Haidilao International, the largest Chinese cuisine player by valuation, was listed on September 26th last year and lock-up expiry will be on March 26th. The stock has returned 24% since listing.

As it heads into lock-up expiry, we will examine Haidilao’s shareholder structure and potential shares up for sale.

Haidilao was included in the Hong Kong Connect Scheme on December 10th, 2018 and shares held by mainland investors have been consistently increasing.

But we think Haidilao’s valuation has built in a perfect growth scenario.

Risk of de-rating for Haidilao warrants a short position.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In this report, we provide an analysis of our pair trade idea between Hyosung Corporation (004800 KS) (market cap of 1,612 billion won) and Hyosung TNC Co Ltd (298020 KS) (market cap of 712 billion won). Our strategy will be to be long Hyosung TNC and be short Hyosung Corp.

In the past six months, Hyosung Corp is up 62% while Hyosung TNC is down 12%. We believe this price divergence has been excessive. The four major reasons why Hyosung Corp’s share price has surged in the past six months are mentioned below. There is a case to be made that the market has already factored into Hyosung Corp’s share price many of the positive factors mentioned below.

Excellent dividends

Corporate activism related stock

Strong financial results

Timing of the increased insider ownerships/Completion of tender offers

Hyosung TNC has underperformed the market as well as Hyosung Corp in the past six months. However, Hyosung TNC appears to be a turnaround story driven by the following factors:

Lippo Malls Indonesia Retail Trust (LMRT SP) (“LMIRT”) today announced the acquisition of Lippo Mall Puri from its sponsor PT Lippo Karawaci Tbk for a consideration of Rp.3,700.0 bil (S$354.7 mil).

There is a significant amount of vendor support provided by Lippo Group to improve the net property income and NPI yield of Lippo Mall Puri. If we exclude the vendor support from the target NPI, the NPI yield excluding vendor support will just be 6.52% per annum.

The transaction is DPU and yield dilutive. The resultant DPU post-transaction will decline from 2.05 S-cents to 1.61 S-cents / 1.42 S-cents. Distribution yield will also fall from 10.25% to 9.28% / 8.85% based on TERP.

The transaction could also potentially result in LMIRT’s gearing increasing from 34.6% to 39.0% which will worsen its balance sheet strength and credit standings.

In view of the unattractive acquisition and potential EFR dilution, investors should avoid LMIRT for now and wait for opportunity to enter with a greater margin of safety.

NIO’s 6-month Lock-up expires today and as of the time of this writing the stock is down by 6.6% from the closing price on Friday, March 8. The stock’s share overhang issue have been well covered on the Smartkarma platform by other analysts (see NIO Post-CBS Rally Making TSLA Valuation a Grand Bargain (Price Target =$3) , NIO (NIO US): Lock-Up Expiry – This Could Get Messy) so while we do not see a need to rehash those details in this insight, here are 3 things that we believe every NIO investor and would-be investor should keep in mind about the company especially if one wants to play the Tesla vs. NIO scenario:

Licensing/Regulatory Risk – NIO has an autonomous driving testing license but no EV manufacturing license. An EV manufacturing license issued by the NDRC is required for EV manufacturers to market and sell their products but a 100k unit scale is a main prerequisite. This is a key reason why NIO entered into a 5-year outsourcing relationship with JAC. While this relationship was assumed to be temporary, there could be many hurdles for NIO to actually obtain a license in the coming years should it decide to invest in production facilities again.

Core IP Held by Suppliers – Powertrain technology is held by CATL and the State-owned JAC is listed as the ES8’s manufacturer on the Ministry of Information and Technology website. Continental AG designs NIO’s vehicle suspension and chassis. It is also unclear how much actual development work other than exterior/cockpit design is done in-house at NIO based on publicly available information. Without scale and IP we believe NIO’s bargaining position with its suppliers is weak and displays stronger characteristics of a distributor than a final assembler.

Low ASP, low margins – NIO’s ASP on the ES8 from what we have seen was $64k per unit in 2018 and $63k per unit in 1Q19 while Tesla’s Model X ASP is about $100k per unit. There is a reason why gross margin at NIO is razor thin and it has more to do with low price point than low volumes in our view.

Given differences between the U.S. and China operating environment for EV makers, we believe Tesla is not a good equity valuation comp for NIO, which is basically a distributor in our view. As such, long term value drivers would most likely come from aftermarket and service revenues, while short-mid term value drivers seem elusive especially in the aftermath of the company’s decision to scrap its production plant investment plans in Shanghai.

Shin Ramyun non-frying noodle dramatically reversed Sub’s fortune. Local street starts believing Sub will hit a ₩100bil OP milestone this year. Local institutions began to scoop up Sub shares since a week ago. Yesterday, local pension/foreign money came in. This led to the largest Sub pushing in many weeks. Holdco/Sub are not at near -2σ.

Street consensus on Sub’s FY19e OP is already upwardly adjusted to ₩106bil. On this, Sub is already at a 17x earnings. ₩106bil OP is immaturely aggressive. 17x isn’t particularly cheap given Sub’s FY18 year-end PER (18.4x).

Valuation wise, Sub price should be pressed down at this level until more dramatic and tangible sales data come out. Holdco discount is still hovering at 50% to NAV. I’d make a stub trade here. Holdco liquidity can be an issue.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this insight, we will highlight PICC and Xinyi Solar.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Haidilao International, the largest Chinese cuisine player by valuation, was listed on September 26th last year and lock-up expiry will be on March 26th. The stock has returned 24% since listing.

