KCL-SPH again extended the closing date of the offer from 18 February to 4 March 2019. M1’s shares are trading at S$2.04 per share, marginally below the VGO price of S$2.06 per share. We believe that the KCL-SPH should get the valid acceptances to complete the delisting and wholly own M1.

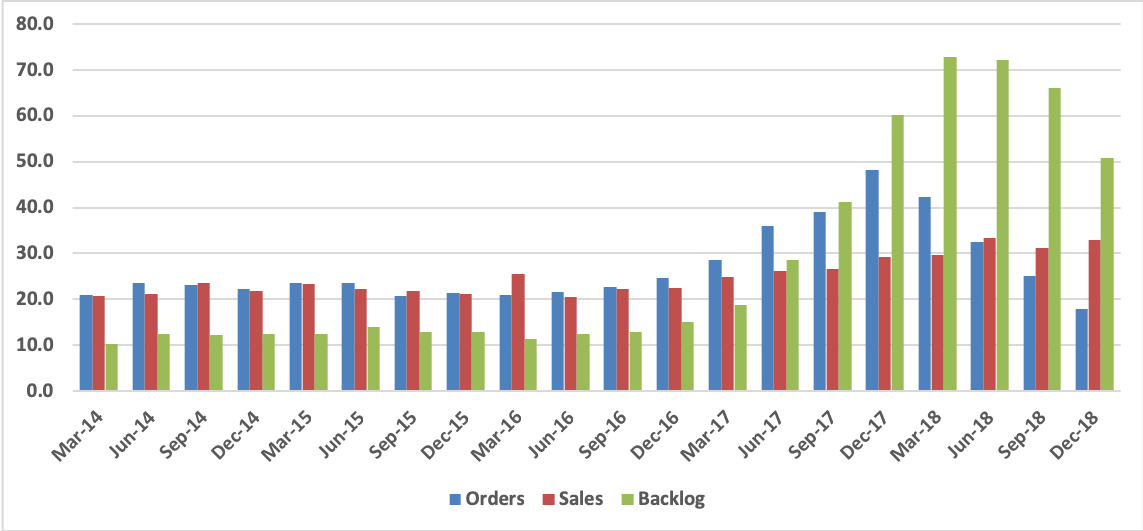

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

China Tower (788 HK) has rallied strongly in recent months and the question raised repeatedly in recent client meetings was “how much further is China Tower likely to rally?”. Chris Hoare sees China Tower’s position as unusual as the price moves are not driven by earnings upgrades or changed 5G expectations. Rather is is a sustained move post the IPO when the information in the market was incomplete and expectations were much lower. We were negative at the time of the IPO but changed our views as more information became available. We remain positive on the scope for revaluation in China Tower given its rapid revenue growth and low valuations vs EM peers. While the recent results were somewhat disappointing, we see good upside as the market factors is lower capex and higher returns.

Subscription rate is 797 to 1. Offer price was fixed at ₩48,000, substantially higher than the upper end. Deal size is now ₩168.5bil. Company value is put at slightly higher than ₩1tril. Demands are spread out pretty well between long-term funds and hot money and local and foreign investors as well. All of the orders are universally placed at 75% of upper end or higher.

Local street is betting on Autoever/Glovis merger not long after this IPO. That is, HMG is still wanting the initial Glovis/Mobis merger plan. To better manage to win shareholder support, they must be thinking that bigger Glovis can be an answer. This means HMG should do whatever it takes to make Autoever bigger in the immediate future.

This is what local street is betting on and why they went really aggressive on this IPO. As witnessed in the bookbuilding results, this street mentalitywon’t be changed any time soon. We should expect even stronger prices after new shares are listed on Mar 28.

Originally scheduled to close March 1st, near the end of February 2019, Bain Capital Japan’s acquisition vehicle (BCJ-34) extended the ¥610/share Tender Offer MBO deadline by 11 days from March 1st to March 11th. Of course, that was something of a moot point – by that time, the shares hadn’t traded at less than a 15% premium to terms for a week after well-known local activist Yoshiaki Murakami’s vehicle Reno KK and affiliates had taken a stake of just below 10%.

