PBoC responds to disappointing start to another year of slowing growth

Talks planned but US-China “clash of civilisations” deepens

Ever faster trains, new airports from Beijing to Antarctica – and more debt

Two-child policy fails to avert demographic crisis

Beijing nails first ever landing on moon’s far side

In my weekly digest China News That Matters, I will give you selected summaries, sourced from a variety of local Chinese-language and international news outlets, and highlight why I think the news is significant. These posts are meant to neither be bullish nor bearish, but help you separate the signal from the noise.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

It has been anything but a happy start to 2019 for the stock markets, which remained under pressure as trading resumed in the new year. A clutch of weak manufacturing data for December – from China to the eurozone and the US – soured the mood for investors through last week.

That was followed by a rare revenue warning from Apple Inc (AAPL US) , citing slowing sales in China, which drew fresh attention to the vulnerability of American companies from the bitter trade war between the world’s two largest economies. The only assets that seemed to be in favour were the safe havens such as Gold (GOLD COMDTY) and the Japanese yen.

Beijing provided the first major lift to market sentiment on Friday, by lowering the reserve requirement ratio for Chinese banks, in a bid to inject more cash into the system. US Fed Chairman Jerome Powell signalling a “patient” approach to monetary policy in a panel discussion in Atlanta later in the day and a strong US jobs report for December completed the trinity of factors that closed the week with a rally in stock markets as well as crude.

Brent and WTI closed nearly 2% higher on the day, just above $57 and just under $48 respectively. Sentiment in the oil market was boosted by initial surveys showing a surprisingly large drop in OPEC production in December.

OPEC/non-OPEC cuts of 1.2 million b/d took effect on January 1 and should yield results in the coming weeks, but we expect crude to remain largely beholden to the twists and turns in the global economy. Just as in the broader financial markets, so in the oil markets, all eyes will now turn to the high-level trade negotiations between the US and China, due to be held in Beijing over January 7-8.

Healius (HLS AU) (until last month known as Primary Health Care Limited), a leading owner of general practice clinics and pathology centres in Australia, announced an unsolicited and conditional proposal (including DD) from Jangho Group Co Ltd A (601886 CH) at A$3.25/share (~10x FY19 EV/EBITDA) in a A$2.0bn deal. Jangho currently holds a 15.9% stake in Healius and has been on the shareholder register for two years.

The Offer price translates to a 33.2% premium to the undisturbed price but below the 12-month high of A$4.09 in March 2018. Optically and when referenced to closest peer Sonic Healthcare (SHL AU), the offer price appears light.

Reflecting the long laundry list of conditions attached to this indicative offer, such as securing debt financing and various regulatory approvals in China and Australia, notably data security, this indicative deal is trading wide at a gross/annualized spread of 25%/47%, assuming a deal completion date in early August.

This proposal does, however, indicate Healius was probably oversold.

This morning, Healius’ board rejected the proposal as it was considered opportunistic and fundamentally undervalued the company.

We analyse the holdings of the world’s largest banks by the 255 global equity funds in our analysis. For each region (America/EMEA/Asia), we have selected the 6 largest banks by total assets, as defined by the S&P Global Market Intelligence Report, 2018.

We find that overall, holdings in these banks are on the decline, and in some cases, investor flight has been acute. Only 2 of the 18 banks are held overweight by global investors, with Citigroup Inc (C US) and Bnp Paribas (BNP FP) seeing the biggest exodus through 2018.

Chinese equities face a crossroad to start the year as the market mulls a more serious phase in the structural decline in China’s economy balanced against renewed efforts to stimulate growth in 2019. The US-China trade dispute and broader US policy shift to contain China’s economic ambitions in high tech industries have contributed to fears of a Chinese led global economic downturn. But these concerns may ease as China and the US progress through trade negotiations restarted amidst a truce on tariff policy through 1-March. The AUD and copper prices have been highly correlated with Chinese equities over the last year, highlighting the broader market implications of trade talks this week and renewed Chinese efforts to restore economic confidence.

A year ago we began publishing Tracking Traffic/Chinese Tourism as the hub for all of our research on China’s tourism sector. This monthly report features analysis of Chinese tourism data, notes from our conversations with industry participants, and links to recent company news and thematic pieces. Our aim is to highlight important trends in China’s tourism sector (and changes to those trends).