As it heads into lock-up expiry, we will examine Haidilao’s shareholder structure and potential shares up for sale.

Haidilao was included in the Hong Kong Connect Scheme on December 10th, 2018 and shares held by mainland investors have been consistently increasing.

But we think Haidilao’s valuation has built in a perfect growth scenario.

Risk of de-rating for Haidilao warrants a short position.

Tesla Motors (TSLA US) has changed its mind, again, and now reportedly is putting on hold plans to close hundreds of its mostly newly opened stores and lay off thousands more employees–at least until the end of the month.

Employees, customers, suppliers, and investors still are reeling over Tesla’s startling decision, announced February 28th, to move immediately to online-only sales, a dramatic reversal of strategy still in place as of the 2018 10-K filing on February 19th in which the company had touted growth via recent store expansions and substantial additions planned globally going forward.

Tesla explained that even with now three substantial price cuts on all its cars and now three significant layoffs since last summer, it must slash costs even more to support the launch of its long overdue $35,000 base version of the flagship Model 3 (see my report Tesla’s New Plan: Buy Before You Try).

I warned clients that Tesla’s stunning strategy reversal seemed driven more by alarming cash consumption plus much weaker than expected sales and profit margins already apparent in what is shaping up to be a disastrous first quarter–troubling trends that may continue. However, as I noted, it also costs money to close stores, get out of leases (good luck with that), fire employees and redistribute remaining staff, and sell off fairly new equipment at steep losses.

Tesla probably hasn’t seen the light–it’s just received as of March 1st a desperately needed cash infusion by finally securing overdue funding for Tesla Shanghai Gigafactory 3 which has been under construction since January (see Tesla – Shanghai Surprise). Unfortunately, the four banks in Tesla’s new “China Loan Agreement,” which the company announced on Thursday with a rare 8-K filing, committed only to fund a one-year limited purpose loan for up to 3.5 billion yuan ($521 million). This is barely enough time or cash to get the Shanghai assembly plant up and running–much less also stave off the current cash crunch.

But Tesla must keep up appearances as well as bolster its liquidity through at least the end of the quarter as it gets ready to reveal Thursday evening the long-awaited Model Y–though I suspect this won’t result in a massive burst of cash from new reservations as Tesla hopes.

Years of robbing Peter to pay Paul hasn’t produced a sustainable growth model for Tesla, mostly because its business strategy still is better described as, “Wow, we didn’t see that coming.”

Continue reading for Bond Angle analysis.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

An attractively valued company with a minimum market cap of USD $1 billion but no sell-side coverage.Doubledragon Properties (DD PM) meets those criteria.

Why Read This Report?

Learn about the Philippines youngest self-made billionaire*, Edgar ‘Injap’ Sia, how he created one of the largest fast-food chains (Mang Inasal) in the country and successfully sold it to Jollibee Foods (JFC PM) for over USD$100 M.

After selling Mang Inasal in 2010, Sia started building DoubleDragon (DD) as he joined hands with Tony Tan (founder of Jollibee Foods (JFC PM) ). DD was listed in 2014 at a market value of USD$85 M (PHP2/share) and reached a market cap of over USD$3 B USD two years after listing (PHP70/share).

DD’s valuation mid-2016 was overhyped and overvalued.

From mid-2016 to late 2018 the share price fell by approximately 75%. Last year the stock bottomed at PHP17.2 despite fundamentals improving drastically between 2016 and 2018.

This has created a unique opportunity to invest in a diversified property company whose main earnings contributor will come from building neighborhood malls in suburban communities outside Metro Manila. It is forecast that 90% of its revenues would be recurring in nature by FY20.

We value DD on a blended a) P/E multiple and b) Cap Rate basis.

DD recently traded around PHP 22/share and is currently valued at 9.5x FY20 P/E, a steep discount to its industry peers. Assuming the company achieves PHP10.8 B in recurring revenues by FY20 the market is currently valuing the company at a 21% Cap Rate vs 7% for its primary peer Sm Prime Holdings (SMPH PM). DD should trade at a discount to SM (long track record, higher liquidity, included in PSE index) but the gap is too wide.

We argue DD should trade at a) 15x P/E and b) 10% cap rate. Combining the two valuation methods we arrive at a blended Fair Value of PHP 40.31/share, or 83% upside from current levels.

Assumptions

Fair Value

15x 2020 P/E

PHP 35

10% Cap Rate

PHP 45.63

BLENDED FAIR VALUE

40.31 PHP

The founders control 70% of the company and expect to grow the current USD$1.2B market cap exponentially the coming 3-5 years. DoubleDragon is a potential multi-bagger in the making.

Catalysts to unlock value at DoubleDragon would be:

FY18 results publication by early April 2019

Delivery of 100 operating CityMalls by FY20

The passing of workable REIT law

Delivery of PHP5.5B FY20 profit target

FCF inflection point coming closer in FY20

Re-discovery by sell-side firms as index inclusion looms

Visibility into FY21-FY25 dividend potential

Footnote: *Injap was reported as having USD$1 B in assets by Forbes in 2017, as the share price of DD has fallen we estimate this has dropped to approximately USD$ 400-500 M, which would still rank him among the top-25 wealthiest individuals in the Philippines.

We believe this presents an excellent opportunity to look at the stock on the short side again.

