The accounting fraud issue had hammered the Celltrion duo nearly equally up until Dec 26. But last two days were different. Healthcare got hurt much more deeply. Celltrion fell only 2.41%, but Healthcare fell 11.52%.

The accounting issue is supposed to be equal to both. KOSPI move and merger are still alive to push up Healthcare. Local institutions and foreigners have bashed both pretty much equally in the last two days. This is another sign that it was more of a price divergence than a mean reversion.

The duo is now at 20D MA and also the yearly mean. I expect it to go substantially below the yearly mean on KOSPI move and merger expectations. A powerful downwardly mean adjusting force still seems to be in action. I’d long Healthcare and short Celltrion to exploit the latest price divergence.

Halla Holdings is falling nearly 5% today. Holdco said it’d give a ₩2,000 div per share. This is about 4.5% div yield at yesterday’s closing price. 5% drop today shouldn’t be much as an ex-dividend date price drop. Mando fell 5%. Mando was oversold relative to the other local auto stocks, particularly to Halla Holdings. They are still close to +1 σ on a 20D MA.

Mando-Hella Elec has been another reason behind Holdco’s valuation divergence against Mando lately. I believe Mando-Hella is being overhyped. Mando-Hella-caused divergence should no longer be effective. I expect ‘downwardly’ mean reversion from now on. I’d go short Holdco and long Mando at this point.

The Offer price of $4.56/share, an 82.4% premium to last close, has been declared final. The price corresponds to the subscription of 329mn domestic shares (~47.16% of the existing issued domestic shares and ~24.02% of the existing total issued shares) @$4.56/share by HEC in January this year.

Of greater significance, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors can justify recommending an Offer to shareholders at any price which gave cash less cavalier than cash.

Dissension rights are available, however, what constitutes a “fair price” under those rights, and the timing of the settlement under such rights, are not evident.

As all PRC approvals have been obtained, this transaction may complete earlier than prior mergers by absorption, which have taken 6-8 months from the initial announcement.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

I initiated SamE short Common/long 1P trade on Nov 29. This trade delivered the highest yield on Dec 13 at 4.55% with Nov 29 as the reference date. We are now slightly below +1 σ.

Common/1P relative price gap should get narrower. Price wise, 1P discount started at 19.81% on Nov 29 and reached the lowest at 16.38% on Dec 13. It reverted back to 18.69%, down 1.12%p. Market cap wise, Common/1P ratio is still higher than Nov 29. This suggests 1P’s catching up job isn’t over yet.

Div yield difference is still at a record high for 1P. CJ Corp (001040 KS)‘s recent class B pref issuance should be another plus. It will play in favor of those ownership transfer related prefs. I’d continue to hold onto this position until we move into March OGM cycle.

On 26 November 2018, 28.22%-shareholder DNO ASA (DNO NO)announced a cash offer for Faroe Petroleum (FPM LN) of GBP 1.52/share, a 21% premium to the pre-announcement price on November 23rd, but a 44.8% premium to Faroe’s share price of GBP 1.05 as at 3 April 2018, the last business day before DNO announced its first acquisition of shares in Faroe.

This is a hostile offer with DNO openly criticising the management’s corporate-governance culture, share performance, operational abilities, and deal-making. An indication of the level of this hostility can be found in the circular to shareholders (page 9): “Since listing, no dividends have been paid and no capital otherwise returned to shareholders. Meanwhile, back at the ranch, the Faroe directors have been awarded a high number of share options at nil cost.” In response, Faroe’s board describes the deal as “opportunistic, unsolicited, and inadequate”, and has advised the shareholders to reject the offer.

The deal was initially conditional on receiving a minimum acceptance of 57.5% of Faroe’s total issued share capital; however after acquiring shares in the market, DNO announced yesterday it held 30% of issued shares in Faroe, triggering a mandatory offer, and Faroe is now therefore subject to takeover regulation, and the deal requires a lower acceptance threshold of 50%.

Currently trading slightly through terms. Together with shares accepting its offer, DNO currently has 43.1%.

The offer has now automatically been extended until the 18 January and DNO has until the 27 January to improve or revise the Offer. This may need a slight kiss to push it over the line.

