Horiba’s share price has rebounded on FY Dec-18 results that were above management’s most recent guidance and better than we had expected. Consolidated operating profit was up 7.5% on a 7.8% increase in sales, and net profit up 37.0% following extraordinary gains (vs. losses the previous year) and a lower effective tax rate.

4Q results were weak, primarily due to the downturn in semiconductor capital spending, but this was no surprise. Total consolidated operating profit was down 10.3% year-on-year on a 2.3% increase in sales in the three months to December, while operating profit on Semiconductor Instruments & Systems (primarily mass flow controllers) was down 32.8% on a 15.8% decrease in sales.

Looking ahead, management is guiding for year-on-year declines in both sales and profits in the six months to June, again due to weak demand for semiconductor equipment, followed by a sharp rebound in 2H and low single-digit growth FY Dec-19 as a whole. Judging from the semiconductor equipment order flow, it appears that a weak 1H will be hard to avoid, while there is as yet no sign pointing to recovery. Nevertheless, we have raised our own sales and profit estimates for this fiscal year and next based on the absolute levels of orders and sales.

Automotive Test Systems and the company’s other businesses should continue to grow, supported by the acquisition of FuelCon AG of Germany (an industry leader in battery and fuel cell validation) and Manta Instruments of the U.S. (which makes nanoparticle tracking analysis systems). The issue, then, is how soon and how rapidly semiconductor related investments will recover. We suspect later and more slowly than management hopes, but in any case the downturn appears to have been discounted.

At ¥5,980 (Friday, February 15, closing price), Horiba has rebounded by 44% from its January 4 low of ¥4,155, but is still 38% below its ¥9,590 all-time high reached last May. It is now selling at 13.6x our EPS estimate for this fiscal year and 12.3x our estimate for FY Dec-20. These and other projected valuations are on the low side of their 5-year historical ranges. Once the recent bounce has been consolidated, there should be another buying opportunity for longer term investors.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this insight, we will provide an analysis of the performance of selected stocks that just joined the Stock Connect last week.

Sutl Enterprise (SUTL SP) did not grow revenues in 2018 as it continued to operate only its flagship Sentosa marina. Change is coming as it has 9 projects in the pipeline which could dramatically alter the financial future of the company by FY21.

The biggest news is the groundbreaking of Puteri Harbor in Malaysia last week. With a sales gallery opening by May 2019, it will be very interesting to follow the progress on this project and its contribution to SUTL’s top/bottom-line results in FY19/FY20.

SUTL is misunderstood by investors because management disclosure is lacking and liquidity is poor. The valuation of SUTL could be improved if investors had a better understanding of the earnings trajectory we could expect in FY19-FY21.

We realize the Tay family is not looking to sell its stake anytime soon so is not concerned about its current market cap. We caution that this might not be a smart way to run a publicly listed company as a more expensive ‘currency’ (stock price) might help the company be taken more seriously when attempting to make acquisitions overseas.

However, this does not alter the fact that 84% of the market cap is cash and the EV of this consistently profitable company is barely 6.7M USD. SUTL is undeniably one of the cheapest stocks on SGX.

ZTO Express (ZTO US)‘s earnings will fail to meet the high expectations of sell-side analysts and investors who seeit as a cheap proxy for Chinese e-commerce activity.

China’s express sector revenue grew 43.5% YoY in 2016, the year ZTO went public. Last year, revenue growth was just half that (21.8%), and we expect the sector’s growth to continue to moderate over the next few years.

The express sector is also evolving in ways that will put downward pressure on profitability and require greater investment from the express companies.

We expect the profitability of ZTO’s express business to decline in the medium-term as the company adjusts to slowing demand and emerging sector trends. Our earnings estimates, which are far below consensus figures, reflect these challenges.

ZTO suffers from declining earnings quality and two accounting issues that we feel make it a risky, unattractive investment. Our 12-month target price for ZTO is US$13.31, based on 16 times our blended 2019-20 EPS estimates. We rate the stock Sell.

In this report, we provide an analysis of our pair trade idea between Doosan Heavy Industries (034020 KS)and Doosan Corp (000150 KS). Our strategy will be to be long Doosan Heavy Industries and be short Doosan Corp. Our base case strategy is to achieve gains of 7-9% on this pair trade over the next six months.

In the past two years, Moon Jae-In administration’s energy policy has been to further reduce the reliance on nuclear power and increase reliance in renewable and coal power. The use of nuclear power in Korea is highly impacted by politics. There are a few stocks in Korea such as Doosan Heavy Industries (034020 KS) where politics is very important. The conservative parties in Korea tend to favor the use of nuclear power. However, the ruling liberal party does not favor the use of nuclear power.

Among the domestic issues, the decline in the nuclear power generation and greater use of coal based power generation have been cited as key reasons why the fine dust problems has increased in Korea in the past two years. In fact, more than 0.42 million Korean citizens have signed petitions in the past few weeks that would oppose the continued decline in the use of nuclear power generation.

Three years ago, Isetan-Mitsukoshi attempted to reverse a strategy of shifting to small format retailing.

At the same time, the department store operator made a final ditch effort to avoid closing department stores and sacked its CEO who had had the temerity to suggest closure was the only way to revive the business.

Last year new management finally realised the old CEO had been right and that culling stores was the only way to improve profit growth.

Now the company is diversifying again but, instead of just small stores, it is planning a big investment into e-commerce with a projected ¥145 billion in sales from personal styling alone.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Sutl Enterprise (SUTL SP) did not grow revenues in 2018 as it continued to operate only its flagship Sentosa marina. Change is coming as it has 9 projects in the pipeline which could dramatically alter the financial future of the company by FY21.

The biggest news is the groundbreaking of Puteri Harbor in Malaysia last week. With a sales gallery opening by May 2019, it will be very interesting to follow the progress on this project and its contribution to SUTL’s top/bottom-line results in FY19/FY20.

