noted that Japanese listed corporate earnings, after nine consecutive ‘up’ quarters, peaked on December 26th, two days before the market reached a twenty-month low having declined 22.5% in the preceding three months. Forecast earnings peaked on November 7th and have led reported earnings to the downside since August last year.

Source: Japan Analytics

ONE-YEAR LAG – Reported and forecast earnings are a lagging indicator and, in this instance, lagged by just under one year. Our preferred leading indicator, the Results & Revision Score which includes earnings momentum factors, peaked on 11th November 2017, 44 trading days ahead of the peak in the Market Composite. As of Friday’s close and with 99% of this quarters’ announcements made, the Results & Revisions Score is at a new 21-month. The score has now fallen by 70% and has halved since October 26th last year. We will cover the outlook in more detail in our upcoming quarterly Results and Revision review. However, the last two cycles (2009 and 2016) saw ‘trough’ scores of -9.6 and -2.1, respectively. There is ample room on the downside as export volumes continue to decline and the increase in the consumption tax in October tips Japan into a recession by year-end.

Source: Japan Analytics

SIDEWAYS – The market has moved sideways through the reporting window rising 0.7% in Yen terms and falling 0.7% in US$ terms. The weakness in the currency has helped offset the slide in profits.

MARKET/SECTOR STRATEGY- We continue to recommend an underweight position in Japan in global portfolios and favour undervalued domestically-orientated companies in the Information Technology, Internet, Media, and Telecommunications sectors. We would avoid or short the financial sectors Banks, Non-Bank Finance and Multi-Industry (Japan Post). We would underweight the Auto and Other Consumer Products sectors as consumer spending contracts further in the US, Europe, China and in Japan later in the year.

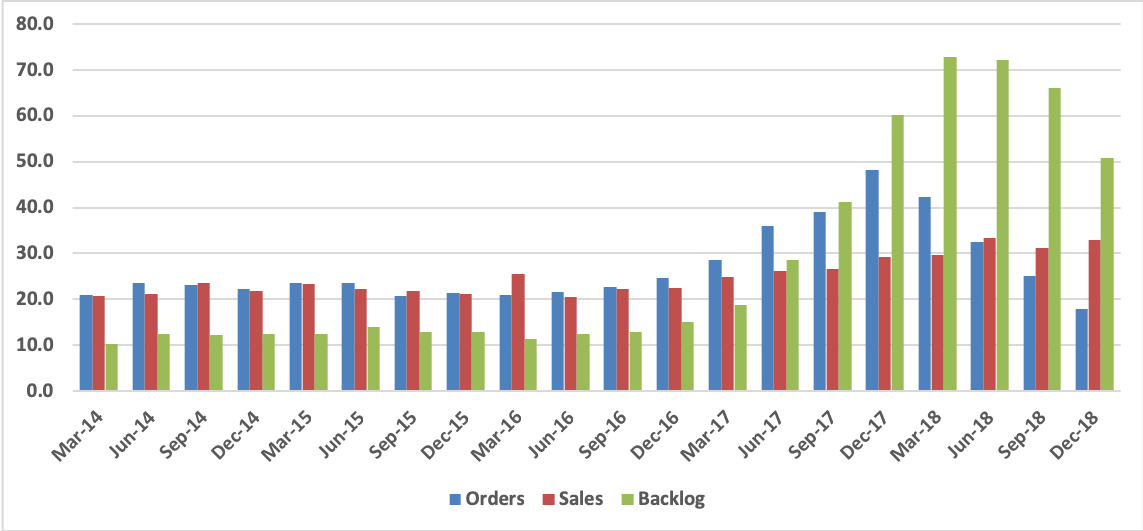

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.