We believe that Jangho’s bid is opportunistic and unattractive. Also, if Jangho puts in an improved bid, getting regulatory blessing will be an uphill task.

One of the reasons why the Nexon’s founder Kim Jung-Joo, who is only 50 years old, is trying to sell his entire stake in Nexon may have been due to the recent allegations about him giving about $380,000 worth of Nexon stock (prior to its listing) to his old high school classmate (who is now a senior public prosecutor) for free. Kim Jung-Joo has repeatedly faced allegations and attended numerous court hearings on this matter in the past two years. He may have gotten a bit tired from all these allegations.

Given the enormous size of this acquisition, the two leading Korean game companies including NCsoft Corp (036570 KS) and Netmarble Games (251270 KS) are not likely to purchase Nexon. Rather, the leading contender to buy Nexon right now is likely to be Tencent Holdings (700 HK). The sheer huge size of this deal will represent one of the largest M&A deals in Asia in 2019.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The average NAV discount of a basket of 40 Holdcos steadily, and not altogether unsurprisingly, widened throughout the year.

Passive, tech-related and illiquid Holdcos widened most; while cross-border and property Holdcos were the best of the worst.

Illiquid, property, and passive Holdcos’ underperformance (or widening) was more pronounced in the first half. Tech Holdcos primarily widened in the second half.

Below the various NAV discount chart summaries of various baskets are my weekly setup/unwind tables.

This, and other relationships discussed below, trade with: 1) a minimum liquidity threshold of US$1mn on a 90-day moving average; and 2) a minimum 20% ‘market capitalisation’ threshold, whereby the value of the holding/Opco held must be at least 20% of the parent’s market cap.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainlanders in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: those with a market capitalization of above USD 5 billion, those with a market capitalization between USD 1 billion and USD 5 billion, and those with a market capitalization between USD 500 million and USD 1 billion.

Thanks to improved Korea-China relation, Opco (004320 KS) shares have nicely rebounded lately. Nongshim Holdco hasn’t caught up. This created the highest price ratio gap in 2 years. On a 20D MA, they are close to the mean. But on a 2 year mean, Holdco is currently and still severely undervalued.

Liquidity has played a major role in the recent price gap widening. At a rebounding cycle like this, liquidity must have been a huge factor. But it shouldn’t be too long until Holdco catches up. Opco has kinda drifted sideways for a while now. This should be time for Holdco to begin a catchup.

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of fully-diluted shares (current shares out + 26.826mm Options + ~2.1mm Award shares).

The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The other terms and conditions of this deal will be set out in the offer document which is expected to be despatched in mid-January 2019 (14-21 days from 28 December).

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.10 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

Healthscope Ltd (HSO AU), Australia’s second-largest private hospital operator, is caught again in a bidding war between Brookfield Asset Management (BAM US) and BGH-AustralianSuper. On 21 December 2018, Healthscope extended exclusive due diligence with Brookfield. Brookfield noted that it has “no reason to believe it would not be willing and able to proceed” with its proposal.

The popular narrative is that should a binding proposal materialise; shareholders can expect a bidding war among the existing bidders, and potential new bidders as Healthscope is “in play”. While there is there is a possibility for some ‘‘sweetening’’ to the bid price, we think that that the formal “winning” bid is unlikely to be materially above the current Brookfield bid.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

As the merger between TMB and Thanachart gets a nudge from the Ministry of Finance and could be finalized this month, we try to answer a few questions in this review:

Takeover premium. Based on our estimates, the potential improvements in ROE from the merger and potential divestment of MBK, we think it justifies an Bt11.1/sh premium for Thanachart. The new best case price target for Thanachart stands at Bt64.25/sh, implying a 29% premium over current share price.

Negotiations will play a key role in the actual takeover price. We provide a table of how much money is left on the table for TMB if they acquire TCAP at lower than what we expect.

Benefits. Thanachart has a higher ROE than TMB and appears smaller but better managed. The merger would allow TMB to re-enter the securities business (more cross-selling), enlarge its asset management franchise, and scale up deposit base for both banks…more so on the Thanachart side.

Size. Even after the merger, the combined bank would still have a much smaller headcount than BAY, smallest of the five largest Thai banks. However, it would have more branches than BAY and just 11% less branches than KBANK.