On the 8th of March, BCJ-34 raised its Tender Offer Price by 14.8% to ¥700/share and extended the Tender Offer by almost two weeks to the 25th of March. It also lowered the amount which needs to be bought to 50.1% from 66.67%. In that amended filing the buyer included words 「公開買付者は、本開買付条件の変更後の本公開買付価格を最終的なものとし、今後、本公開買付価格を一切変更しないことの決定をしております。」which roughly translates to “The Offeror, having changed the terms, has made This Tender Offer Price final, and from this point onward, has decided to absolutely not raise the Tender Offer Price.”

That’s that, but since then, the shares have not traded as low as the newly raised Tender Offer Price.

With one week to go, Aoyama Fudosan yesterdat announced it had lifted its stake to 747,800 shares or 3.00% of shares out, which brings the combined Reno KK/Aoyama Fudosan stake to 11.71%.

Given the 1.1mm shares traded since the 11th (i.e. shares which if Murakami-san had bought he would not have to report until the 19th (today)) and that the share price was up sharply in decent volume this afternoon, it would not be difficult to imagine a higher stake being reported in the days ahead.

Murakami-san is not going away. This is starting to look a bit like another Murakami situation of recent. And that one turned out well.

ZTO Express (ZTO US)‘s earnings will fail to meet the high expectations of sell-side analysts and investors who seeit as a cheap proxy for Chinese e-commerce activity.

China’s express sector revenue grew 43.5% YoY in 2016, the year ZTO went public. Last year, revenue growth was just half that (21.8%), and we expect the sector’s growth to continue to moderate over the next few years.

The express sector is also evolving in ways that will put downward pressure on profitability and require greater investment from the express companies.

We expect the profitability of ZTO’s express business to decline in the medium-term as the company adjusts to slowing demand and emerging sector trends. Our earnings estimates, which are far below consensus figures, reflect these challenges.

ZTO suffers from declining earnings quality and two accounting issues that we feel make it a risky, unattractive investment. Our 12-month target price for ZTO is US$13.31, based on 16 times our blended 2019-20 EPS estimates. We rate the stock Sell.

On March 6th, a day before the Hitachi Ltd (6501 JP) Taiwan elevator business Tender Offer for just over a third of Yungtay Engineering (1507 TT) was expected to close, the closing date was extended to 22 April, notably because the acquiring entity had not yet received Taiwan Ministry of Economy Investment Commission approval for the foreign investment, and the Fair Trading Commission had not yet given the green light, so there was no hope of getting it done by the next day in accordance with Taiwan’s Public Acquisition of Public Company Shares Administrative Law Article 18 Para 2. The proposed purchase price was unchanged at NT$60.

While there have been noises in the market that both Otis and Schindler, which are reported to hold roughly 5-6% each (last year’s shareholder list included UT Park View which United Technologies (UTX US)‘s 10-K showed was a wholly-owned sub) were willing to offer more than Hitachi’s offered NT$60 (and MOPS filings indicate the board approval meeting in end-January referenced a NT$63 potential bid), there was no competitive bid made public and to the authorities by five business days prior to the first bid close (which would have been 26 Feb) as per the same law Article 7 Para 2.

Since then, there have also been other ructions. While terms remain unchanged, it is worthwhile looking into what has been going on. This is still interesting and because of its various inputs, slightly disconcerting to some, and the modalities continue to surprise me.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Subscription rate is 797 to 1. Offer price was fixed at ₩48,000, substantially higher than the upper end. Deal size is now ₩168.5bil. Company value is put at slightly higher than ₩1tril. Demands are spread out pretty well between long-term funds and hot money and local and foreign investors as well. All of the orders are universally placed at 75% of upper end or higher.

Local street is betting on Autoever/Glovis merger not long after this IPO. That is, HMG is still wanting the initial Glovis/Mobis merger plan. To better manage to win shareholder support, they must be thinking that bigger Glovis can be an answer. This means HMG should do whatever it takes to make Autoever bigger in the immediate future.

This is what local street is betting on and why they went really aggressive on this IPO. As witnessed in the bookbuilding results, this street mentalitywon’t be changed any time soon. We should expect even stronger prices after new shares are listed on Mar 28.

