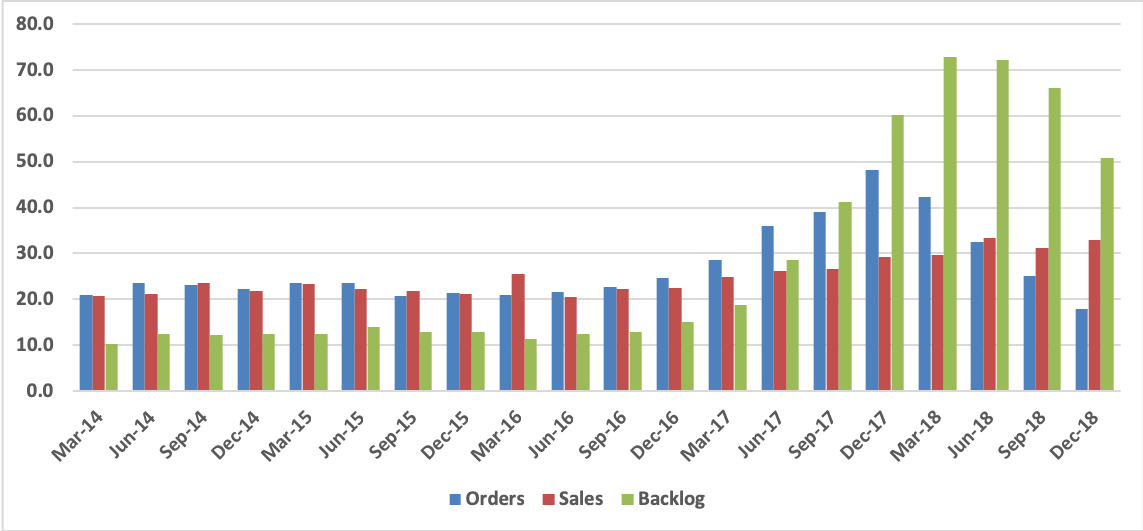

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

It has taken some time, but finally Philippine National Bank (PNB PM) is being recognized by the market. To us though, this is only the beginning. The story with PNB has for a long time been about a turnaround, moving from a sleepy state-owned bank focused on large corporate loans and with a high level of bad loans, to a more invigorated bank with far better credit quality and a new focus on the consumer. The recent milestone of paying a special dividend was a clear sign of how the bank improved since the Asian Financial Crisis (AFC). The market is now awakening to what a new CEO can do with PNB and one who comes from HSBC Philippines. Still PNB’s market capitalization is only 9% of assets compared with 14-20% for the largest three peer banks. There appears a lot more to come.

We met up with management of two companies whose industries couldn’t have been more different. This is the quick run-down on what they are up to recently:

After You posted 14% earnings growth on the back of 20% revenue growth. While this remains healthy, it realizes that domestic market opportunities will become more limited and has started to look abroad with HK as its first market.

Locally, the desserts leader is still planning a slew of new products and some in exclusive partnerships with various airlines such as Air Asia and Thai Smile.

In an effort to reduce storefront expenses, they will start selling certain products outside stores and even online, now 3% of total sales.

Amata’s earnings crashed 28% in 2018 on the back of 2% revenue decline, as Vietnam retroactively forbid certain land sales and even fines the company for past transactions that abided with the law back then!

Grifols SA (GRF SM) and Shanghai RAAS Blood Products Co Ltd (002252.SZ) recently announced an asset exchange that effectively combines the companies’ blood products operations in China. This transaction marks the third investment (two are cross-border) into the industry in the last two years. Despite some challenges arising from recent healthcare reforms, the industry has favorable supply/demand dynamics and high barriers to entry. US-listed China Biologic Products (CBPO US) trades at a significant discount to the implied private market values, but requires patience as management adjusts to the new operating environment.

Given overhang risk, investors have been bailing out of Woori or taking short positions. Woori Bank Employees Stock Ownership Association seems to have absorbed part of the selling from the likes of Blackrock, Samsung Asset, SEB Investment, Northern Trust, State Street, Russell Investment, and JP Morgan Asset. We do note though that Vanguard and TIAA have increased their position during the HoldCo transition.

We delve into the latest financials of Woori Financial Group. The picture is mixed. While efficiency advances were the main positive standout, we highlight sharply higher funding costs and a build-up of precautionary loans as main areas of concern. The bottom line was also boosted by much lower loan loss provisions as headline NPLs fell.