Hyosung Corporation (004800 KS) had fallen 16% just in two days. Holdco is now at a 50% discount to NAV. This is a 10%p drop from 10 days ago (Dec 19). Holdco price must have been overly corrected. The ongoing police investigation on Cho Hyun-joon’s alleged crime won’t lead to a delisting. 10%p drop in discount to NAV must be a price divergence, not a sensible price correction.

Trade volume remained steady. Local hedge funds led the selling on Dec 27. Even they changed their position the following day. No short selling spike has been seen either. Hyosung is one of the highest yielding div holdco stocks. Hyosung Capital liquidation and Anyang Plant revaluation would be another short-term plus.

I’d exploit this price divergence. It would soon revert to the Dec 19 discount level. It should at least stay at the peer average.

Just how will Harbin Electric Co Ltd H (1133 HK)‘s independent directors justify recommending an Offer to shareholders at a price which gave cash less cavalier than cash?

MYOB Group Ltd (MYO AU)‘s directors grudgingly yet understandably enter an agreed deal with KKR.

As previously discussed in Harbin Electric Expected To Be Privatised, Harbin Electric (HE) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption. The Offer price of $4.56/share, an 82.4% premium to last close, is bang in line with that paid by HEC in January this year for new domestic shares. The Offer price has been declared final.

Of note, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors (and the IFA) can justify recommending an Offer to shareholders at any price below the net cash/share, especially when the underlying business is profit-generating.

Dissension rights are available, however, there is no administrative guidance on the substantive as well as procedural rules as to how the “fair price” will be determined under PRC and HK Law.

Trading at a gross/annualised spread of 15%/28% assuming end-July completion, based on the average timeline for merger by absorption precedents. As HEC is only waiting for approval from independent H-shareholders suggests this transaction may complete earlier than precedents.

KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal. The Offer price assumes no full-year dividend is paid.

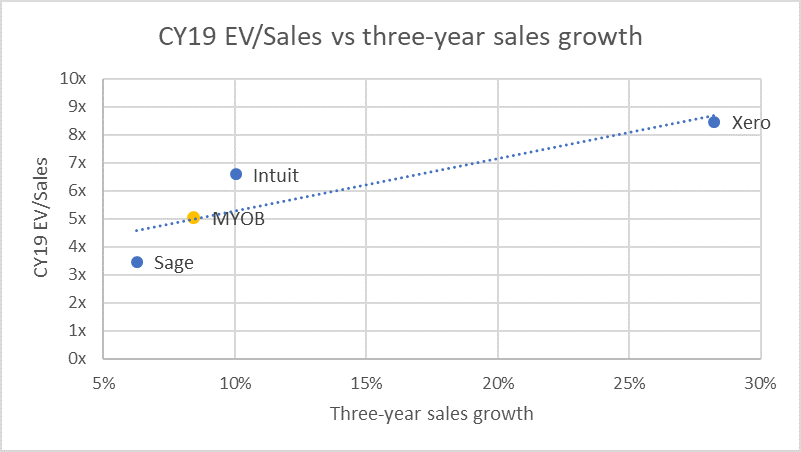

On balance, MYOB’s board has made the right decision to accept KKR’s reduced Offer. The argument that MYOB is a “known turnaround story” is challenged as cloud-based accounting software providers Xero Ltd (XRO AU)and Intuit Inc (INTU US) grab market share. This is also reflected in MYOB’s forecast 7% revenue growth in FY18 and follows a 10% decline in first-half profit, despite a 61% jump in online subscribers.

And there is justification for KKR’s lowering the Offer price: the ASX is down 10% since KKR’s initial tilt, the ASX technology index is off by ~14%, a basket of listed Aussie peers are down 17%, while Xero, the most comparable peer, is down ~20%. The Scheme Offer is at a ~27% premium to the estimated adjusted (for the ASX index) downside price of $2.68/share.

Bain was okay selling at $3.15/share to KKR and will be fine selling its remaining ~6.5% stake at $3.40. Presumably, MYOB sounded out the other major shareholders such as Fidelity, Yarra Funds Management, Vanguard etc as to their read on the revised $3.40 offer, before agreeing to the SIA with KKR.