We would also refer readers to an article from Livedoor news which delves into the company’s issues from a local industry insider’s perspective. The article is in Japanese and the google translated version is almost unintelligible but we summarise the salient points and our perspective below.

Our recent conversation with CyberAgent’s IR team suggests that a significant improvement in the OP margin is unlikely in the next few quarters. The OP margins of both Game business and the Internet Advertisement, while likely to improve gradually, are likely to remain low compared to recent history due to higher advertising and personnel costs.

Upfront investments in AbemaTV are likely to continue until the target of 10m Weekly Average Users (WAU) is met, which could take a year or more. The company expects around 50% of AbemaTV revenue to eventually come from premium users, which seems to be a shift in strategy, from a “free” service towards a more hybrid model.

CyberAgent’s share price closed at ¥4,050 on Tuesday, up 7.1% from its previous close, following the news that the stock was added to the Goldman Sachs’ conviction list with a reiterated buy rating. However, even before this, CyberAgent’s share price had been on a steady increase over the past two weeks (+29.0%), recovering from a one-year low in early February. This increase, despite rather mediocre 1Q results, a downward revision of OP guidance, and lack of any major short term catalysts is an indication that the market deems CyberAgent to be undervalued – mainly on the AbemaTV front.

DAF is a fast growing auto finance company which acquires customers through a network of dealership around China. Its net interest income grew by 66% CAGR from FY2016 to FY2018 while net fees/comms income and profit grew by 39.6% and 61% CAGR over the same period.

However, most of its growth originated from ZhengTong dealers and joint promotion arrangement. Excluding loans from joint promotion arrangement, gross outstanding loan had only grown by 12% CAGR.

In this insight, we will look at the company’s business, analyze the competitive landscape, provide thoughts on valuation, and some questions for management.

In this insight, I’ll run the deal through our framework and comment on valuations.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The eagerly awaited and long promised Model Y is out and it looks…like Model 3. That’s OK, just no shock and awe which Tesla really needed to jumpstart sales momentum–and a wave of sorely needed cash reservations.

Tesla Motors (TSLA US) unveiled Model Y on, perhaps not coincidentally, March 14th which also is Pi Day. Pi is the fundamental ratio which demonstrates that all circles are related–as Model Y is overwhelmingly related with the seminal Model 3 which contributes 75-80% of the newcomer’s platform and technology.

Which means Model Y may be originating with Model 3’s many inherent problems, as I discussed in Tesla’s Plan B 2.0; Y Not, just as Tesla also is juggling the ramp-up of the newly launched $35,000-base model of Model 3 along with sales expansion into Europe and China as well as building a new plant on a shoestring in Shanghai. All this just as the company also has lurched into a radical new online-only sales model with apparently little if any considered preparation (see Tesla’s New Plan: Buy Before You Try).

Another is that Model Y won’t be available until late 2020–at best–which is much later than expected. It’s still not clear when or where Model Y will be in full production or, even more critical, when Tesla will make even a penny of profit on it. Model 3 only recently became marginally profitable, excluding the likely money-losing $35k version, and sales of more profitable but aging Models S and X are in accelerating decline.

And, as I observed last week, Tesla’s track record of long delays in delivering new models coupled with Model 3’s alarming quality and reliability may seriously diminish the hoped-for early bird reservation cash which the company sorely needs to ease its liquidity crunch. At the same time, the pending arrival of Model Y over the next year or so is likely to further dampen already waning demand for Model 3.

In any case, it’s too late for Tesla to preserve profitability in the calamitous first quarter, if not for the full year.

In this series under Smartkarma Originals, CrossASEAN insight providers AngusMackintosh and Jessica Irene seek to determine whether or not we are close to the end of the rainbow and to a period of outperformance for the property sector. Our end conclusions will be based on a series of company visits to the major listed property companies in Indonesia, conversations with local banks, property agents, and other relevant channel checks.

The fourth company that we explore is township developer Alam Sutera Realty (ASRI IJ), which provides an interesting exposure to a mix of landed housing, high-rise and low-rise condominiums through its Alam Sutera Township near Serpong and its Pasir Kemis township 15 km further out on the toll road.

Given the diminishing area of high-value land bank in Alam Sutera, the company has shifted emphasis towards selling low-rise condominiums and commercial lots for shop houses, which has been a success story.

Alam Sutera Realty (ASRI IJ) also has a contract with a Chinese developer, China Fortune Land Development (CFLD), to develop a total of 500 ha over a five year period in its Pasir Kamis Township. This has provided a fillip for the company during a quiet period of marketing sales and will continue to underpin earnings for the next 2 years.

The company stands to benefit from the completion of two new toll-roads, one soon to be completed to the south connecting directly to BSD City and longer term a new toll to Soekarno Hatta Airport to the north.

It will start to utilise new land bank in North Serpong in 2021, which will extend the development potential in the area significantly longer-term.

Management is optimistic about marketing sales for 2019 and expects growth of +16% versus last year’s number, which already exceeded expectations.

Alam Sutera Realty (ASRI IJ) has less recurrent income than peers at around 10% of total revenue but has the potential to see better contributions from the Garuda Wisnu Kencana Cultural Centre (GWK) in Bali.

The new regulations on the booking of sales financed by mortgages introduced in August 2018 will benefit Alam Sutera Realty (ASRI IJ) from a cash flow perspective. Given that the company is consistently producing free cash flow, this is also a strong deleveraging story.

