Tracking Traffic/Chinese Express & Logistics is the hub for our research on China’s express parcels and logistics sectors. Tracking Traffic/Chinese Express & Logistics features analysis of monthly Chinese express and logistics data, notes from our conversations with industry players, and links to company and thematic notes.

This month’s issue covers the following topics:

December express parcel pricing fell by over 9% Y/Y. Average pricing per express parcel fell by 9.1% Y/Y, the worst decline since Q216 (excluding January/February figures distorted by the Lunar New Year holiday).

Express parcel revenue growth remained well below 20% last month. Weak pricing dragged sector revenue growth down to 17% in December, the 4th consecutive month of sub-20% growth.

Intra-city pricing (ie, local delivery) was strong in 2018. Relative to weak inter-city pricing (down 3.1% Y/Y in 2018), pricing for intra-city express shipments was firm, rising by 0.1% last year. In fact, average pricing for intra-city express shipments has risen in four of the last five years.

Underlying domestic transport demand remained firm in December. Although demand for inter-city express shipments appears to be moderating (from high levels), underlying transportation activity in December remained firm. The three modes of freight transport we track (rail, highway, air) in aggregate rose 6.6% Y/Y in December, even as the growth of air freight slowed.

We retain a negative view of China’s express industry’s fundamentals: demand growth is slowing and pricing for inter-city shipments appears to be falling faster than costs can be cut, leading to margin compression.

Local institutions are busy scooping up Hyosung Corporation (004800 KS) shares lately. The owner risk is now gone. There are increasing signs of improving fundamentals on all of the four major subs. Some are already expecting ₩5,000 per share. This is a 9.2% annual div yield at the last closing price.

Discount is also attractive. It is now at 46% to NAV. With this much div yield, discount should be much below the local peer average of 40%.

I’d continue to long Holdco. Hedge would be tricky. Heavy is up 15% YTD. I admit that there is no clear cointegrated relationship between them. But Heavy’s recent rally is more of a speculative money pushing up on the hydrogen vehicle theme. I’d pick Heavy for a hedge.

Ecopro BM Co Ltd (247540 KS) specializes in making cathode active materials for rechargeable batteries that are used in EVs and electrical energy storage systems (ESS). Ecopro BM Co Ltd (247540 KS) is expected to complete its IPO in late February 2019. The institutional book building starts on February 14th, 2019. The IPO deal base size ranges from $96 million to $115 million. According to the bankers’ valuation, the expected market cap after the IPO would range from 796 billion won to 957 billion won.

The bankers selected two stocks including L&F Co Ltd (066970 KS) and Cosmoam&T (005070 KS) as comparable companies to Ecopro BM. An IPO discount of 27.2% to 36.4%, the bankers derived an IPO price range of 37,500 – 42,900 won. The company’s sales and profits have been surging in the past three years. In 1Q-3Q18, it generated sales of 406 billion won (up 107.6% YoY) and operating profit of 36.1 billion won (up 108.5% YoY).

Ecopro BM has the second largest market share in the world after Sumitomo in the NCA high nickel-based cathode materials. Ecopro BM’s major customers include Samsung SDI and Murata Manufacturing Plant (TMM) (Japan).

Mitsubishi has finally given up its hope of convincing Aeon to merge Ministop (9946 JP) with Lawson and is selling its stake in the largest retail group.

There will be no change to the extensive supply relationship between the two companies and Mitsubishi’s food wholesale arm, Mitsubishi Shokuhin (7451 JP).

While Aeon seems to have spurned Mitsubishi for now, it is hard to see how Aeon will progress in the convenience store sector without Mitsubishi’s help. In the short-term Ministop looks like a poor investment but Aeon may have to sell to Mitsubishi eventually and will want a good price for it.

The supermarket sector is the most fragmented and uncompetitive of all retail sectors, a situation encouraged by major suppliers and not ideal for consumers.

Despite some effort from the likes of Aeon, consolidation has failed to materialise beyond a few in-group mergers.

Yet pressure on supermarkets to consolidate has been building due to depopulation in the regions, competitive pressures from other food retailers such as convenience stores and drugstore chains, as well as the emerging online food services.

Change is now coming. The biggest industry consolidation yet was announced last month, a precedent-setting alliance between three major supermarkets, Arcs Co Ltd (9948 JP), Valor Holdings (9956 JP) and Retail Partners (8167 JP), carving up a large chunk of the country into three regional fiefdoms.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