If the markets avoid further declines, this deal will probably get up. If the markets rebound, the outcome is less assured. This Tuesday marks the beginning of a new year and a renewed mandate for investors to take risk, especially an agreed deal; but the current 5.3% annualised spread is tight.

The Ministry of Finance, the major shareholder of TMB, confirmed that both Krung Thai Bank Pub (KTB TB)and Thanachart Capital (TCAP TB)had engaged in merger talks with TMB. Considering an earlier KTB/TMB courtship failed, it is more likely, but by no means guaranteed, that the deal with Thanachart will happen. Bloomberg is also reporting that Thanachart and TMB want to do a deal before the next elections, which is less than two months away.

TMB is much bigger than Thanachart and therefore it may boil down to whether TMB wants to be the target or acquirer. In Athaporn Arayasantiparb, CFA‘s view, a deal with Thanachart would leave TMB as the acquirer rather than the target. But Thanachart’s management has a better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than Bank Of Ayudhya (BAY TB) and would not change the bank rankings; but it would give TMB a bigger presence in asset management, hire-purchase finance and a re-entry into the securities business.

Mando accounts for 45% of Halla’s NAV, which is currently trading at a 50% discount. Sanghyun Park believes the recent narrowing in the discount may be due to the hype attached to Mando-Hella Elec, which he believes is overdone; and recommends a short Holdco and long Mando. Using Sanghyun’s figures, I see the discount to NAV at 51%, 2STD above the 12-month average of ~47%.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

The accounting fraud issue had hammered the Celltrion duo nearly equally up until Dec 26. But last two days were different. Healthcare got hurt much more deeply. Celltrion fell only 2.41%, but Healthcare fell 11.52%.

The accounting issue is supposed to be equal to both. KOSPI move and merger are still alive to push up Healthcare. Local institutions and foreigners have bashed both pretty much equally in the last two days. This is another sign that it was more of a price divergence than a mean reversion.

The duo is now at 20D MA and also the yearly mean. I expect it to go substantially below the yearly mean on KOSPI move and merger expectations. A powerful downwardly mean adjusting force still seems to be in action. I’d long Healthcare and short Celltrion to exploit the latest price divergence.

Halla Holdings is falling nearly 5% today. Holdco said it’d give a ₩2,000 div per share. This is about 4.5% div yield at yesterday’s closing price. 5% drop today shouldn’t be much as an ex-dividend date price drop. Mando fell 5%. Mando was oversold relative to the other local auto stocks, particularly to Halla Holdings. They are still close to +1 σ on a 20D MA.

Mando-Hella Elec has been another reason behind Holdco’s valuation divergence against Mando lately. I believe Mando-Hella is being overhyped. Mando-Hella-caused divergence should no longer be effective. I expect ‘downwardly’ mean reversion from now on. I’d go short Holdco and long Mando at this point.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The Offer price of $4.56/share, an 82.4% premium to last close, has been declared final. The price corresponds to the subscription of 329mn domestic shares (~47.16% of the existing issued domestic shares and ~24.02% of the existing total issued shares) @$4.56/share by HEC in January this year.

Of greater significance, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors can justify recommending an Offer to shareholders at any price which gave cash less cavalier than cash.

Dissension rights are available, however, what constitutes a “fair price” under those rights, and the timing of the settlement under such rights, are not evident.

As all PRC approvals have been obtained, this transaction may complete earlier than prior mergers by absorption, which have taken 6-8 months from the initial announcement.

On 24 December, MYOB Group Ltd (MYO AU) announced that it entered into a scheme implementation agreement under which KKR will acquire MYOB at $3.40 per share, which is 10% lower than 2 November offer price of A$3.77. MYOB claims its decision to recommend KKR’s lower offer was based on current market uncertainty, long-term nature of its strategic growth plans and the go-shop provisions of the deal.

We believe that KKR’s revised offer is opportunistic, but MYOB’s shareholders are caught between a rock and a hard place. Shareholders can take a short-term view and grudgingly accept the revised offer. Alternatively, shareholders can take a long-term view by rejecting the offer and hope MYOB’s strategic growth plans and a market recovery can reverse the inevitable share price collapse.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

On 26 November 2018, 28.22%-shareholder DNO ASA (DNO NO)announced a cash offer for Faroe Petroleum (FPM LN) of GBP 1.52/share, a 21% premium to the pre-announcement price on November 23rd, but a 44.8% premium to Faroe’s share price of GBP 1.05 as at 3 April 2018, the last business day before DNO announced its first acquisition of shares in Faroe.