SUTL is misunderstood by investors because management disclosure is lacking and liquidity is poor. The valuation of SUTL could be improved if investors had a better understanding of the earnings trajectory we could expect in FY19-FY21.

We realize the Tay family is not looking to sell its stake anytime soon so is not concerned about its current market cap. We caution that this might not be a smart way to run a publicly listed company as a more expensive ‘currency’ (stock price) might help the company be taken more seriously when attempting to make acquisitions overseas.

However, this does not alter the fact that 84% of the market cap is cash and the EV of this consistently profitable company is barely 6.7M USD. SUTL is undeniably one of the cheapest stocks on SGX.

ZTO Express (ZTO US)‘s earnings will fail to meet the high expectations of sell-side analysts and investors who seeit as a cheap proxy for Chinese e-commerce activity.

China’s express sector revenue grew 43.5% YoY in 2016, the year ZTO went public. Last year, revenue growth was just half that (21.8%), and we expect the sector’s growth to continue to moderate over the next few years.

The express sector is also evolving in ways that will put downward pressure on profitability and require greater investment from the express companies.

We expect the profitability of ZTO’s express business to decline in the medium-term as the company adjusts to slowing demand and emerging sector trends. Our earnings estimates, which are far below consensus figures, reflect these challenges.

ZTO suffers from declining earnings quality and two accounting issues that we feel make it a risky, unattractive investment. Our 12-month target price for ZTO is US$13.31, based on 16 times our blended 2019-20 EPS estimates. We rate the stock Sell.

In this report, we provide an analysis of our pair trade idea between Doosan Heavy Industries (034020 KS)and Doosan Corp (000150 KS). Our strategy will be to be long Doosan Heavy Industries and be short Doosan Corp. Our base case strategy is to achieve gains of 7-9% on this pair trade over the next six months.

In the past two years, Moon Jae-In administration’s energy policy has been to further reduce the reliance on nuclear power and increase reliance in renewable and coal power. The use of nuclear power in Korea is highly impacted by politics. There are a few stocks in Korea such as Doosan Heavy Industries (034020 KS) where politics is very important. The conservative parties in Korea tend to favor the use of nuclear power. However, the ruling liberal party does not favor the use of nuclear power.

Among the domestic issues, the decline in the nuclear power generation and greater use of coal based power generation have been cited as key reasons why the fine dust problems has increased in Korea in the past two years. In fact, more than 0.42 million Korean citizens have signed petitions in the past few weeks that would oppose the continued decline in the use of nuclear power generation.

Three years ago, Isetan-Mitsukoshi attempted to reverse a strategy of shifting to small format retailing.

At the same time, the department store operator made a final ditch effort to avoid closing department stores and sacked its CEO who had had the temerity to suggest closure was the only way to revive the business.

Last year new management finally realised the old CEO had been right and that culling stores was the only way to improve profit growth.

Now the company is diversifying again but, instead of just small stores, it is planning a big investment into e-commerce with a projected ¥145 billion in sales from personal styling alone.

In this series under Smartkarma Originals, CrossASEAN insight providers AngusMackintosh and Jessica Irene seek to determine whether or not we are close to the end of the rainbow and to a period of outperformance for the property sector. Our end conclusions will be based on a series of company visits to the major listed property companies in Indonesia, conversations with local banks, property agents, and other relevant channel checks.

The fourth company that we explore is township developer Alam Sutera Realty (ASRI IJ), which provides an interesting exposure to a mix of landed housing, high-rise and low-rise condominiums through its Alam Sutera Township near Serpong and its Pasir Kemis township 15 km further out on the toll road.

Given the diminishing area of high-value land bank in Alam Sutera, the company has shifted emphasis towards selling low-rise condominiums and commercial lots for shop houses, which has been a success story.

Alam Sutera Realty (ASRI IJ) also has a contract with a Chinese developer, China Fortune Land Development (CFLD), to develop a total of 500 ha over a five year period in its Pasir Kamis Township. This has provided a fillip for the company during a quiet period of marketing sales and will continue to underpin earnings for the next 2 years.

The company stands to benefit from the completion of two new toll-roads, one soon to be completed to the south connecting directly to BSD City and longer term a new toll to Soekarno Hatta Airport to the north.

It will start to utilise new land bank in North Serpong in 2021, which will extend the development potential in the area significantly longer-term.

Management is optimistic about marketing sales for 2019 and expects growth of +16% versus last year’s number, which already exceeded expectations.

Alam Sutera Realty (ASRI IJ) has less recurrent income than peers at around 10% of total revenue but has the potential to see better contributions from the Garuda Wisnu Kencana Cultural Centre (GWK) in Bali.

The new regulations on the booking of sales financed by mortgages introduced in August 2018 will benefit Alam Sutera Realty (ASRI IJ) from a cash flow perspective. Given that the company is consistently producing free cash flow, this is also a strong deleveraging story.

One of the biggest risks for the company is its US$ debt, which totals US$480m and is made up of two bonds expiring in 2020 and 2022.

From a valuation perspective, Alam Sutera Realty (ASRI IJ) looks very interesting, trading on 4.9x FY19E PER, at 0.67x PBV, and at a 71% discount to NAV. On all three measures, at 1 STD below its historical mean. Our target price of IDR600 takes a blended approach, based on the company trading at historical mean on all three measures implies upside of 91% from current levels. Catalysts include better marketing sales from its low-rise developments at its Alam Sutera township and further cluster sales there, a pick-up in sales and pricing at its Pasir Kemis township, a sale of its office inventory at The Tower, a pick up in recurrent income driven by improving tenant mix at GWK. Given that the company has high levels of US$ debt, a stable currency will also benefit the company. A more dovish outlook on interest rates will also be a positive, given a large and rising portion of buyers use a mortgage to buy its properties.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The company’s flagship Star Vegas casino resort was victimized by an alleged diversion of VIP players by its contract management. Now under corporate control it is beginning to recover.