A constructive view of the Group is thus based on the credibility of what appears to be underlying asset improvement and the benefits of returning to HoldCo status.

We conclude that despite the overhang risk, shares are not expensive. Shares inhabit the highest decile of our global VFM (Valuation, Fundamentals, Momentum) rankings. There may though be a better entry point for bargain hunters.

On March 11’th 2019, Nvidia announced the acquisition of market leading high-speed interconnect company Mellanox for $6.9 billion in an all-cash deal. At first blush, the benefits touted by both companies and accepted by most commentators make sense and the deal will be immediately accretive to both EPS and revenues upon closing according to NVIDIA.

However, the clear and present threat to NVIDIA’s future success has little to do with interconnect technologies. Rather, it is the competitive challenge to their GPU solutions for data center acceleration from a broad spectrum of alternatives from the likes of Alphabet, Baidu, Intel, Xilinx, Advanced Micro Devices etc, not to mention the host of custom-ASIC accelerator startups poised to launch their products this year. The acquisition of Mellanox will do nothing to address this situation and we see it as being a distraction from where the company really needs to be focusing.

It will serve one purpose though, as a BandAid to mask the otherwise inevitable decline in its data center revenue growth in the face of ever-increasing competition.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Silverlake Axis (SILV SP) published 2Q19 results which again confirmed that the long-anticipated rise in revenues (+20% YoY) and profits (+99% YoY) has finally arrived. After three years of stagnation, this is the second quarter in a row that real earnings growth is visible.

YTD the share price of SILV has run by approximately 31% as we saw some larger volume spikes earlier this year which indicate that HNA is now finally off the register as a significant shareholder. Since HNA’s stake had dropped below 5% the new buyer has not had to step forward and disclose its identity.

Importantly, management believes the first half of FY19 was just the beginning of a new 3-year growth cycle and prospects are looking good for both FY2019 (ends June 2019) and FY2020 (ends June 2020). Dividends will continue but might be tempered depending on the number of acquisitions that are made.

Risk-Reward is not as attractive as early November but continues to look solid at these levels with a total return of 20% still achievable (assuming mid-point of historical P/E range) or a total return of 60% (assuming high-end of historical P/E range).

The company’s flagship Star Vegas casino resort was victimized by an alleged diversion of VIP players by its contract management. Now under corporate control it is beginning to recover.

Its US$124m breech of contract claim against the vendor was filed in there Singapore court system and sits at final appeal stage.

Cambodia’s new gaming regulation law will stabilize and eliminate wild west dimension of Poipet casinos. This could lead to major earnings gains and increased investment going forward.

Musashino Bank (8336 JP) was one of the last regional banks to announce 3Q FY3/2019 results, and they were a nasty surprise: a consolidated net loss for the nine months to 31 December 2018, caused by heavy reserving in Q3 (October-December 2018) against the bank’s exposure to the troubled Akebono Brake Industry Co (7238 JP) . While the bank has slashed its full-year net profit guidance from ¥11.1 billion to ¥4.5 billion, this would still require an heroic level of profits in Q4 which the bank has never before achieved. The share price has fallen over 31% in the last twelve months. Valuations at current levels are still high (FY3/2019 PER is 17.6x) and we consider the share price to be vulnerable to further weakness. Caveat emptor (May the buyer beware) !

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We met up with management of two companies whose industries couldn’t have been more different. This is the quick run-down on what they are up to recently:

After You posted 14% earnings growth on the back of 20% revenue growth. While this remains healthy, it realizes that domestic market opportunities will become more limited and has started to look abroad with HK as its first market.

Locally, the desserts leader is still planning a slew of new products and some in exclusive partnerships with various airlines such as Air Asia and Thai Smile.

In an effort to reduce storefront expenses, they will start selling certain products outside stores and even online, now 3% of total sales.

Amata’s earnings crashed 28% in 2018 on the back of 2% revenue decline, as Vietnam retroactively forbid certain land sales and even fines the company for past transactions that abided with the law back then!

Grifols SA (GRF SM) and Shanghai RAAS Blood Products Co Ltd (002252.SZ) recently announced an asset exchange that effectively combines the companies’ blood products operations in China. This transaction marks the third investment (two are cross-border) into the industry in the last two years. Despite some challenges arising from recent healthcare reforms, the industry has favorable supply/demand dynamics and high barriers to entry. US-listed China Biologic Products (CBPO US) trades at a significant discount to the implied private market values, but requires patience as management adjusts to the new operating environment.