This is a hostile offer with DNO openly criticising the management’s corporate-governance culture, share performance, operational abilities, and deal-making. An indication of the level of this hostility can be found in the circular to shareholders (page 9): “Since listing, no dividends have been paid and no capital otherwise returned to shareholders. Meanwhile, back at the ranch, the Faroe directors have been awarded a high number of share options at nil cost.” In response, Faroe’s board describes the deal as “opportunistic, unsolicited, and inadequate”, and has advised the shareholders to reject the offer.

The deal was initially conditional on receiving a minimum acceptance of 57.5% of Faroe’s total issued share capital; however after acquiring shares in the market, DNO announced yesterday it held 30% of issued shares in Faroe, triggering a mandatory offer, and Faroe is now therefore subject to takeover regulation, and the deal requires a lower acceptance threshold of 50%.

Currently trading slightly through terms. Together with shares accepting its offer, DNO currently has 43.1%.

The offer has now automatically been extended until the 18 January and DNO has until the 27 January to improve or revise the Offer. This may need a slight kiss to push it over the line.

We believe that Jangho’s bid is opportunistic and unattractive. Also, if Jangho puts in an improved bid, getting regulatory blessing will be an uphill task.

One of the reasons why the Nexon’s founder Kim Jung-Joo, who is only 50 years old, is trying to sell his entire stake in Nexon may have been due to the recent allegations about him giving about $380,000 worth of Nexon stock (prior to its listing) to his old high school classmate (who is now a senior public prosecutor) for free. Kim Jung-Joo has repeatedly faced allegations and attended numerous court hearings on this matter in the past two years. He may have gotten a bit tired from all these allegations.

Given the enormous size of this acquisition, the two leading Korean game companies including NCsoft Corp (036570 KS) and Netmarble Games (251270 KS) are not likely to purchase Nexon. Rather, the leading contender to buy Nexon right now is likely to be Tencent Holdings (700 HK). The sheer huge size of this deal will represent one of the largest M&A deals in Asia in 2019.

The average NAV discount of a basket of 40 Holdcos steadily, and not altogether unsurprisingly, widened throughout the year.

Passive, tech-related and illiquid Holdcos widened most; while cross-border and property Holdcos were the best of the worst.

Illiquid, property, and passive Holdcos’ underperformance (or widening) was more pronounced in the first half. Tech Holdcos primarily widened in the second half.

Below the various NAV discount chart summaries of various baskets are my weekly setup/unwind tables.

This, and other relationships discussed below, trade with: 1) a minimum liquidity threshold of US$1mn on a 90-day moving average; and 2) a minimum 20% ‘market capitalisation’ threshold, whereby the value of the holding/Opco held must be at least 20% of the parent’s market cap.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Hyosung Corporation (004800 KS) had fallen 16% just in two days. Holdco is now at a 50% discount to NAV. This is a 10%p drop from 10 days ago (Dec 19). Holdco price must have been overly corrected. The ongoing police investigation on Cho Hyun-joon’s alleged crime won’t lead to a delisting. 10%p drop in discount to NAV must be a price divergence, not a sensible price correction.

Trade volume remained steady. Local hedge funds led the selling on Dec 27. Even they changed their position the following day. No short selling spike has been seen either. Hyosung is one of the highest yielding div holdco stocks. Hyosung Capital liquidation and Anyang Plant revaluation would be another short-term plus.

I’d exploit this price divergence. It would soon revert to the Dec 19 discount level. It should at least stay at the peer average.

Just how will Harbin Electric Co Ltd H (1133 HK)‘s independent directors justify recommending an Offer to shareholders at a price which gave cash less cavalier than cash?

MYOB Group Ltd (MYO AU)‘s directors grudgingly yet understandably enter an agreed deal with KKR.

As previously discussed in Harbin Electric Expected To Be Privatised, Harbin Electric (HE) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption. The Offer price of $4.56/share, an 82.4% premium to last close, is bang in line with that paid by HEC in January this year for new domestic shares. The Offer price has been declared final.