Originally scheduled to close March 1st, near the end of February 2019, Bain Capital Japan’s acquisition vehicle (BCJ-34) extended the ¥610/share Tender Offer MBO deadline by 11 days from March 1st to March 11th. Of course, that was something of a moot point – by that time, the shares hadn’t traded at less than a 15% premium to terms for a week after well-known local activist Yoshiaki Murakami’s vehicle Reno KK and affiliates had taken a stake of just below 10%.

On the 8th of March, BCJ-34 raised its Tender Offer Price by 14.8% to ¥700/share and extended the Tender Offer by almost two weeks to the 25th of March. It also lowered the amount which needs to be bought to 50.1% from 66.67%. In that amended filing the buyer included words 「公開買付者は、本開買付条件の変更後の本公開買付価格を最終的なものとし、今後、本公開買付価格を一切変更しないことの決定をしております。」which roughly translates to “The Offeror, having changed the terms, has made This Tender Offer Price final, and from this point onward, has decided to absolutely not raise the Tender Offer Price.”

That’s that, but since then, the shares have not traded as low as the newly raised Tender Offer Price.

With one week to go, Aoyama Fudosan yesterdat announced it had lifted its stake to 747,800 shares or 3.00% of shares out, which brings the combined Reno KK/Aoyama Fudosan stake to 11.71%.

Given the 1.1mm shares traded since the 11th (i.e. shares which if Murakami-san had bought he would not have to report until the 19th (today)) and that the share price was up sharply in decent volume this afternoon, it would not be difficult to imagine a higher stake being reported in the days ahead.

Murakami-san is not going away. This is starting to look a bit like another Murakami situation of recent. And that one turned out well.

ZTO Express (ZTO US)‘s earnings will fail to meet the high expectations of sell-side analysts and investors who seeit as a cheap proxy for Chinese e-commerce activity.

China’s express sector revenue grew 43.5% YoY in 2016, the year ZTO went public. Last year, revenue growth was just half that (21.8%), and we expect the sector’s growth to continue to moderate over the next few years.

The express sector is also evolving in ways that will put downward pressure on profitability and require greater investment from the express companies.

We expect the profitability of ZTO’s express business to decline in the medium-term as the company adjusts to slowing demand and emerging sector trends. Our earnings estimates, which are far below consensus figures, reflect these challenges.

ZTO suffers from declining earnings quality and two accounting issues that we feel make it a risky, unattractive investment. Our 12-month target price for ZTO is US$13.31, based on 16 times our blended 2019-20 EPS estimates. We rate the stock Sell.

On March 6th, a day before the Hitachi Ltd (6501 JP) Taiwan elevator business Tender Offer for just over a third of Yungtay Engineering (1507 TT) was expected to close, the closing date was extended to 22 April, notably because the acquiring entity had not yet received Taiwan Ministry of Economy Investment Commission approval for the foreign investment, and the Fair Trading Commission had not yet given the green light, so there was no hope of getting it done by the next day in accordance with Taiwan’s Public Acquisition of Public Company Shares Administrative Law Article 18 Para 2. The proposed purchase price was unchanged at NT$60.

While there have been noises in the market that both Otis and Schindler, which are reported to hold roughly 5-6% each (last year’s shareholder list included UT Park View which United Technologies (UTX US)‘s 10-K showed was a wholly-owned sub) were willing to offer more than Hitachi’s offered NT$60 (and MOPS filings indicate the board approval meeting in end-January referenced a NT$63 potential bid), there was no competitive bid made public and to the authorities by five business days prior to the first bid close (which would have been 26 Feb) as per the same law Article 7 Para 2.

Since then, there have also been other ructions. While terms remain unchanged, it is worthwhile looking into what has been going on. This is still interesting and because of its various inputs, slightly disconcerting to some, and the modalities continue to surprise me.

Something of a slower week on Smartkarma this week (I contributed to that slowness by being away and under the weather when back) with about 120 insights published. A list of the insights to do with Japan and Korea this week are listed below.