Its US$124m breech of contract claim against the vendor was filed in there Singapore court system and sits at final appeal stage.

Cambodia’s new gaming regulation law will stabilize and eliminate wild west dimension of Poipet casinos. This could lead to major earnings gains and increased investment going forward.

Musashino Bank (8336 JP) was one of the last regional banks to announce 3Q FY3/2019 results, and they were a nasty surprise: a consolidated net loss for the nine months to 31 December 2018, caused by heavy reserving in Q3 (October-December 2018) against the bank’s exposure to the troubled Akebono Brake Industry Co (7238 JP) . While the bank has slashed its full-year net profit guidance from ¥11.1 billion to ¥4.5 billion, this would still require an heroic level of profits in Q4 which the bank has never before achieved. The share price has fallen over 31% in the last twelve months. Valuations at current levels are still high (FY3/2019 PER is 17.6x) and we consider the share price to be vulnerable to further weakness. Caveat emptor (May the buyer beware) !

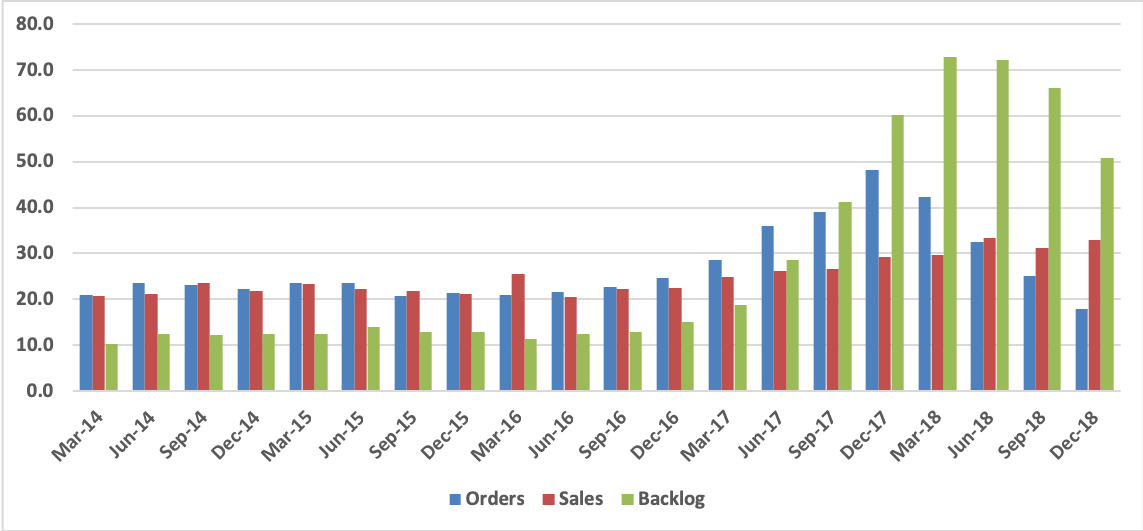

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Horiba’s share price has rebounded on FY Dec-18 results that were above management’s most recent guidance and better than we had expected. Consolidated operating profit was up 7.5% on a 7.8% increase in sales, and net profit up 37.0% following extraordinary gains (vs. losses the previous year) and a lower effective tax rate.

4Q results were weak, primarily due to the downturn in semiconductor capital spending, but this was no surprise. Total consolidated operating profit was down 10.3% year-on-year on a 2.3% increase in sales in the three months to December, while operating profit on Semiconductor Instruments & Systems (primarily mass flow controllers) was down 32.8% on a 15.8% decrease in sales.

Looking ahead, management is guiding for year-on-year declines in both sales and profits in the six months to June, again due to weak demand for semiconductor equipment, followed by a sharp rebound in 2H and low single-digit growth FY Dec-19 as a whole. Judging from the semiconductor equipment order flow, it appears that a weak 1H will be hard to avoid, while there is as yet no sign pointing to recovery. Nevertheless, we have raised our own sales and profit estimates for this fiscal year and next based on the absolute levels of orders and sales.

Automotive Test Systems and the company’s other businesses should continue to grow, supported by the acquisition of FuelCon AG of Germany (an industry leader in battery and fuel cell validation) and Manta Instruments of the U.S. (which makes nanoparticle tracking analysis systems). The issue, then, is how soon and how rapidly semiconductor related investments will recover. We suspect later and more slowly than management hopes, but in any case the downturn appears to have been discounted.

At ¥5,980 (Friday, February 15, closing price), Horiba has rebounded by 44% from its January 4 low of ¥4,155, but is still 38% below its ¥9,590 all-time high reached last May. It is now selling at 13.6x our EPS estimate for this fiscal year and 12.3x our estimate for FY Dec-20. These and other projected valuations are on the low side of their 5-year historical ranges. Once the recent bounce has been consolidated, there should be another buying opportunity for longer term investors.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

ZTO Express (ZTO US)‘s earnings will fail to meet the high expectations of sell-side analysts and investors who seeit as a cheap proxy for Chinese e-commerce activity.

China’s express sector revenue grew 43.5% YoY in 2016, the year ZTO went public. Last year, revenue growth was just half that (21.8%), and we expect the sector’s growth to continue to moderate over the next few years.

The express sector is also evolving in ways that will put downward pressure on profitability and require greater investment from the express companies.

We expect the profitability of ZTO’s express business to decline in the medium-term as the company adjusts to slowing demand and emerging sector trends. Our earnings estimates, which are far below consensus figures, reflect these challenges.

ZTO suffers from declining earnings quality and two accounting issues that we feel make it a risky, unattractive investment. Our 12-month target price for ZTO is US$13.31, based on 16 times our blended 2019-20 EPS estimates. We rate the stock Sell.

In this report, we provide an analysis of our pair trade idea between Doosan Heavy Industries (034020 KS)and Doosan Corp (000150 KS). Our strategy will be to be long Doosan Heavy Industries and be short Doosan Corp. Our base case strategy is to achieve gains of 7-9% on this pair trade over the next six months.

