GMO internet (9449 JP) released 2018 full-year results in 12th February. 2018 was a turbulent year for the company as it ‘surfed’ the cryptocurrency wave. The subsequent downfall was swift and brutal. However, the company deserves some plaudits for cutting its (substantial) losses and attempting to move on (albeit somewhat half-heartedly). Unfortunately, GMO-i has ‘form’ in writing off large losses as shown above. The positive consequence of this saga is a renewed commitment to return value to shareholders with a stated aim of returning 50% of profits. Two-third of that goal is to be met by quarterly dividends, with the balance allocated to share repurchases in the following year.

Having royally ‘screwed up’ with ‘cryptocurrencies’, and trying the patience of remaining shareholders yet again, this policy is to be commended, particularly if more attention is paid to generating the wherewithal to meet the 50% without raiding the listed subsidiaries’ ‘piggy bank’. Apart from the excitement that this move has generated and the year-long support this buying programme will provide to the share price, our two valuation models, find little in the way of further upside potential.

We remain sceptical of investing in GMO-i over the long-term and prefer GMO Payment Gateway (3769 JP) – the best business in the GMO-i ‘stable’ – but consider GMO-PG’s stock overvalued at 57x EV/OP.

Recruit Holdings (6098 JP) reported its 3Q FY03/19 financial results on Wednesday (13th February). Recruit’s revenue and EBITDA were up 6.0% YoY and 11.1% YoY respectively in 3Q FY03/19. This was mostly due to 1) consolidation of the results of Glassdoor Inc. (the company which operates the employment information website glassdoor.com), 2) steady growth in Japanese staffing operations and 3) growth in beauty and real estate app users during the quarter, partially offset by slowdown in global recruitment activity.

Despite its strong 3Q results and steady topline and bottom line growth over the forecast period, at a FY2 EV/EBITDA multiple of 16.0x, Recruit doesn’t look particularly attractive to us. Recruit’s internet advertising business and employment business peers, Yahoo Japan (4689 JP) and Persol Holdings (2181 JP) are trading at FY2 EV/EBITDAs of 6.8x and 7.5x respectively.

Key Financials FY03/18-20E

FY03/18

FY03/19E

FY03/20E

Consolidated Revenue (JPYbn)

2,171

2,327

2,478

YoY Growth %

11.9%

7.2%

6.5%

Consolidated EBITDA (JPYbn)

258

288

312

EBITDA Margin %

11.9%

12.4%

12.6%

Source: Company Disclosures/LSR Estimates

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We met AIS (ADVANC TB) earlier this week at their Analyst Day in Bangkok. The recent results confirm our concerns over market growth slowing, with service revenue flat YoY. The guided 4-6% growth for 2019 may be difficult to achieve. On the mobile side, AIS is feeling competitive pressure from a resurgent DTAC (DTAC TB) and continuing gains from TRUE (TRUE TB) . While “hostilities” have eased recently (less aggressive price offers), we remain wary of the outlook for 2019. On the fixed side, AIS is making slow progress and we continue to think M&A is warranted.

There was a fair amount of discussion around 5G at the meeting, but this looks like a long term issue for AIS. Thailand has never been in the forefront on telecom technology upgrades in the past and there is plenty to do with 4G and fixed broadband still.

Chris Hoare remains cautious on AIS in the current slowing environment, and ahead of delayed elections. Earnings forecasts have edged lower recently and that is translating to lower dividends (a 70% payout ratio to be retained for now). We remain at Neutral with a target price of THB187.

Rakuten (4755 JP) has been under pressure recently from Amazon (AMZN US) and other competitors in its core online mall business and now seems to be giving more attention once again to the original Rakuten Ichiba, including a plan to cut shipping fees, although this also looks like a face-saving way to cut merchant commissions.

Rakuten is also investing in new logistics infrastructure to try and match the customer services levels of Amazon and ZOZO (3092 JP).

As part of this effort, Rakuten just announced a 9.9% stake in a logistics firm called Kantsu. The deal is part of Rakuten’s strategy to accelerate the move towards consolidated shipments of orders on Rakuten Ichiba – one of the key weaknesses of the Rakuten model compared to Amazon and Zozo.

Rakuten also just announced its year-end results this week: Domestic GMVs rose 11.2% to ¥3.4 trillion for the year ending December 2018. While GMVs rose and revenue increased by 9.2% to ¥426 billion, operating income on domestic e-commerce fell 17.7% to ¥61.3 billion partly due to higher logistics costs. For 4Q2018, operating income fell 27.3%.