For me, the MUST READS of this weak are the cashless payment-related pieces by Kirk Boodry and Michael Causton shown at the bottom.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Originally scheduled to close March 1st, near the end of February 2019, Bain Capital Japan’s acquisition vehicle (BCJ-34) extended the ¥610/share Tender Offer MBO deadline by 11 days from March 1st to March 11th. Of course, that was something of a moot point – by that time, the shares hadn’t traded at less than a 15% premium to terms for a week after well-known local activist Yoshiaki Murakami’s vehicle Reno KK and affiliates had taken a stake of just below 10%.

On the 8th of March, BCJ-34 raised its Tender Offer Price by 14.8% to ¥700/share and extended the Tender Offer by almost two weeks to the 25th of March. It also lowered the amount which needs to be bought to 50.1% from 66.67%. In that amended filing the buyer included words 「公開買付者は、本開買付条件の変更後の本公開買付価格を最終的なものとし、今後、本公開買付価格を一切変更しないことの決定をしております。」which roughly translates to “The Offeror, having changed the terms, has made This Tender Offer Price final, and from this point onward, has decided to absolutely not raise the Tender Offer Price.”

That’s that, but since then, the shares have not traded as low as the newly raised Tender Offer Price.

With one week to go, Aoyama Fudosan yesterdat announced it had lifted its stake to 747,800 shares or 3.00% of shares out, which brings the combined Reno KK/Aoyama Fudosan stake to 11.71%.

Given the 1.1mm shares traded since the 11th (i.e. shares which if Murakami-san had bought he would not have to report until the 19th (today)) and that the share price was up sharply in decent volume this afternoon, it would not be difficult to imagine a higher stake being reported in the days ahead.

Murakami-san is not going away. This is starting to look a bit like another Murakami situation of recent. And that one turned out well.

ZTO Express (ZTO US)‘s earnings will fail to meet the high expectations of sell-side analysts and investors who seeit as a cheap proxy for Chinese e-commerce activity.

China’s express sector revenue grew 43.5% YoY in 2016, the year ZTO went public. Last year, revenue growth was just half that (21.8%), and we expect the sector’s growth to continue to moderate over the next few years.

The express sector is also evolving in ways that will put downward pressure on profitability and require greater investment from the express companies.

We expect the profitability of ZTO’s express business to decline in the medium-term as the company adjusts to slowing demand and emerging sector trends. Our earnings estimates, which are far below consensus figures, reflect these challenges.

ZTO suffers from declining earnings quality and two accounting issues that we feel make it a risky, unattractive investment. Our 12-month target price for ZTO is US$13.31, based on 16 times our blended 2019-20 EPS estimates. We rate the stock Sell.

On March 6th, a day before the Hitachi Ltd (6501 JP) Taiwan elevator business Tender Offer for just over a third of Yungtay Engineering (1507 TT) was expected to close, the closing date was extended to 22 April, notably because the acquiring entity had not yet received Taiwan Ministry of Economy Investment Commission approval for the foreign investment, and the Fair Trading Commission had not yet given the green light, so there was no hope of getting it done by the next day in accordance with Taiwan’s Public Acquisition of Public Company Shares Administrative Law Article 18 Para 2. The proposed purchase price was unchanged at NT$60.

While there have been noises in the market that both Otis and Schindler, which are reported to hold roughly 5-6% each (last year’s shareholder list included UT Park View which United Technologies (UTX US)‘s 10-K showed was a wholly-owned sub) were willing to offer more than Hitachi’s offered NT$60 (and MOPS filings indicate the board approval meeting in end-January referenced a NT$63 potential bid), there was no competitive bid made public and to the authorities by five business days prior to the first bid close (which would have been 26 Feb) as per the same law Article 7 Para 2.

Since then, there have also been other ructions. While terms remain unchanged, it is worthwhile looking into what has been going on. This is still interesting and because of its various inputs, slightly disconcerting to some, and the modalities continue to surprise me.

Something of a slower week on Smartkarma this week (I contributed to that slowness by being away and under the weather when back) with about 120 insights published. A list of the insights to do with Japan and Korea this week are listed below.

In this report, we provide an analysis of our pair trade idea between Doosan Heavy Industries (034020 KS)and Doosan Corp (000150 KS). Our strategy will be to be long Doosan Heavy Industries and be short Doosan Corp. Our base case strategy is to achieve gains of 7-9% on this pair trade over the next six months.