In this issue readers can find:

A review of China’s outbound tourist traffic in November, which strengthened: Lifted by extraordinarily strong growth in visits to Hong Kong and, to a lesser extent, Macau, Chinese outbound travel demand rebounded strongly in the seven regional destinations we track. But the fact that November’s growth was led overwhelmingly by Hong Kong and Macau — destinations close enough for weekend or day trips from population centers in Southern China — suggests Chinese tourists’ purse strings are still tight.

An analysis of November domestic Chinese travel activity, which turned weaker: November data from China’s three leading airlines and the Ministry of Transport show moderating domestic travel demand. For combined rail, highway, and air travel, November demand grew by less than 3% Y/Y. Along with the change in destination mix for outbound travel (that favors ‘nearby’ destinations), it now appears domestic demand has weakened, too.

Links to other recent news & research on Chinese tourism: Readers can check out our quick takes on Macau’s December GGR figure, preliminary GTV and revenue figures released by Ctrip.Com International (Adr) (CTRP US), declining US visa issuance to Chinese tourists, and Qatar Airways’ new investment in a leading Chinese airline.

Although we remain positive on the long-term growth of Chinese tourism, it’s clear that near-term demand has weakened substantially. We continue to take a negative view of travel intermediaries like Ctrip, which face intensifying competition from many sources. We are more positive on the prospects of actual owners of Chinese travel and tourism assets, like hotel chain Huazhu Group (HTHT US) and Air China Ltd (H) (753 HK).

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

China’s 2018 auto demand came to 27.8m units according to CAAM’s published statistics, bringing the YoY decline to 3.9%. The results were consistent with our expectations since 1H18, that:

We estimate that the acquisition tax reduction for 1.6L and smaller engine displacement vehicles in 2016 and 2017 front-loaded about 2.0-2.2m units to PC demand in those two years, similar to the impact of tax reduction effect seen in 2009-10. This is a segment that saw 1.1m units in volume reduction in 2018 which should be seen as a natural result of the end of the tax subsidies. In fact we believe that these after-effects of front-loaded demand were most likely more influential on China’s 2018 demand downturn than any headline narratives about negative impacts of trade wars.

Our initial expectations for 2019 are:

The 1.6L and smaller engine displacement segment should see stable to slightly lower annual demand, but there is nothing currently in the statistics that suggests that higher segments should also see declines. This should at least partly be a natural pattern of second and third time car buyers trading up.

As we have pointed out in May China Auto Demand: Weak SAAR Leaves Lingering Headwinds for 2H , CV SAAR was unusually strong in 1H18 so this could be an obvious segment of weakness going into 2019, especially if 4Q average CV SAAR of 3.7m units (vs. 4.2m unit FY18 demand) is any indicator of what to expect going forward.

While we expect some residual effects of the 1.6L and lower segment tax subsidy ending in 2017 to remain in effect in 2019 we do not expect its impact to be as large as it was in 2018. Our low single digit decline scenario considers a lower CV SAAR in YoY terms which appears likely as we head into 2019.

Weimob.com (2013 HK) IPO was priced at the low-end at HKD2.80/share. The retail tranche was 0.79x covered while the institutional tranche was slightly over-subscribed.

I’ve covered most aspects of the deal in my earlier insights:

In this insight, I’ll provide an update on the deal dynamics, valuations and provide a table with the implied valuations at different share price levels.

Since autumn of 2014, the HK-Shanghai Connect, and later the HK-Shenzhen Connect mechanisms have provided means for mainland investors to buy Hong Kong-listed stocks.

We have been tracking the H/A relationships and the Southbound flows per name on a weekly basis and occasionally writing commentary about it since late 2016.

This report provides a brief synopsis of the SOUTHBOUND flows into Hong Kong-listed stocks over the course of 2018, by sector, by average percentage change in mainland ownership of HK shares outstanding subject to the Connect mechanisms, and the top and bottom five names per sector per quarter.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Tim Cook passed the buck to the weak sales in China. However, we believe China’s retailing is running well based on our visits to shopping malls with Apple stores.

Luxury goods sold better in China than all other major markets in the world in 2018.

We believe that the price reduction in Mainland China is just taking market share from Apple Stores in Hong Kong, but not from competitors.

We also believe that the app review process is the fatal shortcoming for AAPL.

Overall, the company has continued to show that its undergraduate program is the driver behind its growth. It grew its 8M 2018 revenue and gross profit both by about 24% YoY. However, there are significant near-term risks if the MOJ Draft for Comments gets implemented. It may result in Kepei registering its schools as for-profit private schools which would shrink its net profit margin.