In the past two years, Moon Jae-In administration’s energy policy has been to further reduce the reliance on nuclear power and increase reliance in renewable and coal power. The use of nuclear power in Korea is highly impacted by politics. There are a few stocks in Korea such as Doosan Heavy Industries (034020 KS) where politics is very important. The conservative parties in Korea tend to favor the use of nuclear power. However, the ruling liberal party does not favor the use of nuclear power.

Among the domestic issues, the decline in the nuclear power generation and greater use of coal based power generation have been cited as key reasons why the fine dust problems has increased in Korea in the past two years. In fact, more than 0.42 million Korean citizens have signed petitions in the past few weeks that would oppose the continued decline in the use of nuclear power generation.

Three years ago, Isetan-Mitsukoshi attempted to reverse a strategy of shifting to small format retailing.

At the same time, the department store operator made a final ditch effort to avoid closing department stores and sacked its CEO who had had the temerity to suggest closure was the only way to revive the business.

Last year new management finally realised the old CEO had been right and that culling stores was the only way to improve profit growth.

Now the company is diversifying again but, instead of just small stores, it is planning a big investment into e-commerce with a projected ¥145 billion in sales from personal styling alone.

In this series under Smartkarma Originals, CrossASEAN insight providers AngusMackintosh and Jessica Irene seek to determine whether or not we are close to the end of the rainbow and to a period of outperformance for the property sector. Our end conclusions will be based on a series of company visits to the major listed property companies in Indonesia, conversations with local banks, property agents, and other relevant channel checks.

The fourth company that we explore is township developer Alam Sutera Realty (ASRI IJ), which provides an interesting exposure to a mix of landed housing, high-rise and low-rise condominiums through its Alam Sutera Township near Serpong and its Pasir Kemis township 15 km further out on the toll road.

Given the diminishing area of high-value land bank in Alam Sutera, the company has shifted emphasis towards selling low-rise condominiums and commercial lots for shop houses, which has been a success story.

Alam Sutera Realty (ASRI IJ) also has a contract with a Chinese developer, China Fortune Land Development (CFLD), to develop a total of 500 ha over a five year period in its Pasir Kamis Township. This has provided a fillip for the company during a quiet period of marketing sales and will continue to underpin earnings for the next 2 years.

The company stands to benefit from the completion of two new toll-roads, one soon to be completed to the south connecting directly to BSD City and longer term a new toll to Soekarno Hatta Airport to the north.

It will start to utilise new land bank in North Serpong in 2021, which will extend the development potential in the area significantly longer-term.

Management is optimistic about marketing sales for 2019 and expects growth of +16% versus last year’s number, which already exceeded expectations.

Alam Sutera Realty (ASRI IJ) has less recurrent income than peers at around 10% of total revenue but has the potential to see better contributions from the Garuda Wisnu Kencana Cultural Centre (GWK) in Bali.

The new regulations on the booking of sales financed by mortgages introduced in August 2018 will benefit Alam Sutera Realty (ASRI IJ) from a cash flow perspective. Given that the company is consistently producing free cash flow, this is also a strong deleveraging story.

One of the biggest risks for the company is its US$ debt, which totals US$480m and is made up of two bonds expiring in 2020 and 2022.

From a valuation perspective, Alam Sutera Realty (ASRI IJ) looks very interesting, trading on 4.9x FY19E PER, at 0.67x PBV, and at a 71% discount to NAV. On all three measures, at 1 STD below its historical mean. Our target price of IDR600 takes a blended approach, based on the company trading at historical mean on all three measures implies upside of 91% from current levels. Catalysts include better marketing sales from its low-rise developments at its Alam Sutera township and further cluster sales there, a pick-up in sales and pricing at its Pasir Kemis township, a sale of its office inventory at The Tower, a pick up in recurrent income driven by improving tenant mix at GWK. Given that the company has high levels of US$ debt, a stable currency will also benefit the company. A more dovish outlook on interest rates will also be a positive, given a large and rising portion of buyers use a mortgage to buy its properties.

We met NTT Docomo Inc (9437 JP) today for a quick chat. Markets are focused on FY19 guidance and the magnitude of price reductions that DoCoMo plans, neither of which were on the table for discussion. We did get a little bit of color on the Q4 competitive environment (not too intense), the mobile payments effort (strategically important but less need to invest heavily like PayPay) and the impending sale of its 34% stake in Sumitomo Mitsui Card.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We cut our target price by 22% to Bt24.7 to factor in disappointing 2018 result. However, we maintain our BUY rating on the back of positive outlook toward its new products and market expansion plan.

The story:

Posted net profit of Bt50m in 4Q18, down 36%YoY and 25%QoQ

Trimmed 2019-21E forecast by 23.8%-24.3% respectively

Expanding strategic partnership

Our new target price of Bt24.7 is based on a target PE’19E of 18.8x which is equivalent to the World’s consumer staples sector.

The discount and variety retailer just opened its fourth store in South-East Asia, mixing Japanese restaurants and cafes with a Donki store and a range of Japanese speciality tenants. The store has all the high-level retail entertainment that its Japanese stores offer but with the added cachet of being from Japan and mixing in a lot more in-mall tenants and food outlets. PPI now plans 200 overseas stores in the medium-term.

Back home, PPI is creating new small store formats which have the potential to reach into parts of Japan its big box stores cannot.

At the same time, PPI is beginning the conversion of 100 Uny stores to mixed food and variety stores. With the first six conversions showing sales growth of 83% over 10 months and gross margins up 59%, PPI’s expectation of an extra ¥20 billion in operating profit once conversions are complete looks very achievable.

The takeover means PPI is now Japan’s fourth-biggest retailer, up from 15th just three years ago.

These multiple ventures reflect the company’s flexibility, adapting to each local market’s needs with formats to match.