In the past two years, Moon Jae-In administration’s energy policy has been to further reduce the reliance on nuclear power and increase reliance in renewable and coal power. The use of nuclear power in Korea is highly impacted by politics. There are a few stocks in Korea such as Doosan Heavy Industries (034020 KS) where politics is very important. The conservative parties in Korea tend to favor the use of nuclear power. However, the ruling liberal party does not favor the use of nuclear power.

Among the domestic issues, the decline in the nuclear power generation and greater use of coal based power generation have been cited as key reasons why the fine dust problems has increased in Korea in the past two years. In fact, more than 0.42 million Korean citizens have signed petitions in the past few weeks that would oppose the continued decline in the use of nuclear power generation.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We have a really interesting and unusual situation in Korea right now with HDC Holdings (012630 KS)going activist on Samyang Foods (003230 KS). HDC Holdings is the second largest owner of Samyang Foods.

HDC Holdings is recommending that the company should exclude executive directors that have been sentenced to imprisonment on cases such as embezzlement and extreme negligence resulting in significant losses for Samyang Foods. This is an agenda which will be discussed in the Samyang Foods’ AGM next month on March 22nd.

HDC Holdings is taking a very unusual move right now in going against the traditional “save face” mentality in the Korea Inc. and trying to publicly urge Samyang Foods to make changes to its BOD.

KCL-SPH again extended the closing date of the offer from 18 February to 4 March 2019. M1’s shares are trading at S$2.04 per share, marginally below the VGO price of S$2.06 per share. We believe that the KCL-SPH should get the valid acceptances to complete the delisting and wholly own M1.

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

ZTO Express (ZTO US)‘s earnings will fail to meet the high expectations of sell-side analysts and investors who seeit as a cheap proxy for Chinese e-commerce activity.

China’s express sector revenue grew 43.5% YoY in 2016, the year ZTO went public. Last year, revenue growth was just half that (21.8%), and we expect the sector’s growth to continue to moderate over the next few years.

The express sector is also evolving in ways that will put downward pressure on profitability and require greater investment from the express companies.

We expect the profitability of ZTO’s express business to decline in the medium-term as the company adjusts to slowing demand and emerging sector trends. Our earnings estimates, which are far below consensus figures, reflect these challenges.

ZTO suffers from declining earnings quality and two accounting issues that we feel make it a risky, unattractive investment. Our 12-month target price for ZTO is US$13.31, based on 16 times our blended 2019-20 EPS estimates. We rate the stock Sell.

On March 6th, a day before the Hitachi Ltd (6501 JP) Taiwan elevator business Tender Offer for just over a third of Yungtay Engineering (1507 TT) was expected to close, the closing date was extended to 22 April, notably because the acquiring entity had not yet received Taiwan Ministry of Economy Investment Commission approval for the foreign investment, and the Fair Trading Commission had not yet given the green light, so there was no hope of getting it done by the next day in accordance with Taiwan’s Public Acquisition of Public Company Shares Administrative Law Article 18 Para 2. The proposed purchase price was unchanged at NT$60.

While there have been noises in the market that both Otis and Schindler, which are reported to hold roughly 5-6% each (last year’s shareholder list included UT Park View which United Technologies (UTX US)‘s 10-K showed was a wholly-owned sub) were willing to offer more than Hitachi’s offered NT$60 (and MOPS filings indicate the board approval meeting in end-January referenced a NT$63 potential bid), there was no competitive bid made public and to the authorities by five business days prior to the first bid close (which would have been 26 Feb) as per the same law Article 7 Para 2.

Since then, there have also been other ructions. While terms remain unchanged, it is worthwhile looking into what has been going on. This is still interesting and because of its various inputs, slightly disconcerting to some, and the modalities continue to surprise me.

Something of a slower week on Smartkarma this week (I contributed to that slowness by being away and under the weather when back) with about 120 insights published. A list of the insights to do with Japan and Korea this week are listed below.

In this report, we provide an analysis of our pair trade idea between Doosan Heavy Industries (034020 KS)and Doosan Corp (000150 KS). Our strategy will be to be long Doosan Heavy Industries and be short Doosan Corp. Our base case strategy is to achieve gains of 7-9% on this pair trade over the next six months.