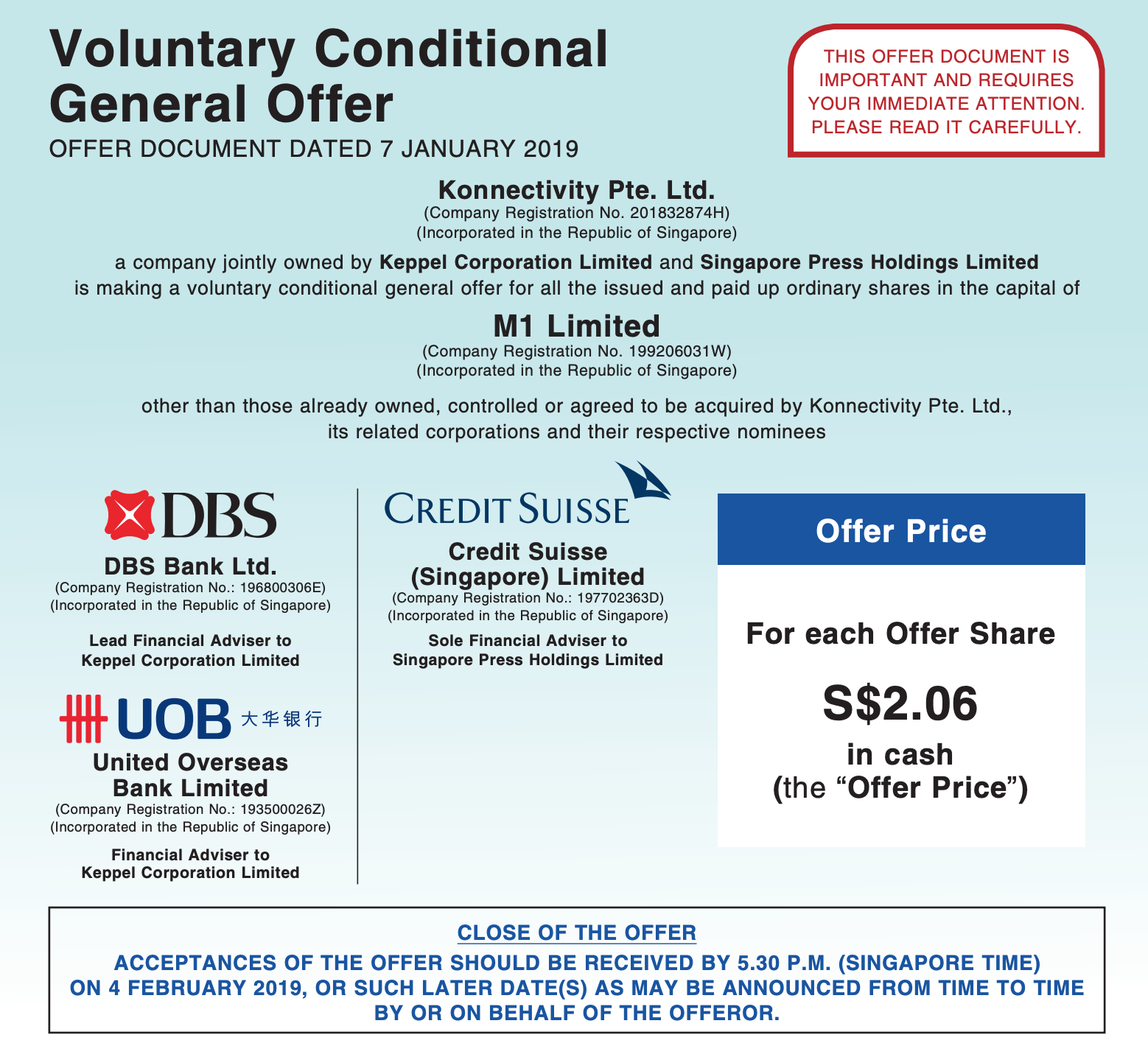

M1 Ltd (M1 SP), the third largest telecom operator in Singapore, is subject to a voluntary conditional offer (VGO) at S$2.06 cash per share from Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP) (KCL-SPH). KCL-SPH said on Tuesday that they wouldn’t increase their S$2.06 offer price “under any circumstances whatsoever.”

KCL-SPH’s stance not to increase their S$2.06 offer price is a clever ploy to the put the ball in Axiata Group (AXIATA MK)’s court. Axiata has three options, in our view. We believe that the probability of a material bid to KCL-SPH’s offer is low with Axiata most likely to retain its stake as a minority shareholder.

Polycab India (POLY IN) plans to raise around US$280m in its IPO through a mix of selling primary and secondary shares. It is the largest manufacturer of wires and cables in India with a 12% market share, as per CRISIL research. The company has also recently entered the consumer electrical segments.

Sales growth has been decent while margin expansion has helped the company to report much higher PATMI growth. Although, cash flow from operations has lagged earnings growth as working capital requirements have been volatile. In addition, receivables quality seems to be deteriorating. To add to that the rationale for the dealers and employees rationalization hasn’t been clearly explained.

In this insight, I’ve covered the above points, compared the company to its listed peers and commented on valuations. Should the deal be offered at multiples close to its wires and cables peers, it might still be interesting.

Last week on 17 January, printing and HR services company and funeral parlor operator Kosaido Co Ltd (7868 JP)announced that Bain Capital Private Equity would conduct an MBO on its shares via Tender Offer, with a minimum threshold for success of acquiring 66.67% of the shares outstanding. The Tender Offer commenced on 18 January and goes through 1 Mach 2019. The Tender Offer Price is ¥610/share, which is a 43.8% premium to the close of the day before the announcement and a 59.7% premium to the one-month VWAP up through the day before the announcement.

The company’s board of directors announced it supported the deal.

Terms & Schedule

Terms & Schedule of Hitachi Tender Offer for Yungtay Engineering

Tender Offer Price

JPY 610

Tender Offer Start Date

18 January 2019

Tender Offer Close Date

1 March 2019

Tender Agent

SMBC Securities

Maximum Shares To Buy

24,913,439 shares

MINIMUM Shares To Buy

16,609,000 shares

Currently Owned Shares

100 shares

Irrevocable Undertakings

Sawada Holdings’ 3,088,500 shares or 12.40% (includes the holdings at both Sawada Holdings and HS Securities).

This deal is probably reasonably straightforward.

It is a big premium to last trade, and a multi-year high.

There is one large holder publicly willing to sell and I expect the cross-holders would be willing to sell too.

Management is involved and supportive.

Except it is being done (and recommended) at a 44% discount to Tangible Book Value Per Share after the directors managed to work Bain up from a 49% discount to TBVPS.

Meanwhile, Descente has brought in Wacoal (3591 JP) as a white knight and made a splash in the business media about its recent success.

Itochu insists that Descente needs Itochu’s management skills, particularly to build a stronger business in China and other overseas markets, and says the only way to make Descente listen is to buy more stock – more than its current nearly 30%.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Lee Seo-Hyun (age 46), the billionaire second daughter of the Samsung Group Lee Gun-Hee, recently stepped down from her position as the CEO of Samsung C&T (028260 KS)‘s fashion business. After resigning from Samsung C&T, Lee Seo-Hyun will become a chairperson of the Samsung Foundation, focusing on corporate social responsibility activities.

Among the various fashion brands, the most problematic has been the 8 Seconds SPA brand, which has been continuing to lose money. Despite big ambitions to make 8 Seconds as one of the leading global SPA brands, this plan has fluttered, especially in the overseas markets such as China. This strongly suggests that there could be a big restructuring of the company’s fashion business in the coming months.

Our NAV analysis of Samsung C&T suggests a range of 122k won to 139k won, which would represent an upside of 11% to 27%. In our NAV analysis, the investment stakes in affiliates were 19.2 trillion won, core business operating value was estimated at 9.9 trillion won (using 8x consensus OP in 2019), net cash of 2.2 trillion won, and Samsung Everland land value (post 50% taxes) of 1.8 trillion won. The range of value reflects the different discount for the quasi-holdco structure (20-30% discount).

Amorepacific appears very tempting for stub trade. The Amore duo now has the widest price divergence on a 20D MA among Korea’s single-sub holdcos. But I would wait on this name. Locally, signals of improving fundamentals are being heard on the local cosmetics stocks. Holdco has traditionally been more susceptible to fundamentals changes. It is very possible that Amore duo leads to upwardly mean reversion in favor of Holdco in the short-term.

Prored Partners is a business consulting company founded in 2009 by the CEO, Mr Satani (who retains 60% of the equity). Prior to setting up Prored, he worked as a business consultant at a consultancy firm subsequently acquired by PwC Consulting. The shares were registered on the Mother’s exchange at the end of July 2018. Unfortunately, it is a micro-cap (market cap Y24bn) but should be of interest to those looking for a very fast growing small cap name. It trades on 17x our forecasts for this year to 10/19. The company has been growing at a fast pace over the last few years. We expect this strong rate of growth to continue, see below.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: those with a market capitalization of above USD 5 billion, those with a market capitalization between USD 1 billion and USD 5 billion, and those with a market capitalization between USD 500 million and USD 1 billion.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Trading around its lowest implied stub inside the past five years, improving sentiment toward cosmetic stocks should support an Amorepacific Group (002790 KS) setup.

Preceding my comments on CKI/PAH, Amorepacific and JCNC are the weekly setup/unwind tables for Asia-Pacific Holdcos.

These relationships trade with a minimum liquidity threshold of US$1mn on a 90-day moving average, and a % market capitalisation threshold – the $ value of the holding/opco held, over the parent’s market capitalisation, expressed as a % – of at least 20%.