United Arrows’ (7606 JP) decision to cancel its e-commerce services contract with ZOZO Inc (3092 JP) was not a surprise at all but could not have come at a worse time. While a move to direct operation of its online store was expected, United Arrows did not have to choose a moment when Zozo’s stock was collapsing. That it did shows how much cooler relations are between the two firms, a critical development given United Arrows was the principal reason for Zozo’s emergence as the leading fashion mall in the early 2000s.

United Arrows will still be selling through Zozotown and its president last week praised Zozotown’s capacity to bring new and younger customers to its brand. The bigger problem is that United Arrows relies less and less on sales from Zozotown each year and more from its own online store – direct e-commerce sales have increased from 20% of all e-commerce sales in FY2016 to 27% in 9M2018.

At Baycrews, another leading merchant on Zozotown, 50% of e-commerce sales are from its own online store, up 12 percentage points in two years.

A further problem is that other merchants are leaving. We reported before that Onward’s departure, while significant, is less of a threat than it might first appear given that Onward already garners 70-75% of sales from its own store so it did not cost much to leave Zozo.

However, another big retailer, Right On, also quit Zozo last month despite the fact that more than 50% of its online sales come from Zozo and it has intermittently been one of the top 20 merchants on Zozo. Right On has struggled in recent years, so leaving Zozo cannot have been an easy decision, suggesting just how seriously upset it was.

Other merchants are likely to view these departures with some concern. Six months ago, the idea of quitting Zozo was not even a remote thought in Japan’s fashion industry but it is now a lively subject of discussion. While most merchants will stay, the recent high profile departures will make a threat to leave look much more real, giving merchants more leverage to negotiate, particularly on Zozo’s take rates.

Whilst OUE C-REIT’s DPU yield and Price-to-NAV appears to be attractive vis-à-vis its peers, investors should take note of the implications of the S$375 mil Convertible Perpetual Preferred Units (“CPPU”) and its impact on OUE C-REIT’s DPU going forward.

Assuming that all S$375 mil CPPUs are converted, a total of 524.2 mil new OUE C-REIT will be issued to OUE Ltd, and the total unit base of OUE C-REIT will expand by 18% to 3,385.8 mil units.

For minority investors of OUE C-REIT, they face the risk of having their DPU yield diluted from a projected 7.1% (before conversion) to 6.2% after conversion.

A Rights Issue to fund CPPU Redemption will be more dilutive than the conversion scenario. Assuming a Rights Issue at 20% discount, DPU yield of OUE C-REIT will drop from a projected 7.1% (before conversion) to 5.8% after Rights Issue.

Minority investors are likely to be at the losing end of this CPPU issue and suffer from yield dilution. Investors should avoid OUE C-REIT for now as the uncertainty over the CPPU conversion remains.

For investors who are still keen to take a position in OUE C-REIT, a fair post-conversion diluted DPU yield would be 6.6%, translating to a recommended entry price of S$0.465 per unit.

UG Healthcare (UGHC SP) showed good topline growth (+15%) but very weak bottom-line performance (-73%) in the second quarter of FY19 (financial year ending June). Weak bottom-line results were caused by delays and cost overruns in opening its latest factory expansion.

While the latest results are a setback I remain a believer in the UG Healthcare story. The eventual goal of reaching 100M SGD in revenues and getting a 10% NPM remains unchanged by the end of FY2020. Should the target be achieved the company trades at 4x 2020 P/E. Competitors in Malaysia trade at mid-teens multiples (or higher) so UG should deserve a significant re-rating the coming two years. Fundamentally, nothing has changed to alter my bear case (0.24 SGD), base case (0.39 SGD) or blue-sky scenario (0.62 SGD) analysis. Liquidity remains an issue at less than 25K SGD/day.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Recruit Holdings (6098 JP) reported its 3Q FY03/19 financial results on Wednesday (13th February). Recruit’s revenue and EBITDA were up 6.0% YoY and 11.1% YoY respectively in 3Q FY03/19. This was mostly due to 1) consolidation of the results of Glassdoor Inc. (the company which operates the employment information website glassdoor.com), 2) steady growth in Japanese staffing operations and 3) growth in beauty and real estate app users during the quarter, partially offset by slowdown in global recruitment activity.