In the past two years, Moon Jae-In administration’s energy policy has been to further reduce the reliance on nuclear power and increase reliance in renewable and coal power. The use of nuclear power in Korea is highly impacted by politics. There are a few stocks in Korea such as Doosan Heavy Industries (034020 KS) where politics is very important. The conservative parties in Korea tend to favor the use of nuclear power. However, the ruling liberal party does not favor the use of nuclear power.

Among the domestic issues, the decline in the nuclear power generation and greater use of coal based power generation have been cited as key reasons why the fine dust problems has increased in Korea in the past two years. In fact, more than 0.42 million Korean citizens have signed petitions in the past few weeks that would oppose the continued decline in the use of nuclear power generation.

In this insight, we will look at the updates on financials and operating metrics, compare it to other listed online education companies, and run the deal through our framework.

The increase in spending on marketing has not yielded the intended results as the growth rates of student enrollment and gross billings slowing down. Furthermore, aggressive spending behavior is similar to that of STG and LAIX and both companies did not perform well post listing.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

On March 6th, a day before the Hitachi Ltd (6501 JP) Taiwan elevator business Tender Offer for just over a third of Yungtay Engineering (1507 TT) was expected to close, the closing date was extended to 22 April, notably because the acquiring entity had not yet received Taiwan Ministry of Economy Investment Commission approval for the foreign investment, and the Fair Trading Commission had not yet given the green light, so there was no hope of getting it done by the next day in accordance with Taiwan’s Public Acquisition of Public Company Shares Administrative Law Article 18 Para 2. The proposed purchase price was unchanged at NT$60.

While there have been noises in the market that both Otis and Schindler, which are reported to hold roughly 5-6% each (last year’s shareholder list included UT Park View which United Technologies (UTX US)‘s 10-K showed was a wholly-owned sub) were willing to offer more than Hitachi’s offered NT$60 (and MOPS filings indicate the board approval meeting in end-January referenced a NT$63 potential bid), there was no competitive bid made public and to the authorities by five business days prior to the first bid close (which would have been 26 Feb) as per the same law Article 7 Para 2.

Since then, there have also been other ructions. While terms remain unchanged, it is worthwhile looking into what has been going on. This is still interesting and because of its various inputs, slightly disconcerting to some, and the modalities continue to surprise me.

Something of a slower week on Smartkarma this week (I contributed to that slowness by being away and under the weather when back) with about 120 insights published. A list of the insights to do with Japan and Korea this week are listed below.

In this report, we provide an analysis of our pair trade idea between Doosan Heavy Industries (034020 KS)and Doosan Corp (000150 KS). Our strategy will be to be long Doosan Heavy Industries and be short Doosan Corp. Our base case strategy is to achieve gains of 7-9% on this pair trade over the next six months.

In the past two years, Moon Jae-In administration’s energy policy has been to further reduce the reliance on nuclear power and increase reliance in renewable and coal power. The use of nuclear power in Korea is highly impacted by politics. There are a few stocks in Korea such as Doosan Heavy Industries (034020 KS) where politics is very important. The conservative parties in Korea tend to favor the use of nuclear power. However, the ruling liberal party does not favor the use of nuclear power.

Among the domestic issues, the decline in the nuclear power generation and greater use of coal based power generation have been cited as key reasons why the fine dust problems has increased in Korea in the past two years. In fact, more than 0.42 million Korean citizens have signed petitions in the past few weeks that would oppose the continued decline in the use of nuclear power generation.

In this insight, we will look at the updates on financials and operating metrics, compare it to other listed online education companies, and run the deal through our framework.

The increase in spending on marketing has not yielded the intended results as the growth rates of student enrollment and gross billings slowing down. Furthermore, aggressive spending behavior is similar to that of STG and LAIX and both companies did not perform well post listing.

Keppel Infrastructure Trust (KIT SP) plans to raise US$450m via an equity placement and non-renounacable preferential offering. Its sponsor, Keppel Corp Ltd (KEP SP) will subscribe in the placement and the preferential offering to maintain its 18.2% stake.