Given overhang risk, investors have been bailing out of Woori or taking short positions. Woori Bank Employees Stock Ownership Association seems to have absorbed part of the selling from the likes of Blackrock, Samsung Asset, SEB Investment, Northern Trust, State Street, Russell Investment, and JP Morgan Asset. We do note though that Vanguard and TIAA have increased their position during the HoldCo transition.

We delve into the latest financials of Woori Financial Group. The picture is mixed. While efficiency advances were the main positive standout, we highlight sharply higher funding costs and a build-up of precautionary loans as main areas of concern. The bottom line was also boosted by much lower loan loss provisions as headline NPLs fell.

A constructive view of the Group is thus based on the credibility of what appears to be underlying asset improvement and the benefits of returning to HoldCo status.

We conclude that despite the overhang risk, shares are not expensive. Shares inhabit the highest decile of our global VFM (Valuation, Fundamentals, Momentum) rankings. There may though be a better entry point for bargain hunters.

On March 11’th 2019, Nvidia announced the acquisition of market leading high-speed interconnect company Mellanox for $6.9 billion in an all-cash deal. At first blush, the benefits touted by both companies and accepted by most commentators make sense and the deal will be immediately accretive to both EPS and revenues upon closing according to NVIDIA.

However, the clear and present threat to NVIDIA’s future success has little to do with interconnect technologies. Rather, it is the competitive challenge to their GPU solutions for data center acceleration from a broad spectrum of alternatives from the likes of Alphabet, Baidu, Intel, Xilinx, Advanced Micro Devices etc, not to mention the host of custom-ASIC accelerator startups poised to launch their products this year. The acquisition of Mellanox will do nothing to address this situation and we see it as being a distraction from where the company really needs to be focusing.

It will serve one purpose though, as a BandAid to mask the otherwise inevitable decline in its data center revenue growth in the face of ever-increasing competition.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this insight, we will provide an analysis of the performance of selected stocks that just joined the Stock Connect last week.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The company’s flagship Star Vegas casino resort was victimized by an alleged diversion of VIP players by its contract management. Now under corporate control it is beginning to recover.

Its US$124m breech of contract claim against the vendor was filed in there Singapore court system and sits at final appeal stage.

Cambodia’s new gaming regulation law will stabilize and eliminate wild west dimension of Poipet casinos. This could lead to major earnings gains and increased investment going forward.

Musashino Bank (8336 JP) was one of the last regional banks to announce 3Q FY3/2019 results, and they were a nasty surprise: a consolidated net loss for the nine months to 31 December 2018, caused by heavy reserving in Q3 (October-December 2018) against the bank’s exposure to the troubled Akebono Brake Industry Co (7238 JP) . While the bank has slashed its full-year net profit guidance from ¥11.1 billion to ¥4.5 billion, this would still require an heroic level of profits in Q4 which the bank has never before achieved. The share price has fallen over 31% in the last twelve months. Valuations at current levels are still high (FY3/2019 PER is 17.6x) and we consider the share price to be vulnerable to further weakness. Caveat emptor (May the buyer beware) !

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Grifols SA (GRF SM) and Shanghai RAAS Blood Products Co Ltd (002252.SZ) recently announced an asset exchange that effectively combines the companies’ blood products operations in China. This transaction marks the third investment (two are cross-border) into the industry in the last two years. Despite some challenges arising from recent healthcare reforms, the industry has favorable supply/demand dynamics and high barriers to entry. US-listed China Biologic Products (CBPO US) trades at a significant discount to the implied private market values, but requires patience as management adjusts to the new operating environment.

Given overhang risk, investors have been bailing out of Woori or taking short positions. Woori Bank Employees Stock Ownership Association seems to have absorbed part of the selling from the likes of Blackrock, Samsung Asset, SEB Investment, Northern Trust, State Street, Russell Investment, and JP Morgan Asset. We do note though that Vanguard and TIAA have increased their position during the HoldCo transition.

We delve into the latest financials of Woori Financial Group. The picture is mixed. While efficiency advances were the main positive standout, we highlight sharply higher funding costs and a build-up of precautionary loans as main areas of concern. The bottom line was also boosted by much lower loan loss provisions as headline NPLs fell.