INTERIM UPDATE – Pasona Group (2168 JP) released their second-quarter results on January 11th. This Insight updates our recent Insight Pasona Non-Grata and re-iterates our buy recommendation. Pasona shares have risen by 15% this year to the intra-say high last Friday. Our target price remains ¥1,500 – a further 18% upside from today’s level.

The shares have underperformed TOPIX by 25% over the last 12 months and in terms of book, see chart below, are trading at near 5 year lows. Earnings for 3/19 were revised down after 1Q (operating profit from Y75bn to Y66bn due to write-off in the rolling stock division). The current forecast in our view is achievable and next year, in the absence of further write-off and growth in other parts of the business, we would expect operating profits to recover to the Y80bn level. This is a big conglomerate with many moving parts, some good and some not so good, but there is a price for everything and given where the shares are now, and where we think earnings are going, we are happy to buy here with the company trading at 0.9x book and the shares yielding just under 3%.

Based on CRC’s (China Railway Corporation) 2019 plan on rail investment, CRRC’s earnings from rail business might be better than estimated. With a 45% increase on new rail delivery mileage, and significantly increase on HSR train (Multiple Units) repair demand, we estimate CRCC’s EPS increase by another 20% yoy to RMB0.53 in 2019E, following a 17% yoy increase in 2018E.

Also, a better earnings outlook might trigger a mild valuation re-rating. The stock trades at 12.8x P/E 2019E (our estimates), attractive vs. its 15.5x historical P/E average since the merger in 2015.

Mitsubishi Corp (8058 JP) is looking to sell 9m shares of Ayala Corporation (AC PM) for approximately US$155m. Post-placement, Mitsubishi Corp will still hold 7.2% of Ayala Corp if the upsize option is not exercised.

The deal scores poorly on our framework owing to its the large deal size relative to its three-month ADV. The company is also slightly more leveraged than its peers. However, it was offset by cheaper valuation and a strong track record.

But, our deal breaker here is the fact that the selldown one year after 2018’s selldown may signal that Mitsubishi Corp. may return to sell more on the market again in the near-term. While Mitsubishi, in the past, has reaffirmed that their partnership with AC will likely continue, it should not serve as a reassurance that it will continue to hold shares in AC.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Amorepacific appears very tempting for stub trade. The Amore duo now has the widest price divergence on a 20D MA among Korea’s single-sub holdcos. But I would wait on this name. Locally, signals of improving fundamentals are being heard on the local cosmetics stocks. Holdco has traditionally been more susceptible to fundamentals changes. It is very possible that Amore duo leads to upwardly mean reversion in favor of Holdco in the short-term.

Prored Partners is a business consulting company founded in 2009 by the CEO, Mr Satani (who retains 60% of the equity). Prior to setting up Prored, he worked as a business consultant at a consultancy firm subsequently acquired by PwC Consulting. The shares were registered on the Mother’s exchange at the end of July 2018. Unfortunately, it is a micro-cap (market cap Y24bn) but should be of interest to those looking for a very fast growing small cap name. It trades on 17x our forecasts for this year to 10/19. The company has been growing at a fast pace over the last few years. We expect this strong rate of growth to continue, see below.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: those with a market capitalization of above USD 5 billion, those with a market capitalization between USD 1 billion and USD 5 billion, and those with a market capitalization between USD 500 million and USD 1 billion.

Shaily Engineering Plastics (SHEP IN) Q2 FY19 results were below our expectations. While revenue increased by 10% YoY, PAT declined by 9% YoY in Q2 FY19. This muted performance was primarily due higher raw material prices and a shortage of labour as well as power outage that resulted in low machine utilization. We analyze the results.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

After initially being very skeptical of the China Tower (788 HK) IPO given it is essentially a price take to its three largest shareholders, we changed our view in early December to a more positive outlook. What changed our view has been series of calls and meetings with the company that suggested a more shareholder friendly approach than expected and a real opportunity to reduce capex substantially through the use of “social resources” (e.g. electricity grid, local government sites). These can be used to deliver co-locations without building towers and poles and imply much lower capital intensity at a time when revenue growth will be accelerating as 5G is rolled out. Management has also given more detail on non-Tower business prospects which can generate higher returns (not under the Master Services Agreement). While small now (2% of revenue) they are growing rapidly. With lower capex than initially guided and a more shareholder friendly management (i.e. higher dividends are possible) we reduce the SOE discount and raise our forecasts (again). We remain at BUY with a new target price of HK$2.20

After three-plus months of speculation that Axiata Group (AXIATA MK) was unhappy with the price and might make a counter-offer, no offer has been forthcoming.

After I wrote on the 2nd in M1 Offer Coming – Market Odds Suggest a Bump But… that the reward/risk did not look that great, shares drifted downward from the S$2.09-2.11 area and into the afternoon of the 7th, traded in the S$2.05-2.07 range, which was the first time in months the shares had traded at or below the prospective offer price.

chart source: Investing.com

Some 20mm+ shares (5.5% of the shares out other than the three major holders) traded between 3pm Singapore time on the 7th and a few minutes after the open the day after the announcement. Then part-way through the day, someone bought a large number of shares lifting the share price two spreads for a while. Since then, the shares have settled back down to the $2.07-2.08 range.

Depending on your opinion of the likelihood of a bump, your execution strategy will differ. It’s still not clear that a bump or counterbid will be forthcoming, but at S$2.07, the risks are better than they were higher.

Over 2017-18, the Australian Securities & Investments Commission (ASIC) undertook a review of allocation in equity raising transactions. The review involved large and mid-sized licensees (brokers), Issuers, International investors and other international regulators. The results of the review were published by ASIC in Dec 2018. This insight highlights some of the key findings.

It’s good to see that some of the standard practices of banks allocating more to existing clients and participants of earlier deals have at least been acknowledged. Even though some institutional investors have outright labelled the allocation process as a “black box”, ASIC doesn’t seem to want to do much about it.

The area where ASIC is more concerned is the messaging to investors which highlights the different definitions of “well-covered” across banks. Although, the banks seem to have mislead the regulator on interpretation of “real-demand” with ECM bankers saying that all orders are taken at face-value. That raises a whole new level of questions on the messaging around demand for the deal.

Kingboard Chemical (148 HK)gets a boost after buying properties from its major shareholder, however, the implied yield is uninspiring.

Preceding my comments on BGF and KBC are the weekly setup/unwind tables for Asia-Pacific Holdcos.

These relationships trade with a minimum liquidity threshold of US$1mn on a 90-day moving average, and a % market capitalisation threshold – the $ value of the holding/opco held, over the parent’s market capitalisation, expressed as a % – of at least 20%.

HDC Holdings (012630 KS) and HDC-OP (294870 KS) price gap is now at a nearly record high. Holdco discount is now 60% to NAV. On a 20D MA, Holdco and Sub are currently below -1 σ.