Despite its strong 3Q results and steady topline and bottom line growth over the forecast period, at a FY2 EV/EBITDA multiple of 16.0x, Recruit doesn’t look particularly attractive to us. Recruit’s internet advertising business and employment business peers, Yahoo Japan (4689 JP) and Persol Holdings (2181 JP) are trading at FY2 EV/EBITDAs of 6.8x and 7.5x respectively.

Key Financials FY03/18-20E

FY03/18

FY03/19E

FY03/20E

Consolidated Revenue (JPYbn)

2,171

2,327

2,478

YoY Growth %

11.9%

7.2%

6.5%

Consolidated EBITDA (JPYbn)

258

288

312

EBITDA Margin %

11.9%

12.4%

12.6%

Source: Company Disclosures/LSR Estimates

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Recruit Holdings (6098 JP) reported its 3Q FY03/19 financial results on Wednesday (13th February). Recruit’s revenue and EBITDA were up 6.0% YoY and 11.1% YoY respectively in 3Q FY03/19. This was mostly due to 1) consolidation of the results of Glassdoor Inc. (the company which operates the employment information website glassdoor.com), 2) steady growth in Japanese staffing operations and 3) growth in beauty and real estate app users during the quarter, partially offset by slowdown in global recruitment activity.

Despite its strong 3Q results and steady topline and bottom line growth over the forecast period, at a FY2 EV/EBITDA multiple of 16.0x, Recruit doesn’t look particularly attractive to us. Recruit’s internet advertising business and employment business peers, Yahoo Japan (4689 JP) and Persol Holdings (2181 JP) are trading at FY2 EV/EBITDAs of 6.8x and 7.5x respectively.

Facebook Inc A (FB US) is a bellwether stock for the equity markets. Although the market capitalisation is approaching $475 billion, the Company is still considered a growth stock. In our view, 2019 could be a pivotal year for the Company after a lack lustre 2018, when FB, although volatile, underperformed the NASDAQ. We believe that investors are underestimating revenue growth for 2019 and that FB is likely to surprise to the upside in Q1-19.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Rakuten (4755 JP) has been under pressure recently from Amazon (AMZN US) and other competitors in its core online mall business and now seems to be giving more attention once again to the original Rakuten Ichiba, including a plan to cut shipping fees, although this also looks like a face-saving way to cut merchant commissions.

Rakuten is also investing in new logistics infrastructure to try and match the customer services levels of Amazon and ZOZO (3092 JP).

As part of this effort, Rakuten just announced a 9.9% stake in a logistics firm called Kantsu. The deal is part of Rakuten’s strategy to accelerate the move towards consolidated shipments of orders on Rakuten Ichiba – one of the key weaknesses of the Rakuten model compared to Amazon and Zozo.

Rakuten also just announced its year-end results this week: Domestic GMVs rose 11.2% to ¥3.4 trillion for the year ending December 2018. While GMVs rose and revenue increased by 9.2% to ¥426 billion, operating income on domestic e-commerce fell 17.7% to ¥61.3 billion partly due to higher logistics costs. For 4Q2018, operating income fell 27.3%.

United Arrows’ (7606 JP) decision to cancel its e-commerce services contract with ZOZO Inc (3092 JP) was not a surprise at all but could not have come at a worse time. While a move to direct operation of its online store was expected, United Arrows did not have to choose a moment when Zozo’s stock was collapsing. That it did shows how much cooler relations are between the two firms, a critical development given United Arrows was the principal reason for Zozo’s emergence as the leading fashion mall in the early 2000s.

United Arrows will still be selling through Zozotown and its president last week praised Zozotown’s capacity to bring new and younger customers to its brand. The bigger problem is that United Arrows relies less and less on sales from Zozotown each year and more from its own online store – direct e-commerce sales have increased from 20% of all e-commerce sales in FY2016 to 27% in 9M2018.

At Baycrews, another leading merchant on Zozotown, 50% of e-commerce sales are from its own online store, up 12 percentage points in two years.

A further problem is that other merchants are leaving. We reported before that Onward’s departure, while significant, is less of a threat than it might first appear given that Onward already garners 70-75% of sales from its own store so it did not cost much to leave Zozo.

However, another big retailer, Right On, also quit Zozo last month despite the fact that more than 50% of its online sales come from Zozo and it has intermittently been one of the top 20 merchants on Zozo. Right On has struggled in recent years, so leaving Zozo cannot have been an easy decision, suggesting just how seriously upset it was.

