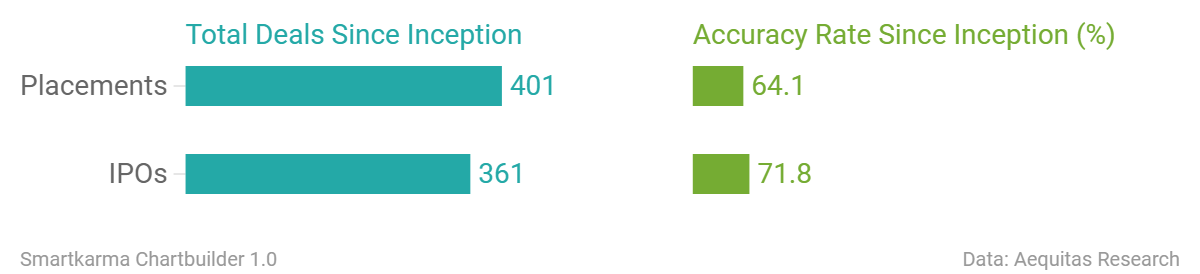

In this briefing:

- Futu Holdings Pre-IPO – Great Metrics but in a Commoditised Industry

- China Tobacco International IPO: Heavy Regulation, Declining Margins – A Bit Late to IPO Party

- Futu Holdings IPO Preview: Running Out of Steam

- IPO Radar: AutoCorp, Honda’s Avatar in Thailand

1. Futu Holdings Pre-IPO – Great Metrics but in a Commoditised Industry

Futu Holdings Ltd (FHL US) plans to raise around US$300m in its US IPO. The company is backed by Tencent Holdings (700 HK) , Matrix Partners and Sequoia, who together own over 45% of the company.

The founding team comes mostly from Tencent, which might explain Tencent’s large stake in the company. Growth for the company has been stupendous despite the jittery markets, with margin financing adding to the top-line growth.

While its low costs will help it to steal clients from the more traditional brokers, other new low-cost brokers seem to be offering similar services at comparable rates. In addition, the company is not licensed or regulated by any entities in China, despite the majority of its client base being Chinese nationals. Furthermore, the company plans to expand into newer overseas market where it doesn’t seem to have much of a cost advantage.

2. China Tobacco International IPO: Heavy Regulation, Declining Margins – A Bit Late to IPO Party

China Tobacco International (GHALPZ CH) is a subsidiary and offshore unit of China National Tobacco Corp., a state-owned enterprise (SOE). The company procures tobacco leaves from regions around the world and exports tobacco leaf products and branded cigarettes to the duty-free outlets outside China’s customs area and in Southeast Asia.

The IPO is expected to raise US$100M and the company expects to use the proceeds to expand market share, acquire new cigarette brands, working capital, and other corporate purposes.

3. Futu Holdings IPO Preview: Running Out of Steam

Futu Holdings Ltd (FHL US) is the fourth largest online broker in Hong Kong. Futu has filed for a Nasdaq IPO to raise $300 million, down from an earlier indication of a $500 million raise according to press reports. Futu is backed by Tencent Holdings (700 HK) (38.2% shareholder), Matrix Partners (6.1%) and Sequoia Capital (4.0%).

At first glance, Futu appears to be a winning new economy company as its rapid revenue growth has been accompanied by rising margins. However, on closer inspection, we believe that Futu’s fundamentals are at best mixed.

4. IPO Radar: AutoCorp, Honda’s Avatar in Thailand

In August 2017, Honda stole the top spot in Thai passenger cars from Toyota and held it for a few months. They are still formidable players, and ACG (AutoCorp) which runs Honda dealerships and service centers across Thailand, is expected to IPO some time in 2019. Here’s our quick look at the company.

- We value this IPO at Bt2/sh using DCF, since there’s really no good comparables. The company is expected to enjoy slower revenue growth and higher margins going forward as car sales slow down nationally and maintenance becomes a bigger chunk of the revenues.

- They only operate in four provinces and run 8 showrooms with over 6,000 sqm of display space. The service centers account for almost 17,200 sqm. The big chunk comes from lower margin car sales. Along with accessories, these account for 84% of revenues.

- The IPO is firmly underwritten by Singapore’s Phillips Securities and is good for more than a quarter of shares outstanding (26%). The founding Rangkanuwat family control all remaining shares and have committed to 6 month lock-up period.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.