One of the biggest risks for the company is its US$ debt, which totals US$480m and is made up of two bonds expiring in 2020 and 2022.

From a valuation perspective, Alam Sutera Realty (ASRI IJ) looks very interesting, trading on 4.9x FY19E PER, at 0.67x PBV, and at a 71% discount to NAV. On all three measures, at 1 STD below its historical mean. Our target price of IDR600 takes a blended approach, based on the company trading at historical mean on all three measures implies upside of 91% from current levels. Catalysts include better marketing sales from its low-rise developments at its Alam Sutera township and further cluster sales there, a pick-up in sales and pricing at its Pasir Kemis township, a sale of its office inventory at The Tower, a pick up in recurrent income driven by improving tenant mix at GWK. Given that the company has high levels of US$ debt, a stable currency will also benefit the company. A more dovish outlook on interest rates will also be a positive, given a large and rising portion of buyers use a mortgage to buy its properties.

In this insight, we will look at the updates on financials and operating metrics, compare it to other listed online education companies, and run the deal through our framework.

The increase in spending on marketing has not yielded the intended results as the growth rates of student enrollment and gross billings slowing down. Furthermore, aggressive spending behavior is similar to that of STG and LAIX and both companies did not perform well post listing.

We recently met with Yahoo Japan (4689 JP) for an update on the company after Q3 results. We thought the financial announcement was positive with encouraging forecasts for profitability, both this year and going forward, and revenue growth potential. In addition, Yahoo Japan reported solid customer growth for mobile payments joint venture PayPay, driven by strong marketing support and an attractive proposition for offline merchants. We think the latter is very important for the development of mobile payments in Japan and PayPay has had a robust start.

We cut our target price by 22% to Bt24.7 to factor in disappointing 2018 result. However, we maintain our BUY rating on the back of positive outlook toward its new products and market expansion plan.

The story:

Posted net profit of Bt50m in 4Q18, down 36%YoY and 25%QoQ

Trimmed 2019-21E forecast by 23.8%-24.3% respectively

Expanding strategic partnership

Our new target price of Bt24.7 is based on a target PE’19E of 18.8x which is equivalent to the World’s consumer staples sector.

Risks: (1) Fluctuations in raw material prices

(2) Exchange rate fluctuations

(3) Highly competitive industry

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The discount and variety retailer just opened its fourth store in South-East Asia, mixing Japanese restaurants and cafes with a Donki store and a range of Japanese speciality tenants. The store has all the high-level retail entertainment that its Japanese stores offer but with the added cachet of being from Japan and mixing in a lot more in-mall tenants and food outlets. PPI now plans 200 overseas stores in the medium-term.

Back home, PPI is creating new small store formats which have the potential to reach into parts of Japan its big box stores cannot.

At the same time, PPI is beginning the conversion of 100 Uny stores to mixed food and variety stores. With the first six conversions showing sales growth of 83% over 10 months and gross margins up 59%, PPI’s expectation of an extra ¥20 billion in operating profit once conversions are complete looks very achievable.

The takeover means PPI is now Japan’s fourth-biggest retailer, up from 15th just three years ago.

These multiple ventures reflect the company’s flexibility, adapting to each local market’s needs with formats to match.

Its recent decision to close down its e-commerce business is not a weakness but a positive move, demonstrating that PPI understands where its strengths lie: in live store entertainment.

With our Post Card Series, our aim is to bring on-ground realities & perspectives from cities across India. In this insight, we share our takeaways from our visit to Surat, the diamond hub of India. Our focus is Titan Co Ltd (TTAN IN) and the impact on margins.

Studded jewellery has more margins than plain gold jewellery. Part of Titan’s plan is to improve the mix in favour of studded jewellery which could help it command even higher margins. Titan anticipates this mix to improve to 50% by FY2023. Our interactions indicate a limited possibility of this change in mix. Operating leverage may be the only driver that can help in margin expansion.

We revise our FY20 EBIT margin & EPS estimates. Our FY20 EBIT margin is revised from 12.63% to 11.6% for FY20, continues to be higher than consensus which is at 10.82%. While we see limited margin expansion possibility, revenue growth likely to surprise. We introduce our FY21 EPS estimate at INR 28.75 compared to consensus EPS which is at INR 25.50.

Trust is a factor which cannot be easily replicated or acquired. The trust that Titan enjoys argues for a higher PE multiple. Based on a two-year average forward multiple 51x, our target price for Titan is INR 1466 which represents an upside of 37% from the last close price of INR 1070

An old favorite in the Asian arbitrageur’s investment universe is the Hang Lung stub. The Hang Lung Group acquired Hang Lung Properties (formerly named Amoy Properties) and designated the subsidiary as its property investment arm. After both companies were listed in 1992, the same year that the company entered the mainland with its purchase of the Grand Gateway 66 and Plaza 66 in Shanghai, the pair was open to arbs. The Hang Lung Group now controls over RMB 130 (USD 19.4b) billion of property in Hong Kong and China.

In the wonderful world of Asian holding companies, Hang Lung needs little introduction. However, in this insight I would like to highlight a trade idea. I will detail why I think now is the right time to setup a stub trade and some background information on the company and what assets constitute the stub.

We visited one big-cap stock, Berli Jucker, and one pip-squeak recent IPO M Vision today. A couple of highlights:

Slow revenue growth at BJC at under 5% largely driven by Big C (hypermarket), but earnings growth was strong at 28% mainly due to lower cost of palm oil in the snack business.