Its recent decision to close down its e-commerce business is not a weakness but a positive move, demonstrating that PPI understands where its strengths lie: in live store entertainment.

Eurobank Ergasias Sa (EUROB GA) FY18 results were satisfactory. The bank is now weaned off ELA, pays a tax rate of 33% for the first time in many years, generates robust deposit inflows, enhancing the liquidity position, and is actively reducing NPEs. Management foresees the current problem loan ratio at 37.1% easing to 16% in 2019 and 9% by 2021. Problem exposures will be slashed by €10bn in 2019 through securitizations, collateral liquidations, sales, recoveries and charge-offs. Recent data show a much more benign situation regarding negative NPE formation. The worst seems to be behind the Greek Banking System, barring some external global or regional event or domestic policy misstep.

The legal framework for banks has improved with the Katseli Law providing lenders with greater protection for recovering mortgage NPE foreclosures in the event of default on restructured loans. The real estate auction system has also been gaining much greater traction.

Eurobank is engaged in a corporate transformation plan in order to unlock value, improve capitalisation, and manage NPEs. The plan revolves around a merger with Grivalia, “Pillar” (€2bn mortgage NPE securitization), “Cairo” (€7.5bn multi-asset securitization), the creation of a loan servicer, and a hive down. The bank will focus on core banking rather than functioning as a distressed real estate asset manager.

The outlook for the Greek economy has improved somewhat. The 2019 Budget is based on a primary surplus target of 3.5% of GDP. Exports and private consumption are drivers for solid growth of around 2%. The cash buffer of at least EUR26.5 bn is equivalent to 2 years of gross financing needs. Moody’s raised Greece’s issuer rating to B1 from B3 and its outlook to stable from positive (Feb19). The sovereign gained market access with recent 5year €2.5bn and 10year €2.5bn issues. A tailwind will be the resurgence of “animal spirits” under a New Democracy administration after elections later this year.

Eurobank trades at a P/Book of 0.4x (European median is 0.8x) and a franchise valuation of 4% (European median of 12%). We believe these valuations are quite attractive in the grand scheme of things, especially given the progress underway on reduction of NPEs, the elimination of ELA, and the deposit inflow position. A caveat remains the reduction in SH Funds and the subsequent increase in Debt/Equity. While the PH Score™ is no more than average, we are encouraged by positive trends regarding asset quality improvement, an expanding NIM, enhanced liquidity, and efficiency gains. This is a fair Score at a compelling valuation- whatever metric you choose to use.

Underlying profitability continues to deteriorate at Vodafone Idea (IDEA IN) (IDEA). Chris Hoare has updated his liquidity analysis, and estimates that IDEA needs prices to rise by over 50% to hit cash flow break-even in the medium term. That needs market behavior to change from Jio in particular. Bulls will point to IDEA’s current capital raising and the large capital raising planned at Bharti Airtel (BHARTI IN) as signalling a possible end to hostilities. However, the math at IDEA is such that even a $3.5bn injection gives only temporary relief. What they really need are price increases. Without them (and even with the capital increase), Chris thinks IDEA runs out of cash in about 2 years. We retain our Reduce recommendation and cut our price target to INR16.

SamE shocked the market with 4Q results. OP was down nearly 30% YoY and even 20% from the already heavily adjusted street consensus of ₩13.4tril. The main reason was Amazon’s canceled order. Amazon canceled a significant portion of memory chips, mostly DRAM to be used in its IDCs.

The market guessed that Amazon might have delayed purchase to further capitalize on falling prices. But Amazon had canceled DRAM order because there were fundamental flaws in SamE’s custom DRAM chips at chip design level.

The street was expecting a bounce back for memory chip ASP in 2H this year. SamE’s technical issue may push it back further. Meanwhile, SamE’s next quarterly profit level can be even worse. Some in the local street already adjusted SamE’s 1Q OP down to slightly above ₩7tril. At this level, SamE’s FY19e PER would be at 11~12x. This is a very aggressive territory for SamE.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In this report, we provide an analysis of our pair trade idea between Doosan Heavy Industries (034020 KS)and Doosan Corp (000150 KS). Our strategy will be to be long Doosan Heavy Industries and be short Doosan Corp. Our base case strategy is to achieve gains of 7-9% on this pair trade over the next six months.

In the past two years, Moon Jae-In administration’s energy policy has been to further reduce the reliance on nuclear power and increase reliance in renewable and coal power. The use of nuclear power in Korea is highly impacted by politics. There are a few stocks in Korea such as Doosan Heavy Industries (034020 KS) where politics is very important. The conservative parties in Korea tend to favor the use of nuclear power. However, the ruling liberal party does not favor the use of nuclear power.

Among the domestic issues, the decline in the nuclear power generation and greater use of coal based power generation have been cited as key reasons why the fine dust problems has increased in Korea in the past two years. In fact, more than 0.42 million Korean citizens have signed petitions in the past few weeks that would oppose the continued decline in the use of nuclear power generation.

Three years ago, Isetan-Mitsukoshi attempted to reverse a strategy of shifting to small format retailing.

At the same time, the department store operator made a final ditch effort to avoid closing department stores and sacked its CEO who had had the temerity to suggest closure was the only way to revive the business.

Last year new management finally realised the old CEO had been right and that culling stores was the only way to improve profit growth.

Now the company is diversifying again but, instead of just small stores, it is planning a big investment into e-commerce with a projected ¥145 billion in sales from personal styling alone.

In this series under Smartkarma Originals, CrossASEAN insight providers AngusMackintosh and Jessica Irene seek to determine whether or not we are close to the end of the rainbow and to a period of outperformance for the property sector. Our end conclusions will be based on a series of company visits to the major listed property companies in Indonesia, conversations with local banks, property agents, and other relevant channel checks.

The fourth company that we explore is township developer Alam Sutera Realty (ASRI IJ), which provides an interesting exposure to a mix of landed housing, high-rise and low-rise condominiums through its Alam Sutera Township near Serpong and its Pasir Kemis township 15 km further out on the toll road.