In this insight, we will provide updates on the company’s 8M 2018 financials and operating performance, the potential impact of policy change and compare its valuation to other listed education peers. We will also run the deal through our framework.

We noted in Ten Years On – Asia Outperforms Advanced Economies Asia’s economies and companies have outperformed advanced country peers in the ten years to 2017. Growing by 6.8%, real, through the crisis the region is 188% larger in US dollar terms while US dollar per capita incomes 170% higher compared with 2007. In this note we argue even though Asian stock markets have underperformed since 2010 and the bulk of global capital flows have gone to advanced countries, Asia’s time is coming. Valuations are cheap. Growth fundamentals strong. There are few external or internal imbalances. Macroeconomic management has been better than in advanced economies and the scope to ease policy to ward off headwinds in 2019 is greater. China has already started.

A nine-day winning streak until Thursday, January 10, had put Brent and WTI back in the bull market (gains of >20% from their 52-week lows). It was capped by a highly volatile trading day and a lower close of the benchmark crude futures on Friday, pointing to a return of uncertainty and indecisiveness in the market.

US-China trade talks over January 7-8, which were extended to January 9, set last week off to a flying start. There were no deals for sure, but the two sides appeared to have narrowed their differences. That was enough to send the stock markets climbing, with crude prices in tow.

Follow-up negotiations at a higher level are expected in the US later this month, though no dates have been announced yet. For now, it seems the financial markets, probably in gloom fatigue and perhaps oversold, needed any excuse to recover and a baby step towards the resolution of the US-China trade dispute was as good as any.

Of course, one can’t ignore the US Fed’s dovish turn, which also provided a major boost to sentiment. US Federal Reserve Chairman Jerome Powell said on Thursday that the central bank would be “patient” over future rate hikes. It was music to investors’ ears.

OPEC heavyweight Saudi Arabia repeated its promise to slash exports, with the energy minister providing specific figures for the benefit of the media and the market, and fundamentals had done their bit to help crude’s rally.

However, macroeconomic data and business outlook from companies across the world continues to be weak and disappointing. And crude remains firmly in the grip of the economic sentiment, maintaining a very strong correlation with the equity markets since last October.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: those with a market capitalization of above USD 5 billion, those with a market capitalization between USD 1 billion and USD 5 billion, and those with a market capitalization between USD 500 million and USD 1 billion.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We analyse the holdings of the world’s largest banks by the 255 global equity funds in our analysis. For each region (America/EMEA/Asia), we have selected the 6 largest banks by total assets, as defined by the S&P Global Market Intelligence Report, 2018.

We find that overall, holdings in these banks are on the decline, and in some cases, investor flight has been acute. Only 2 of the 18 banks are held overweight by global investors, with Citigroup Inc (C US) and Bnp Paribas (BNP FP) seeing the biggest exodus through 2018.

Chinese equities face a crossroad to start the year as the market mulls a more serious phase in the structural decline in China’s economy balanced against renewed efforts to stimulate growth in 2019. The US-China trade dispute and broader US policy shift to contain China’s economic ambitions in high tech industries have contributed to fears of a Chinese led global economic downturn. But these concerns may ease as China and the US progress through trade negotiations restarted amidst a truce on tariff policy through 1-March. The AUD and copper prices have been highly correlated with Chinese equities over the last year, highlighting the broader market implications of trade talks this week and renewed Chinese efforts to restore economic confidence.

A year ago we began publishing Tracking Traffic/Chinese Tourism as the hub for all of our research on China’s tourism sector. This monthly report features analysis of Chinese tourism data, notes from our conversations with industry participants, and links to recent company news and thematic pieces. Our aim is to highlight important trends in China’s tourism sector (and changes to those trends).

In this issue readers can find:

A review of China’s outbound tourist traffic in November, which strengthened: Lifted by extraordinarily strong growth in visits to Hong Kong and, to a lesser extent, Macau, Chinese outbound travel demand rebounded strongly in the seven regional destinations we track. But the fact that November’s growth was led overwhelmingly by Hong Kong and Macau — destinations close enough for weekend or day trips from population centers in Southern China — suggests Chinese tourists’ purse strings are still tight.

An analysis of November domestic Chinese travel activity, which turned weaker: November data from China’s three leading airlines and the Ministry of Transport show moderating domestic travel demand. For combined rail, highway, and air travel, November demand grew by less than 3% Y/Y. Along with the change in destination mix for outbound travel (that favors ‘nearby’ destinations), it now appears domestic demand has weakened, too.