Other merchants are likely to view these departures with some concern. Six months ago, the idea of quitting Zozo was not even a remote thought in Japan’s fashion industry but it is now a lively subject of discussion. While most merchants will stay, the recent high profile departures will make a threat to leave look much more real, giving merchants more leverage to negotiate, particularly on Zozo’s take rates.

Whilst OUE C-REIT’s DPU yield and Price-to-NAV appears to be attractive vis-à-vis its peers, investors should take note of the implications of the S$375 mil Convertible Perpetual Preferred Units (“CPPU”) and its impact on OUE C-REIT’s DPU going forward.

Assuming that all S$375 mil CPPUs are converted, a total of 524.2 mil new OUE C-REIT will be issued to OUE Ltd, and the total unit base of OUE C-REIT will expand by 18% to 3,385.8 mil units.

For minority investors of OUE C-REIT, they face the risk of having their DPU yield diluted from a projected 7.1% (before conversion) to 6.2% after conversion.

A Rights Issue to fund CPPU Redemption will be more dilutive than the conversion scenario. Assuming a Rights Issue at 20% discount, DPU yield of OUE C-REIT will drop from a projected 7.1% (before conversion) to 5.8% after Rights Issue.

Minority investors are likely to be at the losing end of this CPPU issue and suffer from yield dilution. Investors should avoid OUE C-REIT for now as the uncertainty over the CPPU conversion remains.

For investors who are still keen to take a position in OUE C-REIT, a fair post-conversion diluted DPU yield would be 6.6%, translating to a recommended entry price of S$0.465 per unit.

UG Healthcare (UGHC SP) showed good topline growth (+15%) but very weak bottom-line performance (-73%) in the second quarter of FY19 (financial year ending June). Weak bottom-line results were caused by delays and cost overruns in opening its latest factory expansion.

While the latest results are a setback I remain a believer in the UG Healthcare story. The eventual goal of reaching 100M SGD in revenues and getting a 10% NPM remains unchanged by the end of FY2020. Should the target be achieved the company trades at 4x 2020 P/E. Competitors in Malaysia trade at mid-teens multiples (or higher) so UG should deserve a significant re-rating the coming two years. Fundamentally, nothing has changed to alter my bear case (0.24 SGD), base case (0.39 SGD) or blue-sky scenario (0.62 SGD) analysis. Liquidity remains an issue at less than 25K SGD/day.