I initiated a stub trade on the duo on Dec 11. It paid off on a short term horizon until the duo reached within -0.5~0 σ on a 20D MA. Yield peaked at 4.6% on Dec 14. If you approached with a longer term horizon, things wouldn’t have been as enjoyable.

The only possibly explainable factor for the recent price divergence is HDC I-Controls’ need to dump a 1.78% Holdco stake. 1.78% overhang risk is not enough to sustain this much divergence and current 60% Holdco discount.

The duo has again entered < -1 σ territory at yesterday’s closing prices. I’d first make another short-term stub trade. I’d hold onto the position until they reach within -0.5~0 σ on a 20D MA with a loss cut at -5%. But a little longer term approach to hunt for a higher yield wouldn’t be a bad idea at this point.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

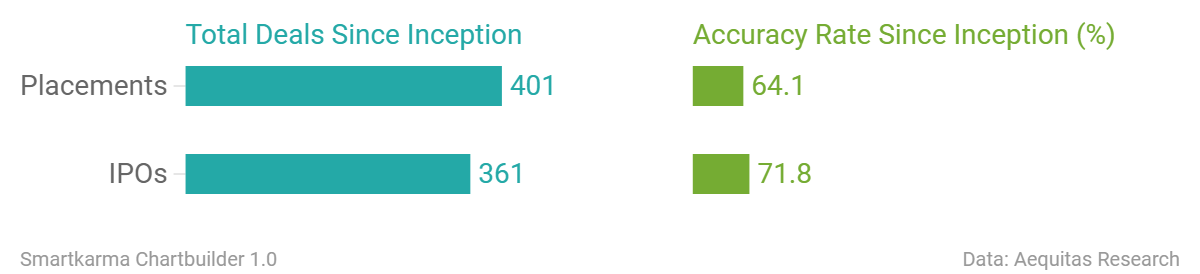

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Despite a shaky 2018 Q4 market and the disappointing Softbank Corp (9434 JP)‘s IPO, we have been getting a steady stream of newsflow on upcoming IPOs.

Starting with upcoming IPOs, Chengdu Expressway Company Limited (1785 HK) and Weimob.com (2013 HK) will be listing next week on Tuesday, 15th January. Weimob was priced at the low end of its price range while Chengdu Expressway’s IPO was at a fixed price of HK$2.20. We are bearish on both IPOs. Weimob is overly reliant on Tencent for its SaaS and Ads business and, at the same time, Tencent will only own less than 3% stake after listing. Whereas Chengdu Expressway has been a well-managed company but valuation implies limited upside. Trading liquidity will likely remain tepid as like Qilu Expressway Co Ltd (1576 HK) which listed mid last year.

In the pipeline, we are hearing that Kepei Education (KEPEI HK) will likely open its book next Monday. We will be following up with a note on valuation. In other IPOs that are coming in this quarter, Helenbergh China and Zhongliang, both property developers, are looking to IPO in this quarter. Viva Biotech Shanghai Ltd (1577881D HK) is also looking to list in Hong Kong Q2 while Urban Commons, a US property developer, is planning a US$500m REIT IPO in Singapore.

Activity seems healthy for the ECM space, but sentiment has not been the best as seen from Xiaomi’s high profile IPO that took a hit just as its lockup expired. Its share price has corrected from a high of HK$22.20 to just above HK$10.34 this Friday. This should not have been a big surprise since many have already pointed out that its valuation should really have been closer to that of a hardware business and we pointed out that the IPO’s trajectory would likely be similar to Razer.

This reminds us of a particular listing last year, Razer Inc (1337 HK) , and, in fact, both bear quite a handful of similarities. Strong portfolio of investors, hardware business with software capabilities, expensive valuations, and etc. The stock did well at first but has come back down to earth since then.

Accuracy Rate:

Our overall accuracy rate is 72% for IPOs and 64% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

China Tobacco International (Hong Kong, US$100m)

China East Education (Hong Kong, US$400m)

Ebang International (Hong Kong, re-filed)

MicuRx Pharma (Hong Kong, re-filed)

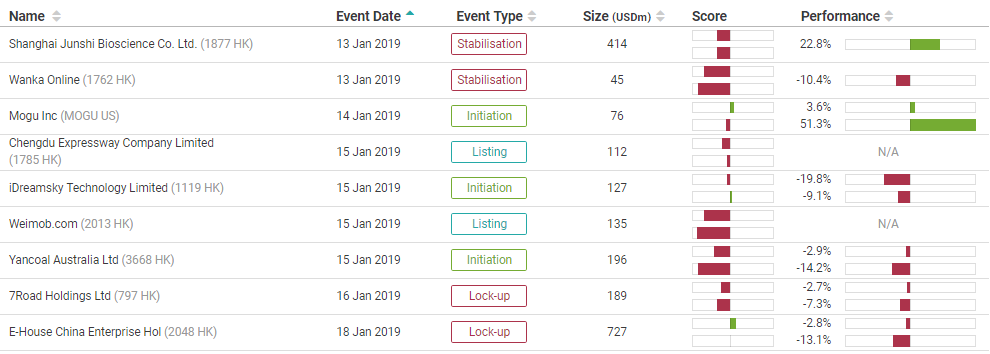

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

In the three months to December, MonotaRO’s domestic (parent company) sales continued to grow at an annual rate close to 25%, indicating that full-year consolidated results should be close to management’s guidance and our own estimates. This also suggests that our 18% sales growth forecast for 2019 could be conservative.

Parent company data for December show sales up 18.4% year-on-year in nominal terms, but up 24.6% when adjusted for the number of working days in the month. The figures for November were 27.3% growth in nominal terms, but 21.3% adjusted.

In the three months to December, adjusted sales were up 24.2%, a slight improvement from 23.9% growth in 3Q. In FY Dec-18 as a whole, reported parent company sales were up 24.4% to ¥105.3 billion, slightly exceeding management’s ¥104.1 billion guidance.

At ¥2,523 (Friday, January 11, close), the shares have dropped 25% since October. They are now selling at 61x our EPS estimate for FY Dec-18, 54x our estimate for FY Dec-19 and 47x our estimate for FY Dec-20. Price/sales multiples for the same three years are 5.7x, 4.8x and 4.2x.

Consolidated results for FY Dec-18 are due to be announced by the end of January.

MonotaRO is the only pure-play e-commerce MRO (Maintenance, Repair and Operation) investment in the Japanese stock market. With over 10,000 SKUs (stock keeping units – i.e., individual items, including gloves, hand and power tools, hardware, painting supplies, etc.) for sale to construction companies, manufacturers, auto repair shops and other customers, the company is both driving and benefitting from the growth of Japan’s B2B MRO market. Overseas subsidiaries in South Korea, Indonesia and China, which account for about 4% of consolidated sales, are not yet profitable.

We highlighted in a recent note Chris Hoare‘s positive outlook for China Tower (788 HK). Our view takes into account the 5G build-out commencing this year, improved capex efficiency from using “social resources”, the rapid growth in non-tower businesses that lie outside the Master Services Agreement (MSA), and the valuation benefit from what looks like surprisingly investor friendly management.