Links to other recent news & research on Chinese tourism: Readers can check out our quick takes on Macau’s December GGR figure, preliminary GTV and revenue figures released by Ctrip.Com International (Adr) (CTRP US), declining US visa issuance to Chinese tourists, and Qatar Airways’ new investment in a leading Chinese airline.

Although we remain positive on the long-term growth of Chinese tourism, it’s clear that near-term demand has weakened substantially. We continue to take a negative view of travel intermediaries like Ctrip, which face intensifying competition from many sources. We are more positive on the prospects of actual owners of Chinese travel and tourism assets, like hotel chain Huazhu Group (HTHT US) and Air China Ltd (H) (753 HK).

PBoC responds to disappointing start to another year of slowing growth

Talks planned but US-China “clash of civilisations” deepens

Ever faster trains, new airports from Beijing to Antarctica – and more debt

Two-child policy fails to avert demographic crisis

Beijing nails first ever landing on moon’s far side

In my weekly digest China News That Matters, I will give you selected summaries, sourced from a variety of local Chinese-language and international news outlets, and highlight why I think the news is significant. These posts are meant to neither be bullish nor bearish, but help you separate the signal from the noise.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We expect Chinese domestic express demand to continue to moderate in 2019, and in response we expect the express companies to increase their investments in ‘last-mile’ and international delivery, which will probably create a drag on profitability in the medium-term. Although we believe e-commerce giants Alibaba and JD.com would like their growing portfolios of logistics investments to become self-funding sooner rather than later, we foresee somewhat limited investor appetite for more large Chinese logistics IPOs in 2019, since many high-profile offerings have faltered since going public.

Progress, yet trade war still morphing into tech war

Economic espionage: US targets Chinese spying

Tesla dreams big in China despite consumption fears

Bank funding beckons for SMEs

Yuan leaps as hopes fade for US rate hikes

In my weekly digest China News That Matters, I will give you selected summaries, sourced from a variety of local Chinese-language and international news outlets, and highlight why I think the news is significant. These posts are meant to neither be bullish nor bearish, but help you separate the signal from the noise.

The recent trade talk meeting between the US and Chinese government went into an extended unplanned third day which could be seen as a positive development – a sign that both sides are serious on getting a deal done. President Trump’s recent tweet citing “”Talks with China are going very well!” has been responded positively in Asian equities market. Is it all just that or are there more in the company?

Value made a comeback, but growth remains core: In May 2018, we examined the divide between value and growth stocks, ( Notes from the Silk Road: Small-Mid Cap Screening for Zulu Warriors). As Q3 unfolded, this eventuated with a +7.5% reversal in favour of value stocks, only to see growth resume dominance in October and November.

The optimal value/growth style dynamic: We feel exposure to growth at a reasonable price (GARP) coupled with a healthy FCF yield (via our amended Zulu Screen) should provide some healthy medium to long term returns for investors.

The Screen’s Risk: The Zulu Screen relies on analyst estimates. When market sentiment is weak and forecasts are not amended in a timely manner, the screen is susceptible to mis-selection.

Q2 2018 screening list succumbed to volatile markets: This was seen in our May screen with our list posting on average a 30% decline in share price, relative to the broader Asia-Pacific Ex-Japan declining 13.6% and the Asia Pacific index by 11.8%.

Are there reasons for the underperformance? 10 of the 19 stocks in the May screen were from Hong Kong, which saw the Hang Seng Index (HIS) decline 16% over the same period. The decrease seems due to concern over trade wars and doubts about the China economy. Our key approach to stock selection is to take a medium-to-long-term view as well as focus on quality ranked stocks relative to their peers. This is highlighted via the average stock rank of the group declining only 15.8% from 89.6 to 75.5 points.

Our Q1 2019 screen selected only 9 stocks. Of the 9 stocks identified, the average PEG Ratio was 0.4x, the price to FCF yield was 11% and ROCE was 25%. Stocks were selected from Australia, New Zealand, India, Korea, Japan, Hong Kong, Taiwan and Singapore. Cowell Fashion Company from Korea was the only remaining stock from our May screening.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Despite a shaky 2018 Q4 market and the disappointing Softbank Corp (9434 JP)‘s IPO, we have been getting a steady stream of newsflow on upcoming IPOs.