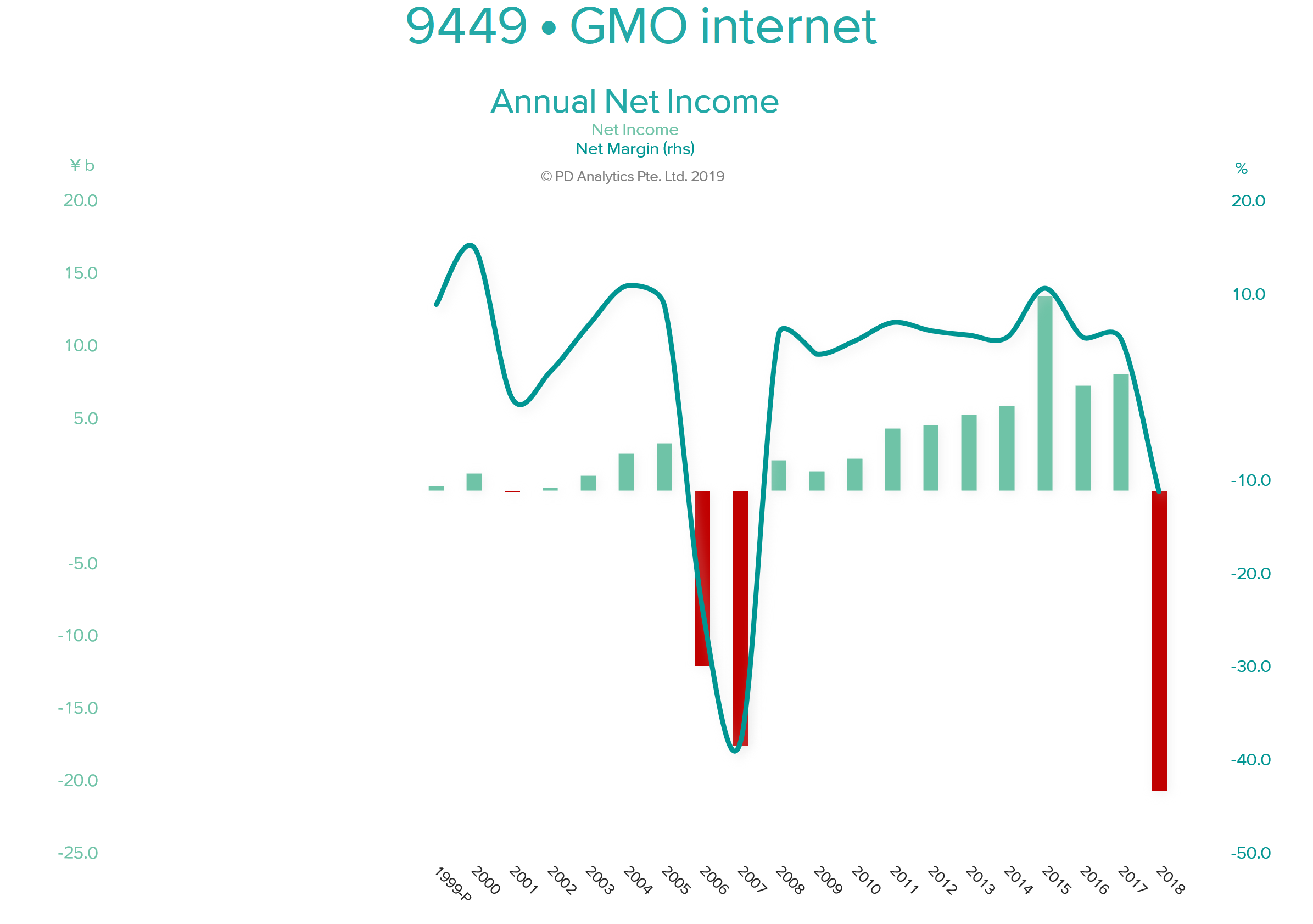

GMO internet (9449 JP) released 2018 full-year results in 12th February. 2018 was a turbulent year for the company as it ‘surfed’ the cryptocurrency wave. The subsequent downfall was swift and brutal. However, the company deserves some plaudits for cutting its (substantial) losses and attempting to move on (albeit somewhat half-heartedly). Unfortunately, GMO-i has ‘form’ in writing off large losses as shown above. The positive consequence of this saga is a renewed commitment to return value to shareholders with a stated aim of returning 50% of profits. Two-third of that goal is to be met by quarterly dividends, with the balance allocated to share repurchases in the following year.

Having royally ‘screwed up’ with ‘cryptocurrencies’, and trying the patience of remaining shareholders yet again, this policy is to be commended, particularly if more attention is paid to generating the wherewithal to meet the 50% without raiding the listed subsidiaries’ ‘piggy bank’. Apart from the excitement that this move has generated and the year-long support this buying programme will provide to the share price, our two valuation models, find little in the way of further upside potential.

We remain sceptical of investing in GMO-i over the long-term and prefer GMO Payment Gateway (3769 JP) – the best business in the GMO-i ‘stable’ – but consider GMO-PG’s stock overvalued at 57x EV/OP.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Recruit Holdings (6098 JP) reported its 3Q FY03/19 financial results on Wednesday (13th February). Recruit’s revenue and EBITDA were up 6.0% YoY and 11.1% YoY respectively in 3Q FY03/19. This was mostly due to 1) consolidation of the results of Glassdoor Inc. (the company which operates the employment information website glassdoor.com), 2) steady growth in Japanese staffing operations and 3) growth in beauty and real estate app users during the quarter, partially offset by slowdown in global recruitment activity.

Despite its strong 3Q results and steady topline and bottom line growth over the forecast period, at a FY2 EV/EBITDA multiple of 16.0x, Recruit doesn’t look particularly attractive to us. Recruit’s internet advertising business and employment business peers, Yahoo Japan (4689 JP) and Persol Holdings (2181 JP) are trading at FY2 EV/EBITDAs of 6.8x and 7.5x respectively.

Facebook Inc A (FB US) is a bellwether stock for the equity markets. Although the market capitalisation is approaching $475 billion, the Company is still considered a growth stock. In our view, 2019 could be a pivotal year for the Company after a lack lustre 2018, when FB, although volatile, underperformed the NASDAQ. We believe that investors are underestimating revenue growth for 2019 and that FB is likely to surprise to the upside in Q1-19.

