In this briefing:

- Sing Holdings – Surge in Full-Year Earnings with a Surprise Hike in Dividend. 67% Upside. BUY.

- Naspers: Softbank Buyback a Guide for Naspers?

- What’s Down with Muji (7453 JP)?

- Komatsu, HCM, CAT: The Stock Punishment Does Not Match the Outlook Deterioration Crime

- Tencent (700 HK): In Fact Benefited from License Suspension

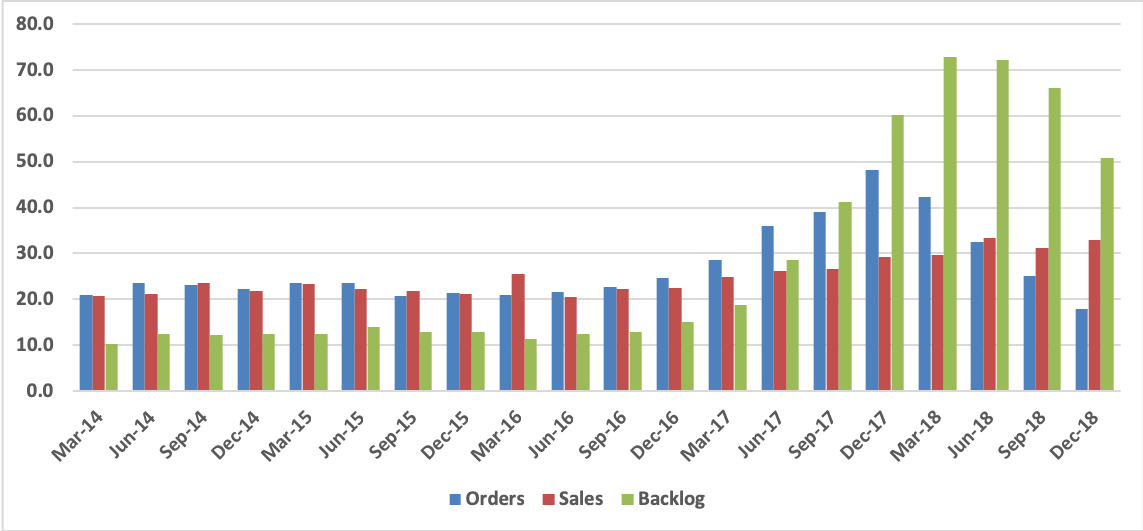

1. Sing Holdings – Surge in Full-Year Earnings with a Surprise Hike in Dividend. 67% Upside. BUY.

Sing Holdings (SING SP) announced its FY18 full-year results this evening.

Results were largely in line with expectations.

Take-up rate at Parc Botannia improved from 62% in 3Q FY19 to 66% in 4Q FY19. With the biggest agency in Singapore marketing the project, sales at Parc Botannia is expected to pick up in 2019.

A key surprise in Sing Holdings’ FY18 results was the 20% hike in its dividend to 1.2 S-cents per share in FY18.

My fair value for SHL is pegged at S$0.66 per share, implying an upside potential of 67%. I maintain my BUY recommendation on Sing Holdings Ltd.

2. Naspers: Softbank Buyback a Guide for Naspers?

Recently, Softbank’s (9984 JP) shares jumped +18% after announcing a $5.5bn share buyback. Using Smartkarma’s holdco monitor, the discount to NAV had widened to around 55% prior to the announcement but is now sitting around 40-45%. There were a few key reasons for the buyback: (1) the Softbank Corp (9434 JP) (KK) IPO netted $20bn, giving the company the flexibility to do the buyback, and (2) Softbank is taking a more disciplined approach to further platform investments.

Both these arguments are also available to Naspers (NPN SJ) management and a move to buy back 5% of market cap is feasible and we believe would narrow the discount. The question is whether management are listening. They have been dismissive of buybacks in the past but this could change.

3. What’s Down with Muji (7453 JP)?

Ryohin Keikaku (7453 JP) has downgraded full-year forecasts for its Muji retail chain but still expects record sales and solid profit growth in FY2018.

Overseas sales have been going from strength to strength, but previously stellar results at home have weakened, particularly in the home and accessories category which is under pressure from competitors, including even Nitori (9843 JP).

Muji is responding and also has big plans to grow food retailing, a big potential market.

4. Komatsu, HCM, CAT: The Stock Punishment Does Not Match the Outlook Deterioration Crime

We have been struck by the degree of underperformance of the construction machinery names despite strong earnings performance. While the cyclical nature of the names makes judging performance purely on earnings results (or even the outlook) hazardous, in this case we believe the market has been premature and excessive in its derating of these stocks which have sold off to similar levels as the WFE names such as Tokyo Electron (8035 JP) and Robotics names such as Fanuc Corp (6954 JP).

While it is possible that Komatsu Ltd (6301 JP), Hitachi Construction Machinery (6305 JP) and Caterpillar Inc (CAT US) have sold off partly due to their China exposure, it needs to be emphasised that 1) these companies are no longer heavily dependent on China and revenue exposure is 12% for HCM, 10% for CAT and 7% for Komatsu, and 2) while the Chinese market at about 60k excavators is probably close to the top of its cycle, it is not a bubble like in 2010 when it 111k units and thus a collapse in demand is unlikely (though a decline is).

As the table below notes, earnings estimates for the construction machinery companies have only tapered marginally from their peaks, and while find the forecasts for continued growth into 2020 somewhat optimistic the resilience of mining demand means we are disinclined to dismiss them out of hand. On the other hand estimates for WFE and Robot names have dropped significantly, but despite this, share price performance is similar for all three categories of stocks. We discuss this stark discrepancy further below.

Change in 2019 OP Estimate Vs. Peak | Peak OP Estimate Date | Peak to Trough Share Price Change | Share Price Vs. Peak | Peak Share Price Date | |

Caterpillar | -6.4% | Aug 18 | -35.2% | -21.4% | Jan 18 |

Komatsu | -2.1% | Dec 18 | -49.7% | -38.8% | Jan 18 |

Hitachi Construction Machinery | -4.6% | Oct 18 | -50.5% | -41.2% | Feb 18 |

Average | -4.4% | -45.1% | -33.8% | ||

ASML | -10.1% | Jan 19 | -31.2% | -14.4% | Jul 18 |

Applied Materials | -38.4% | Apr 18 | -53.2% | -36.8% | Mar 18 |

LAM Research | -28.7% | Apr 18 | -46.4% | -21.3% | Mar 18 |

Tokyo Electron | -36.6% | Jul 18 | -49.9% | -32.4% | Nov 17 |

Average | -28.5% | -45.2% | -26.2% | ||

Fanuc | -44.7% | Mar 18 | -52.9% | -42.4% | Jan 18 |

Yaskawa | -34.7% | Mar 18 | -58.5% | -47.0% | Jan 18 |

Harmonic Drive Systems | -43.2% | May 18 | -65.9% | -49.3% | Jan 18 |

Average | -40.9% | -59.1% | -46.2% |

5. Tencent (700 HK): In Fact Benefited from License Suspension

- Tencent’s market share as measured by the number of active users increased during the the period license suspension.

- We believe that Tencent’s market share as measured by active users will bring increased market share as measured by revenues.

- We also believe that during the hard times small companies always die.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.