Starting with upcoming IPOs, Chengdu Expressway Company Limited (1785 HK) and Weimob.com (2013 HK) will be listing next week on Tuesday, 15th January. Weimob was priced at the low end of its price range while Chengdu Expressway’s IPO was at a fixed price of HK$2.20. We are bearish on both IPOs. Weimob is overly reliant on Tencent for its SaaS and Ads business and, at the same time, Tencent will only own less than 3% stake after listing. Whereas Chengdu Expressway has been a well-managed company but valuation implies limited upside. Trading liquidity will likely remain tepid as like Qilu Expressway Co Ltd (1576 HK) which listed mid last year.

In the pipeline, we are hearing that Kepei Education (KEPEI HK) will likely open its book next Monday. We will be following up with a note on valuation. In other IPOs that are coming in this quarter, Helenbergh China and Zhongliang, both property developers, are looking to IPO in this quarter. Viva Biotech Shanghai Ltd (1577881D HK) is also looking to list in Hong Kong Q2 while Urban Commons, a US property developer, is planning a US$500m REIT IPO in Singapore.

Activity seems healthy for the ECM space, but sentiment has not been the best as seen from Xiaomi’s high profile IPO that took a hit just as its lockup expired. Its share price has corrected from a high of HK$22.20 to just above HK$10.34 this Friday. This should not have been a big surprise since many have already pointed out that its valuation should really have been closer to that of a hardware business and we pointed out that the IPO’s trajectory would likely be similar to Razer.

This reminds us of a particular listing last year, Razer Inc (1337 HK) , and, in fact, both bear quite a handful of similarities. Strong portfolio of investors, hardware business with software capabilities, expensive valuations, and etc. The stock did well at first but has come back down to earth since then.

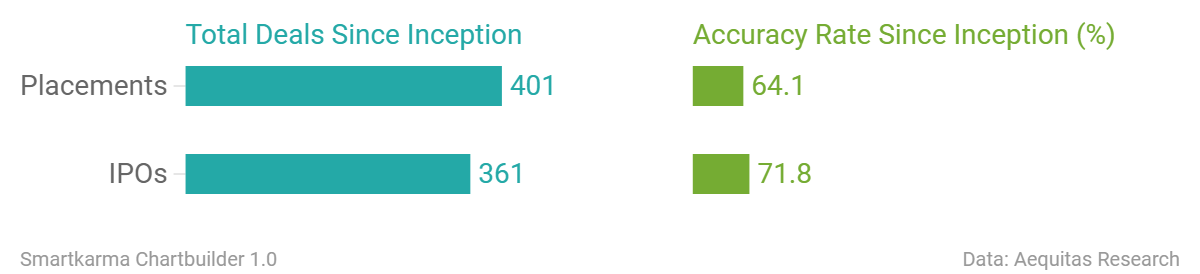

Accuracy Rate:

Our overall accuracy rate is 72% for IPOs and 64% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

China Tobacco International (Hong Kong, US$100m)

China East Education (Hong Kong, US$400m)

Ebang International (Hong Kong, re-filed)

MicuRx Pharma (Hong Kong, re-filed)

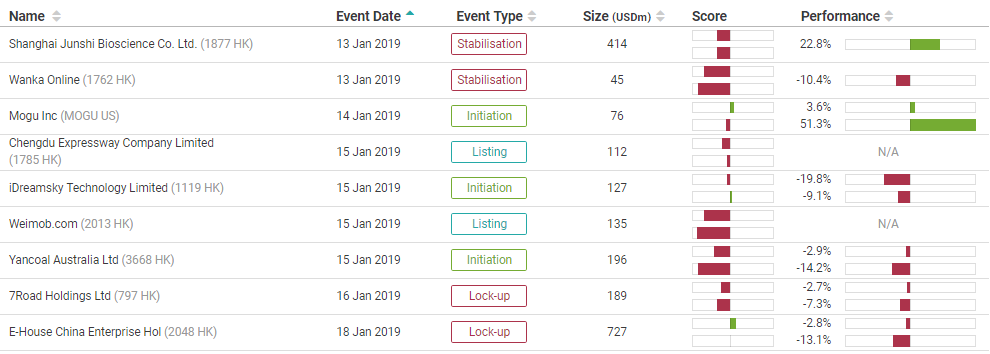

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

INVESTMENT VIEW: The same macro factors which knocked more than a third off Apple Inc (AAPL US)‘s share price have lifted Gold (GOLD COMDTY) prices by nearly 10% since Sept-18. However, we believe the market narrative could swiftly reverse if the US and China reach a trade agreement in the coming weeks. We would look to press our short on Gold…and even go long Apple.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Primary/secondary Uranium supplies currently 112% of 2017 demand

Uranium supply deficits extremely unlikely before 2022

Global Uranium demand to fall 25-40% by 2050

Primary Uranium sector LT SELL

We have independently audited global nuclear construction statistics in order to determine future Uranium demand. Although near-term statistics match those in the public domain, long-term demand determined via construction pipeline illustrates substantial discrepancies. Compiling planned plant construction, operational extensions, nameplate upgrades, versus decommissioning announcements/events, and in many cases, public policy inertia; has led us to believe that despite historical primary supply shortages, global nuclear demand peaked in 2006.