This note focuses on four key issues facing the Chinese telcos in 2019:

5G capex (March) (this is by far the most important),

Regulatory newsflow (February/ March),

Operating trend improvements (August), and

Emerging business opportunities driving future growth (August).

We remain positive on the telcos which trade at low multiples. China Unicom (762 HK) continues to trade at a discount, yet is most exposed to the positive story emerging at China Tower. We switch our top pick among the telcos from China Mobile (941 HK) back to China Unicom as a result. Alastair Jones thinks China Telecom’s (728 HK) premium multiple is at risk if management execution on the cost base doesn’t improve. It is our least preferred telco at this stage. Overall, we expect China Tower to outperform all telcos and it is our top pick. The upgrade to China Tower flows through the telcos (valuation and costs) and our new target prices are as follows: China Unicom to HK$14.4, China Telecom to HK$5.4 and China Mobile to HK$96.

In November 2017, Toshiba Corp (6502 JP) bowed to the inevitable and issued shares in order to shore up shareholder equity ahead of the 31 March 2018 deadline where if the company had not announced a positive shareholder equity number, it would have been delisted according to the Enforcement Rules of the Tokyo Stock Exchange.

So it issued ¥600 billion of equity in an accelerated privately-negotiated placement to hedge funds. There was some jawboning later from domestic institutions who had not gotten the show on the deal, but they would do well to remember that when Toshiba was in dire straits earlier that year, and continued listing was not guaranteed because of accounting issues which were later overcome (before the equity issuance), it was the hedge funds who bought dozens of percent of the company – not domestic financial institutions. In any case, the equity was predictably needed, but as a way of making it clear that it would not be forever, the release accompanying the financing said the company would accelerate returns to shareholders once the sale of Toshiba Memory Corporation was complete.

That return of capital to shareholders was announced in June 2018 after the closing of the TMC transaction had been confirmed. Toshiba would buy back ¥700 billion of shares. At the time, that was up to 40% of shares outstanding, but the shares rose as the shares of companies with large buyback plans do, and it took until November to dot the “i”s and cross the “t”s on making sure that the cash in the bank account was deemed distributable capital surplus. On November 8th, a year after announcing the sale of equity, Toshiba announced the start of a Very Large Buyback. A few days later the company announced a large ToSTNeT-3 buyback, offering to buy back all ¥700 billion of shares the following morning at that day’s close. A week later the company had bought back ¥243 billion or more than 35% of the total buyback then announced further purchases would be made in the market.

That’s when the fun began.

For previous recent treatment on the Toshiba buyback, see the following:

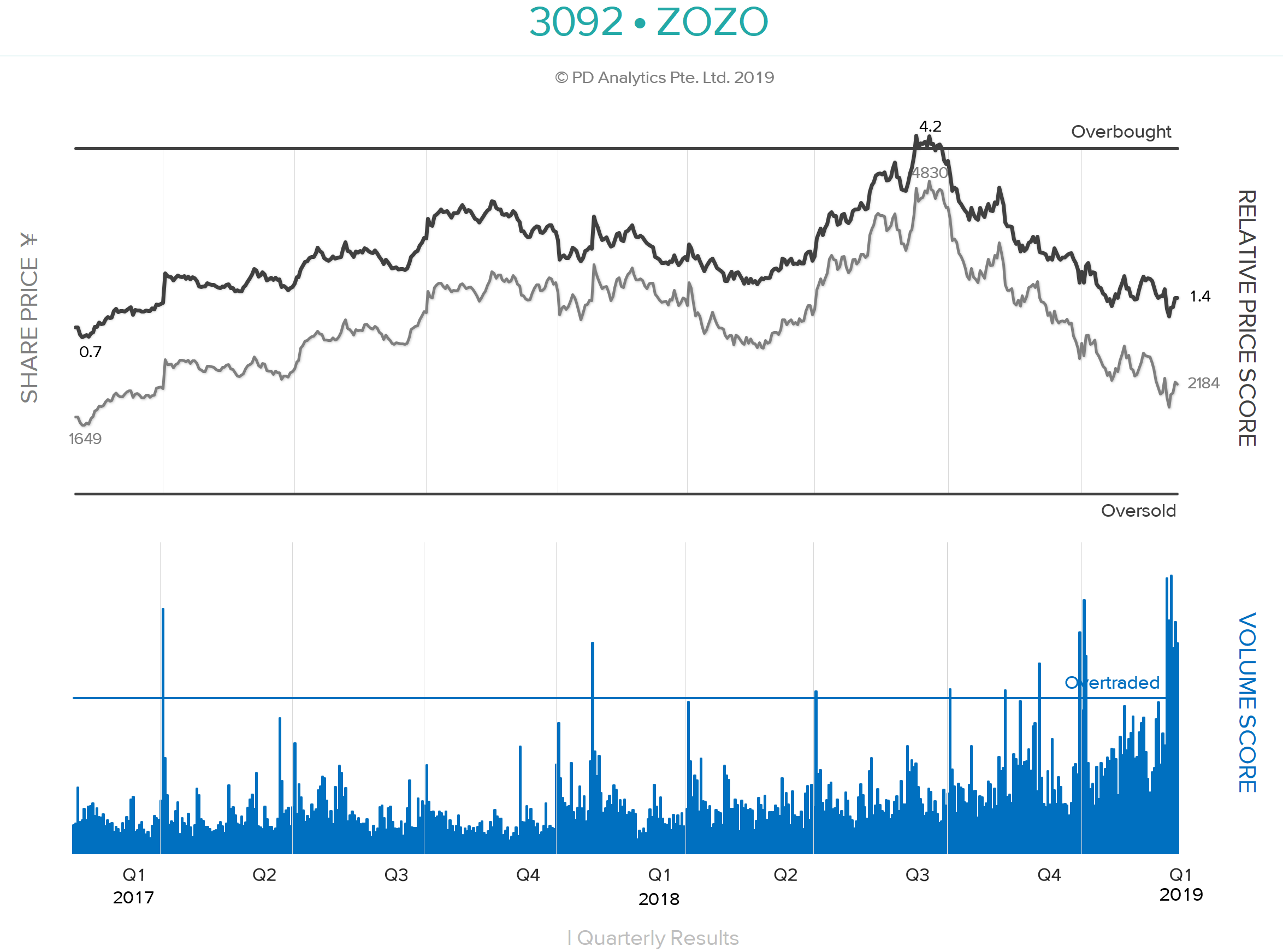

ONWARD AND OUT – ZOZO (3092 JP), formerly Start Today, has been the sixth-most-traded large capitalisation stock over the last ten trading days after Benefit One (2412 JP), Rizap (2928 JP), Takeda Pharmaceutical (4502 JP), Hoshizaki (6465 JP), and Workman Co Ltd (7564 JP). According to Nikkei XTECH, on 25th December apparel maker Onward (8016 JP) suspended selling of its products on ZOZOTOWN and will leave the platform altogether. Although Onward products are estimated to account for less than 3% of total transactions on the site, there are concerns that other apparel makers will follow suit as a result of the emerging direct competition on the site from ZOZO’s private label. Since reaching our 4.0 ‘Overbought’ threshold on 9th July 2018, ZOZO shares have corrected by 57% – the worst performance of any large cap from that date – as concerns mounted over the private brand strategy and the behaviour of CEO Yusaku Maezawa. Since bottoming on 4th January, the shares have risen by 18% following positive comments from the CEO about sales over the New Year holiday period.