A constructive view of the Group is thus based on the credibility of what appears to be underlying asset improvement and the benefits of returning to HoldCo status.

We conclude that despite the overhang risk, shares are not expensive. Shares inhabit the highest decile of our global VFM (Valuation, Fundamentals, Momentum) rankings. There may though be a better entry point for bargain hunters.

On March 11’th 2019, Nvidia announced the acquisition of market leading high-speed interconnect company Mellanox for $6.9 billion in an all-cash deal. At first blush, the benefits touted by both companies and accepted by most commentators make sense and the deal will be immediately accretive to both EPS and revenues upon closing according to NVIDIA.

However, the clear and present threat to NVIDIA’s future success has little to do with interconnect technologies. Rather, it is the competitive challenge to their GPU solutions for data center acceleration from a broad spectrum of alternatives from the likes of Alphabet, Baidu, Intel, Xilinx, Advanced Micro Devices etc, not to mention the host of custom-ASIC accelerator startups poised to launch their products this year. The acquisition of Mellanox will do nothing to address this situation and we see it as being a distraction from where the company really needs to be focusing.

It will serve one purpose though, as a BandAid to mask the otherwise inevitable decline in its data center revenue growth in the face of ever-increasing competition.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this insight, we will provide an analysis of the performance of selected stocks that just joined the Stock Connect last week.

Sutl Enterprise (SUTL SP) did not grow revenues in 2018 as it continued to operate only its flagship Sentosa marina. Change is coming as it has 9 projects in the pipeline which could dramatically alter the financial future of the company by FY21.

The biggest news is the groundbreaking of Puteri Harbor in Malaysia last week. With a sales gallery opening by May 2019, it will be very interesting to follow the progress on this project and its contribution to SUTL’s top/bottom-line results in FY19/FY20.

SUTL is misunderstood by investors because management disclosure is lacking and liquidity is poor. The valuation of SUTL could be improved if investors had a better understanding of the earnings trajectory we could expect in FY19-FY21.

We realize the Tay family is not looking to sell its stake anytime soon so is not concerned about its current market cap. We caution that this might not be a smart way to run a publicly listed company as a more expensive ‘currency’ (stock price) might help the company be taken more seriously when attempting to make acquisitions overseas.

However, this does not alter the fact that 84% of the market cap is cash and the EV of this consistently profitable company is barely 6.7M USD. SUTL is undeniably one of the cheapest stocks on SGX.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Given overhang risk, investors have been bailing out of Woori or taking short positions. Woori Bank Employees Stock Ownership Association seems to have absorbed part of the selling from the likes of Blackrock, Samsung Asset, SEB Investment, Northern Trust, State Street, Russell Investment, and JP Morgan Asset. We do note though that Vanguard and TIAA have increased their position during the HoldCo transition.

We delve into the latest financials of Woori Financial Group. The picture is mixed. While efficiency advances were the main positive standout, we highlight sharply higher funding costs and a build-up of precautionary loans as main areas of concern. The bottom line was also boosted by much lower loan loss provisions as headline NPLs fell.

A constructive view of the Group is thus based on the credibility of what appears to be underlying asset improvement and the benefits of returning to HoldCo status.

We conclude that despite the overhang risk, shares are not expensive. Shares inhabit the highest decile of our global VFM (Valuation, Fundamentals, Momentum) rankings. There may though be a better entry point for bargain hunters.

On March 11’th 2019, Nvidia announced the acquisition of market leading high-speed interconnect company Mellanox for $6.9 billion in an all-cash deal. At first blush, the benefits touted by both companies and accepted by most commentators make sense and the deal will be immediately accretive to both EPS and revenues upon closing according to NVIDIA.

However, the clear and present threat to NVIDIA’s future success has little to do with interconnect technologies. Rather, it is the competitive challenge to their GPU solutions for data center acceleration from a broad spectrum of alternatives from the likes of Alphabet, Baidu, Intel, Xilinx, Advanced Micro Devices etc, not to mention the host of custom-ASIC accelerator startups poised to launch their products this year. The acquisition of Mellanox will do nothing to address this situation and we see it as being a distraction from where the company really needs to be focusing.