Since plateauing and despite strong Chinese growth, nuclear power generation has fallen <2% over the past two decades, a decline that is predicted to accelerate as a number of developed and developing nations pursue other energy options.

The macro-trend not replacing existing nuclear infrastructure means (dependent on assumptions), according to our calculations, global uranium demand will decrease between 20 to 40% by 2050.

As opposed to signifying a fundamental change in underlying demand, we believe that recent Uranium price increases are the result of producers closing primary operations, and substituting production with purchases on the spot market to meet long-term contract obligations. In addition, hedge funds are buying physical uranium in order to realise profits on potential future commodity price increases. Critically, we determine that primary and secondary supplies are more than sufficient to meet forecast demand over the next four to five years; before taking into account substantial existing global uranium stocks, some of which are able to re-enter the spot market at short notice.

China Xinhua Education (2779 HK) listed in Q1 of 2018 and we wrote in our insight that the founder had vocational schools that have been separated from China Xinhua that seemed to be his prized asset. Fast forward to December 2018, the prized asset has finally filed its draft prospectus under the entity China East Education (CEE HK) and it is looking to raise US$400m in its IPO.

In this insight, we will analyze the company’s financial and operating performance, compare it to listed education companies, and provide some questions we have for management.

According to a local media outlet called Chosun Daily, it stated that one of the bankers in the deal (Deutsche Bank), already sent teaser letters of this deal to Tencent Holdings (700 HK) and KKR and in the teaser letter, it mentioned about potentially selling nearly 47% of Nexon Co Ltd (3659 JP) (Japan).

The question about whether or not Kim Jung-Joo decides to sell NXC Corp (Korea) or Nexon Co Ltd (3659 JP) (Japan) has important consequences not just for him and his family but also to the minority shareholders of Nexon Co Ltd (3659 JP). If Kim Jung-Joo decides to sell NXC Corp (Korea), there may not be much upside for the minority shareholders of Nexon Co Ltd (3659 JP) since current regulations do not require the buyers to pay potentially additional control premium to the minority shareholders as well.

However, if Kim Jung-Joo decides to sell Nexon Co Ltd (3659 JP) (Japan), there may be an opportunity for the minority shareholders to gain from an additional control premium. We think that this is one of the reasons why Nexon Co Ltd (3659 JP) shares are up 13% YTD as some of the investors may think that there could be a higher probability that Kim Jung-Joo ends up selling Nexon Co Ltd (3659 JP) (Japan), instead of NXC Corp (Korea).

In our third report in the Belt and Road Initiative (BRI) or One Belt One Road (OBOR) series, we examine a brand-new US strategic initiative to finance emerging markets economies, including OBOR, African, and Latin American countries.

The on-going trade war between China and the US makes the issue very political. Rightfully so, we believe the creation of the International Development Finance Corporation (“IDFC”) could be politically-motivated, but IDFC is no competition to the BRI as the latter deploys much greater funding (about USD40bn a year).

However, we see the merits of IDFC and the positive effects on Emerging Asia. After all, more competition for influence and more fund flow will help fund projects, and, perhaps, help reduce poverty (if good governance is observed). We also expect IDFC’s USD60bn fund to create more investable projects for institutional investors and lower funding cost for countries that need large infrastructure funding and countries that have been suspicious of the BRI such as India, Indonesia, the Philippines, Vietnam, and Sri Lanka.

The founding team comes mostly from Tencent, which might explain Tencent’s large stake in the company. Growth for the company has been stupendous despite the jittery markets, with margin financing adding to the top-line growth.

While its low costs will help it to steal clients from the more traditional brokers, other new low-cost brokers seem to be offering similar services at comparable rates. In addition, the company is not licensed or regulated by any entities in China, despite the majority of its client base being Chinese nationals. Furthermore, the company plans to expand into newer overseas market where it doesn’t seem to have much of a cost advantage.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Despite a shaky 2018 Q4 market and the disappointing Softbank Corp (9434 JP)‘s IPO, we have been getting a steady stream of newsflow on upcoming IPOs.