Of note, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors (and the IFA) can justify recommending an Offer to shareholders at any price below the net cash/share, especially when the underlying business is profit-generating.

Dissension rights are available, however, there is no administrative guidance on the substantive as well as procedural rules as to how the “fair price” will be determined under PRC and HK Law.

Trading at a gross/annualised spread of 15%/28% assuming end-July completion, based on the average timeline for merger by absorption precedents. As HEC is only waiting for approval from independent H-shareholders suggests this transaction may complete earlier than precedents.

KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal. The Offer price assumes no full-year dividend is paid.

On balance, MYOB’s board has made the right decision to accept KKR’s reduced Offer. The argument that MYOB is a “known turnaround story” is challenged as cloud-based accounting software providers Xero Ltd (XRO AU)and Intuit Inc (INTU US) grab market share. This is also reflected in MYOB’s forecast 7% revenue growth in FY18 and follows a 10% decline in first-half profit, despite a 61% jump in online subscribers.

And there is justification for KKR’s lowering the Offer price: the ASX is down 10% since KKR’s initial tilt, the ASX technology index is off by ~14%, a basket of listed Aussie peers are down 17%, while Xero, the most comparable peer, is down ~20%. The Scheme Offer is at a ~27% premium to the estimated adjusted (for the ASX index) downside price of $2.68/share.

Bain was okay selling at $3.15/share to KKR and will be fine selling its remaining ~6.5% stake at $3.40. Presumably, MYOB sounded out the other major shareholders such as Fidelity, Yarra Funds Management, Vanguard etc as to their read on the revised $3.40 offer, before agreeing to the SIA with KKR.

If the markets avoid further declines, this deal will probably get up. If the markets rebound, the outcome is less assured. This Tuesday marks the beginning of a new year and a renewed mandate for investors to take risk, especially an agreed deal; but the current 5.3% annualised spread is tight.

The Ministry of Finance, the major shareholder of TMB, confirmed that both Krung Thai Bank Pub (KTB TB)and Thanachart Capital (TCAP TB)had engaged in merger talks with TMB. Considering an earlier KTB/TMB courtship failed, it is more likely, but by no means guaranteed, that the deal with Thanachart will happen. Bloomberg is also reporting that Thanachart and TMB want to do a deal before the next elections, which is less than two months away.

TMB is much bigger than Thanachart and therefore it may boil down to whether TMB wants to be the target or acquirer. In Athaporn Arayasantiparb, CFA‘s view, a deal with Thanachart would leave TMB as the acquirer rather than the target. But Thanachart’s management has a better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than Bank Of Ayudhya (BAY TB) and would not change the bank rankings; but it would give TMB a bigger presence in asset management, hire-purchase finance and a re-entry into the securities business.

Mando accounts for 45% of Halla’s NAV, which is currently trading at a 50% discount. Sanghyun Park believes the recent narrowing in the discount may be due to the hype attached to Mando-Hella Elec, which he believes is overdone; and recommends a short Holdco and long Mando. Using Sanghyun’s figures, I see the discount to NAV at 51%, 2STD above the 12-month average of ~47%.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

The accounting fraud issue had hammered the Celltrion duo nearly equally up until Dec 26. But last two days were different. Healthcare got hurt much more deeply. Celltrion fell only 2.41%, but Healthcare fell 11.52%.

The accounting issue is supposed to be equal to both. KOSPI move and merger are still alive to push up Healthcare. Local institutions and foreigners have bashed both pretty much equally in the last two days. This is another sign that it was more of a price divergence than a mean reversion.

The duo is now at 20D MA and also the yearly mean. I expect it to go substantially below the yearly mean on KOSPI move and merger expectations. A powerful downwardly mean adjusting force still seems to be in action. I’d long Healthcare and short Celltrion to exploit the latest price divergence.

Halla Holdings is falling nearly 5% today. Holdco said it’d give a ₩2,000 div per share. This is about 4.5% div yield at yesterday’s closing price. 5% drop today shouldn’t be much as an ex-dividend date price drop. Mando fell 5%. Mando was oversold relative to the other local auto stocks, particularly to Halla Holdings. They are still close to +1 σ on a 20D MA.