PRIVATE-LABEL STRETCH GOALS– The ‘teething problems’ of ZOZO entering the private-label apparel business have been well-documented by Michael Causton in a recent Insight on Smartkarma. Michael rightly questions the feasibility of the company scaling a ¥200b apparel business within the next three years while targeting an additional incremental ¥400b in e-commerce revenue, particularly as it has taken ZOZO twenty years to reach the first ¥100b in annual revenues. In the DETAIL section below, we shall examine ZOZO’s current and possible future financial condition as it strives to become one of the top-ten global fashion retailers.

‘ZOSO’ & THE STAIRWAY TO HEAVEN – In addition to some notable purchases of modern art at record-breaking prices, CEO Maezawa also last year booked himself on Space X’s first flight to the moon. With apologies, the lyrics of the peerless song from Led Zeppelin’s untitled fourth album – known by fans as ‘Zoso’ after the symbol designed by Jimmy Page for the inner sleeve – come to mind:-

There’s a lad(y) who’s sure All that glitters is gold And (s)he’s buying a stairway to heaven When(s)he gets there (s)he knows If the stores are all closed With a word (s)he can get what (s)he came for.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

M1 Ltd (M1 SP), the third largest telecom operator in Singapore, is subject to a bid. On 7 January 2019, Konnectivity launched a voluntary conditional offer (VGO) at S$2.06 cash per share. Konnectivity is jointly owned by Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP).

M1’s shares are trading a touch above the VGO price of S$2.06 per share as the market is betting that Axiata Group (AXIATA MK) may ride in with its competing offer. However, we believe that shareholders should accept the offer as Axiata is unlikely to engage in a bidding war due to several factors.

In this report, we discuss some of the major changes in regulation and recent important news related to the Korea National Pension Fund Service (NPS), including changes to the voting rights of outsourced Korean equity investments by NPS as well as how it may deal with the Hanjin Kal Corp (180640 KS) corporate governance issues.

It was reported yesterday that the NPS will allow 57 trillion won ($51 billion) of Korean equity investments which are currently managed indirectly by numerous outsourced asset management companies to have their own respective voting rights. The Financial Services Commission (FSC) announced yesterday that an amendment to the enforcement ordinance of the Capital Market Act was passed allowing NPS’s indirectly managed Korean equity investments’ voting rights to be exercised by the outsourced asset managers rather than by NPS itself passed the Cabinet meeting.

What are the major implication? As a result of this move, this will act as a key positive catalyst spurring on greater corporate activism since NPS’s outsourced fund managers will have greater freedom to make more aggressive decisions to improve shareholder value of Korean companies. In addition, it also reduces the overall responsibility of carrying out the Stewardship Code changes to not just on NPS but on the rest of the major asset management companies in Korea.

A combination of, optimism surrounding U.S.-China trade talks, and Fed Chairman Powell’s comments have led to a continuation of the oversold bounce which began on 12/26, and the S&P 500 is now trading just below the 12/19 pre-Fed rate hike area. ~2,350 on the S&P 500 remains the support level to monitor. A retest of this low remains the most likely scenario, though it is far from a guarantee due to the potential for a “V” reversal. We examine an array of factors leading to our intact cautious outlook, and highlight attractive set-ups within Consumer Discretionary and Health Care Sectors.

In this report, we provide an analysis of our pair trade idea between BGF Co Ltd (027410 KS) and Bgf Retail (282330 KS). Our strategy will be to be long BGF Co & Short BGF Retail. BGF Co Ltd (027410 KS)‘s share price plummeted by 48% in the past year while Bgf Retail (282330 KS) had a tiny gain of 0.7% in the same period. In the past year, BGF Co was down versus BGF Retail for pretty much the entire year. The BGF/BGF Retail share price ratio has been trending downwards since March 23rd, 2018. The current ratio is 0.037 and it is now close to approaching two σ.

The following are the major catalysts that could boost BGF Co shares higher than BGF Retail shares within the next six months.

Temporary relief from big market fears, seasonality, & trading volume

Market’s concerns about the size of tender offer rather than the value of BGF Co post tender offer in 2018

NAV discount to its intrinsic value at an all-time high – Our NAV analysis of BGF Co suggests that it is trading at a 51% discount to its NAV, which is close to its all time highest discount. Typically, the Korean holdcos trade at a 20-40% discount to their intrinsic value so it is unusual for the holdco to trade with so much discount.

Government is likely to slow down the minimum wage hikes

Please see some recent buy ideas, all very cheap, that we believe offer decent longer term growth and have had a dreadful December. We have written on all recently and below is a summary of the main points as well as an some valuation metrics. All are sensibly priced in our view now.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Healius (HLS AU), formerly known as Primary Health Care (PRY AU), is a leading Australian owner of GP clinics and pathology centres. Healius just took four days to reject Jangho Group Co Ltd A (601886 CH)’s 3 January 2018 proposal of A$3.25 cash per share as it “is opportunistic and fundamentally undervalues Healius.”

We believe that rejection of Jangho’s proposal provides shareholders with option value. If Healius’ growth initiatives generate value, we believe that the shares will be worth more than Jangho’s proposal. If Healius’ growth initiatives stall and the shares slide, we believe that Jangho will once again table a proposal.

In August 2017, Honda stole the top spot in Thai passenger cars from Toyota and held it for a few months. They are still formidable players, and ACG (AutoCorp) which runs Honda dealerships and service centers across Thailand, is expected to IPO some time in 2019. Here’s our quick look at the company.

We value this IPO at Bt2/sh using DCF, since there’s really no good comparables. The company is expected to enjoy slower revenue growth and higher margins going forward as car sales slow down nationally and maintenance becomes a bigger chunk of the revenues.

They only operate in four provinces and run 8 showrooms with over 6,000 sqm of display space. The service centers account for almost 17,200 sqm. The big chunk comes from lower margin car sales. Along with accessories, these account for 84% of revenues.

The IPO is firmly underwritten by Singapore’s Phillips Securities and is good for more than a quarter of shares outstanding (26%). The founding Rangkanuwat family control all remaining shares and have committed to 6 month lock-up period.

Healius (HLS AU) (until last month known as Primary Health Care Limited), a leading owner of general practice clinics and pathology centres in Australia, announced an unsolicited and conditional proposal (including DD) from Jangho Group Co Ltd A (601886 CH) at A$3.25/share (~10x FY19 EV/EBITDA) in a A$2.0bn deal. Jangho currently holds a 15.9% stake in Healius and has been on the shareholder register for two years.