Good progress in Vietnam with expansion of the bottle capacity this year and SABECO increasing purchases of bottles.

Overall unimpressed. The company isn’t expecting to grow revenues more than 9% this year, and many of the cost cuts we saw in 2018 are clearly one-offs. Higher oil prices are likely to lead to rising palm oil prices this year too, since the two commodities are linked through substitution effect.

MVP underwent a bad year on the profit level, but their various businesses, at least on the top line level, looks like it could recover quickly this year.

Best World International (BEST SP) share price has been hammered due to the recent article in Business Times, although the company has addressed them one by one. The annual meeting that recently took place in their office in Singapore shed some light on the seemingly “new but not so new” franchise business model in China. The company also has started to engage Key Opinion Leaders (KOL) aka social media influencers as part of their social selling campaign.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Sutl Enterprise (SUTL SP) did not grow revenues in 2018 as it continued to operate only its flagship Sentosa marina. Change is coming as it has 9 projects in the pipeline which could dramatically alter the financial future of the company by FY21.

The biggest news is the groundbreaking of Puteri Harbor in Malaysia last week. With a sales gallery opening by May 2019, it will be very interesting to follow the progress on this project and its contribution to SUTL’s top/bottom-line results in FY19/FY20.

SUTL is misunderstood by investors because management disclosure is lacking and liquidity is poor. The valuation of SUTL could be improved if investors had a better understanding of the earnings trajectory we could expect in FY19-FY21.

We realize the Tay family is not looking to sell its stake anytime soon so is not concerned about its current market cap. We caution that this might not be a smart way to run a publicly listed company as a more expensive ‘currency’ (stock price) might help the company be taken more seriously when attempting to make acquisitions overseas.

However, this does not alter the fact that 84% of the market cap is cash and the EV of this consistently profitable company is barely 6.7M USD. SUTL is undeniably one of the cheapest stocks on SGX.

ZTO Express (ZTO US)‘s earnings will fail to meet the high expectations of sell-side analysts and investors who seeit as a cheap proxy for Chinese e-commerce activity.

China’s express sector revenue grew 43.5% YoY in 2016, the year ZTO went public. Last year, revenue growth was just half that (21.8%), and we expect the sector’s growth to continue to moderate over the next few years.

The express sector is also evolving in ways that will put downward pressure on profitability and require greater investment from the express companies.

We expect the profitability of ZTO’s express business to decline in the medium-term as the company adjusts to slowing demand and emerging sector trends. Our earnings estimates, which are far below consensus figures, reflect these challenges.

ZTO suffers from declining earnings quality and two accounting issues that we feel make it a risky, unattractive investment. Our 12-month target price for ZTO is US$13.31, based on 16 times our blended 2019-20 EPS estimates. We rate the stock Sell.

BGF Holdco/Sub have been oscillating within ±1σ since early Feb. Last Friday, Sub again made a move. This time it diverted a little further. They are now close to -2σ. Holdco is now at a 46% discount to NAV.

Overall sector outlook is still unpromising. Local street sentiments are still divided. BGF Retail is showing interest in Korea’s third internet bank. This may become a price divergence factor. But this issue is still too early to have real impact.

Shorting is still going pretty heavy on Sub. Sub price divergence shouldn’t last any further from this point. I’d make my trade here.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Starting with bad news in Korea, Homeplus REIT (HREIT KS)‘s IPO was pulled on the 14th of March which when it was supposed to price. The reason cited was weak demand which stemmed from growth concerns and difficulty in valuing this business.

On the other hand, Hong Kong’s IPO market is getting busier. This week alone, we had Dongzheng Automotive Finance (2718 HK) and Koolearn (1797 HK) that have already opened for bookbuilding and will price next week. We also heard that Sun Car Insurance is already started pre-marketing and it will likely open its books next week. The company had only just re-filed their draft prospectus last week.

In India, the focus is on Embassy Office Parks REIT (EOP IN) as this is the country’s first ever REIT IPO. It is also the first time there is a strategic tranche in an Indian IPO which has been taken up by Capital Group. Sumeet Singh has pointed out in his insight that with cost of debt of the REIT being at 9 – 9.25%, it is hard to fathom buying equity at a FY2020E dividend yield of 8.25%. This yield had already been inflated by the lack of interest payments. For detailed explanation, read his insight, Embassy Office Parks REIT IPO – FY19 Revised Down, Yield Propped up by Zero Coupon Bond.

In other countries, we heard that Leong Hup International (LEHUP MK) is aiming to pre-market next month whereas, in Australia, there had been chatter that Prospa Advance Pty (PGL AU) may be back for an IPO again after it had beaten its own estimates from the IPO prospectus.