Mando-Hella Elec has been another reason behind Holdco’s valuation divergence against Mando lately. I believe Mando-Hella is being overhyped. Mando-Hella-caused divergence should no longer be effective. I expect ‘downwardly’ mean reversion from now on. I’d go short Holdco and long Mando at this point.

The Offer price of $4.56/share, an 82.4% premium to last close, has been declared final. The price corresponds to the subscription of 329mn domestic shares (~47.16% of the existing issued domestic shares and ~24.02% of the existing total issued shares) @$4.56/share by HEC in January this year.

Of greater significance, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors can justify recommending an Offer to shareholders at any price which gave cash less cavalier than cash.

Dissension rights are available, however, what constitutes a “fair price” under those rights, and the timing of the settlement under such rights, are not evident.

As all PRC approvals have been obtained, this transaction may complete earlier than prior mergers by absorption, which have taken 6-8 months from the initial announcement.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

On 24 December, MYOB Group Ltd (MYO AU) announced that it entered into a scheme implementation agreement under which KKR will acquire MYOB at $3.40 per share, which is 10% lower than 2 November offer price of A$3.77. MYOB claims its decision to recommend KKR’s lower offer was based on current market uncertainty, long-term nature of its strategic growth plans and the go-shop provisions of the deal.

We believe that KKR’s revised offer is opportunistic, but MYOB’s shareholders are caught between a rock and a hard place. Shareholders can take a short-term view and grudgingly accept the revised offer. Alternatively, shareholders can take a long-term view by rejecting the offer and hope MYOB’s strategic growth plans and a market recovery can reverse the inevitable share price collapse.

New Pride Corp (900100 KS) announced a ₩36.2bil rights offer. This is a public offering, so there won’t be subscription rights to trade. Pricing will be done as 3-day VWAP on Jan 9~11 at a 30% discount.

Supposedly, we can have ample opportunity to arb trade. This may be what the company is hoping. Simply, we wait until Jan 16~17 (subscription period) and see the spread. At this much discount, there must be a huge spread opening.

Proration risk can be much more annoying than a usual stockholder offering. In the previous public offering event by New Pride, subscription rate went as high as 370 to 1. It should be way much lower this time. But still this is risky enough.

LG Chem Ltd (051910 KS) 1P is now at a 44.20% discount to Common. Div would be the same as last year of ₩6,000 despite lower earnings. Payout would be 28%. Div yield for Common will be 1.68%, and 3.03% for 1P. Div yield difference stands at 1.35%p. This is a record high at least since 2014.

1P’s discount to Common is hovering at the highest level in 2 years. On a 20D MA, it is close to +1 σ. It may not be tempting enough for those seeking high yields. Otherwise, this’d be worth giving it a shot. Liquidity shouldn’t be an issue. Short recovering risk on Common also appears to be limited.

Daelim Industrial (000210 KS) is one of the main targets of local activist movement. This makes a setting for higher dividends. Common div yield to 1.58% and Pref to 4.18%. Difference is 2.59%p. This is the widest gap in many years.

Pref is currently at a 60.89% discount to Common. Among those > ₩100bil MC prefs, it is the second highest discounted pref, only behind CJ Cheiljedang 1P (097955 KS). Local street expects at least ₩1,600 div per share. This should be a conservative estimate. On a 20D MA, Pref is above +1 σ.

Dec 26 is record date of dividend payout. I expect a price catchup movement tomorrow in favor of Pref. I’d go long Pref and short Common as early in the morning as possible.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainlanders in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: those with a market capitalization of above USD 5 billion, those with a market capitalization between USD 1 billion and USD 5 billion, and those with a market capitalization between USD 500 million and USD 1 billion.

Thanks to improved Korea-China relation, Opco (004320 KS) shares have nicely rebounded lately. Nongshim Holdco hasn’t caught up. This created the highest price ratio gap in 2 years. On a 20D MA, they are close to the mean. But on a 2 year mean, Holdco is currently and still severely undervalued.

Liquidity has played a major role in the recent price gap widening. At a rebounding cycle like this, liquidity must have been a huge factor. But it shouldn’t be too long until Holdco catches up. Opco has kinda drifted sideways for a while now. This should be time for Holdco to begin a catchup.