It will serve one purpose though, as a BandAid to mask the otherwise inevitable decline in its data center revenue growth in the face of ever-increasing competition.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this insight, we will provide an analysis of the performance of selected stocks that just joined the Stock Connect last week.

Sutl Enterprise (SUTL SP) did not grow revenues in 2018 as it continued to operate only its flagship Sentosa marina. Change is coming as it has 9 projects in the pipeline which could dramatically alter the financial future of the company by FY21.

The biggest news is the groundbreaking of Puteri Harbor in Malaysia last week. With a sales gallery opening by May 2019, it will be very interesting to follow the progress on this project and its contribution to SUTL’s top/bottom-line results in FY19/FY20.

SUTL is misunderstood by investors because management disclosure is lacking and liquidity is poor. The valuation of SUTL could be improved if investors had a better understanding of the earnings trajectory we could expect in FY19-FY21.

We realize the Tay family is not looking to sell its stake anytime soon so is not concerned about its current market cap. We caution that this might not be a smart way to run a publicly listed company as a more expensive ‘currency’ (stock price) might help the company be taken more seriously when attempting to make acquisitions overseas.

However, this does not alter the fact that 84% of the market cap is cash and the EV of this consistently profitable company is barely 6.7M USD. SUTL is undeniably one of the cheapest stocks on SGX.

ZTO Express (ZTO US)‘s earnings will fail to meet the high expectations of sell-side analysts and investors who seeit as a cheap proxy for Chinese e-commerce activity.

China’s express sector revenue grew 43.5% YoY in 2016, the year ZTO went public. Last year, revenue growth was just half that (21.8%), and we expect the sector’s growth to continue to moderate over the next few years.

The express sector is also evolving in ways that will put downward pressure on profitability and require greater investment from the express companies.

We expect the profitability of ZTO’s express business to decline in the medium-term as the company adjusts to slowing demand and emerging sector trends. Our earnings estimates, which are far below consensus figures, reflect these challenges.

ZTO suffers from declining earnings quality and two accounting issues that we feel make it a risky, unattractive investment. Our 12-month target price for ZTO is US$13.31, based on 16 times our blended 2019-20 EPS estimates. We rate the stock Sell.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Musashino Bank (8336 JP) was one of the last regional banks to announce 3Q FY3/2019 results, and they were a nasty surprise: a consolidated net loss for the nine months to 31 December 2018, caused by heavy reserving in Q3 (October-December 2018) against the bank’s exposure to the troubled Akebono Brake Industry Co (7238 JP) . While the bank has slashed its full-year net profit guidance from ¥11.1 billion to ¥4.5 billion, this would still require an heroic level of profits in Q4 which the bank has never before achieved. The share price has fallen over 31% in the last twelve months. Valuations at current levels are still high (FY3/2019 PER is 17.6x) and we consider the share price to be vulnerable to further weakness. Caveat emptor (May the buyer beware) !

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

On March 11’th 2019, Nvidia announced the acquisition of market leading high-speed interconnect company Mellanox for $6.9 billion in an all-cash deal. At first blush, the benefits touted by both companies and accepted by most commentators make sense and the deal will be immediately accretive to both EPS and revenues upon closing according to NVIDIA.

However, the clear and present threat to NVIDIA’s future success has little to do with interconnect technologies. Rather, it is the competitive challenge to their GPU solutions for data center acceleration from a broad spectrum of alternatives from the likes of Alphabet, Baidu, Intel, Xilinx, Advanced Micro Devices etc, not to mention the host of custom-ASIC accelerator startups poised to launch their products this year. The acquisition of Mellanox will do nothing to address this situation and we see it as being a distraction from where the company really needs to be focusing.

It will serve one purpose though, as a BandAid to mask the otherwise inevitable decline in its data center revenue growth in the face of ever-increasing competition.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this insight, we will provide an analysis of the performance of selected stocks that just joined the Stock Connect last week.

Sutl Enterprise (SUTL SP) did not grow revenues in 2018 as it continued to operate only its flagship Sentosa marina. Change is coming as it has 9 projects in the pipeline which could dramatically alter the financial future of the company by FY21.

The biggest news is the groundbreaking of Puteri Harbor in Malaysia last week. With a sales gallery opening by May 2019, it will be very interesting to follow the progress on this project and its contribution to SUTL’s top/bottom-line results in FY19/FY20.