Starting with upcoming IPOs, Chengdu Expressway Company Limited (1785 HK) and Weimob.com (2013 HK) will be listing next week on Tuesday, 15th January. Weimob was priced at the low end of its price range while Chengdu Expressway’s IPO was at a fixed price of HK$2.20. We are bearish on both IPOs. Weimob is overly reliant on Tencent for its SaaS and Ads business and, at the same time, Tencent will only own less than 3% stake after listing. Whereas Chengdu Expressway has been a well-managed company but valuation implies limited upside. Trading liquidity will likely remain tepid as like Qilu Expressway Co Ltd (1576 HK) which listed mid last year.

In the pipeline, we are hearing that Kepei Education (KEPEI HK) will likely open its book next Monday. We will be following up with a note on valuation. In other IPOs that are coming in this quarter, Helenbergh China and Zhongliang, both property developers, are looking to IPO in this quarter. Viva Biotech Shanghai Ltd (1577881D HK) is also looking to list in Hong Kong Q2 while Urban Commons, a US property developer, is planning a US$500m REIT IPO in Singapore.

Activity seems healthy for the ECM space, but sentiment has not been the best as seen from Xiaomi’s high profile IPO that took a hit just as its lockup expired. Its share price has corrected from a high of HK$22.20 to just above HK$10.34 this Friday. This should not have been a big surprise since many have already pointed out that its valuation should really have been closer to that of a hardware business and we pointed out that the IPO’s trajectory would likely be similar to Razer.

This reminds us of a particular listing last year, Razer Inc (1337 HK) , and, in fact, both bear quite a handful of similarities. Strong portfolio of investors, hardware business with software capabilities, expensive valuations, and etc. The stock did well at first but has come back down to earth since then.

Accuracy Rate:

Our overall accuracy rate is 72% for IPOs and 64% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

China Tobacco International (Hong Kong, US$100m)

China East Education (Hong Kong, US$400m)

Ebang International (Hong Kong, re-filed)

MicuRx Pharma (Hong Kong, re-filed)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

We highlighted in a recent note Chris Hoare‘s positive outlook for China Tower (788 HK). Our view takes into account the 5G build-out commencing this year, improved capex efficiency from using “social resources”, the rapid growth in non-tower businesses that lie outside the Master Services Agreement (MSA), and the valuation benefit from what looks like surprisingly investor friendly management.

This note focuses on four key issues facing the Chinese telcos in 2019:

5G capex (March) (this is by far the most important),

Regulatory newsflow (February/ March),

Operating trend improvements (August), and

Emerging business opportunities driving future growth (August).

We remain positive on the telcos which trade at low multiples. China Unicom (762 HK) continues to trade at a discount, yet is most exposed to the positive story emerging at China Tower. We switch our top pick among the telcos from China Mobile (941 HK) back to China Unicom as a result. Alastair Jones thinks China Telecom’s (728 HK) premium multiple is at risk if management execution on the cost base doesn’t improve. It is our least preferred telco at this stage. Overall, we expect China Tower to outperform all telcos and it is our top pick. The upgrade to China Tower flows through the telcos (valuation and costs) and our new target prices are as follows: China Unicom to HK$14.4, China Telecom to HK$5.4 and China Mobile to HK$96.

In the semiconductor industry, particularly in the DRAM sector, there has been significant consolidation leading some to hypothesize that there’s now an oligopoly that will cause prices to normalize and thus end the business’ notorious revenue cycles. Here we will take a critical look at this argument to explain its fallacy.

In their public presentations, central banks seem to be contemplating the use of neutral interest rates (r*) in addition to unemployment/inflation theories. R* has the advantage of appearing to be subject to mathematical precision, yet it’s unobservable, and so unfalsifiable. Thus, it permits central banks to present any policy conclusion they want without fear of verifiable contradiction. R* is the policy rate that would equate the future supply of and demand for loans. It rises and falls as an economy strengthens and weakens. Long-term observation during the non-inflationary gold standard, period indicated that r* in an average economy was 2% plus, which would become 4% plus with today’s 2% inflation target. The Fed may soon end this tightening cycle with the fed funds rate at or near 2¾%, which would be r* if the rate of lending and borrowing in America remained stable thereafter. Rising (falling) lending would indicate a higher (lower) r*.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