Given the diminishing area of high-value land bank in Alam Sutera, the company has shifted emphasis towards selling low-rise condominiums and commercial lots for shop houses, which has been a success story.

Alam Sutera Realty (ASRI IJ) also has a contract with a Chinese developer, China Fortune Land Development (CFLD), to develop a total of 500 ha over a five year period in its Pasir Kamis Township. This has provided a fillip for the company during a quiet period of marketing sales and will continue to underpin earnings for the next 2 years.

The company stands to benefit from the completion of two new toll-roads, one soon to be completed to the south connecting directly to BSD City and longer term a new toll to Soekarno Hatta Airport to the north.

It will start to utilise new land bank in North Serpong in 2021, which will extend the development potential in the area significantly longer-term.

Management is optimistic about marketing sales for 2019 and expects growth of +16% versus last year’s number, which already exceeded expectations.

Alam Sutera Realty (ASRI IJ) has less recurrent income than peers at around 10% of total revenue but has the potential to see better contributions from the Garuda Wisnu Kencana Cultural Centre (GWK) in Bali.

The new regulations on the booking of sales financed by mortgages introduced in August 2018 will benefit Alam Sutera Realty (ASRI IJ) from a cash flow perspective. Given that the company is consistently producing free cash flow, this is also a strong deleveraging story.

One of the biggest risks for the company is its US$ debt, which totals US$480m and is made up of two bonds expiring in 2020 and 2022.

From a valuation perspective, Alam Sutera Realty (ASRI IJ) looks very interesting, trading on 4.9x FY19E PER, at 0.67x PBV, and at a 71% discount to NAV. On all three measures, at 1 STD below its historical mean. Our target price of IDR600 takes a blended approach, based on the company trading at historical mean on all three measures implies upside of 91% from current levels. Catalysts include better marketing sales from its low-rise developments at its Alam Sutera township and further cluster sales there, a pick-up in sales and pricing at its Pasir Kemis township, a sale of its office inventory at The Tower, a pick up in recurrent income driven by improving tenant mix at GWK. Given that the company has high levels of US$ debt, a stable currency will also benefit the company. A more dovish outlook on interest rates will also be a positive, given a large and rising portion of buyers use a mortgage to buy its properties.

We met NTT Docomo Inc (9437 JP) today for a quick chat. Markets are focused on FY19 guidance and the magnitude of price reductions that DoCoMo plans, neither of which were on the table for discussion. We did get a little bit of color on the Q4 competitive environment (not too intense), the mobile payments effort (strategically important but less need to invest heavily like PayPay) and the impending sale of its 34% stake in Sumitomo Mitsui Card.

We recently met with Yahoo Japan (4689 JP) for an update on the company after Q3 results. We thought the financial announcement was positive with encouraging forecasts for profitability, both this year and going forward, and revenue growth potential. In addition, Yahoo Japan reported solid customer growth for mobile payments joint venture PayPay, driven by strong marketing support and an attractive proposition for offline merchants. We think the latter is very important for the development of mobile payments in Japan and PayPay has had a robust start.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Three years ago, Isetan-Mitsukoshi attempted to reverse a strategy of shifting to small format retailing.

At the same time, the department store operator made a final ditch effort to avoid closing department stores and sacked its CEO who had had the temerity to suggest closure was the only way to revive the business.

Last year new management finally realised the old CEO had been right and that culling stores was the only way to improve profit growth.

Now the company is diversifying again but, instead of just small stores, it is planning a big investment into e-commerce with a projected ¥145 billion in sales from personal styling alone.

In this series under Smartkarma Originals, CrossASEAN insight providers AngusMackintosh and Jessica Irene seek to determine whether or not we are close to the end of the rainbow and to a period of outperformance for the property sector. Our end conclusions will be based on a series of company visits to the major listed property companies in Indonesia, conversations with local banks, property agents, and other relevant channel checks.

The fourth company that we explore is township developer Alam Sutera Realty (ASRI IJ), which provides an interesting exposure to a mix of landed housing, high-rise and low-rise condominiums through its Alam Sutera Township near Serpong and its Pasir Kemis township 15 km further out on the toll road.

Given the diminishing area of high-value land bank in Alam Sutera, the company has shifted emphasis towards selling low-rise condominiums and commercial lots for shop houses, which has been a success story.

Alam Sutera Realty (ASRI IJ) also has a contract with a Chinese developer, China Fortune Land Development (CFLD), to develop a total of 500 ha over a five year period in its Pasir Kamis Township. This has provided a fillip for the company during a quiet period of marketing sales and will continue to underpin earnings for the next 2 years.

The company stands to benefit from the completion of two new toll-roads, one soon to be completed to the south connecting directly to BSD City and longer term a new toll to Soekarno Hatta Airport to the north.

It will start to utilise new land bank in North Serpong in 2021, which will extend the development potential in the area significantly longer-term.

Management is optimistic about marketing sales for 2019 and expects growth of +16% versus last year’s number, which already exceeded expectations.

Alam Sutera Realty (ASRI IJ) has less recurrent income than peers at around 10% of total revenue but has the potential to see better contributions from the Garuda Wisnu Kencana Cultural Centre (GWK) in Bali.

The new regulations on the booking of sales financed by mortgages introduced in August 2018 will benefit Alam Sutera Realty (ASRI IJ) from a cash flow perspective. Given that the company is consistently producing free cash flow, this is also a strong deleveraging story.

One of the biggest risks for the company is its US$ debt, which totals US$480m and is made up of two bonds expiring in 2020 and 2022.