SUTL is misunderstood by investors because management disclosure is lacking and liquidity is poor. The valuation of SUTL could be improved if investors had a better understanding of the earnings trajectory we could expect in FY19-FY21.

We realize the Tay family is not looking to sell its stake anytime soon so is not concerned about its current market cap. We caution that this might not be a smart way to run a publicly listed company as a more expensive ‘currency’ (stock price) might help the company be taken more seriously when attempting to make acquisitions overseas.

However, this does not alter the fact that 84% of the market cap is cash and the EV of this consistently profitable company is barely 6.7M USD. SUTL is undeniably one of the cheapest stocks on SGX.

ZTO Express (ZTO US)‘s earnings will fail to meet the high expectations of sell-side analysts and investors who seeit as a cheap proxy for Chinese e-commerce activity.

China’s express sector revenue grew 43.5% YoY in 2016, the year ZTO went public. Last year, revenue growth was just half that (21.8%), and we expect the sector’s growth to continue to moderate over the next few years.

The express sector is also evolving in ways that will put downward pressure on profitability and require greater investment from the express companies.

We expect the profitability of ZTO’s express business to decline in the medium-term as the company adjusts to slowing demand and emerging sector trends. Our earnings estimates, which are far below consensus figures, reflect these challenges.

ZTO suffers from declining earnings quality and two accounting issues that we feel make it a risky, unattractive investment. Our 12-month target price for ZTO is US$13.31, based on 16 times our blended 2019-20 EPS estimates. We rate the stock Sell.

In this report, we provide an analysis of our pair trade idea between Doosan Heavy Industries (034020 KS)and Doosan Corp (000150 KS). Our strategy will be to be long Doosan Heavy Industries and be short Doosan Corp. Our base case strategy is to achieve gains of 7-9% on this pair trade over the next six months.

In the past two years, Moon Jae-In administration’s energy policy has been to further reduce the reliance on nuclear power and increase reliance in renewable and coal power. The use of nuclear power in Korea is highly impacted by politics. There are a few stocks in Korea such as Doosan Heavy Industries (034020 KS) where politics is very important. The conservative parties in Korea tend to favor the use of nuclear power. However, the ruling liberal party does not favor the use of nuclear power.

Among the domestic issues, the decline in the nuclear power generation and greater use of coal based power generation have been cited as key reasons why the fine dust problems has increased in Korea in the past two years. In fact, more than 0.42 million Korean citizens have signed petitions in the past few weeks that would oppose the continued decline in the use of nuclear power generation.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Horiba’s share price has rebounded on FY Dec-18 results that were above management’s most recent guidance and better than we had expected. Consolidated operating profit was up 7.5% on a 7.8% increase in sales, and net profit up 37.0% following extraordinary gains (vs. losses the previous year) and a lower effective tax rate.

4Q results were weak, primarily due to the downturn in semiconductor capital spending, but this was no surprise. Total consolidated operating profit was down 10.3% year-on-year on a 2.3% increase in sales in the three months to December, while operating profit on Semiconductor Instruments & Systems (primarily mass flow controllers) was down 32.8% on a 15.8% decrease in sales.

Looking ahead, management is guiding for year-on-year declines in both sales and profits in the six months to June, again due to weak demand for semiconductor equipment, followed by a sharp rebound in 2H and low single-digit growth FY Dec-19 as a whole. Judging from the semiconductor equipment order flow, it appears that a weak 1H will be hard to avoid, while there is as yet no sign pointing to recovery. Nevertheless, we have raised our own sales and profit estimates for this fiscal year and next based on the absolute levels of orders and sales.

Automotive Test Systems and the company’s other businesses should continue to grow, supported by the acquisition of FuelCon AG of Germany (an industry leader in battery and fuel cell validation) and Manta Instruments of the U.S. (which makes nanoparticle tracking analysis systems). The issue, then, is how soon and how rapidly semiconductor related investments will recover. We suspect later and more slowly than management hopes, but in any case the downturn appears to have been discounted.

At ¥5,980 (Friday, February 15, closing price), Horiba has rebounded by 44% from its January 4 low of ¥4,155, but is still 38% below its ¥9,590 all-time high reached last May. It is now selling at 13.6x our EPS estimate for this fiscal year and 12.3x our estimate for FY Dec-20. These and other projected valuations are on the low side of their 5-year historical ranges. Once the recent bounce has been consolidated, there should be another buying opportunity for longer term investors.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.