The Offer price translates to a 33.2% premium to the undisturbed price but below the 12-month high of A$4.09 in March 2018. Optically and when referenced to closest peer Sonic Healthcare (SHL AU), the offer price appears light.

Reflecting the long laundry list of conditions attached to this indicative offer, such as securing debt financing and various regulatory approvals in China and Australia, notably data security, this indicative deal is trading wide at a gross/annualized spread of 25%/47%, assuming a deal completion date in early August.

This proposal does, however, indicate Healius was probably oversold.

This morning, Healius’ board rejected the proposal as it was considered opportunistic and fundamentally undervalued the company.

A year ago we began publishing Tracking Traffic/Chinese Tourism as the hub for all of our research on China’s tourism sector. This monthly report features analysis of Chinese tourism data, notes from our conversations with industry participants, and links to recent company news and thematic pieces. Our aim is to highlight important trends in China’s tourism sector (and changes to those trends).

In this issue readers can find:

A review of China’s outbound tourist traffic in November, which strengthened: Lifted by extraordinarily strong growth in visits to Hong Kong and, to a lesser extent, Macau, Chinese outbound travel demand rebounded strongly in the seven regional destinations we track. But the fact that November’s growth was led overwhelmingly by Hong Kong and Macau — destinations close enough for weekend or day trips from population centers in Southern China — suggests Chinese tourists’ purse strings are still tight.

An analysis of November domestic Chinese travel activity, which turned weaker: November data from China’s three leading airlines and the Ministry of Transport show moderating domestic travel demand. For combined rail, highway, and air travel, November demand grew by less than 3% Y/Y. Along with the change in destination mix for outbound travel (that favors ‘nearby’ destinations), it now appears domestic demand has weakened, too.

Links to other recent news & research on Chinese tourism: Readers can check out our quick takes on Macau’s December GGR figure, preliminary GTV and revenue figures released by Ctrip.Com International (Adr) (CTRP US), declining US visa issuance to Chinese tourists, and Qatar Airways’ new investment in a leading Chinese airline.

Although we remain positive on the long-term growth of Chinese tourism, it’s clear that near-term demand has weakened substantially. We continue to take a negative view of travel intermediaries like Ctrip, which face intensifying competition from many sources. We are more positive on the prospects of actual owners of Chinese travel and tourism assets, like hotel chain Huazhu Group (HTHT US) and Air China Ltd (H) (753 HK).

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP)and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of FD shares. The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.08 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

M1 has seen ~175mm shares traded since the initial announcement – all at prices above the proposed Offer Price of S$2.06. In that time, Starhub has popped and fallen back, and SingTel has fallen almost 10% to its lowest level in seven years.

Clearly, there is expectation that either Axiata will counter or Keppel and SPH will raise the Offer to bring Axiata onside. Travis Lundy doesn’t see who would join Axiata in bidding for M1 at a price of 8+x TTM EBITDA when there is price competition to come. He thinks it more likely that a small kiss (perhaps even a decent bump to S$2.30 or even more) to the price is made by the Offerors SPH and Keppel to get Axiata over the line. However, he does not think the Offerors need to offer that much to dislodge retail shareholders if the IFA comes out and says “increased competition puts the dividend in danger“.

Healius, a leading Australian owner of GP clinics and pathology centres, announced an unsolicited and conditional proposal from Jangho Group Co Ltd A (601886 CH) for A$3.25/share (~9.6x FY19 EV/EBITDA) in a A$2.0bn deal. Jangho currently holds a 15.9% stake in Healius and could potentially go hostile here.

Pricing looks off according to Arun George, at a 15% discount to peers on a CY2019 EV/EBITDA metric.

Still, Healius is not without issues, having to pay a backpay bill to staff last year, bump salaries for workers at its Victorian pathology division, while also losing a lucrative national bowel screening contract in 2017.

Notwithstanding the price, as Healius is an owner of sensitive medical data, the FIRB would take a very close look at this transaction, especially one where the acquirer is a Chinese entity, given the recent rejection of the CKI/APA Group (APA AU) deal and Huawei’s 5G.

As the merger between TMB and Thanachart gets a nudge from the Ministry of Finance and could be finalized this month, Athaporn Arayasantiparb, CFA tackles the obvious questions – what price and what benefits?

Based on his estimates, the potential improvements in ROE from the merger and potential divestment of Thanachart’s 19% stake in MBK, he thinks it justifies a Bt11.1/sh premium or Bt64.25/sh. Anything above that would feasibly be value destroying.

In terms of benefits, Thanachart has a higher ROE than TMB and appears smaller but better managed. The merger would allow TMB to re-enter the securities business (more cross-selling), enlarge its asset management franchise, and scale up the deposit base for both banks.

Reportedly Nexon’s founder Kim Jung-Joo and other related parties plan to sell their 98.64% stake in NXC Corp, which owns a 47.98% stake in Nexon. Nexon has a market cap of $11.6bn but the rumoured price tag for the 47.98% take is $8.9bn implying a significant management premium.

Initially launched as a voluntary conditional Offer late November, DNO ASA (DNO NO)crept over 30% in Faroe this week and is now required to launch an MGO. The Offer price remains the same at GBP 1.52/share, however, the acceptance condition falls to 50% from 57.5% previously.

Faroe’s pushback on the Offer – that the 21% premium offered to pre-announcement price is only “about half the average premium paid on all UK takeovers over the last 10 years” – is disingenuous. DNO built a 27.68% stake in a matter of days back in April 2018, clearly telescoping that a full-blown Offer was a possibility (although denying it at the time). The unaffected price prior to the acquisition of that stake should be used as a reference point for the current Offer. This translates to a 44.8% premium.

DNO has 43.1% in the bag, close to the 50% needed. There are investors (like Cavendish, holding 1.38%) who side with Faroe saying that the Offer is too low. With shares trading through terms, my bet is that DNO may need to kiss this offer, say 5-10%, to get it over the line.

Curtis Lehnert recommends closing out the set-up trade, now that he sees the stub having reverted to its long-term average level. Since his recommendation, the trade has made a notional gain of 5% in a two and a half month time span. As an aside I back out a discount to NAV of 21%, off its recent low of ~28% in early Nov, and compares to a 12-month average of 19%.

Back in September, I discussed in StubWorld: Matheson Unloads JLT, Unwind Takarathat Matheson may use the net proceeds of £1.7bn (US$2.2bn) from selling its 40.16% stake in Jardine Lloyd Thompson Group P (JLT LN)into Marsh & Mclennan Cos (MMC US)‘sOffer, towards increasing its stake in JS, as there was/is still some room before the maximum 85% ownership level was reached. This is what happened (or at least a token amount of the proceeds), with Matheson buying ~2.5mn shares in Strategic for ~US90mn in early October. Matheson now holds a little less than 84% by my calculation – the group unhelpfully states it holds 84% without going into decimal places.

After touching a 17-year low ratio level of 1.41x (JM/JS) last September, that has blown out to 1.83x, having closed the year at 1.89x, a two-and-a-half year high, and compares to the long-term average of 1.7x.