From a valuation perspective, Alam Sutera Realty (ASRI IJ) looks very interesting, trading on 4.9x FY19E PER, at 0.67x PBV, and at a 71% discount to NAV. On all three measures, at 1 STD below its historical mean. Our target price of IDR600 takes a blended approach, based on the company trading at historical mean on all three measures implies upside of 91% from current levels. Catalysts include better marketing sales from its low-rise developments at its Alam Sutera township and further cluster sales there, a pick-up in sales and pricing at its Pasir Kemis township, a sale of its office inventory at The Tower, a pick up in recurrent income driven by improving tenant mix at GWK. Given that the company has high levels of US$ debt, a stable currency will also benefit the company. A more dovish outlook on interest rates will also be a positive, given a large and rising portion of buyers use a mortgage to buy its properties.

We met NTT Docomo Inc (9437 JP) today for a quick chat. Markets are focused on FY19 guidance and the magnitude of price reductions that DoCoMo plans, neither of which were on the table for discussion. We did get a little bit of color on the Q4 competitive environment (not too intense), the mobile payments effort (strategically important but less need to invest heavily like PayPay) and the impending sale of its 34% stake in Sumitomo Mitsui Card.

We recently met with Yahoo Japan (4689 JP) for an update on the company after Q3 results. We thought the financial announcement was positive with encouraging forecasts for profitability, both this year and going forward, and revenue growth potential. In addition, Yahoo Japan reported solid customer growth for mobile payments joint venture PayPay, driven by strong marketing support and an attractive proposition for offline merchants. We think the latter is very important for the development of mobile payments in Japan and PayPay has had a robust start.

We cut our target price by 22% to Bt24.7 to factor in disappointing 2018 result. However, we maintain our BUY rating on the back of positive outlook toward its new products and market expansion plan.

The story:

Posted net profit of Bt50m in 4Q18, down 36%YoY and 25%QoQ

Trimmed 2019-21E forecast by 23.8%-24.3% respectively

Expanding strategic partnership

Our new target price of Bt24.7 is based on a target PE’19E of 18.8x which is equivalent to the World’s consumer staples sector.

Risks: (1) Fluctuations in raw material prices

(2) Exchange rate fluctuations

(3) Highly competitive industry

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In this series under Smartkarma Originals, CrossASEAN insight providers AngusMackintosh and Jessica Irene seek to determine whether or not we are close to the end of the rainbow and to a period of outperformance for the property sector. Our end conclusions will be based on a series of company visits to the major listed property companies in Indonesia, conversations with local banks, property agents, and other relevant channel checks.

The fourth company that we explore is township developer Alam Sutera Realty (ASRI IJ), which provides an interesting exposure to a mix of landed housing, high-rise and low-rise condominiums through its Alam Sutera Township near Serpong and its Pasir Kemis township 15 km further out on the toll road.

Given the diminishing area of high-value land bank in Alam Sutera, the company has shifted emphasis towards selling low-rise condominiums and commercial lots for shop houses, which has been a success story.

Alam Sutera Realty (ASRI IJ) also has a contract with a Chinese developer, China Fortune Land Development (CFLD), to develop a total of 500 ha over a five year period in its Pasir Kamis Township. This has provided a fillip for the company during a quiet period of marketing sales and will continue to underpin earnings for the next 2 years.

The company stands to benefit from the completion of two new toll-roads, one soon to be completed to the south connecting directly to BSD City and longer term a new toll to Soekarno Hatta Airport to the north.

It will start to utilise new land bank in North Serpong in 2021, which will extend the development potential in the area significantly longer-term.

Management is optimistic about marketing sales for 2019 and expects growth of +16% versus last year’s number, which already exceeded expectations.

Alam Sutera Realty (ASRI IJ) has less recurrent income than peers at around 10% of total revenue but has the potential to see better contributions from the Garuda Wisnu Kencana Cultural Centre (GWK) in Bali.

The new regulations on the booking of sales financed by mortgages introduced in August 2018 will benefit Alam Sutera Realty (ASRI IJ) from a cash flow perspective. Given that the company is consistently producing free cash flow, this is also a strong deleveraging story.

One of the biggest risks for the company is its US$ debt, which totals US$480m and is made up of two bonds expiring in 2020 and 2022.

From a valuation perspective, Alam Sutera Realty (ASRI IJ) looks very interesting, trading on 4.9x FY19E PER, at 0.67x PBV, and at a 71% discount to NAV. On all three measures, at 1 STD below its historical mean. Our target price of IDR600 takes a blended approach, based on the company trading at historical mean on all three measures implies upside of 91% from current levels. Catalysts include better marketing sales from its low-rise developments at its Alam Sutera township and further cluster sales there, a pick-up in sales and pricing at its Pasir Kemis township, a sale of its office inventory at The Tower, a pick up in recurrent income driven by improving tenant mix at GWK. Given that the company has high levels of US$ debt, a stable currency will also benefit the company. A more dovish outlook on interest rates will also be a positive, given a large and rising portion of buyers use a mortgage to buy its properties.

We met NTT Docomo Inc (9437 JP) today for a quick chat. Markets are focused on FY19 guidance and the magnitude of price reductions that DoCoMo plans, neither of which were on the table for discussion. We did get a little bit of color on the Q4 competitive environment (not too intense), the mobile payments effort (strategically important but less need to invest heavily like PayPay) and the impending sale of its 34% stake in Sumitomo Mitsui Card.

We recently met with Yahoo Japan (4689 JP) for an update on the company after Q3 results. We thought the financial announcement was positive with encouraging forecasts for profitability, both this year and going forward, and revenue growth potential. In addition, Yahoo Japan reported solid customer growth for mobile payments joint venture PayPay, driven by strong marketing support and an attractive proposition for offline merchants. We think the latter is very important for the development of mobile payments in Japan and PayPay has had a robust start.

We cut our target price by 22% to Bt24.7 to factor in disappointing 2018 result. However, we maintain our BUY rating on the back of positive outlook toward its new products and market expansion plan.