KIT announced the acquisition of IXOM in Nov 2018 and has been talking about the need to issue equity ever since. Its earlier presentations seem to indicate a preference for raising a large sum via an equity issuance. Furthermore, despite the smaller raise the accretion to DPU is probably only marginal.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Something of a slower week on Smartkarma this week (I contributed to that slowness by being away and under the weather when back) with about 120 insights published. A list of the insights to do with Japan and Korea this week are listed below.

In this report, we provide an analysis of our pair trade idea between Doosan Heavy Industries (034020 KS)and Doosan Corp (000150 KS). Our strategy will be to be long Doosan Heavy Industries and be short Doosan Corp. Our base case strategy is to achieve gains of 7-9% on this pair trade over the next six months.

In the past two years, Moon Jae-In administration’s energy policy has been to further reduce the reliance on nuclear power and increase reliance in renewable and coal power. The use of nuclear power in Korea is highly impacted by politics. There are a few stocks in Korea such as Doosan Heavy Industries (034020 KS) where politics is very important. The conservative parties in Korea tend to favor the use of nuclear power. However, the ruling liberal party does not favor the use of nuclear power.

Among the domestic issues, the decline in the nuclear power generation and greater use of coal based power generation have been cited as key reasons why the fine dust problems has increased in Korea in the past two years. In fact, more than 0.42 million Korean citizens have signed petitions in the past few weeks that would oppose the continued decline in the use of nuclear power generation.

In this insight, we will look at the updates on financials and operating metrics, compare it to other listed online education companies, and run the deal through our framework.

The increase in spending on marketing has not yielded the intended results as the growth rates of student enrollment and gross billings slowing down. Furthermore, aggressive spending behavior is similar to that of STG and LAIX and both companies did not perform well post listing.

Keppel Infrastructure Trust (KIT SP) plans to raise US$450m via an equity placement and non-renounacable preferential offering. Its sponsor, Keppel Corp Ltd (KEP SP) will subscribe in the placement and the preferential offering to maintain its 18.2% stake.

KIT announced the acquisition of IXOM in Nov 2018 and has been talking about the need to issue equity ever since. Its earlier presentations seem to indicate a preference for raising a large sum via an equity issuance. Furthermore, despite the smaller raise the accretion to DPU is probably only marginal.

Yokogawa Electric is one of the world’s leading suppliers of distributed control systems (DCS) used in the LNG, oil & gas, petrochemical and other industries. It is particularly strong in LNG, having provided control systems for dozens of liquefaction trains, LNG carriers and re-gasification plants.

Unlike Chiyoda Corporation (6366 JP) and JGC (1963 JP), which depend on a small number of large engineering, procurement and construction (EPC) orders, which can be as large as ¥500 billion, Yokogawa only rarely receives an order as large as ¥10 billion and most of its orders are less than ¥1 billion. It is geared primarily to ongoing investments and operating expenditures in its user industries, less exposed to highly variable orders for large LNG and other engineering projects, and relatively immune to cost overruns and other problems at projects gone wrong.

Margins have expanded over the past several years due to a combination of restructuring and technological advance. Unprofitable non-core businesses have been abandoned or sold, high-wage domestic employees retired, and administration, manufacturing and logistics rationalized. Enterprise and robotic process automation (RPA) software have been introduced and an Industrial Internet of Things (IIoT) cloud computing platform is under development. Top-line growth has been slow, but the operating margin has risen from from 5.0% in FY Mar-12 to 8.0% in FY Mar-18, and should reach 10% in FY Mar-21, in our estimation.

At ¥2,215 (Wednesday, March 13 closing price), the shares are selling at 23x our EPS estimate for FY Mar-19 and 20x our estimate for FY Mar-21. Projected EV/EBITDA multiples for the same two years are 9.8x and 8.2x. These and other projected valuation multiples are above their recent historical averages, but indicate upside potential of 20% or more if the anticipated upturn in new LNG investments materializes. Investors willing to take on more speculative risk should look at Chiyoda and JGC.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In this report, we provide an analysis of our pair trade idea between Doosan Heavy Industries (034020 KS)and Doosan Corp (000150 KS). Our strategy will be to be long Doosan Heavy Industries and be short Doosan Corp. Our base case strategy is to achieve gains of 7-9% on this pair trade over the next six months.