GMO Internet, Inc. (9449 JP) announced its consolidated financial results for its full-year FY12/18 yesterday (12th February). Despite heavy losses incurred in the cryptocurrency mining business in FY12/18, GMO managed to achieve a solid year with 20% YoY growth in top-line alongside a 23.5% YoY growth in operating profits. Excluding the crypto losses, the operating profit increased 35.7% YoY, with an OPM of 13.2% compared to 11.4% reported a year ago. For the full-year, the company has reported a net loss of JPY20.7bn as opposed to a net profit of JPY8bn in FY12/17, blaming the crypto losses for the decline. For FY12/18, the management has proposed a dividend of JPY29.5 per share (compared to JPY23 paid in FY12/17) in spite of reporting net losses for the fiscal year. Further, the company has also allocated JPY1.36bn (equivalent to 0.7% of outstanding shares at the current price) for share repurchases in FY2019.

Excluding the Crypto Segment, GMO’s Net Profit Grew 4.1% YoY in FY12/18

JPY (bn)

FY12/17

FY12/18

YoY Change

FY12/18 Excluding Crypto

FY12/18 Excl. Crypto Vs. FY12/17

Consensus

Company Vs. Consensus

Revenue

154.3

185.2

20.1%

180.9

17.3%

183.3

1.0%

Operating Profit

17.6

21.8

23.5%

23.9

35.7%

22.8

-4.5%

OPM

11.4%

11.8%

13.2%

12.4%

Net Profit

8.0

-20.7

-357.9%

8.4

4.1%

Source: Company Disclosures, Capital IQ

GMO is currently trading at JPY1,741 per share which we believe is undervalued compared to its combined equity stake in 8 listed subsidiaries. The company share price has lost more than 40% since it peaked in June last year due to the negativity surrounding its cryptocurrency and mining segment. However, we believe further downside is limited as the company has closed down a majority of its mining related business which weighs very little on the consolidated performance of the company. Further, the company’s key businesses, Internet Infrastructure, Online Advertising & Media and Internet Finance generate solid recurring revenues, which should help the company achieve strong growth. Following its earnings announcement, the share price gained 5.6% from the previous days close.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Facebook Inc A (FB US) is a bellwether stock for the equity markets. Although the market capitalisation is approaching $475 billion, the Company is still considered a growth stock. In our view, 2019 could be a pivotal year for the Company after a lack lustre 2018, when FB, although volatile, underperformed the NASDAQ. We believe that investors are underestimating revenue growth for 2019 and that FB is likely to surprise to the upside in Q1-19.

GMO Internet, Inc. (9449 JP) announced its consolidated financial results for its full-year FY12/18 yesterday (12th February). Despite heavy losses incurred in the cryptocurrency mining business in FY12/18, GMO managed to achieve a solid year with 20% YoY growth in top-line alongside a 23.5% YoY growth in operating profits. Excluding the crypto losses, the operating profit increased 35.7% YoY, with an OPM of 13.2% compared to 11.4% reported a year ago. For the full-year, the company has reported a net loss of JPY20.7bn as opposed to a net profit of JPY8bn in FY12/17, blaming the crypto losses for the decline. For FY12/18, the management has proposed a dividend of JPY29.5 per share (compared to JPY23 paid in FY12/17) in spite of reporting net losses for the fiscal year. Further, the company has also allocated JPY1.36bn (equivalent to 0.7% of outstanding shares at the current price) for share repurchases in FY2019.

Excluding the Crypto Segment, GMO’s Net Profit Grew 4.1% YoY in FY12/18

JPY (bn)