The story:

Posted net profit of Bt50m in 4Q18, down 36%YoY and 25%QoQ

Trimmed 2019-21E forecast by 23.8%-24.3% respectively

Expanding strategic partnership

Our new target price of Bt24.7 is based on a target PE’19E of 18.8x which is equivalent to the World’s consumer staples sector.

The discount and variety retailer just opened its fourth store in South-East Asia, mixing Japanese restaurants and cafes with a Donki store and a range of Japanese speciality tenants. The store has all the high-level retail entertainment that its Japanese stores offer but with the added cachet of being from Japan and mixing in a lot more in-mall tenants and food outlets. PPI now plans 200 overseas stores in the medium-term.

Back home, PPI is creating new small store formats which have the potential to reach into parts of Japan its big box stores cannot.

At the same time, PPI is beginning the conversion of 100 Uny stores to mixed food and variety stores. With the first six conversions showing sales growth of 83% over 10 months and gross margins up 59%, PPI’s expectation of an extra ¥20 billion in operating profit once conversions are complete looks very achievable.

The takeover means PPI is now Japan’s fourth-biggest retailer, up from 15th just three years ago.

These multiple ventures reflect the company’s flexibility, adapting to each local market’s needs with formats to match.

Its recent decision to close down its e-commerce business is not a weakness but a positive move, demonstrating that PPI understands where its strengths lie: in live store entertainment.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We met NTT Docomo Inc (9437 JP) today for a quick chat. Markets are focused on FY19 guidance and the magnitude of price reductions that DoCoMo plans, neither of which were on the table for discussion. We did get a little bit of color on the Q4 competitive environment (not too intense), the mobile payments effort (strategically important but less need to invest heavily like PayPay) and the impending sale of its 34% stake in Sumitomo Mitsui Card.

We recently met with Yahoo Japan (4689 JP) for an update on the company after Q3 results. We thought the financial announcement was positive with encouraging forecasts for profitability, both this year and going forward, and revenue growth potential. In addition, Yahoo Japan reported solid customer growth for mobile payments joint venture PayPay, driven by strong marketing support and an attractive proposition for offline merchants. We think the latter is very important for the development of mobile payments in Japan and PayPay has had a robust start.

We cut our target price by 22% to Bt24.7 to factor in disappointing 2018 result. However, we maintain our BUY rating on the back of positive outlook toward its new products and market expansion plan.

The story:

Posted net profit of Bt50m in 4Q18, down 36%YoY and 25%QoQ

Trimmed 2019-21E forecast by 23.8%-24.3% respectively

Expanding strategic partnership

Our new target price of Bt24.7 is based on a target PE’19E of 18.8x which is equivalent to the World’s consumer staples sector.

The discount and variety retailer just opened its fourth store in South-East Asia, mixing Japanese restaurants and cafes with a Donki store and a range of Japanese speciality tenants. The store has all the high-level retail entertainment that its Japanese stores offer but with the added cachet of being from Japan and mixing in a lot more in-mall tenants and food outlets. PPI now plans 200 overseas stores in the medium-term.

Back home, PPI is creating new small store formats which have the potential to reach into parts of Japan its big box stores cannot.

At the same time, PPI is beginning the conversion of 100 Uny stores to mixed food and variety stores. With the first six conversions showing sales growth of 83% over 10 months and gross margins up 59%, PPI’s expectation of an extra ¥20 billion in operating profit once conversions are complete looks very achievable.

The takeover means PPI is now Japan’s fourth-biggest retailer, up from 15th just three years ago.

These multiple ventures reflect the company’s flexibility, adapting to each local market’s needs with formats to match.

Its recent decision to close down its e-commerce business is not a weakness but a positive move, demonstrating that PPI understands where its strengths lie: in live store entertainment.

Eurobank Ergasias Sa (EUROB GA) FY18 results were satisfactory. The bank is now weaned off ELA, pays a tax rate of 33% for the first time in many years, generates robust deposit inflows, enhancing the liquidity position, and is actively reducing NPEs. Management foresees the current problem loan ratio at 37.1% easing to 16% in 2019 and 9% by 2021. Problem exposures will be slashed by €10bn in 2019 through securitizations, collateral liquidations, sales, recoveries and charge-offs. Recent data show a much more benign situation regarding negative NPE formation. The worst seems to be behind the Greek Banking System, barring some external global or regional event or domestic policy misstep.

The legal framework for banks has improved with the Katseli Law providing lenders with greater protection for recovering mortgage NPE foreclosures in the event of default on restructured loans. The real estate auction system has also been gaining much greater traction.

Eurobank is engaged in a corporate transformation plan in order to unlock value, improve capitalisation, and manage NPEs. The plan revolves around a merger with Grivalia, “Pillar” (€2bn mortgage NPE securitization), “Cairo” (€7.5bn multi-asset securitization), the creation of a loan servicer, and a hive down. The bank will focus on core banking rather than functioning as a distressed real estate asset manager.

The outlook for the Greek economy has improved somewhat. The 2019 Budget is based on a primary surplus target of 3.5% of GDP. Exports and private consumption are drivers for solid growth of around 2%. The cash buffer of at least EUR26.5 bn is equivalent to 2 years of gross financing needs. Moody’s raised Greece’s issuer rating to B1 from B3 and its outlook to stable from positive (Feb19). The sovereign gained market access with recent 5year €2.5bn and 10year €2.5bn issues. A tailwind will be the resurgence of “animal spirits” under a New Democracy administration after elections later this year.

Eurobank trades at a P/Book of 0.4x (European median is 0.8x) and a franchise valuation of 4% (European median of 12%). We believe these valuations are quite attractive in the grand scheme of things, especially given the progress underway on reduction of NPEs, the elimination of ELA, and the deposit inflow position. A caveat remains the reduction in SH Funds and the subsequent increase in Debt/Equity. While the PH Score™ is no more than average, we are encouraged by positive trends regarding asset quality improvement, an expanding NIM, enhanced liquidity, and efficiency gains. This is a fair Score at a compelling valuation- whatever metric you choose to use.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.