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of fully-diluted shares (current shares out + 26.826mm Options + ~2.1mm Award shares).

The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The other terms and conditions of this deal will be set out in the offer document which is expected to be despatched in mid-January 2019 (14-21 days from 28 December).

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.10 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

Healthscope Ltd (HSO AU), Australia’s second-largest private hospital operator, is caught again in a bidding war between Brookfield Asset Management (BAM US) and BGH-AustralianSuper. On 21 December 2018, Healthscope extended exclusive due diligence with Brookfield. Brookfield noted that it has “no reason to believe it would not be willing and able to proceed” with its proposal.

The popular narrative is that should a binding proposal materialise; shareholders can expect a bidding war among the existing bidders, and potential new bidders as Healthscope is “in play”. While there is there is a possibility for some ‘‘sweetening’’ to the bid price, we think that that the formal “winning” bid is unlikely to be materially above the current Brookfield bid.

As the merger between TMB and Thanachart gets a nudge from the Ministry of Finance and could be finalized this month, we try to answer a few questions in this review:

Takeover premium. Based on our estimates, the potential improvements in ROE from the merger and potential divestment of MBK, we think it justifies an Bt11.1/sh premium for Thanachart. The new best case price target for Thanachart stands at Bt64.25/sh, implying a 29% premium over current share price.

Negotiations will play a key role in the actual takeover price. We provide a table of how much money is left on the table for TMB if they acquire TCAP at lower than what we expect.

Benefits. Thanachart has a higher ROE than TMB and appears smaller but better managed. The merger would allow TMB to re-enter the securities business (more cross-selling), enlarge its asset management franchise, and scale up deposit base for both banks…more so on the Thanachart side.

Size. Even after the merger, the combined bank would still have a much smaller headcount than BAY, smallest of the five largest Thai banks. However, it would have more branches than BAY and just 11% less branches than KBANK.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

One of the reasons why the Nexon’s founder Kim Jung-Joo, who is only 50 years old, is trying to sell his entire stake in Nexon may have been due to the recent allegations about him giving about $380,000 worth of Nexon stock (prior to its listing) to his old high school classmate (who is now a senior public prosecutor) for free. Kim Jung-Joo has repeatedly faced allegations and attended numerous court hearings on this matter in the past two years. He may have gotten a bit tired from all these allegations.

Given the enormous size of this acquisition, the two leading Korean game companies including NCsoft Corp (036570 KS) and Netmarble Games (251270 KS) are not likely to purchase Nexon. Rather, the leading contender to buy Nexon right now is likely to be Tencent Holdings (700 HK). The sheer huge size of this deal will represent one of the largest M&A deals in Asia in 2019.

The average NAV discount of a basket of 40 Holdcos steadily, and not altogether unsurprisingly, widened throughout the year.

Passive, tech-related and illiquid Holdcos widened most; while cross-border and property Holdcos were the best of the worst.

Illiquid, property, and passive Holdcos’ underperformance (or widening) was more pronounced in the first half. Tech Holdcos primarily widened in the second half.

Below the various NAV discount chart summaries of various baskets are my weekly setup/unwind tables.

This, and other relationships discussed below, trade with: 1) a minimum liquidity threshold of US$1mn on a 90-day moving average; and 2) a minimum 20% ‘market capitalisation’ threshold, whereby the value of the holding/Opco held must be at least 20% of the parent’s market cap.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainlanders in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: those with a market capitalization of above USD 5 billion, those with a market capitalization between USD 1 billion and USD 5 billion, and those with a market capitalization between USD 500 million and USD 1 billion.

Thanks to improved Korea-China relation, Opco (004320 KS) shares have nicely rebounded lately. Nongshim Holdco hasn’t caught up. This created the highest price ratio gap in 2 years. On a 20D MA, they are close to the mean. But on a 2 year mean, Holdco is currently and still severely undervalued.

Liquidity has played a major role in the recent price gap widening. At a rebounding cycle like this, liquidity must have been a huge factor. But it shouldn’t be too long until Holdco catches up. Opco has kinda drifted sideways for a while now. This should be time for Holdco to begin a catchup.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.