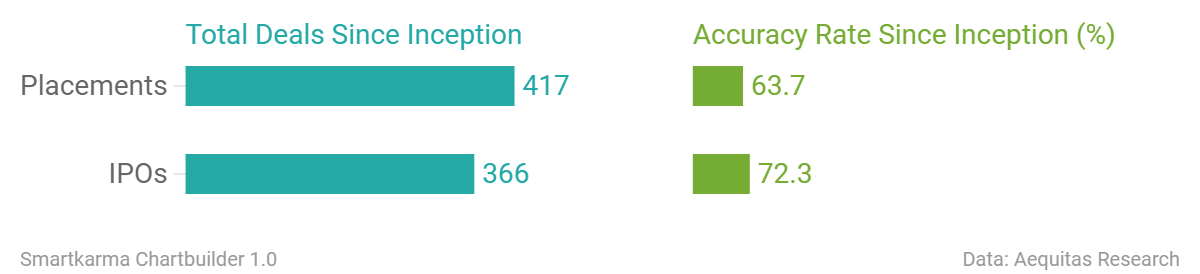

Accuracy Rate:

Our overall accuracy rate is 72.4% for IPOs and 63.7% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

FriendTimes Inc. (Hong Kong, >US$100m)

Frontage (Hong Kong, re-filed)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Three years ago, Isetan-Mitsukoshi attempted to reverse a strategy of shifting to small format retailing.

At the same time, the department store operator made a final ditch effort to avoid closing department stores and sacked its CEO who had had the temerity to suggest closure was the only way to revive the business.

Last year new management finally realised the old CEO had been right and that culling stores was the only way to improve profit growth.

Now the company is diversifying again but, instead of just small stores, it is planning a big investment into e-commerce with a projected ¥145 billion in sales from personal styling alone.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In my original insight on January 15, 2019 TRADE IDEA: Amorepacific (002790 KS) Stub: A Beautiful Opportunity, I proposed setting up a stub trade to profit from the mis-priced stub business of Amorepacific that was trading at its widest discount to NAV in at least three years. During the 65 calendar days that followed, Amorepacific Group (002790 KS) has gained 7.3% and the outperformed Amorepacific Corp (090430 KS) by 2.84%. The trade has reverted to average levels in a period of about two months and in this insight I will outline why I think the trade is over.

I should have seen this coming. The asset is juicy enough, and they have a large enough stake, and the company is small enough, that this is an easy trade to do if you can get the funding. It makes eminent sense to be able to put the money down and go for it.

I have covered this minor disaster of an MBO (Management BuyOut) of Kosaido Co Ltd (7868 JP) since it was launched, with the original question of what one could do (other than refuse). Famed/notorious Japanese activist Yoshiaki Murakami and his associated companies started buying in and then the stock quickly cleared the Bain Capital Japan vehicle’s bid price. The deal was extended, then the Bain bid was raised to ¥700/share last week with the minimum threshold set at 50.01% not 66.67% but still the shares had not traded that low, and did not following the news. But Bain played chicken with Murakami and the market in its amended filing, including the words 「公開買付者は、本開買付条件の変更後の本公開買付価格を最終的なものとし、今後、本公開買付価格を一切変更しないことの決定をしております。」which roughly translates to “The Offeror, having changed the terms, has made This Tender Offer Price final, and from this point onward, has decided to absolutely not raise the Tender Offer Price.”

So now Murakami-san has launched a Tender Offer of his own. Murakami-affiliated entities Minami Aoyama Fudosan KK and Reno KK have launched a Tender Offer at ¥750/share to buy a minimum of 9,100,900 shares and a maximum of all remaining shares. The entities currently own 3,355,900 shares (13.47%) between them – up from 11.71% reported up through yesterday [as noted in yesterday’s insight, it looked likely from the volume and trading patterns prior to yesterday’s Large Shareholder Report that they had continued buying].

Buying a minimum of 9,100,900 shares at ¥750/share should be easier for Murakami-san’s bidding entity than buying a minimum of 12,456,800 shares (Bain Capital’s minimum threshold) at ¥700/share, but the Murakami TOB Tender Agent is Mita Securities, which is a lesser-known agent and it is possible that the main agent for the Bain tender (SMBC Securities) could make life difficult for its account holders.

The likelihood that Murakami-san doesn’t have his bid funded or won’t follow through is, in my eyes, effectively zero. Tender Offer announcements are vetted by both the Kanto Local Finance Bureau and the Stock Exchange. You know this has been in the works for a couple of weeks simply because of that aspect. But one of the two documents released today includes an explanation of the process Murakami-san’s companies have gone through to arrive at this bid, and that tells you it may have gone on longer.

So what next? The easy answer is there is now a put at ¥750/share. Unless there is not. Weirder things have happened.

Read on…

For Recent Insights on the Kosaido Situation Published on Smartkarma…

The company is an internet key opinion leader (KOL) incubator in China. Revenue and GMV grew at impressive rates of 63% and 57% YoY in FY2018, respectively.

The idea of being able to leverage on KOLs influence over consumers to understand demand and retain consumers is interesting but Ruhnn has yet to demonstrate that it has a sustainable business model.

Gross margin has deteriorated and losses widened as a percentage of revenue. Service fee paid to KOLs as a percentage of revenue has increased and showed little improvement in 9M FY2019. The company depends heavily on the top KOL, Zhang Dayi, to generate revenue, almost half of the company’s GMV and revenue is generated from her.

In our first report on Prada S.P.A. (1913 HK): An expensive luxury, we explained how creative accounting was disguising their business reality. Since then, the stock has fallen 44% and the dividend has been cut. However, we think the key issues have yet to be addressed. They report growth, good operating cashflow and a solid financial position, but in-store sales are stagnant, margins falling, inventory rising and credit quality declining. It seems that profits are being inflated in order to pay dividends, largely to the controlling family.