Strategic continues to trade “cheap” at ~44% discount to NAV, adjusted for the cross-holding. The spread between Matheson and Strategic is around its widest inside a year. Furthermore, as Matheson increased its stake, Strategic also acquired shares in Matheson earlier last year. Both elevate the cross-holding, which in principle you would expect the two companies to become even more closely aligned.

I’d recommend buying into Strategic for its attractive NAV discount and further share acquisitions from Matheson.

Stub Wrap

Using a basket of 40 Holdcos I constructed, the average NAV discount in 2018 steadily widened throughout the year. Elsewhere:

Passive, tech-related and illiquid Holdcos widened most; while cross-border and property Holdcos were the best of the worst.

Illiquid, property, and passive Holdcos’ underperformance (or widening) was more pronounced in the first half. Tech Holdcos primarily widened in the second half.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP)and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of FD shares. The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.08 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

M1 has seen ~175mm shares traded since the initial announcement – all at prices above the proposed Offer Price of S$2.06. In that time, Starhub has popped and fallen back, and SingTel has fallen almost 10% to its lowest level in seven years.

Clearly, there is expectation that either Axiata will counter or Keppel and SPH will raise the Offer to bring Axiata onside. Travis Lundy doesn’t see who would join Axiata in bidding for M1 at a price of 8+x TTM EBITDA when there is price competition to come. He thinks it more likely that a small kiss (perhaps even a decent bump to S$2.30 or even more) to the price is made by the Offerors SPH and Keppel to get Axiata over the line. However, he does not think the Offerors need to offer that much to dislodge retail shareholders if the IFA comes out and says “increased competition puts the dividend in danger“.

Healius, a leading Australian owner of GP clinics and pathology centres, announced an unsolicited and conditional proposal from Jangho Group Co Ltd A (601886 CH) for A$3.25/share (~9.6x FY19 EV/EBITDA) in a A$2.0bn deal. Jangho currently holds a 15.9% stake in Healius and could potentially go hostile here.

Pricing looks off according to Arun George, at a 15% discount to peers on a CY2019 EV/EBITDA metric.

Still, Healius is not without issues, having to pay a backpay bill to staff last year, bump salaries for workers at its Victorian pathology division, while also losing a lucrative national bowel screening contract in 2017.

Notwithstanding the price, as Healius is an owner of sensitive medical data, the FIRB would take a very close look at this transaction, especially one where the acquirer is a Chinese entity, given the recent rejection of the CKI/APA Group (APA AU) deal and Huawei’s 5G.

As the merger between TMB and Thanachart gets a nudge from the Ministry of Finance and could be finalized this month, Athaporn Arayasantiparb, CFA tackles the obvious questions – what price and what benefits?

Based on his estimates, the potential improvements in ROE from the merger and potential divestment of Thanachart’s 19% stake in MBK, he thinks it justifies a Bt11.1/sh premium or Bt64.25/sh. Anything above that would feasibly be value destroying.

In terms of benefits, Thanachart has a higher ROE than TMB and appears smaller but better managed. The merger would allow TMB to re-enter the securities business (more cross-selling), enlarge its asset management franchise, and scale up the deposit base for both banks.

Reportedly Nexon’s founder Kim Jung-Joo and other related parties plan to sell their 98.64% stake in NXC Corp, which owns a 47.98% stake in Nexon. Nexon has a market cap of $11.6bn but the rumoured price tag for the 47.98% take is $8.9bn implying a significant management premium.

Initially launched as a voluntary conditional Offer late November, DNO ASA (DNO NO)crept over 30% in Faroe this week and is now required to launch an MGO. The Offer price remains the same at GBP 1.52/share, however, the acceptance condition falls to 50% from 57.5% previously.

Faroe’s pushback on the Offer – that the 21% premium offered to pre-announcement price is only “about half the average premium paid on all UK takeovers over the last 10 years” – is disingenuous. DNO built a 27.68% stake in a matter of days back in April 2018, clearly telescoping that a full-blown Offer was a possibility (although denying it at the time). The unaffected price prior to the acquisition of that stake should be used as a reference point for the current Offer. This translates to a 44.8% premium.

DNO has 43.1% in the bag, close to the 50% needed. There are investors (like Cavendish, holding 1.38%) who side with Faroe saying that the Offer is too low. With shares trading through terms, my bet is that DNO may need to kiss this offer, say 5-10%, to get it over the line.

Curtis Lehnert recommends closing out the set-up trade, now that he sees the stub having reverted to its long-term average level. Since his recommendation, the trade has made a notional gain of 5% in a two and a half month time span. As an aside I back out a discount to NAV of 21%, off its recent low of ~28% in early Nov, and compares to a 12-month average of 19%.

Back in September, I discussed in StubWorld: Matheson Unloads JLT, Unwind Takarathat Matheson may use the net proceeds of £1.7bn (US$2.2bn) from selling its 40.16% stake in Jardine Lloyd Thompson Group P (JLT LN)into Marsh & Mclennan Cos (MMC US)‘sOffer, towards increasing its stake in JS, as there was/is still some room before the maximum 85% ownership level was reached. This is what happened (or at least a token amount of the proceeds), with Matheson buying ~2.5mn shares in Strategic for ~US90mn in early October. Matheson now holds a little less than 84% by my calculation – the group unhelpfully states it holds 84% without going into decimal places.

After touching a 17-year low ratio level of 1.41x (JM/JS) last September, that has blown out to 1.83x, having closed the year at 1.89x, a two-and-a-half year high, and compares to the long-term average of 1.7x.

Strategic continues to trade “cheap” at ~44% discount to NAV, adjusted for the cross-holding. The spread between Matheson and Strategic is around its widest inside a year. Furthermore, as Matheson increased its stake, Strategic also acquired shares in Matheson earlier last year. Both elevate the cross-holding, which in principle you would expect the two companies to become even more closely aligned.

I’d recommend buying into Strategic for its attractive NAV discount and further share acquisitions from Matheson.

Stub Wrap

Using a basket of 40 Holdcos I constructed, the average NAV discount in 2018 steadily widened throughout the year. Elsewhere:

Passive, tech-related and illiquid Holdcos widened most; while cross-border and property Holdcos were the best of the worst.

Illiquid, property, and passive Holdcos’ underperformance (or widening) was more pronounced in the first half. Tech Holdcos primarily widened in the second half.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

I initiated SamE short Common/long 1P trade on Nov 29. This trade delivered the highest yield on Dec 13 at 4.55% with Nov 29 as the reference date. We are now slightly below +1 σ.

Common/1P relative price gap should get narrower. Price wise, 1P discount started at 19.81% on Nov 29 and reached the lowest at 16.38% on Dec 13. It reverted back to 18.69%, down 1.12%p. Market cap wise, Common/1P ratio is still higher than Nov 29. This suggests 1P’s catching up job isn’t over yet.

Div yield difference is still at a record high for 1P. CJ Corp (001040 KS)‘s recent class B pref issuance should be another plus. It will play in favor of those ownership transfer related prefs. I’d continue to hold onto this position until we move into March OGM cycle.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.