FY12/17

FY12/18

YoY Change

FY12/18 Excluding Crypto

FY12/18 Excl. Crypto Vs. FY12/17

Consensus

Company Vs. Consensus

Revenue

154.3

185.2

20.1%

180.9

17.3%

183.3

1.0%

Operating Profit

17.6

21.8

23.5%

23.9

35.7%

22.8

-4.5%

OPM

11.4%

11.8%

13.2%

12.4%

Net Profit

8.0

-20.7

-357.9%

8.4

4.1%

Source: Company Disclosures, Capital IQ

GMO is currently trading at JPY1,741 per share which we believe is undervalued compared to its combined equity stake in 8 listed subsidiaries. The company share price has lost more than 40% since it peaked in June last year due to the negativity surrounding its cryptocurrency and mining segment. However, we believe further downside is limited as the company has closed down a majority of its mining related business which weighs very little on the consolidated performance of the company. Further, the company’s key businesses, Internet Infrastructure, Online Advertising & Media and Internet Finance generate solid recurring revenues, which should help the company achieve strong growth. Following its earnings announcement, the share price gained 5.6% from the previous days close.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Facebook Inc A (FB US) is a bellwether stock for the equity markets. Although the market capitalisation is approaching $475 billion, the Company is still considered a growth stock. In our view, 2019 could be a pivotal year for the Company after a lack lustre 2018, when FB, although volatile, underperformed the NASDAQ. We believe that investors are underestimating revenue growth for 2019 and that FB is likely to surprise to the upside in Q1-19.

GMO Internet, Inc. (9449 JP) announced its consolidated financial results for its full-year FY12/18 yesterday (12th February). Despite heavy losses incurred in the cryptocurrency mining business in FY12/18, GMO managed to achieve a solid year with 20% YoY growth in top-line alongside a 23.5% YoY growth in operating profits. Excluding the crypto losses, the operating profit increased 35.7% YoY, with an OPM of 13.2% compared to 11.4% reported a year ago. For the full-year, the company has reported a net loss of JPY20.7bn as opposed to a net profit of JPY8bn in FY12/17, blaming the crypto losses for the decline. For FY12/18, the management has proposed a dividend of JPY29.5 per share (compared to JPY23 paid in FY12/17) in spite of reporting net losses for the fiscal year. Further, the company has also allocated JPY1.36bn (equivalent to 0.7% of outstanding shares at the current price) for share repurchases in FY2019.

Excluding the Crypto Segment, GMO’s Net Profit Grew 4.1% YoY in FY12/18

JPY (bn)

FY12/17

FY12/18

YoY Change

FY12/18 Excluding Crypto

FY12/18 Excl. Crypto Vs. FY12/17

Consensus

Company Vs. Consensus

Revenue

154.3

185.2

20.1%

180.9

17.3%

183.3

1.0%

Operating Profit

17.6

21.8

23.5%

23.9

35.7%

22.8

-4.5%

OPM

11.4%

11.8%

13.2%

12.4%

Net Profit

8.0

-20.7

-357.9%

8.4

4.1%

Source: Company Disclosures, Capital IQ

GMO is currently trading at JPY1,741 per share which we believe is undervalued compared to its combined equity stake in 8 listed subsidiaries. The company share price has lost more than 40% since it peaked in June last year due to the negativity surrounding its cryptocurrency and mining segment. However, we believe further downside is limited as the company has closed down a majority of its mining related business which weighs very little on the consolidated performance of the company. Further, the company’s key businesses, Internet Infrastructure, Online Advertising & Media and Internet Finance generate solid recurring revenues, which should help the company achieve strong growth. Following its earnings announcement, the share price gained 5.6% from the previous days close.

Parco (8251 JP) is enjoying a new lease of life under J Front Retailing (3086 JP) ownership, investing assiduously in updating existing buildings and showing a decisiveness to rebuild entirely where location merits it and even closing down stores that don’t work.

It will celebrate its 50th anniversary this year by opening four new buildings, including the flagship Parco Shibuya and is forecasting a 28% rise in revenue for 2016-2021.

Fundamental trends at Hana Financial (086790 KS) are benign and stand out within South Korea’s improving and deep value banking universe. Key metrics/signal at 12M18 positive fundamental momentum and value-quality trends embodied in a high PH Score™.

Hana is an important constituent of South Korea’s Banking Sector, holding approximately 13% of the system total loans, 15% of deposits and about 40% of the nation’s trade finance due to the bank’s entrenched foreign-currency clearing system. This valuable franchise is backed by strengthening capitalisation, improving asset quality after a difficult period for banks grappling with corporate exposures, and discrete gains on Efficiency and Profitability post sizeable merger and integration costs.

Corporate governance remains an issue to monitor after the nepotism scandal of recent years and was covered by Douglas Kim last year.

Having said that, Hana is a slightly higher risk than peers with a HY profile given its default rating.