Itochu planned on buying 7.21 million shares out of the 75.37mm shares which bear voting rights (as of the commencement of the Tender), and 15,115,148mm shares were tendered, which led to a pro-ration rate of 47.7% which was 0.3% below my the middle of my “wide range” expected pro-ration rate of 42-54% and 0.7% beyond the 44-47% tighter range discussed in Descente Descended and Itochu Angle Is More Hostile of 28 February.

Two more central ideas were discussed in that piece:

The hostility shown by Descente management during the Tender Offer had led Itochu to abandon discussions about post-tender management until after the Tender Offer was completed. Both sides indicated a willingness to pick up where things had left off – at Descente’s request – but Descente needed to stew a bit.

The revelation by ANTA Sports in an interview with the CEO in the Nikkei in late February that ANTA supported Itochu meant that the likelihood of Itochu NOT having enough votes to put through its own slate of directors was almost zero. At a combined 47.0% of post-Tender voting rights, if 94% or less of shares were to vote, it would mean Itochu could get the majority of over 50% and determine the entire slate of directors themselves. If there was another shareholder holding a couple of percent which supported Itochu, it would be a done deal even if everyone voted. And that 2-3% existed.

So… the threat that Itochu would hold an EGM to seat new directors to oblige a stronger course for management was a very strong probability. Management who was rabidly opposed to Itochu owning the stake could not very well bow down in front of Itochu post-tender just to save its own hide – not after the employee union and the OB group came out against. President Ishimoto had effectively put himself in an untenable position unless a miracle occurred because Itochu could not legally walk away from its offer, and Ishimoto-san was bad-mouthing Itochu even as they were negotiating during the Tender Offer Period.

It was not, therefore, any surprise that President Ishimoto would step down. The surprise for me was that the news he would go came out as talks commenced over the weekend (but did not “bridge the gap” as the Nikkei reported), before we got to the first business day post-results.

Talks apparently continue with no resolution, and the media reports offer no hint as to what the issues might be.

Recent Insights on the Descente/Wacoal and Itochu/Descente Situations on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

After 6 months of haggling and due diligence, debt negotiation, and structuring, global education company Navitas Ltd (NVT AU) has now signed a Board-recommended Scheme Implementation Deed with a consortium led by Australian Private Equity firm BGH Capital consortium which includes Navitas Founder Rod Jones (also the largest holder at 13%) and AustralianSuper.

The agreed Scheme Price of A$5.825 is a 6% uplift from the original A$5.50 offered in the preliminary, indicative, non-binding offer announced on 10 October 2018 and a 34% premium to the undisturbed price of 9 October 2018 of A$4.35/share.

This history is that the consortium came in at A$5.50 (plus another cash+RollCo scrip offer), a month or so later the company effectively rejected it by not allowing the consortium to do due diligence after management lifted earnings guidance. This upset a number of shareholders. In November the share price ranged from A$4.95-5.25 or so and Chairman Tracey Horton got only 51% support at the AGM that month. The shares fell briefly below A$4.70 in early January this year before BGH came back in mid-January with a “revised indicative offer” of A$5.825 whereupon the shares bounced from about A$4.90 to about A$5.50 then climbed to A$5.60+ on 10mm shares volume in 3 days.

The shares hovered around A$5.58-5.62 for 6-7 weeks until the beginning of March, briefly traded into the A$5.70s, and then traded back down the last few days this week to the A$5.59-5.63 area.

On Thursday 21 March the shares were halted for the day, StreetTalk had an article about the deal being imminent, and late in the afternoon, the BGH SID was announced.

Now we start the official process. The Scheme document is expected to be dispatched in May 2019 with a deal completed by end-June or early July. I expect this deal gets up.

Navitas Ltd (NVT AU), an Australian-listed education company, entered into a binding agreement to be acquired by the BGH Consortium. As a reminder on 15 January 2019, the BGH Consortium bid against itself by offering a revised proposal of A$5.825 cash per share, 6% higher than its previous rejected offer.

Navitas’ board have unanimously recommended the scheme. We believe that BGH Consortium’s proposal is attractive and shareholders should accept the offer.

The return on this pair trade was 8.2%. (Thisassumes no commission costs, pricing spreads, taxes, or borrowing cost) using closing share price as of March 12th to March 21st, 2019. This trade was made over a period of 9 days so the annualized returns would be 332%.

We believe that Hyosung TNC is up so much in the past 9 days mainly because it appears that a few investors saw this stock as an undervalued stock that was being ignored by the market. In our report, Korean Stubs Spotlight: A Pair Trade Between Hyosung Corp and Hyosung TNC, we mentioned that Hyosung TNC appears to be a turnaround story driven by the following four key factors:

INVESTMENT VIEW: The Australian Bureau of Meteorology raised its ENSO Outlook back to El Nino ALERT from WATCH, which is linked to regional droughts, lower yields and higher prices for agriculture across South East Asia. As such, we believe the recent correction in Crude Palm Oil (CPO) prices is over and recommend buying back into shares of key producers with leverage to higher CPO prices, like Golden Agri Resources (GGR SP) (GAR).

We initiate coverage of S with a BUY rating, based on a target price of Bt4.2 derived from a sum-of-the-parts (SOTP) methodology and implying 16.5xPE’19E, a 23% discount to the average of its peers in the Thai real estate sector.