In the past two years, Moon Jae-In administration’s energy policy has been to further reduce the reliance on nuclear power and increase reliance in renewable and coal power. The use of nuclear power in Korea is highly impacted by politics. There are a few stocks in Korea such as Doosan Heavy Industries (034020 KS) where politics is very important. The conservative parties in Korea tend to favor the use of nuclear power. However, the ruling liberal party does not favor the use of nuclear power.

Among the domestic issues, the decline in the nuclear power generation and greater use of coal based power generation have been cited as key reasons why the fine dust problems has increased in Korea in the past two years. In fact, more than 0.42 million Korean citizens have signed petitions in the past few weeks that would oppose the continued decline in the use of nuclear power generation.

In this insight, we will look at the updates on financials and operating metrics, compare it to other listed online education companies, and run the deal through our framework.

The increase in spending on marketing has not yielded the intended results as the growth rates of student enrollment and gross billings slowing down. Furthermore, aggressive spending behavior is similar to that of STG and LAIX and both companies did not perform well post listing.

Keppel Infrastructure Trust (KIT SP) plans to raise US$450m via an equity placement and non-renounacable preferential offering. Its sponsor, Keppel Corp Ltd (KEP SP) will subscribe in the placement and the preferential offering to maintain its 18.2% stake.

KIT announced the acquisition of IXOM in Nov 2018 and has been talking about the need to issue equity ever since. Its earlier presentations seem to indicate a preference for raising a large sum via an equity issuance. Furthermore, despite the smaller raise the accretion to DPU is probably only marginal.

Yokogawa Electric is one of the world’s leading suppliers of distributed control systems (DCS) used in the LNG, oil & gas, petrochemical and other industries. It is particularly strong in LNG, having provided control systems for dozens of liquefaction trains, LNG carriers and re-gasification plants.

Unlike Chiyoda Corporation (6366 JP) and JGC (1963 JP), which depend on a small number of large engineering, procurement and construction (EPC) orders, which can be as large as ¥500 billion, Yokogawa only rarely receives an order as large as ¥10 billion and most of its orders are less than ¥1 billion. It is geared primarily to ongoing investments and operating expenditures in its user industries, less exposed to highly variable orders for large LNG and other engineering projects, and relatively immune to cost overruns and other problems at projects gone wrong.

Margins have expanded over the past several years due to a combination of restructuring and technological advance. Unprofitable non-core businesses have been abandoned or sold, high-wage domestic employees retired, and administration, manufacturing and logistics rationalized. Enterprise and robotic process automation (RPA) software have been introduced and an Industrial Internet of Things (IIoT) cloud computing platform is under development. Top-line growth has been slow, but the operating margin has risen from from 5.0% in FY Mar-12 to 8.0% in FY Mar-18, and should reach 10% in FY Mar-21, in our estimation.

At ¥2,215 (Wednesday, March 13 closing price), the shares are selling at 23x our EPS estimate for FY Mar-19 and 20x our estimate for FY Mar-21. Projected EV/EBITDA multiples for the same two years are 9.8x and 8.2x. These and other projected valuation multiples are above their recent historical averages, but indicate upside potential of 20% or more if the anticipated upturn in new LNG investments materializes. Investors willing to take on more speculative risk should look at Chiyoda and JGC.

We visited one big-cap stock, Berli Jucker, and one pip-squeak recent IPO M Vision today. A couple of highlights:

Slow revenue growth at BJC at under 5% largely driven by Big C (hypermarket), but earnings growth was strong at 28% mainly due to lower cost of palm oil in the snack business.

Good progress in Vietnam with expansion of the bottle capacity this year and SABECO increasing purchases of bottles.

Overall unimpressed. The company isn’t expecting to grow revenues more than 9% this year, and many of the cost cuts we saw in 2018 are clearly one-offs. Higher oil prices are likely to lead to rising palm oil prices this year too, since the two commodities are linked through substitution effect.

MVP underwent a bad year on the profit level, but their various businesses, at least on the top line level, looks like it could recover quickly this year.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.