Shares of Hana are attractively priced, trading on earnings and dividend yields of 19% and 3.8%, respectively, a dividend-adjusted PEG factor of 2x, a P/B of 0.47x, and a franchise value of 5% with the tailwinds of a quintile 1 PH Score™. In line with regulatory change regarding higher DPRs, Hana will raise its dividend payout ratio to 25.5% in 2019 from 22.5% in 2018.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

As we wrote about in Preference for NTT Retained on Its Commitment to a Substantial Long Term Profit Increase, we like the long term story at NTT (Nippon Telegraph & Telephone) (9432 JP) given its relatively low payout ration, long term opportunities for cost reductions as their workforce shrinks through retirements. While government action and the announced price cuts announced by NTT Docomo Inc (9437 JP) hurt sentiment to the sector in 2H18, Chris Hoare remains positive. The recent 3Q results were decent with the key positives being a rising dividend and strong cash flow growth which is in line with our long term positive thesis on the stock. We remain Buyers with a target price of ¥7,150.

Valuetronics reported its 3Q19 figures this week which showed a 7.5% decline in revenues but a small (+2.6%) increase in bottom line profits. Stronger margins in its ICE segment offset weakness in its CE segment.

Valuetronics Holdings (VALUE SP) remains a solid company run by a good management team with interesting clients in consumer electronics and automotive. The valuation of the company is cheap (5x ex-cash 2019 P/E) and the balance sheet is rock solid.

All these positives are currently being overshadowed by the US-China trade war as the company has 100% of its production in China and does 45.7% of its sales in North-America. While many companies try to downplay the impact of the trade-war Valuetronics cannot hide and the alternatives it is working on to offset the tariff impact will surely cause short-term disruption and increased costs.

YTD the share price is +12% as the market is hoping for a positive resolution to the US-China trade war. Management is cautious on macro political improvements as trade war friction is unlikely to dissipate soon. Given the weak outlook for its CE segment and no significant new customer wins in its ICE segment risk/reward does not seem very attractive despite good dividend yield and cheap valuation.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

As we wrote about in Preference for NTT Retained on Its Commitment to a Substantial Long Term Profit Increase, we like the long term story at NTT (Nippon Telegraph & Telephone) (9432 JP) given its relatively low payout ration, long term opportunities for cost reductions as their workforce shrinks through retirements. While government action and the announced price cuts announced by NTT Docomo Inc (9437 JP) hurt sentiment to the sector in 2H18, Chris Hoare remains positive. The recent 3Q results were decent with the key positives being a rising dividend and strong cash flow growth which is in line with our long term positive thesis on the stock. We remain Buyers with a target price of ¥7,150.

Valuetronics reported its 3Q19 figures this week which showed a 7.5% decline in revenues but a small (+2.6%) increase in bottom line profits. Stronger margins in its ICE segment offset weakness in its CE segment.

Valuetronics Holdings (VALUE SP) remains a solid company run by a good management team with interesting clients in consumer electronics and automotive. The valuation of the company is cheap (5x ex-cash 2019 P/E) and the balance sheet is rock solid.

All these positives are currently being overshadowed by the US-China trade war as the company has 100% of its production in China and does 45.7% of its sales in North-America. While many companies try to downplay the impact of the trade-war Valuetronics cannot hide and the alternatives it is working on to offset the tariff impact will surely cause short-term disruption and increased costs.

YTD the share price is +12% as the market is hoping for a positive resolution to the US-China trade war. Management is cautious on macro political improvements as trade war friction is unlikely to dissipate soon. Given the weak outlook for its CE segment and no significant new customer wins in its ICE segment risk/reward does not seem very attractive despite good dividend yield and cheap valuation.

The Chinese smartphone market, which commands approximately 30.0% of the global smartphone market, experienced declining sales in 4Q2018. The Chinese smartphone market fell by 9.7% YoY in 4QFY2018 .

Meanwhile, the global smartphone market fell by 4.9% YoY in the same quarter as a result of conditions in China, longer replacement cycles and a lack of technological innovations in the industry.

Apple continued to suffer with iPhone shipments to China falling by 20.3% YoY during the last quarter.

5G compatible phones are likely to turn around industry performance, however, the introduction of such devices will most likely occur in the latter half of 2019. Apple, in question is rumoured to release their 5G compatible iPhone in 2020, later than close competitor Samsung.

Slow market conditions are likely to prevail until the next generation of communication technology becomes commercialised. Until such a time, companies such as Apple, and parts suppliers to smartphone vendors may continue to struggle with slowing performance similar to that of present. However, over the long term, companies stand to benefit once 5G is released in spite of the short term outlook not being too favourable.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.