The story:

Asset value to drive long-term sustainable growth

19 projects under development worth a combined Bt36bn to drive sales over the next three years

REITs will be a key catalyst to boost recurring income

Higher revenue contribution from hotel business

Risks:

Tightened credit approval

Raw material costs & F/X fluctuation

Sources: CGS Research, company data

Background: In 2014, Santi Bhirombhakdi** and his property arm, Singha Property Management, acquired a major stake in RASA, a listed property company on the SET, and changed its name to “Singha Estate Public Company Limited”, or “S”. This new major shareholder quickly unveiled plans to transform S into a holding company. During 2015-17, the company made several acquisitions including (1) a 51.56% stake in NVD, a low-rise property developer that operates under the “Nirvana” brand with a current market value of Bt2.7bn; (2) Suntowers, an office complex worth Bt4.5bn; and (3) a mixed-use commercial complex owned by the major holder’s family business worth over Bt6bn. It also set up a joint venture with a partner to invest in and operate 26 hotels in the UK worth Bt8.6bn.

Note: ** Owner of Boon Rawd Brewerey, Thailand’s oldest brewery and maker of Singha Beer

Revenue breakdown:

The residential property segment contributed 41% of S’s 2018 total revenue. This segment includes the development and sale of high-rise and-low rise projects such as single detached houses, townhomes, home offices, and condominiums.

The commercial property segment contributed 36% of total revenue. This business includes space for rent, common-service charges for utilities, security systems, and other service fees. The company owns two commercial property projects — The Lighthouse (a community mall) and Suntowers (an office complex).

S owns 37 hotels with a combined 4,271 rooms comprising (1) two hotels with 297 rooms in Thailand, namely Santiburi Beach Resort & Spa and Phi Phi Island Village Beach Resort; (2) 22 hotels in England and 7 in Scotland (total of 3,115 rooms) under a 50:50 JV with FICO Group; and (3) 6 Outrigger-branded hotels with 859 rooms. This segment accounts for 18% of sales.

The company also provides construction materials such as precast concrete and aluminum, as well as hotel management services. These two segments contribute 3% and 2% respectively.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Since its announcement on 4Q2018 results and termination of Jiading plant construction, NIO’s share price has been halved. We believe the market has over-reacted on NIO’s cashflow risk. With the expected 30-50% reduction on NEV (New Energy Vehicle) subsidies, all the Start-ups would have worse-than-ever cashflow pressure in 2019. But NIO might survive.

In China’s NEV market, NIO’s market position remains unique among all the Chinese Start-ups. Tesla is still NIO’s main competitor. NIO’s ES6 has capability to compete with Tesla’s Model Y, based on our comparison. Tesla and NIO both have to rely on external funding. The other Chinese Start-ups have to compete with traditional OEMs who have much less cash flow pressures.

NIO’s 4Q2018 financial data were in good trend. We estimate its net loss in 2019 to be further narrowed to Rmb6.1bn. With estimated Rmb13.2bn cash balance at end-Feb 2019, NIO have enough money to cover its estimated cash outflow in the next two year. And it would be able to get another round of external funding in 2020/2021, as long as its business operation ramps up as expected.

We met up with management of two companies whose industries couldn’t have been more different. This is the quick run-down on what they are up to recently:

After You posted 14% earnings growth on the back of 20% revenue growth. While this remains healthy, it realizes that domestic market opportunities will become more limited and has started to look abroad with HK as its first market.

Locally, the desserts leader is still planning a slew of new products and some in exclusive partnerships with various airlines such as Air Asia and Thai Smile.

In an effort to reduce storefront expenses, they will start selling certain products outside stores and even online, now 3% of total sales.

Amata’s earnings crashed 28% in 2018 on the back of 2% revenue decline, as Vietnam retroactively forbid certain land sales and even fines the company for past transactions that abided with the law back then!

Subscription rate is 797 to 1. Offer price was fixed at ₩48,000, substantially higher than the upper end. Deal size is now ₩168.5bil. Company value is put at slightly higher than ₩1tril. Demands are spread out pretty well between long-term funds and hot money and local and foreign investors as well. All of the orders are universally placed at 75% of upper end or higher.

Local street is betting on Autoever/Glovis merger not long after this IPO. That is, HMG is still wanting the initial Glovis/Mobis merger plan. To better manage to win shareholder support, they must be thinking that bigger Glovis can be an answer. This means HMG should do whatever it takes to make Autoever bigger in the immediate future.

This is what local street is betting on and why they went really aggressive on this IPO. As witnessed in the bookbuilding results, this street mentalitywon’t be changed any time soon. We should expect even stronger prices after new shares are listed on Mar 28.

On March 11’th 2019, Nvidia announced the acquisition of market leading high-speed interconnect company Mellanox for $6.9 billion in an all-cash deal. At first blush, the benefits touted by both companies and accepted by most commentators make sense and the deal will be immediately accretive to both EPS and revenues upon closing according to NVIDIA.

However, the clear and present threat to NVIDIA’s future success has little to do with interconnect technologies. Rather, it is the competitive challenge to their GPU solutions for data center acceleration from a broad spectrum of alternatives from the likes of Alphabet, Baidu, Intel, Xilinx, Advanced Micro Devices etc, not to mention the host of custom-ASIC accelerator startups poised to launch their products this year. The acquisition of Mellanox will do nothing to address this situation and we see it as being a distraction from where the company really needs to be focusing.

It will serve one purpose though, as a BandAid to mask the otherwise inevitable decline in its data center revenue growth in the face of ever-increasing competition.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this insight, we will provide an analysis of the performance of selected stocks that just joined the Stock Connect last week.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.