After initially being very skeptical of the China Tower (788 HK) IPO given it is essentially a price take to its three largest shareholders, we changed our view in early December to a more positive outlook. What changed our view has been series of calls and meetings with the company that suggested a more shareholder friendly approach than expected and a real opportunity to reduce capex substantially through the use of “social resources” (e.g. electricity grid, local government sites). These can be used to deliver co-locations without building towers and poles and imply much lower capital intensity at a time when revenue growth will be accelerating as 5G is rolled out. Management has also given more detail on non-Tower business prospects which can generate higher returns (not under the Master Services Agreement). While small now (2% of revenue) they are growing rapidly. With lower capex than initially guided and a more shareholder friendly management (i.e. higher dividends are possible) we reduce the SOE discount and raise our forecasts (again). We remain at BUY with a new target price of HK$2.20

The Education Ministry of China promulgated Burden Relief Measures for Students in Primary and Secondary Schools (中小学生减负措施).

The market is concerned about “Article 15” on the educator license.

We note that a large number of teachers in part-time schools took the educator exam in November 2018.

We expect that the incremental passers of the educator exam will be many more than the number of EDU’s vacancies, and that most of the passers will prefer to work for giants such as EDU or TAL (TAL) as opposed to other part-time schools.

It was reported on January 3rd that Korean founder and heretofore effective controller of Nexon Co Ltd (3659 JP) Mr. Kim Jung-Ju and family, who exercise their ownership of Nexon through near 100% (98.64% according to Douglas Kim) control of NXC Corp (Korea) and NXC’s control of NXMH B.V.B.A (Belgium), planned to sell their stakes in NXC for up to 10 trillion won (US$8.9 billion).

Those two companies – NXC Corp (Korea) and NXMH (Belgium) – own 253.6mm shares and 167.2mm shares respectively, or direct and indirect ownership by NXC of just under a 48% stake in Nexon (3659 JP). Yoo Junghyun (Kim Jung-Ju’s wife) directly holds another 5.12mm shares at last look.

Nexon was founded in Korea in 1994 and moved its headquarters from Seoul to Tokyo in 2005, listing itself on the TSE in December 2011. The company is a well-known gamemaker (over 80 PC and online/mobile games), with famous games such as MapleStory, Dungeon & Fighter, and Counter Strike.

The Korea Economic Daily said in its report on the 3rd of January that Deutsche Bank and Morgan Stanley had been selected as advisors to run a sale process, and a formal non-binding offer to potential bidders was expected next month. A Korea Herald article suggested that “potential buyers, according to industry speculation, include China’s Tencent, Korea’s Netmarble Games, China’s NetEase and Electronic Arts of the US.”

The Big Question

In the second piece, Douglas Kim questions whether Kim Jung-Ju would sell NXC (and NXMH) as reported by the local press, or whether NXC and NXMH would sell their stakes in Japan-listed Nexon, the implication being that if they sold the stake in Nexon, it would mean buyers would get a large stake in a single company, whereas there is a bunch of other stuff floating around in NXC and its subsidiaries.

The other question is whether Tencent or another buyer buying NXC would trigger a mandatory Tender Offer for the shares in Nexon in Japan. The letter of the law in the TOB Rules changed a bit over 10 years ago would indicate not, but there are questions (and precedents) here.

Out-performance in the US economy, as was seen in 2018, seems much less likely in the year ahead. Lower oil prices and slowing high tech sectors will dampen activity and assets in the US more than many other developed and EM countries. The boost to equities and growth from US tax policy has passed its peak. US politics is set to become increasingly partisan over the next two years of the Trump administration. US trade policy has softened in the wake on the sharp fall in US equities in Q4. Several EM countries have resolved their deep political distractions, and their economies have improved since mid-year. We can see the USD reversing more of its gains in the last year as the global economic outlook stabilises and the Fed enters an extended pause in rates policy.

The ability to have stable prices has great value.

According to Edward Gibbon, the decaying Roman Empire exhibited five hallmarks: 1) concern with displaying affluence instead of building wealth; 2) obsession with sex; 3) freakish and sensationalistic art; 4) widening disparity between the rich and the poor; and 5) increased demand to live off the state. Most DMs and many EMs display similar symptoms today because fiscal and monetary policies, the foundation of both ancient and modern societies, are identical: increasing welfare outlays by artificially inflating the money supply. The Roman Empire took more than four centuries to destroy what the Republic had built in the previous five centuries because clipping and debasing coins inflated currency supplies slowly. Entering debits and credits in the books of commercial and central banks is much more efficient.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.